Trading was just the beginning. Welcome to crypto's super app era.

The crypto industry is quietly pivoting through one of its most important business model shifts since the advent of Bitcoin. Drawing lessons from Asian super apps, simple platforms are leveling up into unified ecosystems, diversifying revenues amid maturing regulation.

Centralized efficiency and decentralized innovation have converged in a market projected to reach 4 billion users by 2030. Here's an overview of crypto super apps.

What is a crypto super app?

A super app pulls your balance and identity into a single interface, bundling everything from trading to AI to social media. It's an aggregation layer for a constantly expanding menu of services.

At its core, the model is about reducing fragmentation across financial and digital services. Instead of juggling 10 logins for 10 different tools, platforms bring them together into a single environment.

Crypto exchanges are evolving alongside their regulatory environments and philosophies into financial operating systems that can take on traditional banks. There’s no single blueprint for this overhaul — approaches vary depending on market conditions and regulatory constraints.

In practice, this maturation tends to follow four stages:

- Pure trading exchange — single revenue stream.

- Multi-product platform — lending, staking, margin trading. Trading still drives 70–80% of revenue.

- Financial services hub — payments, crypto cards, custody, asset management. Trading share drops below 60%.

- Daily driver super app — social features, commerce, third-party mini-programs. Trading falls under 30%, resembling WeChat Pay's model or Telegram's ambitions.

This shake-up isn't just happening at exchanges. Traditional banks and brokerages are enhancing their apps with crypto, stablecoin payments, and tokenized products. Social networks and messaging apps are dipping their toes into wallets and basic financial services.

Why everything is converging now

Several structural shifts are driving this transition from single-purpose exchanges to multi-service platforms.

Coinbase CEO Brian Armstrong said it directly:

"We want to be a bank replacement for people, their primary financial account."

The company's rebranding positions Base (formerly Coinbase Wallet) as an all-in-one financial hub, loaded with social networking features, Apple Pay deposits for USDC purchases, and upcoming add-ons like tokenized real-world assets, stocks, and derivatives.

However, the super app narrative is not a guaranteed outcome. It is an emerging direction shaped by infrastructure maturity, regulation, and user behavior — not a settled end state.

Large global exchanges are taking on broader ecosystem roles, supporting payments, applications, and infrastructure layers across multiple markets.

Binance — still the heavyweight with roughly 38% of the global market share — has expanded into payments and ecosystem infrastructure through BNB Chain, which supports thousands of decentralized applications and real-world integrations across multiple sectors, from ride-hailing to food delivery to public transport.

While large CEXs have an early advantage, the super app model remains open, with fintechs, social platforms, and on-chain ecosystems all competing for different parts of the stack.

The underlying driver — market expansion beyond trading

Crypto is moving beyond spot and derivative trading to capture markets orders of magnitude larger. The crypto exchange market sits at a modest $55 billion. Meanwhile, social platforms pull in $208 billion, payments $788 billion, and global financial services a massive $36 trillion.

Crypto rails now handle payments, real-world assets, prediction markets, AI — things that used to live entirely outside the ecosystem. Super apps reflect this shift at the product level, encompassing more of a user's financial life.

Which platforms become super apps?

Reaching super app status demands strong user relationships and deep funding rails. That puts crypto exchanges in the driver's seat. The deeper their liquidity, the smoother their execution, custody, and distribution — and the easier it becomes to roll out new services.

Users with active balances are also best positioned to take the next action. Binance Pay is a prime example of a crypto-native payment feature breaking into everyday life — to the point of being integrated with national systems like Brazil's Pix.

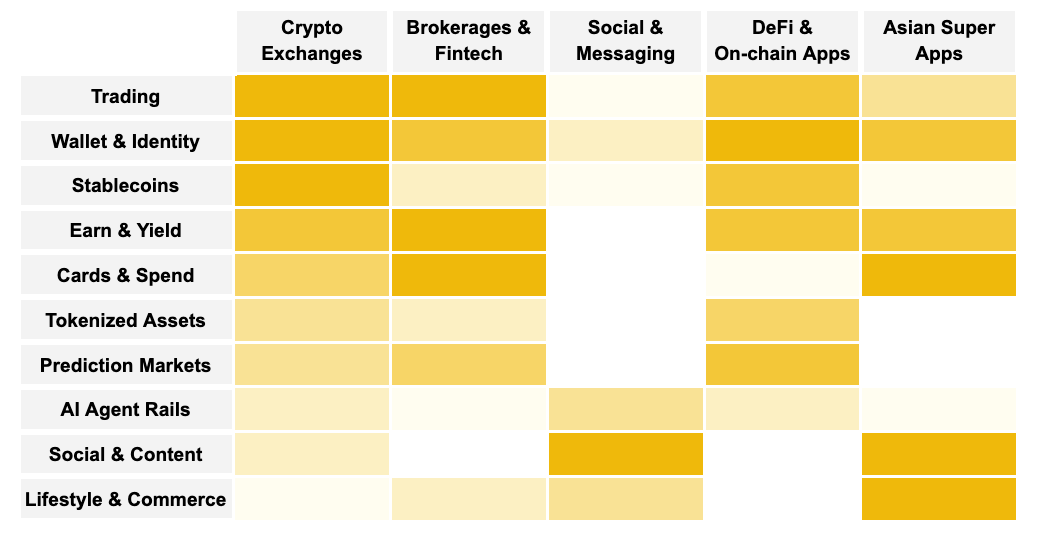

The super app stack is multi-layered, which creates coverage gaps. The competitive landscape is uneven:

- Crypto exchanges are the most broadly encompassing. Their biggest strengths: trading, wallets, stablecoins, and yield. Tokenized RWAs, AI, and social layers are secondary — but growing.

- Brokerages and fintech firms cover trading and spending. But they're weak on stablecoin-native rails, offer limited access to tokenized assets, and have no social surfaces.

- Social platforms own user attention and support commerce and AI rails. Yet they lack depth in financial services — with some exceptions in Asia.

- DeFi and on-chain apps offer a competitive range of services but struggle with distribution and social or lifestyle features.

Key drivers of the super app shift

The super app logic isn't new. But the surrounding product space is finally ripe for aggregation. Here are the main fuel sources:

#1 Stablecoin market is booming

Stablecoins have surged to $316 billion, weaving together trades, cross-border payments, settlements, yield, and tokenized assets. Fintech firms and giants like PayPal now treat them as a vital link between users and everything else — savings, on-chain investments, you name it.

Shifting from speculative trading to everyday usefulness needs a stable unit of account. Payments are the magnet that keeps people coming back to super apps. Stablecoins' 24/7 transaction capability makes them the perfect backbone for bundling services into a single, smooth experience.

Cost is another advantage. Legacy systems like cross-border remittance are notoriously expensive. Stablecoins dramatically reduce those fees, enabling fintechs to offer competitive services — paying remote workers in stablecoins, for example. Meanwhile, yield-bearing stablecoins (such as Sky Protocol's SUSDS) let users hold assets on-chain while earning passive returns automatically.

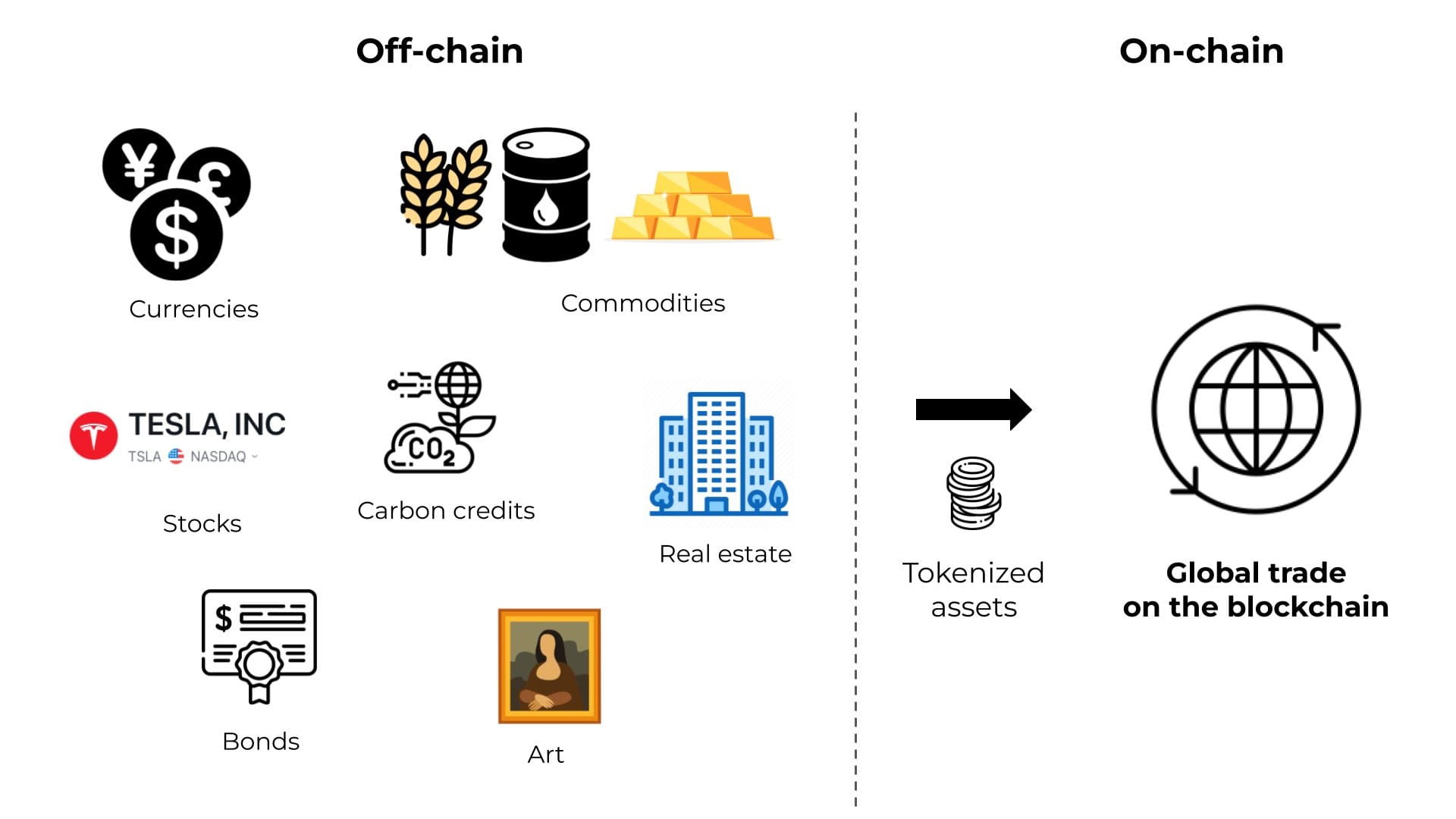

#2 Tokenization is growing

Tokenization brings real-world assets onto the blockchain. Real estate, fine art, corporate stock — all can now live on-chain. What was once theoretical has grown into a $25 billion market.

Super apps can now bring together a user's entire financial life: crypto, tokenized stocks, fiat — the whole picture. Tokenization acts as the connective tissue between payments, yield, and long-term investing, making traditionally illiquid assets accessible to the average user.

Super apps put it all within reach, democratizing trading through fractional ownership.

#3 Payment rails are turning institutional

Platforms like Ripple and Fireblocks now offer "asset-agnostic" infrastructure — meaning apps no longer need to stitch together half a dozen vendors just to move money. Transactions flow across stablecoins with smoother on/off ramps, simplified compliance, and stronger custody and treasury management baked in.

These institutional-grade rails are the plumbing behind everyday services: bank transfers, ACH, card payments — all running inside super apps without users ever noticing the complexity.

#4 Regulation supports product bundles

The GENIUS Act (July 2025) — the US federal framework for stablecoin issuance — flipped a switch. SEC Chair Paul Atkins backed the model, calling it consistent with where regulation is headed. As the regulatory scope widens, companies can pack more products into the same interface without juggling separate legal entities every time.

#5 CEX trading fees are shrinking

Trading-dependent models have proven fragile. In Q4 2024, top 10 centralized exchanges shattered records with $6.5 trillion in spot volume. Then over the next two quarters, volume crashed over 40% — even as prices climbed.

Users flocked to DEXs. Staking stepped up as a cornerstone revenue generator. Platforms now take a significant chunk of user rewards. At press time, Kraken charges 15–30%, Coinbase takes 25–35%, and Binance's cut ranges from 9.95% to nearly 40% depending on the asset.

Lending and interest products bring recession-proof revenue — enough to weather bear markets when trading volume dries up. Token listing fees are another direct revenue source: $50,000 to several million depending on the exchange tier.

#6 API access is now monetized

What was once free internal infrastructure is now a monetizable product. Data-hungry businesses pay a premium for direct access to deep liquidity pools. Institutional analysts, wallet developers, portfolio trackers, and researchers have become the primary customers for enterprise plans.

The economics are straightforward. CMC's free tier offers 10k calls per month without historical data. Paid tiers provide up to 3 million calls per month with unlimited historical data and endpoints. Crypto.com's unified REST and WebSocket APIs serve both retail and professional segments.

Reality check: Limitations of the super app model

The super app model isn’t without trade-offs. Bundling services increases platform risk, raises regulatory complexity across jurisdictions, and may conflict with crypto’s original ethos of modular, user-controlled finance.

Furthermore, this model isn’t guaranteed to win everywhere. In many markets, users prefer specialized apps over all-in-one platforms. Regulation also varies widely, which can limit how tightly services can be bundled. And in crypto specifically, fragmentation and self-custody are often features, not bugs.

In other words, aggregation creates convenience — but it can also introduce trade-offs around control, risk, and user trust.

Lessons from Telegram and WeChat

China's WeChat serves over 1.3 billion monthly users — a sprawling ecosystem that blends instant messaging, social networking, and mobile payments with over 2 million "mini programs." It's the blueprint for the plugin architecture: a host app orchestrating smaller "apps within an app."

Those mini programs let developers build lightweight applications that require no installation and update themselves over the air. WeChat now processes over 74% of China's mobile payments and touches more than 200 industries — from food delivery to government administrative tools.

Meanwhile, over 8,000 Telegram mini-apps now reach more than half a billion users, with significantly higher retention than traditional mobile apps. They power ride-sharing, e-commerce, and DeFi tools, with the TON blockchain enabling seamless, in-app crypto transactions.

Crypto exchanges with super app ambitions are borrowing the playbook. Coinbase's MiniKit SDK for Base lets developers spin up lightweight apps that run inside the super app interface while piggybacking on the platform's security framework.

Minimizing onboard friction

The "learn-as-you-go" approach has become the industry's golden standard — platforms offer intuitive onboarding where complex concepts are introduced gradually with step-by-step education aids and visual cues.

Apple Pay changed the game for crypto onboarding. Suddenly, users could fund their accounts with a single fingerprint scan — no manual wallet setup, no copying long addresses. Tap to buy USDC, tap to trade, tap to pay. The friction that once stopped newcomers in their tracks is gone.

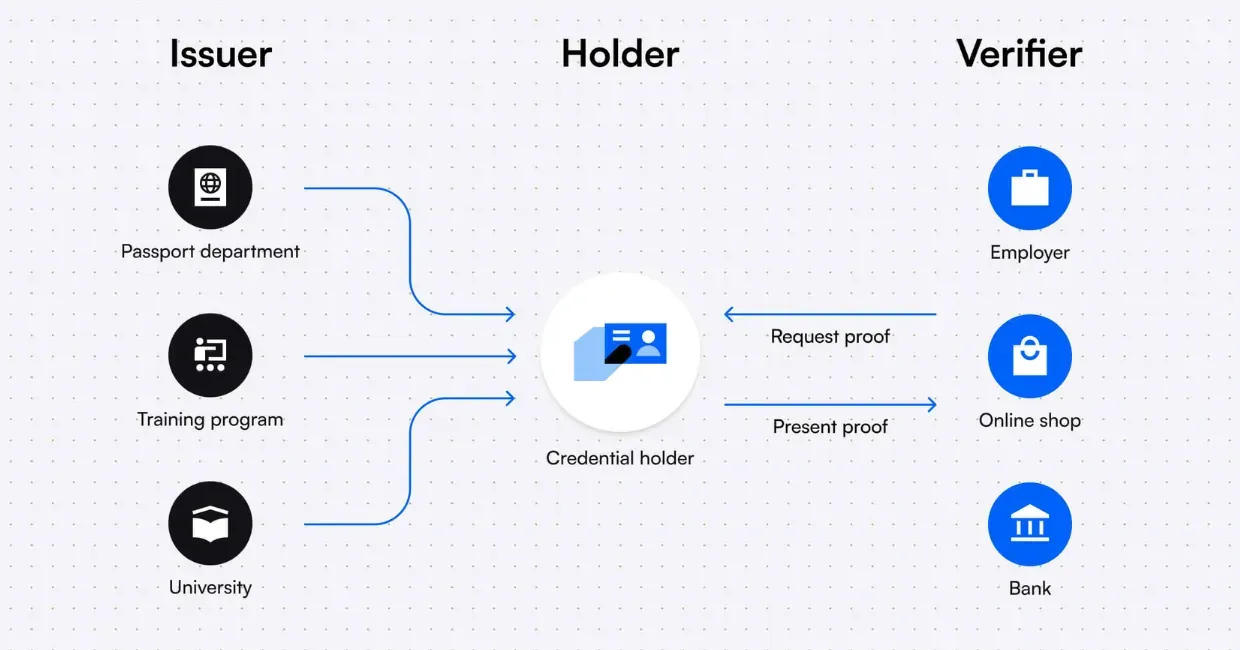

Then there's decentralized identity. Instead of creating separate logins for every exchange, wallet, and dApp, blockchain-based IDs let you carry your credentials with you. Think "Sign in with Google," but no corporation holds the keys. Your identity lives on-chain.

One profile works across dozens of platforms. And as digital ID infrastructure matures, this same system could eventually integrate government-issued credentials — driver's licenses, passports, even voting rights — all controlled by you, not a tech giant.

Payments: The magnet that keeps users coming back

According to McKinsey's report, end-user stablecoin payments doubled in 2025, hitting $390 billion. The B2B segment surged 733%, and card-linked stablecoin spending jumped 673%. But behind those impressive growth rates lies a glaring imbalance — 95% of total volume still sits in trading, treasury, and settlement.

Demand is lagging behind supply. That's not a problem — it's an opportunity. AI and social features could be the key to balancing the scales.

Why AI and social features matter more than they seem

One of crypto's biggest hurdles to mass adoption is complexity. Social media and feed-based products use design patterns that drive frequent, often habitual use. In crypto, newcomers can easily get lost navigating unfamiliar surfaces.

AI can cut through the complexity. Social features can fuel engagement. Together, they may prove essential for helping crypto super apps finally break through.

Who wins the race?

The platforms best positioned to lead this shift share three traits: deep liquidity, a wide product range, and large existing user bases.

But the next phase is about creating habits, not features. Will crypto super apps become useful enough, and often enough, to keep users inside one environment?

For most players in the space, the question isn’t whether this shift happens — but how to capture a meaningful role within it. The platforms that crack daily engagement — not just weekly trading — will define the next era.

Geography matters too. The next billion crypto users won't all come from North America or Europe. Asia, Africa, and Latin America are where super app behavior is already embedded. WeChat, Grab, Mercado Pago are how millions manage their financial lives every day.

For crypto, the open question is whether any current surface — stablecoin payments, yield, trading, or wallet-based discovery — can play that anchor role at consumer scale. Payments look promising. Stablecoins are already moving billions. But 95% of that volume still sits in trading and settlement, not everyday spending.

That gap is also an opportunity.