Staking vs. savings: Where your crypto works hardest

Buying crypto and waiting is the default. But your coins can do more than just sit there.

Two popular alternatives are staking and crypto savings. Both let you earn something extra on what you already hold, but don’t let the surface similarity fool you.

One ties up your assets in a blockchain’s inner workings. The other works more like a savings account you wish your bank offered — but built for digital money.

Which one actually fits your life? That depends on what you hold, how long you can leave it alone, and how much complexity you’re willing to deal with.

Let's break it down.

TL;DR

- Staking locks your crypto into a proof-of-stake blockchain (like Ethereum or Solana) to help validate transactions. You earn rewards — but your funds may be locked for days or weeks.

- Crypto savings are more like a bank account. Deposit your assets, earn interest (usually daily), and withdraw anytime — no validator drama.

- Staking only works with proof-of-stake coins (ETH, SOL, ADA, and a few others).

- Crypto savings work with almost anything — Bitcoin, stablecoins, even fiat.

- Lock-ups matter. Staking often means you can't sell during a crash. Savings keep you liquid.

- Slashing is a thing. Validators who mess up can lose your staked crypto. That doesn't happen with savings.

What is crypto staking?

You lock up your crypto to help a blockchain do its job. In exchange, the network pays you. To understand how this works, here is a quick bit of context.

Veteran blockchains like Bitcoin run on proof of work. Miners burn massive amounts of electricity solving math problems to validate transactions.

Newer rivals — Ethereum (since 2022), Solana, Cardano, Avalanche, and others — use proof of stake. Instead of miners competing, validators commit their own crypto as collateral. That's "staking."

You put up your tokens as a good-faith deposit. The network trusts you because you'd lose money by cheating. Act right, and you get paid. Simple.

How much does staking pay?

Your rewards come from the blockchain itself — and you're usually paid in the same crypto you locked up. This means you’re doubling down on exposure to that asset.

The returns are expressed as APY (Annual Percentage Yield), which depends on the network's reward rate, the size of your stake, and the lock-up period.

Typical ranges vary wildly — from under 2% on some networks to over 15% on others. But higher yield usually means higher risk.

Three ways to stake crypto

Most people don't run their own validators to stake. Here are the three main paths.

Solo (for the hardcore). You run the whole operation yourself. That means deep technical know-how and — on Ethereum — a minimum of 32 ETH (roughly $80k+ depending on market). It's the most decentralized option, but also the least practical for regular people.

Pooled (the easy button). Join forces with other holders on centralized exchanges or DeFi protocols. A pool operator handles the messy technical work. You contribute whatever crypto you have, and everyone splits the rewards proportionally.

Liquid (keep your options open). You stake through a protocol like Lido and get a receipt token — for example, stETH for staked Ethereum. That token stays liquid. You can trade it, lend it, or use it elsewhere in DeFi while your original crypto still earns staking rewards. The trade-off is extra risk from the protocol itself.

Downsides of staking

Staking rewards exist because staking involves real commitments and risks.

- Lock-ups. Your crypto may stay locked for weeks — on many DeFi platforms, common fixed terms range from 30 to 120 days. If the market drops during that period, you can't move your assets.

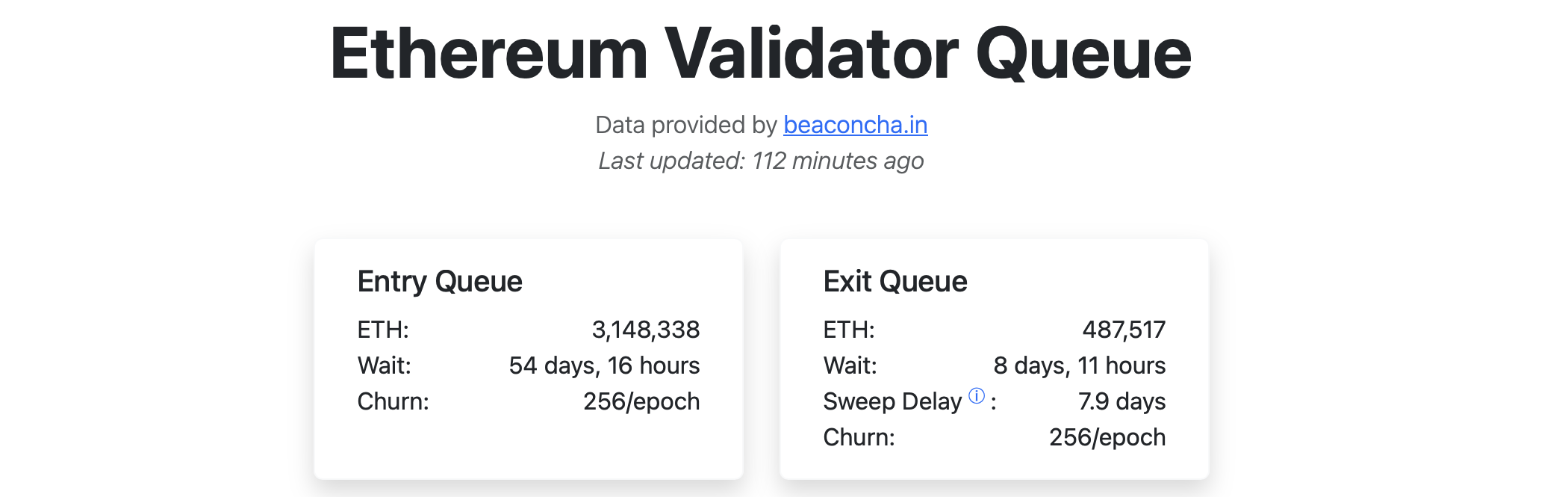

- Entry/exit queues. Ethereum's bonding and unbonding isn't instant. New validators currently wait roughly 54 days to become active, while exiting takes over 8 days. Wait times fluctuate based on network demand.

- Slashing. Validators who misbehave — whether due to technical failure or malicious action — can lose a portion of their staked crypto. If you stake through a pool, you share that risk, even if you didn't run the validator yourself.

- Smart contract risk. Liquid staking and pooled staking are powered by smart contract code. If those contracts have bugs or get exploited, stakers can lose funds. No insurance, no recourse.

- Reward rate volatility. Staking APYs aren't fixed. They fluctuate based on network demand and the number of active validators. A 10% APY today could be 4% six months from now.

- Tax treatment. In the US and most countries, staking rewards are treated as income — you owe taxes on the value at the time of receipt. Rules vary by jurisdiction, so check local guidance.

Crypto savings: Simpler alternative

Crypto savings work more like a traditional bank account — but with much higher interest rates. With no validator to run, there are no slashing risks.

You just deposit and earn while the platform handles yield-generation and security. Behind the scenes, your funds (crypto or fiat) could be lent out, staked, or deployed across DeFi protocols.

You basically do nothing to earn a slice of that revenue as interest. Depending on the product, withdrawal is available either at maturity or anytime.

What you get:

- 5–8% APY on stablecoins and fiat — vs. 0.01% at a traditional bank

- Daily compounding — your interest earns interest, every 24 hours

- 24/7 access — no bank hours, no "3–5 business days"

- No lock-ups (unless you choose fixed-term for higher rates)

- Works with Bitcoin, stablecoins, even fiat — assets that can't be staked

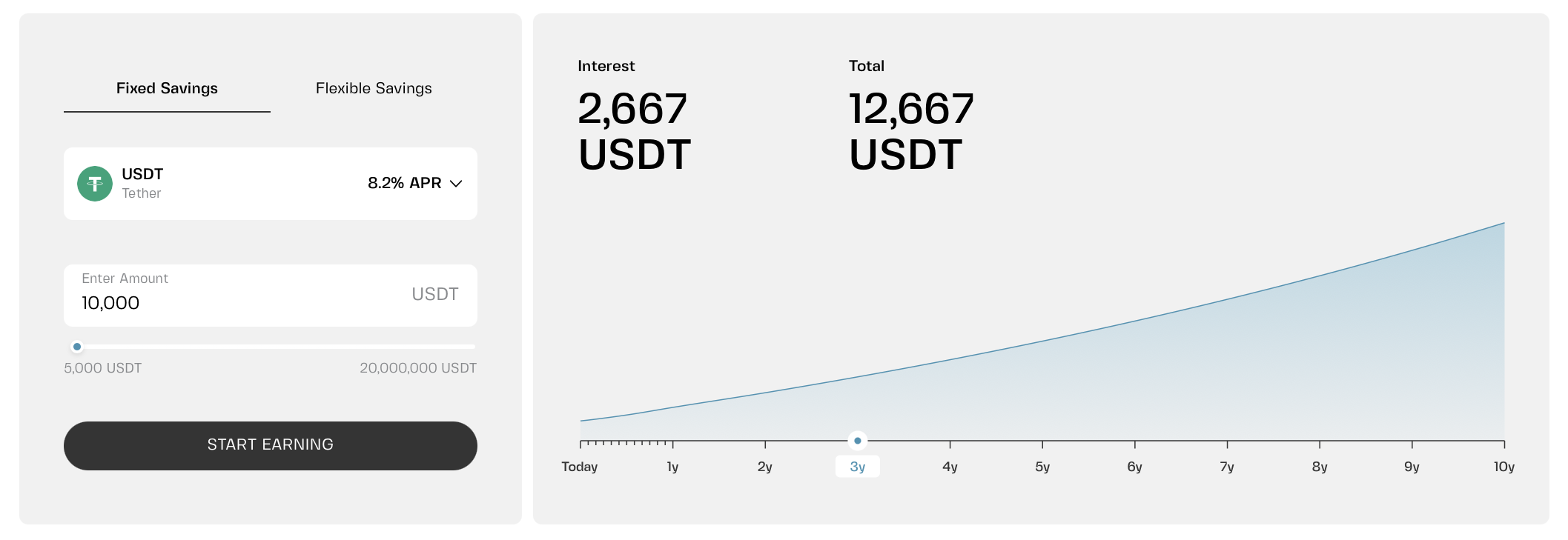

Some platforms offer flexible and fixed-term savings products with different rates and withdrawal conditions. For example, Clapp’s Flexible Savings offers instant withdrawals with up to 5.2% APY, while fixed-term options can reach higher yields.

High yields vs. falling prices

With staking, your exposure is amplified — in both directions. If the asset appreciates, you benefit from both price gains and rewards. But if it drops, losses can outweigh the yield.

Suppose you stake $20,000 worth of crypto at a 15% APY. One year later, you have $23,000 worth of that token. But if the price falls 40%, your position drops to $13,800 — below your original investment, despite the rewards.

Crypto savings don’t eliminate price risk either. The key difference is flexibility: with non-locked products, you can withdraw or rebalance at any time instead of waiting through an unstaking period.

Key differences at a glance

So where does your crypto actually work hardest?

Crypto savings tend to be a better fit for Bitcoin or stablecoin holders who want to earn in a user-friendly, familiar environment. They offer steady yield without slashing risk or validator overhead — and flexible products keep your funds accessible.

That said, staking may come out ahead in specific cases.

When staking makes sense

Staking appeals to long-term believers who don't need immediate access. It's a good fit when:

- You hold proof-of-stake coins like ETH or SOL for the long term

- You're comfortable with lock-up periods and can't panic-sell during a crash

- You want direct exposure to the network's yield mechanism

- You understand the risks — slashing, unbonding periods, variable rates

When savings makes more sense

Savings also work well for emergency funds or cash you might need soon. Flexible accounts let you earn yield without losing access — making them the best fit when:

- You hold Bitcoin, stablecoins, or other non-stakeable assets

- You want flexibility — withdraw anytime without waiting days

- You don't want to worry about validators, slashing, or smart contract bugs

- You prefer predictable rates and simple setup

Which to choose?

Staking and crypto savings both let your crypto work while you hold — but they operate on completely different mechanics.

Staking pays protocol-level rewards but comes with lock-ups, slashing risk, and technical complexity. It only works with specific coins.

Crypto savings apply to a much broader range of assets — Bitcoin, stablecoins, even fiat. They're simpler, and flexible products don't require you to trust your funds to a validator or commit to a lock-up period.

These options aren't mutually exclusive. You can get the best of both worlds.

Some investors stake a portion of their ETH or SOL for network rewards, while keeping stablecoins in flexible savings for liquidity. Others put long-term savings into fixed-term accounts for higher guaranteed rates.

Don't chase the highest yields blindly. The goal is to match your strategy to how you actually use your money.

Frequently asked questions

1. What's the difference between staking and crypto savings?

Staking locks your crypto into a blockchain network to help validate transactions. You earn rewards, but your funds may be locked for days or weeks. Crypto savings are more like a bank account — deposit your assets, earn interest, and withdraw anytime. Staking only works with proof-of-stake coins like ETH or SOL. Savings work with Bitcoin, stablecoins, even fiat.

2. Can I stake Bitcoin?

No. Bitcoin uses proof of work, not proof of stake. There's no native staking mechanism for BTC. To earn on Bitcoin, you need lending platforms or savings products that accept BTC deposits — like Clapp's Flexible or Fixed Savings.

3. What is slashing and can I lose my crypto staking?

Yes. Slashing is when a validator loses a portion of staked crypto as a penalty for misbehavior — either malicious action or technical failure. In pooled or liquid staking, you share this risk. Savings products don't have slashing risk.

4. Which one has better returns?

It depends. Staking on some networks can reach 10–15% APY, but rates are volatile and come with lock-ups and risk. Crypto savings on stablecoins offer 5–8% APY — lower but more predictable, with no lock-ups and no slashing. "Better" depends on your risk tolerance and how much access you need.

5. Is my crypto safe in a savings account?

It depends on the platform. Choose platforms with regulated licenses, institutional-grade custody (like Fireblocks), and transparent terms. No platform is 100% risk-free, but a regulated one is significantly safer than chasing 15% yields from unknown protocols.

6. Are staking rewards taxable?

In most countries, yes. Staking rewards are typically treated as taxable income at the time you receive them. Interest from crypto savings is also usually taxable. The rules vary by jurisdiction, so check with a local tax professional.

7. Which one is better for beginners?

Crypto savings, without question. No validators to research, no lock-ups to worry about, no slashing risk. Just deposit and earn. On Clapp, you can start with as little as €10 in Flexible Savings. Once you're comfortable, you can explore staking if you hold proof-of-stake assets.