The hidden advantage of borrowing when you don't need the money

Would you open a credit line when you don't need the cash?

Most people wouldn't. They wait until an unexpected expense shows up or an investment opportunity can't be ignored. Only then do they start looking for liquidity.

The problem is that urgency rarely works in your favor. By the time you need money, markets may be down, your collateral may have lost value, and you're forced to make decisions under pressure.

A better approach is to prepare before any of that happens.

Open a credit line while your portfolio is healthy, your LTV is low, and you have time to think clearly. Then, if life — or the market — throws you a curveball, the liquidity is already there.

Let's look at why borrowing before you need it can be one of the smartest ways to manage a crypto portfolio.

TL;DR

- Securing a credit line before you need it makes sense. Applying during a calm market may give you better terms and more time to think.

- 0% APR at low LTV means it costs nothing to keep a credit line open. Your safety net has no monthly fee.

- Liquidity on demand is valuable. When an opportunity or emergency appears, you don't want to be scrambling for approval.

- You're a better negotiator when you're not desperate. Last-minute borrowing puts you at a disadvantage.

- The best time to open a credit line is when everything is fine. That way, you're ready when it's not.

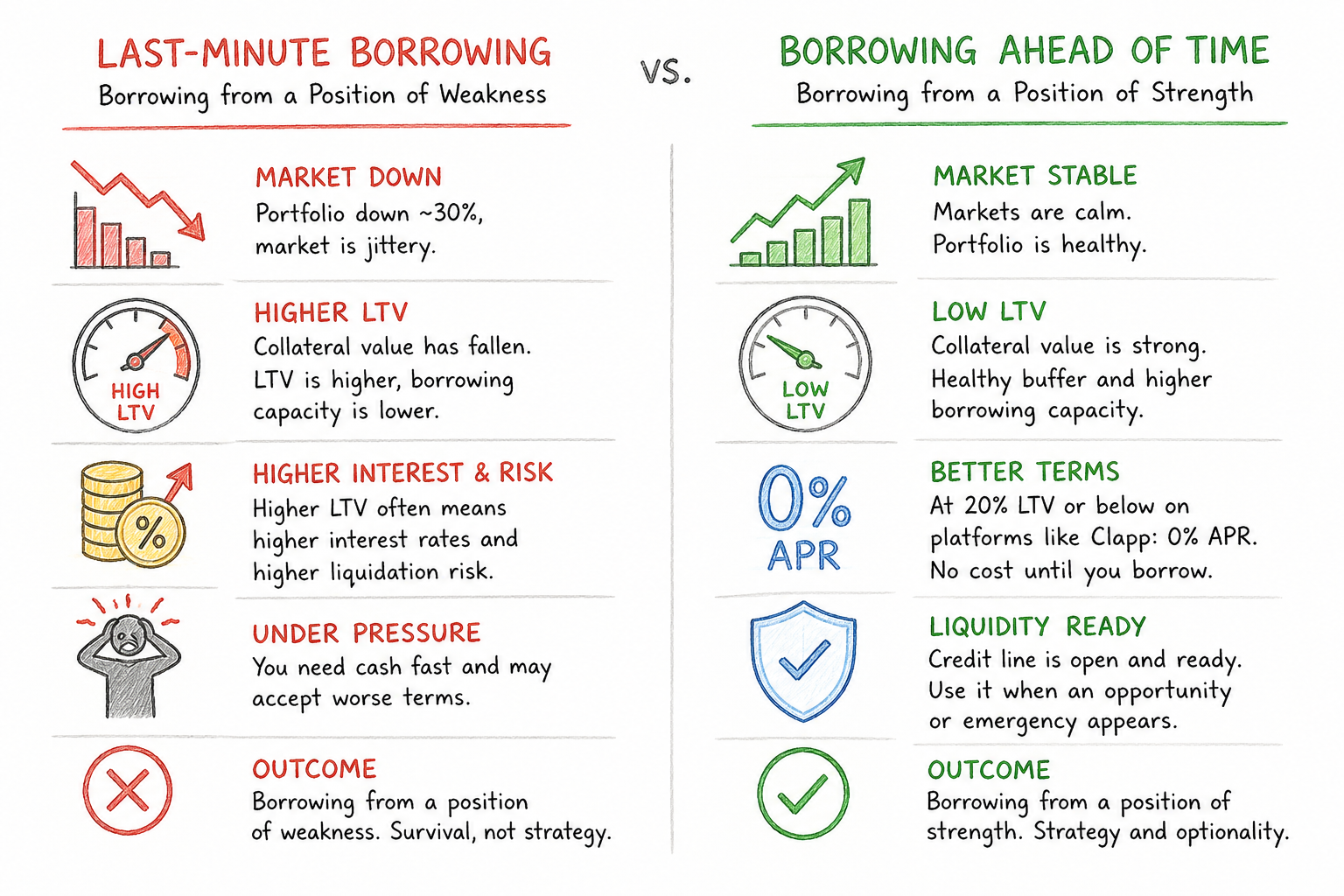

The problem with last-minute borrowing

Picture this.

You need cash fast because an emergency comes up. Meanwhile, your portfolio is down 30%, and the whole market is jittery.

What happens if you apply for a loan or credit line?

The value of your collateral has fallen. That pushes your LTV (loan-to-value) higher, reducing your borrowing capacity. You must deposit more assets to secure the needed amount.

On many platforms, a higher LTV also means paying a higher interest rate. If your LTV climbs too far, you could eventually face liquidation.

So the terms you're offered aren't great. What's worse, you're under time pressure, willing to accept whatever you can get.

You've just borrowed from a position of weakness.

That's not a strategy. That's survival.

Now imagine the opposite scenario.

Borrowing from a position of strength

Markets are calm, your portfolio is healthy, and you don't actually need cash. Even so, you decide to open a credit line.

Why?

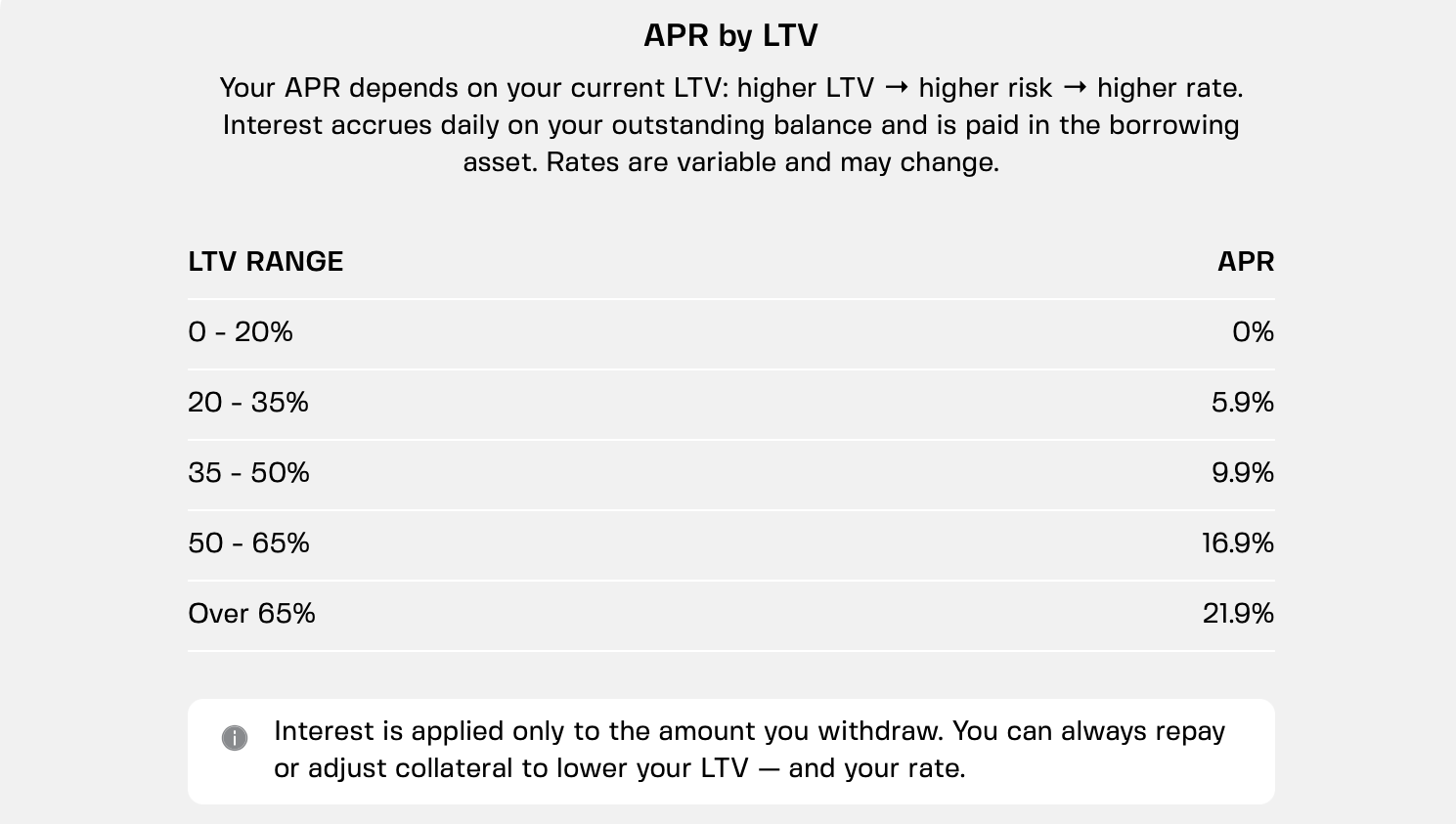

Because this is when your position is strongest. Your LTV is naturally low, giving you a comfortable collateral buffer. On some platforms, including Clapp, borrowing at 20% LTV or below even means 0% APR. Your credit line sits there, ready if you ever need it, without costing you anything until you borrow.

Then an opportunity appears — or life throws you an unexpected expense.

You don't need to apply for financing or rethink your portfolio. The liquidity is already there. You draw what you need, repay it on your own terms, and move on.

That's the advantage of borrowing from a position of strength.

The approval window matters

When markets are stable, your collateral is likely to be worth more. That means a lower LTV and a larger borrowing buffer.

Apply during a market downturn and the picture can look very different. Falling asset prices push your LTV higher, reducing how much you can borrow against the same portfolio. On some platforms, a higher LTV can also mean paying a higher interest rate.

The same portfolio can produce very different borrowing conditions depending on when you open your credit line.

You can't control the market. But you can choose whether to prepare before volatility arrives — or wait until you're forced to react.

The psychology of having a safety net

There's another advantage that's easy to overlook: peace of mind.

When you already have a credit line in place, you're less likely to make decisions under pressure. You don't have to panic-sell during a market downturn or rush into unfavorable terms because you suddenly need liquidity.

Instead, you have options. You can wait and assess the situation. And if you decide to borrow, it's because it makes sense — not because you've run out of alternatives.

That isn't just more comfortable. It's a better way to manage risk.

Your hidden advantage in action

Imagine you've opened a credit line but haven't used it. It simply sits there, available if you ever need it. At 20% LTV or below on Clapp, it isn't costing you anything.

Six months later, the market drops 30%. Most investors are focused on protecting their portfolios. Some are forced to sell.

Meanwhile, a project you've been following for months suddenly trades at a price you didn't expect to see again.

Instead of selling existing holdings or waiting for financing, you draw from your credit line and deploy capital immediately. When the opportunity passes, you repay the amount on your own schedule.

That's the hidden advantage.

The credit line wasn't opened for a specific purchase or emergency. It was opened so you'd have liquidity before you needed it. In other words, it bought you optionality — and in investing, optionality is often worth more than people realize.

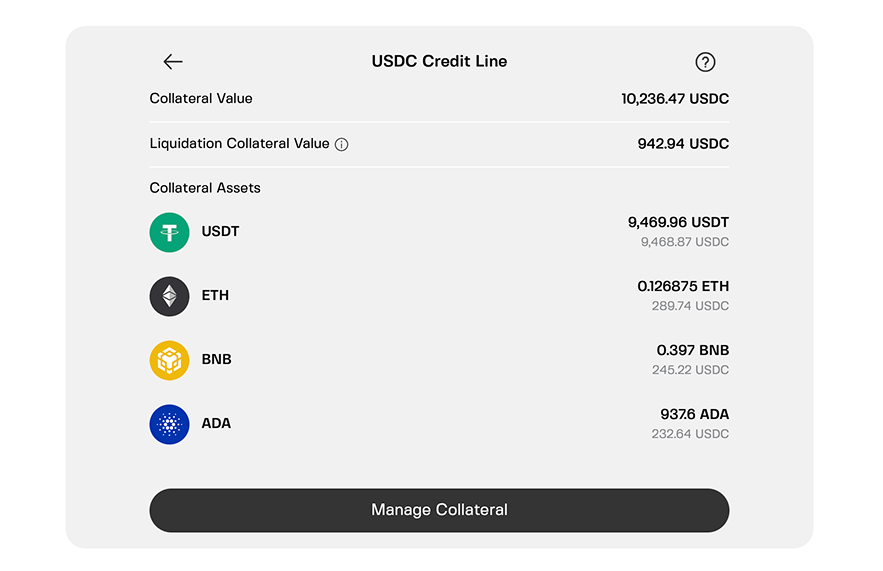

How credit lines work when you don't need them

You don't have to borrow a cent. As long as your collateral supports it, your credit line simply remains available.

On Clapp, borrowing at 20% LTV or below comes with 0% APR. There's no monthly fee and no obligation to draw funds. Your credit line is simply there if and when you need it.

And because it's a credit line — not a fixed-term loan — you stay in control. Borrow only what you need, repay whenever it suits you, and the available credit replenishes as you repay.

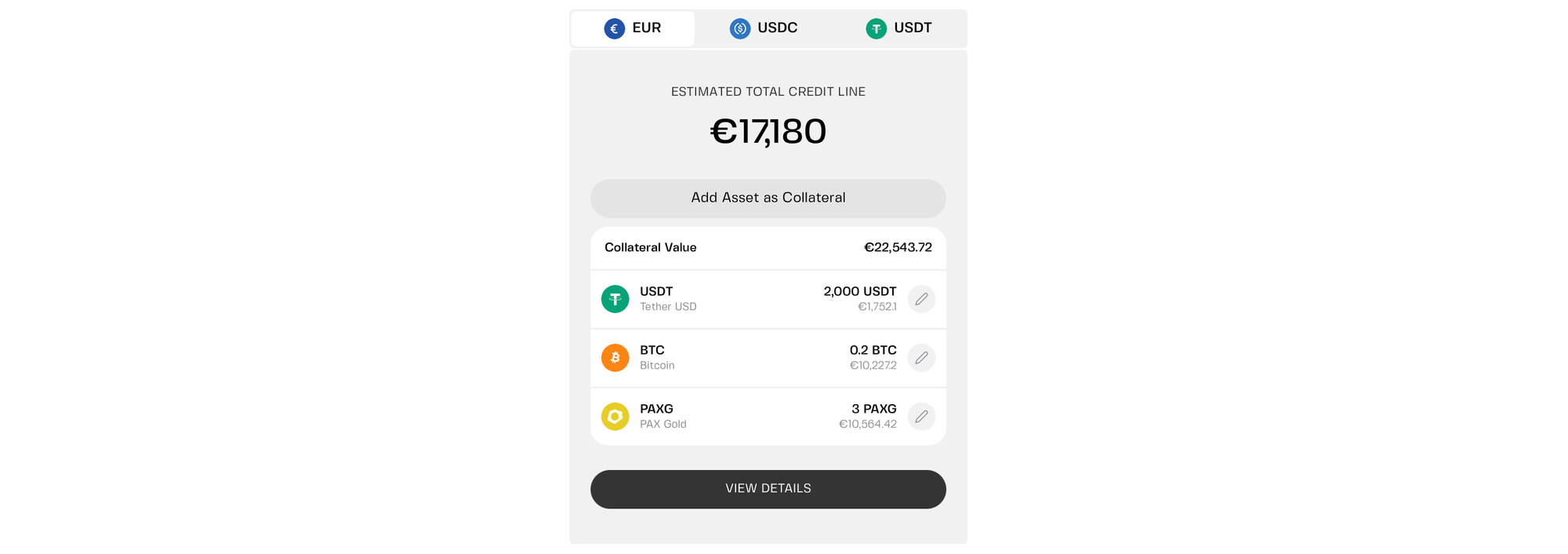

Flexibility extends to your collateral, too. Instead of relying on a single asset, Clapp lets you secure your credit line with a basket of up to 25 cryptocurrencies. As your portfolio changes, you can add, remove, or swap collateral without closing your credit line or applying for a new one.

Think of it as liquidity that's always within reach. Your collateral stays invested, but if an opportunity or unexpected expense arises, you don't have to start arranging financing from scratch.

The bigger picture

Most people think about borrowing only after they need it. A better approach is to think about liquidity before you do.

Opening a credit line while your portfolio is healthy doesn't mean you expect to borrow tomorrow. It means you're putting liquidity in place while you still have the flexibility to structure it on your own terms.

That's the hidden advantage. A credit line is a way to prepare — so that when markets move or life gets in the way, you have options instead of difficult choices.

Frequently asked questions

1. Does a credit line cost anything if I don't use it?

On platforms that offer 0% APR at low LTV, no. Keep your LTV at or below the threshold (20% on Clapp) and your credit line costs nothing until you draw from it. Check your lender's terms carefully, as conditions vary.

2. What happens if my collateral drops in value after I open the credit line?

Your LTV rises. If it climbs above the 0% threshold, you may start paying interest. You can add more collateral, repay part of the drawn amount, or do nothing if you're still within safe limits.

3. Can I open a credit line and never use it?

Yes. It's a safety net. It's there if you need it, but you're not obligated to borrow, and it costs nothing until you actually use it and your LTV leaves the zero-interest zone.

4. Does opening a credit line affect my credit score?

No. Crypto credit lines don't check traditional credit. They're secured by your collateral alone, which is why you deposit more than your borrowing limit. Your credit score isn't involved.

5. Is this strategy only for large portfolios?

No, the math works at any scale. A $5,000 credit line with 0% APR is just as useful as a $50,000 one. It's about having optionality — not the size of the limit.