0% interest on crypto loans? Yes, it exists. Here's the catch.

Banks won't lend you money at 0%. Credit cards certainly won't. So how can a crypto platform offer something for nothing? And yet, it's real — with a few caveats.

Let's break down how 0% crypto borrowing works, who it's actually for, and whether it makes sense for you.

In a nutshell

Some platforms let you borrow against your crypto at 0% interest — but only if you keep your loan-to-value ratio (LTV) low enough.

- All loans are over-collateralized, so you must pledge more crypto than what you borrow.

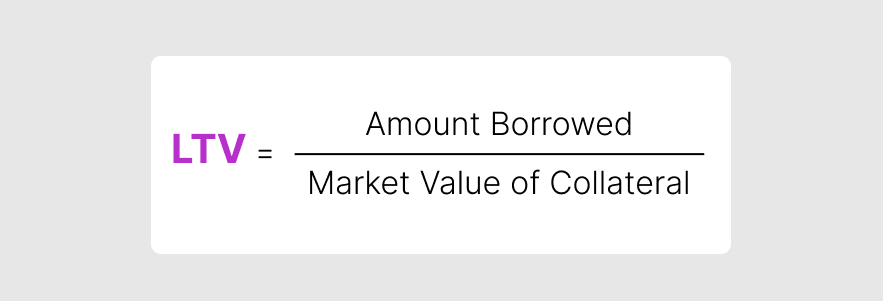

- Your provider's acceptable LTV (loan-to-value ratio) determines that gap — e.g., 50% LTV means you can borrow half of your collateral value.

- Interest is expressed as APR (Annual Percentage Rate) — the total yearly cost of borrowing money, also used in traditional banking.

Lower LTVs ensure better protection for you and your lender if the market goes south. As crypto prices fluctuate, so does your collateral value. If it falls too rapidly, your pledged assets may be auto-liquidated.

That's why lenders incentivize responsible borrowing behavior. The more conservative you are, the less it costs to borrow.

On Clapp, for example, borrow $10,000 in USDT against $50,000 in BTC (that's 20% LTV), and your interest rate is zero. Not 0.5% or "0% for the first month." Literally nothing.

But you can't max out your borrowing power and expect to pay nothing.

Wait — how do they make money?

Fair question. If you're paying 0%, how does the platform stay in business?

First, not everyone pays 0%. Most borrowers take out larger loans relative to their collateral — say, 50% or 60% LTV — and pay interest like normal. That revenue subsidizes the safe, conservative borrowers.

Second, there are still fees somewhere. For instance, you might pay a small spread when you swap assets or move funds within that same crypto app. But on the loan or credit line itself? It costs you nothing as long as you play it safe.

Think of it like a gym membership. The people who sign up in January and never show up are subsidizing the equipment for the regulars who actually use it. Same idea here.

The catch (there's always one)

Here's where people get tripped up.

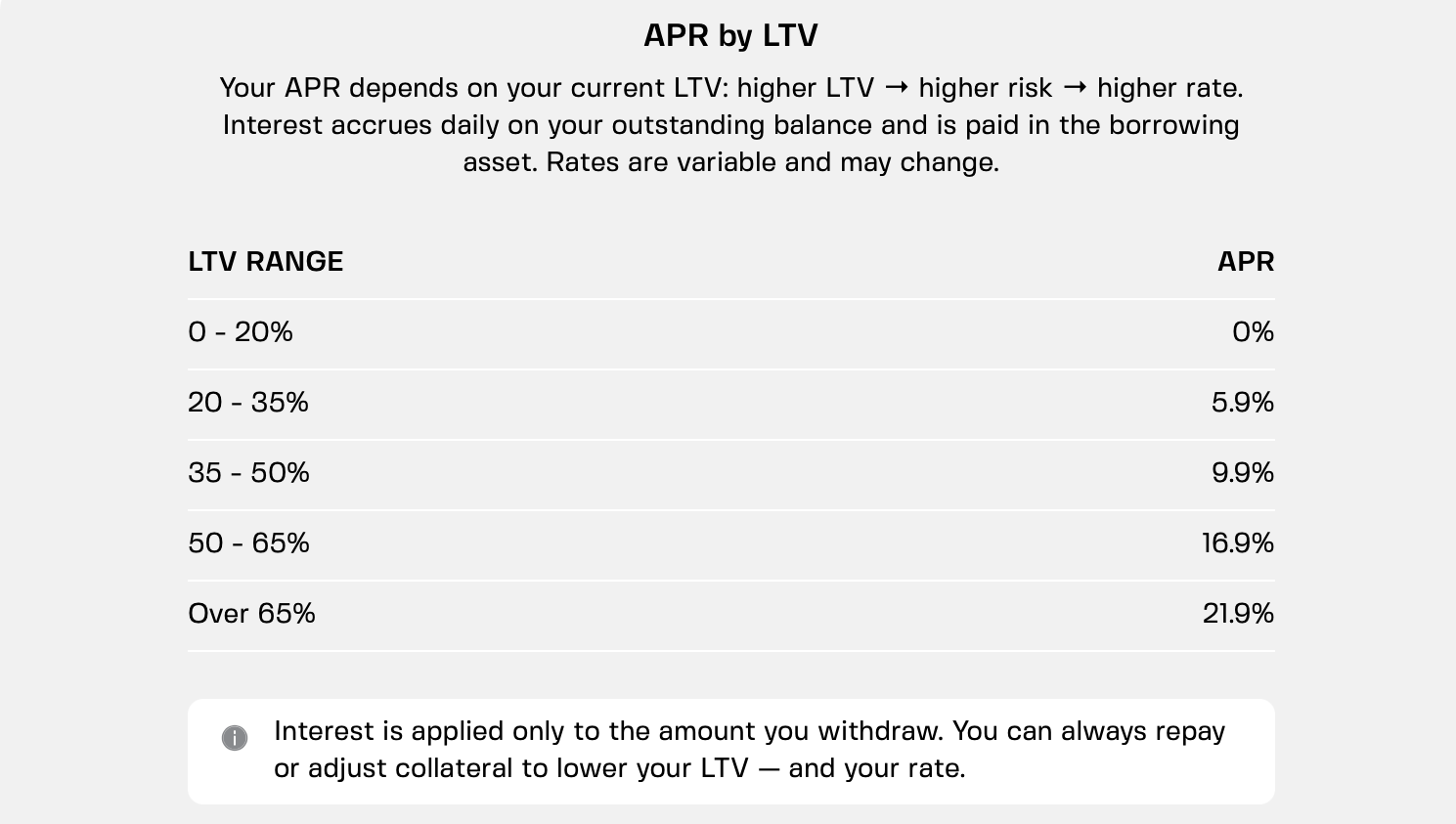

Catch #1: 0% isn't automatic. You have to maintain a low LTV. Borrow more than your lender's threshold, and your rate kicks in. The safer you are, the less you pay — which is honestly a pretty fair trade.

Catch #2: Markets move. Suppose you start with 20% LTV or less. If the collateral drops 30%, your LTV jumps. Suddenly you're over the threshold, and that 0% rate becomes yesterday's news. Either add more collateral or pay down some of the loan. Ignore it, and you're paying interest like everyone else.

Catch #3: You still have to pay back the loan. This sounds obvious, but it's worth saying. 0% interest isn't 0% principal. The money you borrow eventually needs to go back. Some people treat credit lines like free money and forget the part where they have to repay it.

Catch #4: Not all platforms offer this. Most crypto lenders charge interest across the board. The 0% model is still relatively rare. If you're on a platform that doesn't offer it, you're paying regardless of how safely you borrow.

Who is this actually for?

The 0% APR model isn't designed for everyone. Here's who it actually makes sense for:

The safety-net borrower. You don't need cash right now, but you want a credit line ready in case of emergency. Park your crypto, set up a 20% LTV line, and let it sit. It costs you nothing until you use it. That's insurance, not debt.

The short-term liquidity user. You need cash for two weeks while you wait for a transfer to clear. Borrow at 0%, use the funds, repay quickly. Total cost: zero.

The strategic holder. You believe in specific coins long term but see a short-term opportunity elsewhere. Borrow against your BTC at 0%, use the funds for the opportunity, repay when it plays out. You kept your assets and captured the upside.

Who should think twice

This isn't for people who want to max out their borrowing power. If you're trying to borrow 50% or 60% of your collateral's value, you're paying interest — and you should. That's riskier for everyone involved.

It's also not for people who treat credit lines as free money with no repayment plan. The loan still exists. 0% interest doesn't mean 0% responsibility.

How to borrow at 0% interest

The mechanics are pretty standard across platforms, with one twist. Here's how it works if your lender offers a 20% LTV threshold for zero interest:

- You deposit crypto as collateral — BTC, ETH, stablecoins, whatever's accepted

- You choose how much to borrow, based on your collateral's value

- Keep your loan below 20% of your collateral's value → 0% APR

- Borrow more than that → standard interest rates apply

Once your loan is active, the funds land in your account. You can use them in-app, withdraw to your bank, or just let them sit until you need them. Repay anytime — no penalties, no schedules.

With a Clapp a credit line (not a term loan), you only pay interest on what you actually use. And if you're in that 0% bucket? That's nothing at all.

Bottom line: 0% crypto loans are real

Not a trick, not a teaser rate, not fine-print bait-and-switch. But not free money either.

Those products reward conservative borrowing — the kind where you leave plenty of buffer between your loan and your collateral's value. If markets dip, you have room to breathe. If they rally, your upside stays intact.

The catch isn't that the 0% is fake. It's that most people won't qualify for it, because most people want to borrow more than they safely should.

Borrow smart, pay nothing. Borrow aggressively, pay like everyone else. Seems fair.

Frequently asked questions

1. Does 0% APR mean I pay nothing to borrow?

That's right — as long as you keep your LTV at 20% or below. Borrow $10,000 against $50,000 in crypto and you pay zero interest. Not for a month. Not as a teaser rate. Zero, full stop. The moment your LTV creeps higher, standard rates kick in. But stay conservative, stay at zero.

2. What happens if collateral price drops while I have a 0% loan?

Your LTV moves with the market. Say you borrowed $10,000 against $50,000 in BTC (20% LTV). If BTC drops 30%, your collateral is now worth $35,000. Your LTV climbs to around 28% — which might push you over the 0% threshold.

From there, you can either add more collateral to bring LTV back down, or repay part of the loan. Act fast and your 0% rate returns. Ignore it and you'll start paying interest like everyone else.

3. Is this better than just selling my crypto when I need cash?

Depends on what you believe happens next.

If you think crypto is going to zero, sell. But if you're a long-term believer, borrowing lets you have it both ways: cash now, upside later. Plus, no tax event when you borrow. Selling triggers taxes in most places, but borrowing doesn't.

4. Can I lose my crypto if I borrow against it?

Only if you ignore the warnings. Platforms don't want to liquidate your collateral — it's bad for everyone. That's why they send alerts long before things get dangerous.

If your LTV climbs toward 70-80% and you do nothing, yes — the system may auto-sell a portion to protect itself. But with a 20% LTV loan, you'd have plenty of time to add collateral or repay before anything happens.

5. How much can I actually borrow at 0%?

It depends on what you pledge. On Clapp, keep your LTV at 20% or below and the rate is zero. So if you deposit $50,000 in BTC, you can borrow up to $10,000 at 0%. You can borrow more, but the rate won't be zero past that 20% threshold. The trade-off is simple: safety costs nothing, risk costs something.