Multi-collateral borrowing: Why using one asset is leaving money on the table

Suppose you have $50,000 in crypto but need $25,000 in liquidity. Would you just take out a simple loan — or optimize how you borrow?

Most people would look at their biggest holding (say, Bitcoin), pledge it as collateral, and call it a day. That way, you can still HODL and get cash for immediate needs. Repay on time and get your coins back.

That works, but the default way is not always the smartest.

Not all collateral is created equal. Different assets have different risk profiles, different volatility, and different borrowing power. Using just one coin means you're taking a volatility risk while leaving flexibility — and sometimes money — on the table.

Let's talk about multi-collateral borrowing and why mixing assets might be a wise move.

TL;DR

- Single-asset collateral locks you in. Pledge one coin, and you're tied to its performance.

- Different assets have different LTVs. Stablecoins borrow more efficiently than volatile crypto.

- Multi-collateral lets you mix. Combine BTC, ETH, and stablecoins into one collateral pool.

- You can swap assets after borrowing. No need to close and reopen your credit line.

- More flexibility means fewer liquidations. Adapt to market moves without panicking.

The problem with putting all your eggs in one basket

Let's look at our example closely. You pledge $50,000 in Bitcoin to borrow $25,000. Your LTV (loan-to-value ratio) is 50%. Not bad.

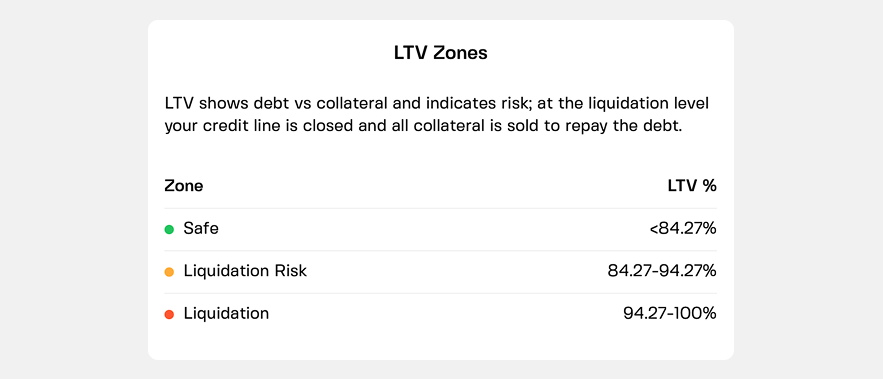

LTV is a core risk metric for any lender — it determines how much you can borrow, how much you pay in interest, and whether your collateral stays intact in a market crash. When LTV rises above a critical threshold (say, 80%, depending on the platform), the lender liquidates part or all of your holdings.

Your initial 50% is a moderate starting point. Then Bitcoin drops 20% → Your collateral is now $40,000 → LTV rises to 62.5%.

That safety buffer is shrinking.

Now what?

On a single-asset system, your options are limited:

a) Add more Bitcoin

b) Pay down the loan

c) Wait and hope

You can't swap to a less volatile asset or diversify your risk. You're ride-or-die with Bitcoin's performance.

That's the hidden cost of single-asset borrowing. You're essentially tying your loan's fate to that one coin's price swings. And it’s not just about liquidation risk — as your LTV rises, borrowing costs can increase as well, turning a “cheap” loan into a more expensive one over time.

Stablecoins change the math

Stablecoins are designed to maintain a peg to fiat (e.g., US dollar for USDT or USDC), commodities (e.g., gold for PAXG), or other financial instruments. This makes them less volatile than assets like Bitcoin or ETH — and more efficient as collateral.

As a result, platforms assign them higher LTV ratios — sometimes 80–90% instead of 50–60%. In simple words, you can borrow more against $50,000 in USDT compared to the same $50,000 in BTC.

Here's how this may work:

- Pledge $50,000 in BTC — get up to around $30,000–$35,000 (≈60–70% LTV)

- Pledge $50,000 in USDT or USDC — get up to around $40,000–$45,000 (≈80–90% LTV)

Same dollar value, but different borrowing power.

If you hold both, why not mix them? Pledge stablecoins for efficient borrowing and crypto for upside exposure. If your lender allows it, you get the best of both worlds — still HODL while unlocking more borrowing power with less risk.

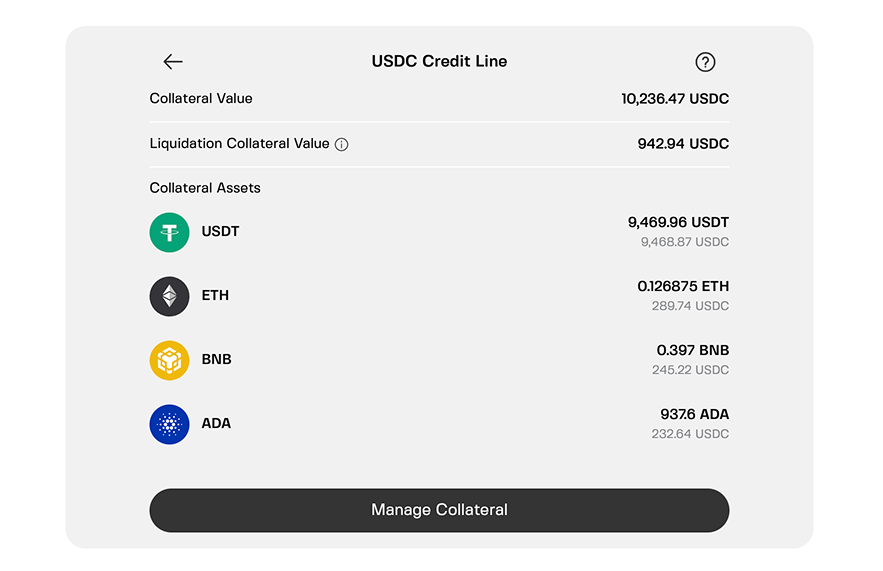

How multi-collateral borrowing works

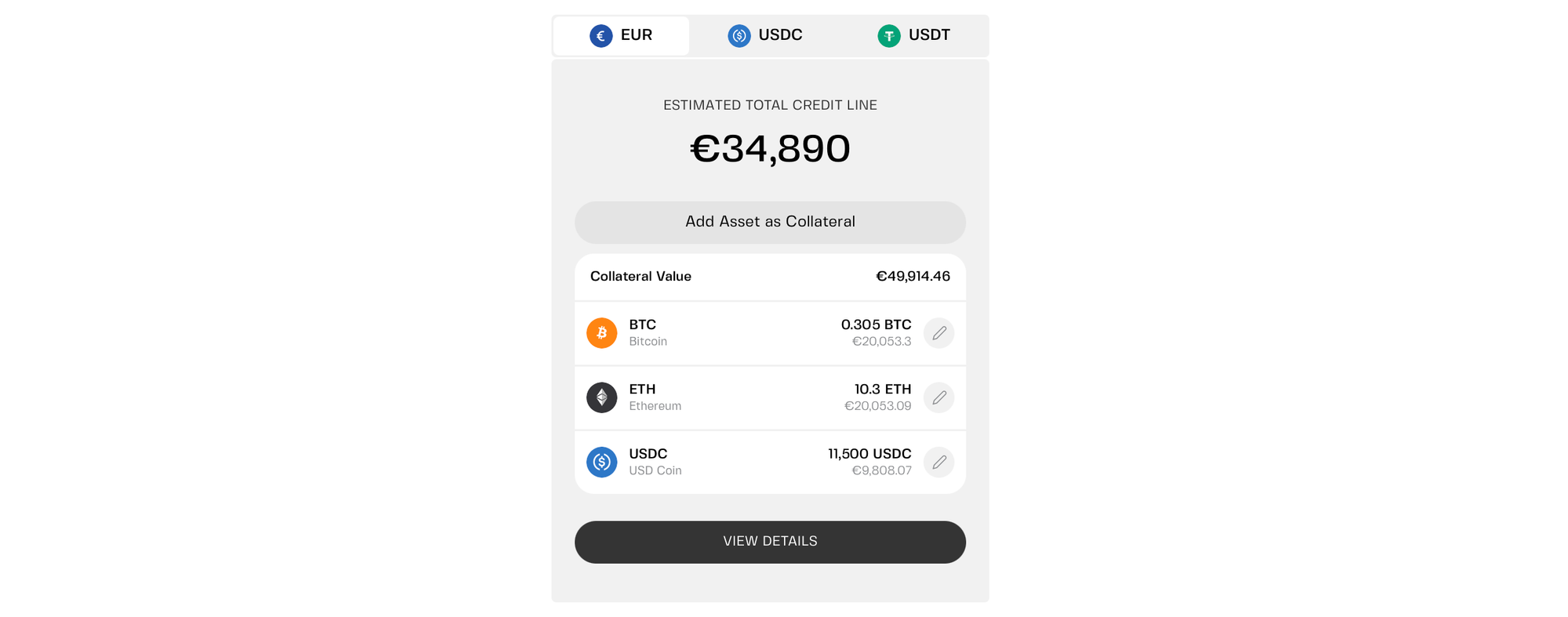

Instead of pledging a single asset, you deposit a basket of assets into one collateral pool. Here's how it works on Clapp at current market prices.

Example:

- Roughly €20,000 in BTC (0.305 BTC)

- Roughly €20,000 in ETH (10.3 ETH)

- Roughly €10,000 in USDC (11,500 USDC)

Total collateral: approximately €50,000.

The lender offers a borrowing limit of €35,000, but you choose to play it safe and borrow just €15,000 against the pool — roughly a third of its current market worth. This places your LTV at a conservative 30%.

Now, what happens if Bitcoin tanks, and ether follows?

Your USDC stablecoins keep your overall LTV from spiking as hard. You have buffer, options, and breathing room. The larger the share of stables or fiat, the safer you are.

And you can get even more flexible.

Some platforms let you swap collateral assets after borrowing. See ether outperforming? Swap some BTC for ETH without closing your credit line. Worried about a crash? Add more stablecoins to your collateral pool.

You can adapt as markets move.

Real-world example: Surviving a crash

Single-asset borrower: Pledges $50,000 in BTC. Borrows $25,000.

BTC drops 40% → Collateral now $30,000 → LTV climbs to 83.3%.

Right at the edge of liquidation risk. Only option: add more BTC or repay part of the loan. Might be forced to sell at a loss.

Multi-asset borrower: Pledges $30,000 in BTC, $10,000 in ETH, $10,000 in USDC. Borrows the same $25,000.

BTC drops 40%. ETH drops 30%. USDC stays flat.

- New collateral value: BTC $18,000 + ETH $7,000 + USDC $10,000 = $35,000.

- New LTV: $25,000 / $35,000 = 71.4%. Still under pressure, but below liquidation thresholds on many platforms.

Plus, they have options. They can strategically swap some of their depreciated BTC into more USDC to stabilize the pool further. Or they can use the USDC they already have as a buffer.

Same starting capital. Same loan. Completely different outcome.

Why platforms don't all offer this

Multi-collateral borrowing is more complex under the hood.

The platform needs to track multiple assets, calculate blended LTV ratios, handle different volatility profiles, and manage liquidation logic across a basket — not just one coin.

That's why many lenders stick to single-asset loans. It's simpler to build and easier to explain.

But simpler isn't always better. For borrowers who hold diversified portfolios, single-asset lending is a square peg in a round hole.

Multi-collateral in practice

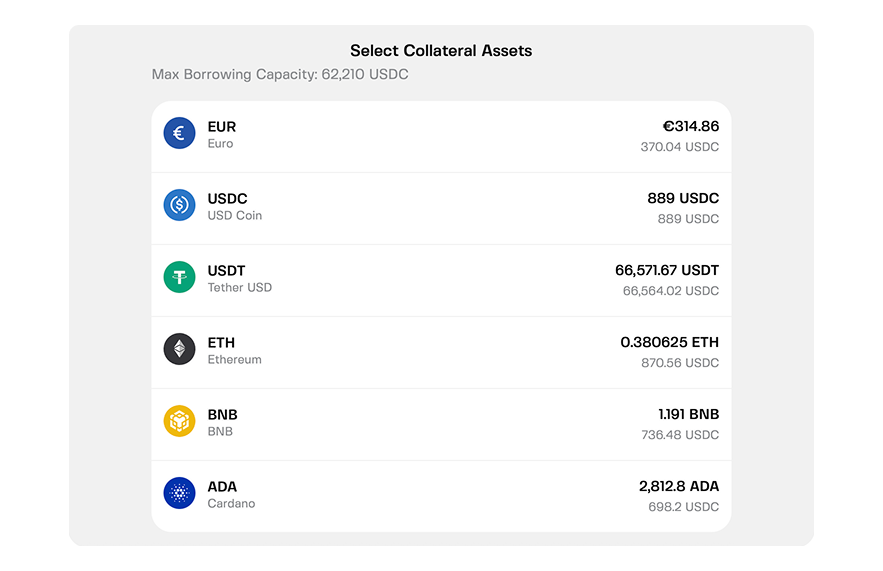

On Clapp, you can open a multi-collateral credit line using up to 25 different assets. BTC, ETH, stablecoins, even fiat — mix and match.

Keep your overall LTV at 20% or below? 0% APR.

And you can swap collateral anytime — even after borrowing. If market conditions change, you can rebalance your collateral by adding stablecoins or adjusting your exposure.

You're not locked into a single asset's performance. You can adapt as markets move.

Achieve more with a collateral bundle

Single-asset borrowing works. But if you hold more than one type of crypto, you're leaving flexibility on the table.

Multi-collateral borrowing lets you:

- Mix volatile and stable assets to smooth out risk

- Achieve better borrowing efficiency with stablecoins

- Swap collateral without closing your credit line

- Survive crashes without panic-selling

The crypto market doesn't move in straight lines — so your collateral strategy shouldn't either.

Don't put all your eggs in one basket. Spread your risk across assets that behave differently.

Frequently asked questions

1. Is multi-collateral borrowing riskier than single-asset?

Not necessarily. It depends what you pledge. A pool with stablecoins is safer than pure BTC — they're designed to hold their peg. The key is diversifying within your collateral, not just adding more of the same volatile asset.

2. Can I withdraw one asset from my collateral pool?

Depends on the platform. Some allow partial withdrawals if your LTV stays safe. On Clapp, you can add or remove assets anytime as long as your remaining collateral still covers your loan.

3. How are LTV ratios calculated across different assets?

Usually a blended LTV based on the weighted average of each asset's individual LTV. For example, if BTC has 60% LTV and USDC has 90% LTV, a 50/50 pool would have roughly 75% blended LTV. The platform handles the math for you.

4. What happens if one of my collateral assets crashes?

Your blended LTV rises, but typically less than if all your collateral was in that one asset. You'll receive the same warnings — add more collateral or pay down the loan. But you have more tools to respond, like swapping the crashing asset for a stable one.

5. Do I pay more interest on multi-collateral borrowing?

No. Interest is based on your total borrowing and LTV, not on how many assets you've pledged. Some platforms even reward lower LTV with 0% APR regardless of how many assets are in your pool.