Inside STRC’s drop: Stress test for Strategy’s Bitcoin funding engine

A record low in Strategy's preferred stock has sparked intense debate about whether the company's funding model is dragging down Bitcoin. But not everyone is worried. Here's a look at the mechanics behind the decline and the levers still available to the company.

TL;DR

- STRC is Strategy's income-focused preferred stock, designed to turn investor demand for yield into new Bitcoin purchases.

- The recent sell-off reflects concerns over dividends, cash reserves, and capital management — not a collapse of the underlying funding model.

- Unlike MSTR, STRC aims to trade close to its $100 par value, with Strategy adjusting dividends and share issuance to help keep it there.

- Strategy has responded with a broader capital management overhaul, including higher dividends, larger cash reserves, share buybacks, and a new Bitcoin monetization program.

- The biggest risk isn't the recent 32 BTC sale — it's whether Strategy can continue raising capital while maintaining confidence in its preferred-share ecosystem.

Strategy and STRC

STRC ("Stretch") is a perpetual preferred stock that provides indirect, income-generating exposure to Bitcoin. It is designed to turn investor demand for yield into structural buying pressure for the leading cryptocurrency.

In simple terms, preferred shares are debt-like instruments that remain part of the company's equity, meaning Strategy never has to repay them because they have no maturity date. The firm also cannot default on STRC in the same way it can on traditional debt.

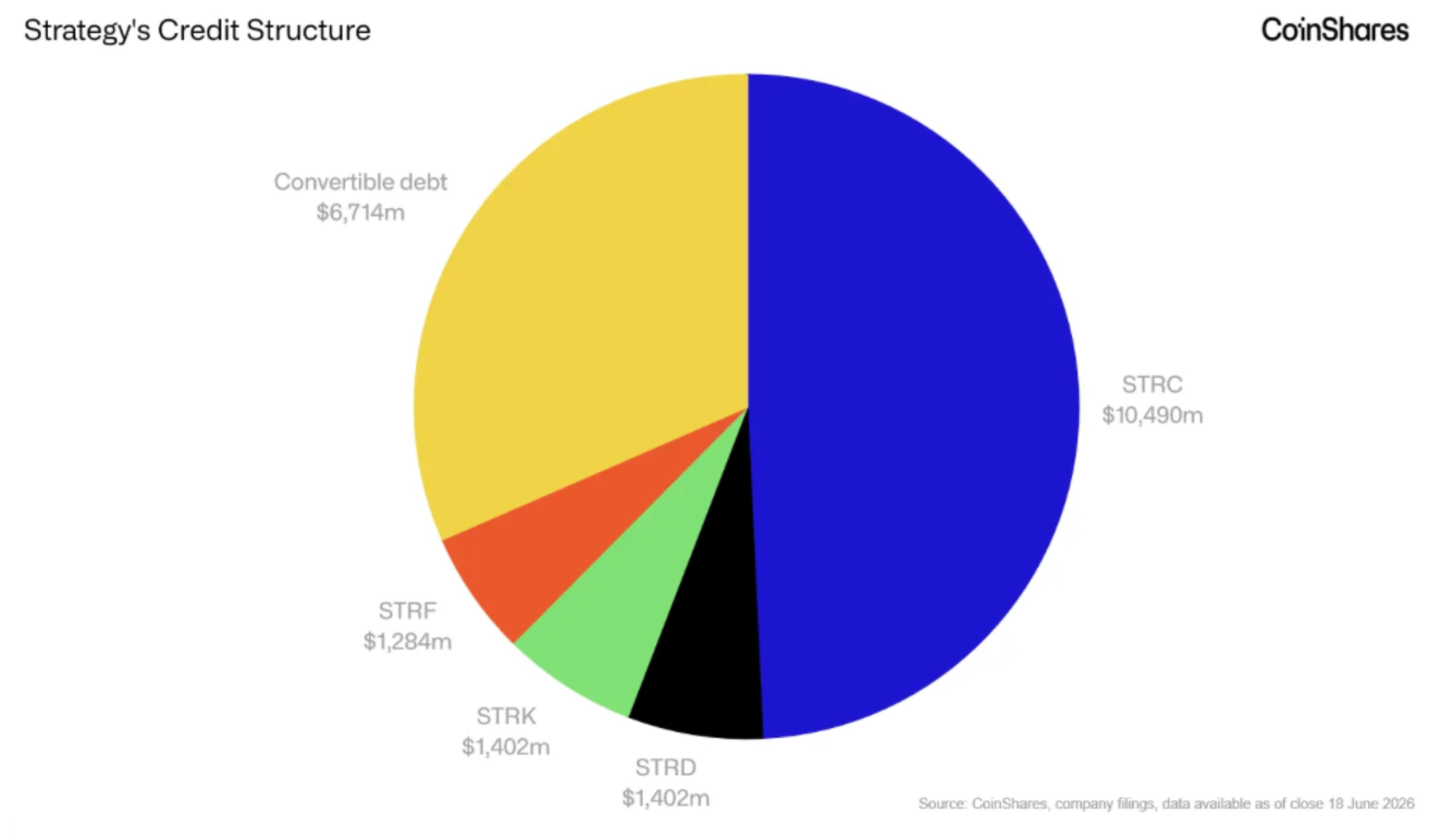

STRC is the fifth type of preferred share issued by Strategy, joining STRF, STRK, STRD, and STRE. As the name suggests, preferred shares have priority over common stock. In the event of bankruptcy, preferred shareholders are paid before common shareholders.

Here's how it works:

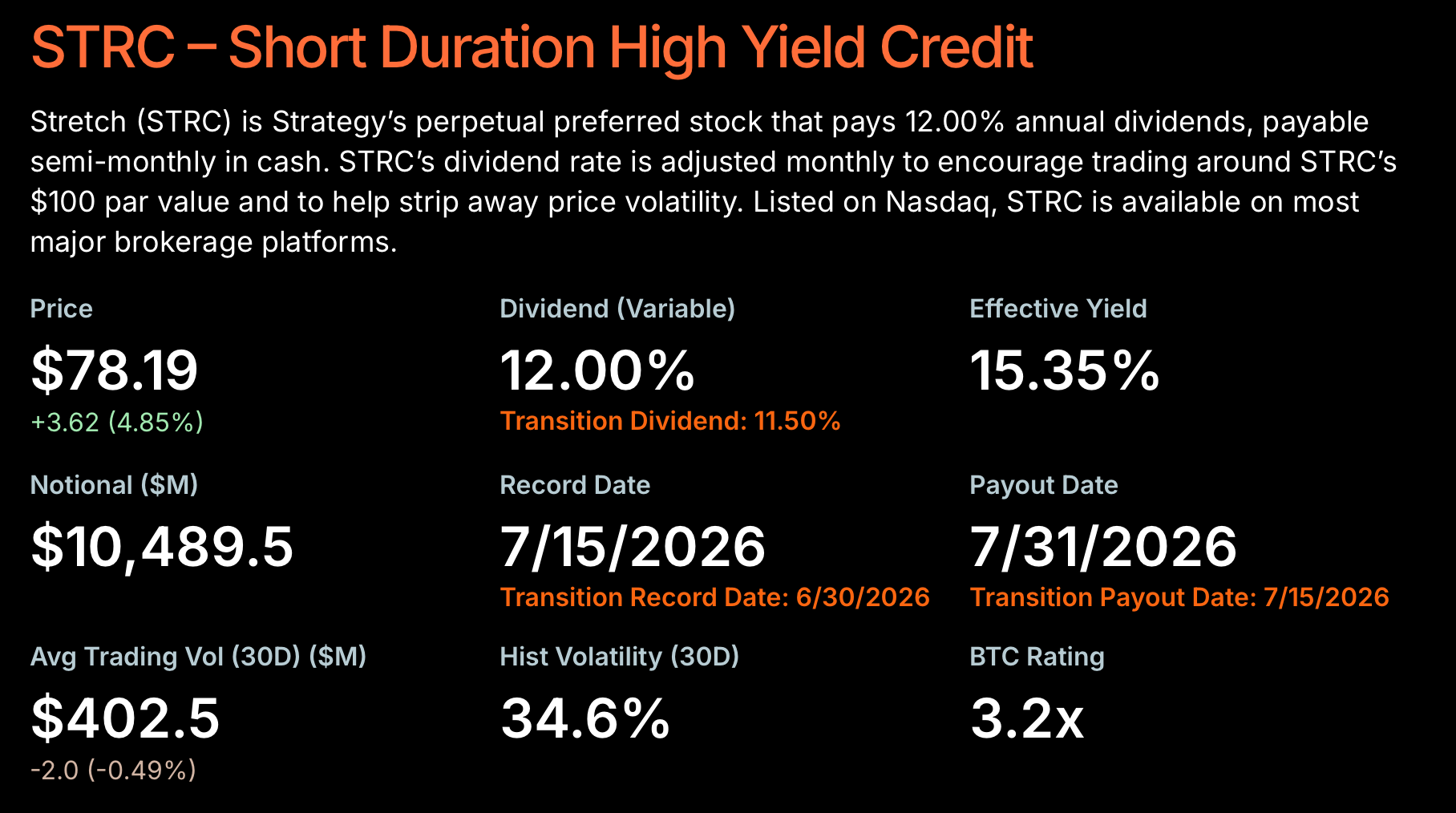

- Classified as short-duration high-yield credit, STRC functions separately from the company's common stock (MSTR) to avoid dilution.

- Proceeds from STRC sales fund new Bitcoin purchases, helping expand the firm's treasury.

- While currently trading at $74.57, STRC is designed to trade as close as possible to its $100 par value, ideally within a range of $99–$100.

- Compared with common stock, STRC offers lower historical 30-day volatility — currently, 34.6% vs. MSTR's 74%.

- STRC pays an annual dividend (11.50% at press time; 12% starting from July 1), distributed semi-monthly in cash.

Why did Strategy launch STRC?

Strategy uses STRC to fund Bitcoin acquisitions while reducing its reliance on common-share dilution and traditional convertible debt. While providing indirect BTC exposure, it also appeals to more conservative, yield-seeking investors expecting steady cash dividends.

This product achieves three core goals for the biggest corporate Bitcoin holder:

- Funding BTC purchases, creating a flywheel that steadily grows the collateral base behind the company's shares.

- Democratizing yield by allowing a broader range of investors to access double-digit dividend payments.

- Stabilizing capital strategy through an adjustable dividend that Strategy can tweak to keep the stock trading near its $100 par value.

Strategy has two main ways to influence the share price:

- If STRC trades above par, Strategy can effectively cap the upside by issuing additional shares at $100 through its at-the-market (ATM) program. Alternatively, it can redeem the shares at $101, removing the incentive to pay a premium.

- If STRC falls too far below its target range, Strategy can support demand by increasing the dividend rate.

How does STRC fuel Bitcoin buying?

STRC is designed to convert investor demand for stable yield into buying pressure for Bitcoin.

The company only sells newly issued STRC shares at exactly $100 — never below. So whenever the stock trades around par, part of the trading volume reflects Strategy issuing fresh shares to meet excess demand.

The ratio between STRC trading volume and the size of the ATM issuance varies. For illustration, assume it equals 40%. That means:

- Strategy issues new STRC equal to 40% of that day's trading volume. On a $100 million volume day, that would amount to $40 million of newly issued STRC.

- The proceeds are immediately used to purchase $40 million worth of Bitcoin.

- Issuing preferred shares also increases leverage by $40 million. Strategy typically offsets this by issuing roughly $80 million worth of new MSTR shares and using those proceeds to buy more Bitcoin.

In this simplified example cited by Crypto Narratives, Strategy ultimately purchases $120 million worth of Bitcoin. Every additional dollar of preferred stock is therefore backed by roughly $3 of Bitcoin on the balance sheet.

This roughly corresponds to the company's current leverage ratio of around 33%, measured as debt divided by Bitcoin holdings.

Simply issuing more STRC increases financial leverage. That is why Strategy pairs preferred-share issuance with ATM sales of its common stock. New MSTR shares do not increase debt, while the additional Bitcoin strengthens asset coverage and helps keep leverage in check.

Risks associated with STRC

Despite not being a direct Bitcoin proxy, STRC remains closely tied to the health of the broader crypto market.

- Bitcoin exposure. Strategy's ability to fund dividends ultimately depends on the value of its Bitcoin holdings and continued access to capital markets.

- Market volatility. Crypto downturns can drive STRC well below its $100 par value.

- Variable payouts. Every month, Strategy's board adjusts the dividend rate to encourage trading around par and help reduce price volatility.

At launch in August 2025, STRC paid a 9% annual dividend, equal to $0.80 per share. By mid-March 2026, that rate had risen to 11.50%, while the cash payment adjusted to $0.48 per share.

Why is STRC falling?

On June 18, 2026, STRC dropped below $83, roughly 17% beneath its target value and its lowest level since launch. The decline set off a market-wide debate, arriving amid a sharp Bitcoin sell-off and a series of controversial management decisions.

About a month earlier, Strive Asset Management announced daily dividends for SATA. Combined with its higher 13% yield, the move intensified competitive pressure on Strategy as it sought shareholder approval to switch STRC to semi-monthly dividend payments.

SATA is another perpetual preferred stock tied to Bitcoin. However, unlike Strategy, Strive relies primarily on a dedicated cash reserve rather than billions of dollars in outstanding convertible debt.

Strategy then repurchased $1.5 billion of its 2029 convertible notes at an 8% discount. The transaction was partly funded using a cash reserve established in late 2025 to cover dividend and debt obligations. As a result, that reserve fell to roughly six months' worth of STRC dividend coverage, compared with the company's previous target of around 24 months.

On June 1, Strategy sold 32 BTC — its first Bitcoin sale since 2022. The market reacted sharply: Bitcoin’s price dropped below $72,000, triggering $93 million in liquidations, while Strategy shares fell over 9% in a single day.

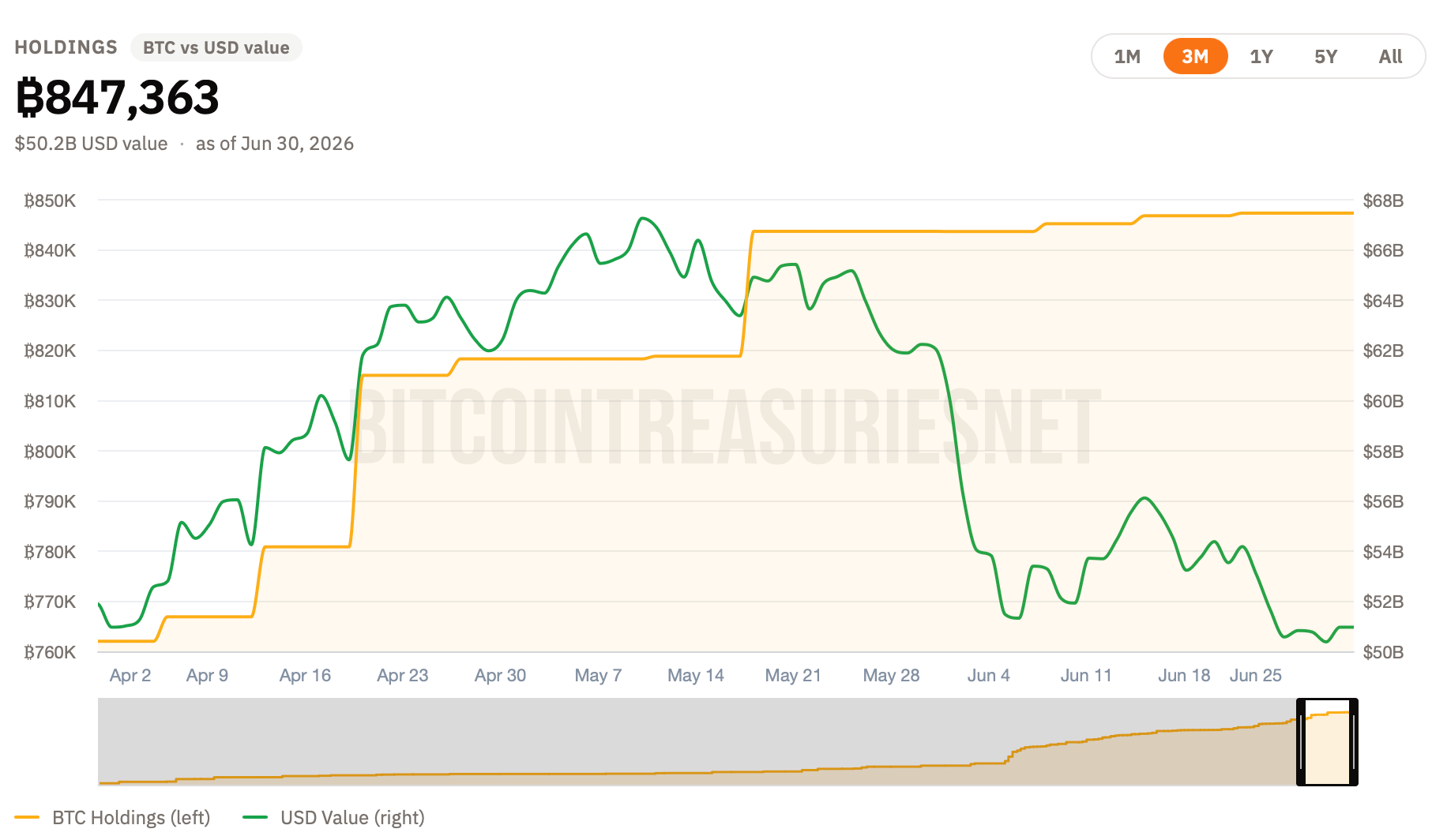

Since then, STRC has sunk well below its par value of $100, hitting a low of $74.50 on June 26, 2026. New Bitcoin purchases (June 8, 15, and 22) failed to undo the damage. At present, Strategy holds 847,363 BTC valued at roughly $50.2 billion — significantly below the cost basis of $64.10 billion.

How serious is this decline?

STRC is not a direct Bitcoin proxy, but its latest dip contrasted with Bitcoin's recovery. Does this disconnect threaten Strategy's future?

CoinShares expert Alexander Schmidt attributes STRC's weakness to uncertainty surrounding Strategy's approach to funding and meeting future obligations. He also notes that while Bitcoin's rebound strengthens Strategy's asset base, it does not automatically increase the cash available to pay dividends or eliminate claims that rank ahead of STRC holders.

Bitcoin sale: Alarming, but not existential

For years, Strategy's core narrative was simple: never sell Bitcoin. The sale of 32 BTC in June 2026 was therefore interpreted by some as an alarm bell, despite representing just 0.0038% of the company's holdings.

Selling Bitcoin to fund preferred-share distributions reversed the usual flow of capital — issuing securities to buy more BTC — and muddied the broader investment thesis.

Even so, this is far from an existential threat. According to Schmidt, a true worst-case scenario would require several things to happen at once:

- Strategy loses access to common equity markets.

- Cash reserves continue to shrink.

- Bitcoin sales become a recurring source of dividend funding.

- Bitcoin asset coverage deteriorates significantly.

- Repeated dividend increases fail to stabilize STRC.

New capital management playbook

The days of relying almost exclusively on issuing new securities to fund Bitcoin purchases are gone. On June 29, Strategy introduced its broadest capital management overhaul to date. The Digital Credit Capital Framework aims to strengthen confidence in STRC and other preferred securities, preserve long-term Bitcoin exposure, and give management greater flexibility when supporting its capital structure.

- Formalized USD reserve policy. It now holds roughly $2.55 billion in cash reserves, covering about 17 months of expected preferred dividends and interest payments. The board committed to maintaining liquidity equivalent to at least 12 months of those obligations, with additional support available through a newly authorized Bitcoin monetization program if needed.

- Higher STRC dividend. The annual rate rises from 11.5% to 12.0%, effective from July 2026. Going forward, Strategy says it will review the payout each month based on factors including STRC's trading price, market yields, Bitcoin volatility, credit spreads, reserve coverage, and broader capital market conditions.

- Active balance-sheet management. The board authorized up to $1 billion of preferred share buybacks, another $1 billion for MSTR repurchases, and a Bitcoin monetization program. The latter allows limited BTC sales to build reserves, fund dividends, or repurchase securities when management believes doing so creates more value than issuing additional equity.

As CEO Phong Le put it, the company is evolving from "one-way capital issuance" toward a more dynamic capital allocation model.

Strategy moves to semi-monthly payments

Earlier in June, Strategy transitioned STRC from monthly to semi-monthly dividend payments. CEO Phong Le described the change as a way to "stabilize price, dampen cyclicality, drive liquidity, and grow demand for STRC while giving holders faster reinvestment opportunities."

As a result, investors receive the same annual income, but split across twice as many payments. However, as Schmidt points out, the move does not strengthen Strategy's underlying credit profile or compensate investors for what some consider an insufficient yield.

Three core ways to support STRC

The company has several levers available to influence STRC and its broader capital structure.

1. Boost payment frequency further

Following the shift to semi-monthly dividends, Strategy could theoretically adopt the same daily dividend model as Strive. While this would not change the underlying credit fundamentals, it could make STRC more attractive to income-focused investors by reducing ex-dividend price adjustments.

2. Increase the dividend yield

As discussed above, Strategy can raise STRC's dividend to improve its competitiveness. Investors frequently compare it with Strive's SATA, currently holding an edge thanks to its higher 13% annualized yield, daily distributions, and debt-free balance sheet.

3. Swap senior debt for common equity

In simple terms, Strategy could issue new MSTR shares and use the proceeds to repay part of its outstanding convertible debt. Unlike equity, convertible notes eventually mature, so replacing them with common stock removes future repayment obligations.

This would further strengthen the company's balance sheet. It would also provide STRC holders with a larger asset cushion, since convertible noteholders rank ahead of preferred shareholders in a bankruptcy.

Wrapping up

STRC's recent slide has exposed the limits of Strategy's latest funding engine, but it has not broken the broader model. Short-term price weakness does not automatically break the mechanism of converting investor demand for income into new Bitcoin purchases.

What matters more is whether Strategy can keep attracting capital while maintaining enough cash to support dividends and preserve confidence in the structure. For now, it still has several levers to pull, from adjusting dividend payouts to reshaping its capital structure. If investor confidence holds, STRC's weakness may end up looking more like a stress test than a structural failure.