Crypto loans 101: What first-time borrowers learn the hard way

The best loan is one you never have to stress about.

Borrowing against crypto sounds perfect. Instant liquidity while your coins keep working for you. No credit checks, no paperwork. No selling, no tax event.

But the ads leave out the late-night LTV alert, the scramble to add funds, and that gut punch when you realize you pushed things too far.

For first-time borrowers, crypto loans come with a learning curve — sometimes a painful one. This guide breaks down the risks hidden in the fine print and the rookie mistakes to avoid.

TL;DR

- Crypto loans are over-collateralized. You borrow less than you pledge. That's the trade-off for no credit checks.

- LTV is everything. Lower ratio = safer loan. 20–30% is the sweet spot for most people.

- Markets move fast. Your 50% LTV today could be 80% tomorrow. Have a plan.

- Liquidation isn't a threat — it's a promise if you ignore the warnings.

- Read the fine print. Some platforms charge fees you don't expect.

Where crypto loans win

You deposit crypto into a platform's wallet or smart contract. That's your collateral. Based on its value, the platform lets you borrow a percentage — usually 50–70%.

Let's start with the upsides.

Crypto-backed loans are approved based on your collateral alone — no credit history needed. They're faster and much more accessible compared to traditional bank loans.

You get funding in seconds or minutes. Access cash without triggering capital gains taxes or losing potential future price appreciation.

No credit checks. Your collateral is the only thing that matters. No income verification, no FICO score, no "we'll get back to you in 7–10 business days."

You keep your upside. If your collateral's price doubles while you have a loan, you still benefit. You never sold, so there's no tax to pay.

Borrowing costs less. Due to being over-collateralized, these loans can offer lower rates than traditional unsecured loans.

As of May 2026, personal loan rates in the US generally stand at 6.20%-35% APR (Annual Percentage Rate). For crypto, this ranges from 6% to 22% APR, depending on collateral — but conservative borrowers may also unlock 0% APR on some platforms.

Crypto loans aren't for maxing out

Borrowers can often secure up to 86% of their collateral value, but that's rarely a wise move.

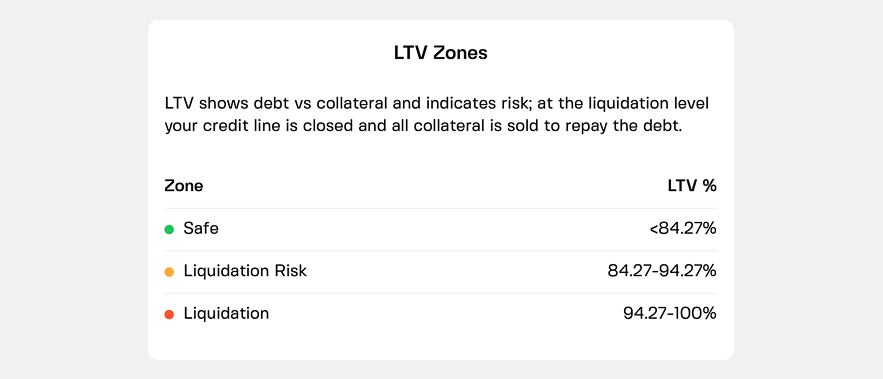

That percentage is called LTV, or loan-to-value ratio. And because crypto is volatile, keeping it low is your best defense.

Push LTV too high, and the platform may sell your collateral to cover the loan. That's liquidation.

If your collateral drops in value, your loan stays the same. The buffer protects the lender — and also protects you from instant liquidation.

Borrow $5,000 against $10,000 in BTC? That's 50% LTV. Borrow $2,000 against $10,000? That's 20% LTV — much safer.

LTV pitfalls you can't afford to ignore

Here's what first-time borrowers miss.

Your LTV doesn't stay still. Markets move — and your collateral shifts with them. Price declines cause LTV to expand, climbing toward the liquidation threshold.

You can't just "wait it out" indefinitely. If the market stays down and you have no extra collateral, the platform will sell your assets to cover the loan. At the worst possible moment.

You borrow at 40% LTV. Comfortable, right? Think again:

- The market drops 30%. Your LTV jumps to about 57%. That might still be safe, but you're closer to danger.

- The market drops 50%. You're at 80% LTV — liquidation territory.

That said, liquidation isn't an instant wipeout — at least in CeFi. Most platforms send warnings first.

Those are called margin calls. They are triggered when your collateral value falls close to the liquidation threshold, and you’re asked to add funds or reduce your loan. Your LTV is what determines how close you are to that point.

Margin calls may give you 24–48 hours to act. Add collateral, pay down the loan, or risk losing your crypto. But ignore the warnings? Your assets get sold, often at a loss, and sometimes with an extra fee.

Fees on top of interest: Read the fine print

Your loan can cost you more than just the interest rate.

- Origination fees. Some platforms charge a percentage just to open the loan. Usually 0.5–2%.

- Hidden spreads. The exchange rate when you borrow stablecoins might not be market rate. A 0.5% spread here, a 1% spread there — it adds up.

- Liquidation fees. If you get liquidated, some platforms charge an extra fee on top of selling your collateral. Read the terms.

- Unstaking costs. If your collateral is staked, unlocking it might take days and cost gas fees.

The good news is some platforms keep it simple and show all costs upfront.

The 20% rule that saves beginners

Here's a rule of thumb that works for most first-time borrowers.

Borrow at 20% LTV. Not 50%. Not 60%.

At 20% LTV, Bitcoin needs to drop about 75% to liquidate you. That's survived every crash in crypto history except the very first one.

At 50% LTV, a normal bear market (40–50% drop) puts you dangerously close to liquidation.

The tradeoff (and bottom line) is this: borrow less to sleep better.

And on platforms that offer 0% APR at low LTV, borrowing less doesn't even cost you interest.

Your best loan might not be a loan at all

Your collateral stays locked until you repay. If an opportunity comes up, you can't access it. And if you only pledged one asset, your loan's fate is tied to that single coin's price swings.

Different platforms structure borrowing differently. Some rely on fixed-term loans, while others offer more flexible credit line models.

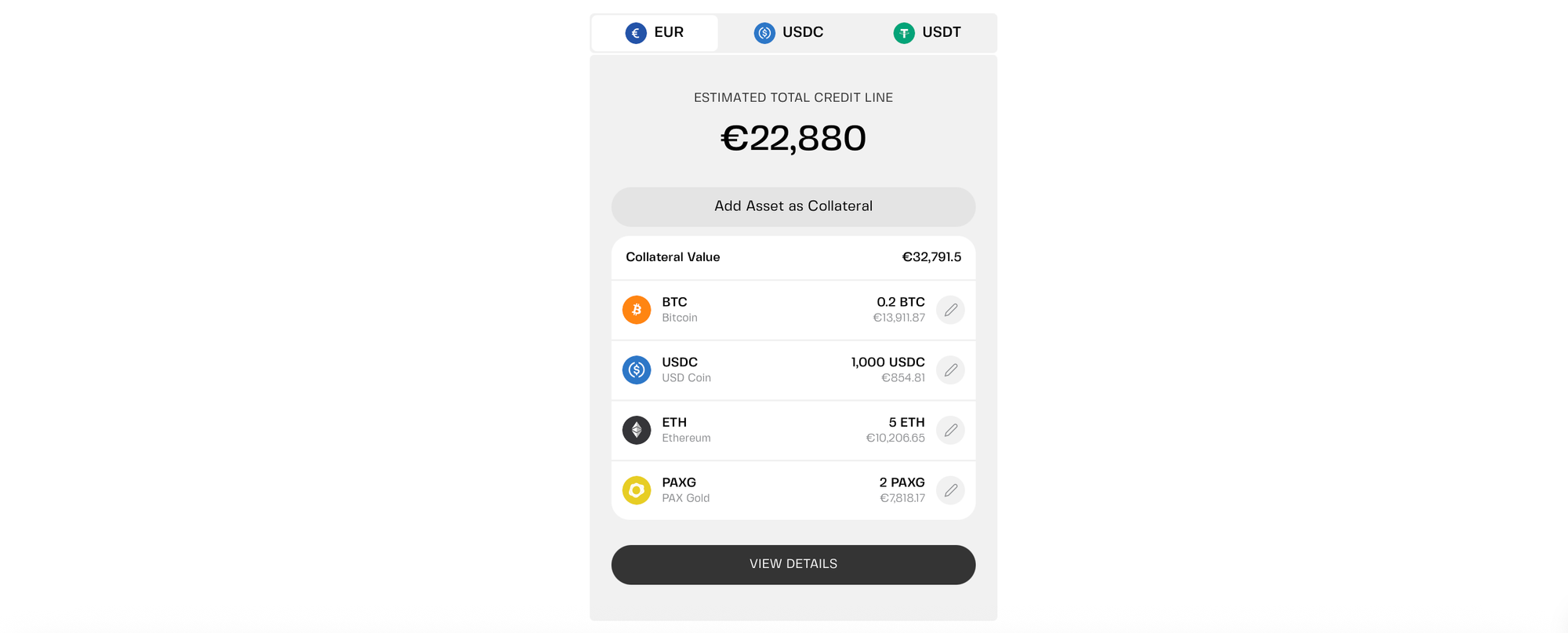

One example is a multi-collateral credit line, where multiple assets back a single borrowing limit.

You're not locked into a fixed term. Borrow when you need to, pay back when it suits you. Your collateral stays accessible — you can even swap assets without closing the line.

Most importantly, there's no fixed repayment schedule. Just keep your LTV in the safe zone, and you stay in control.

Example: How Clapp handles it

On Clapp, you can deposit up to 25 different assets as collateral — BTC, ETH, stablecoins, even fiat. Your LTV determines your rate.

At lower LTV levels (20% or below), APR drops to 0%.

Because it's a credit line (not a fixed loan), you only pay interest on what you actually use. Your liquidity is on hand when you need it, with collateral you can mix and match as markets move.

Like any crypto borrowing product, it still requires risk management, especially in volatile markets where LTV can shift quickly.

What to do before you borrow

Ask yourself these three questions.

1. Do I really need this money? Borrowing against crypto is for liquidity, not gambling. If you're borrowing to buy more crypto without a clear plan, that's leverage — not a loan.

2. Can I handle a 30% drop? Assume the market will move against you. What's your LTV after a 30% crash? Do you have extra collateral to add? Cash to pay down the loan?

3. What's my exit plan? When will you repay? How? What if the loan runs longer than expected?

If you can't answer these, you're not ready.

A first-time borrower's checklist

Before you click "borrow," run through this list.

- LTV at 20–30% — not higher

- Extra collateral ready — stablecoins in savings, more BTC on the side

- Know the fees — interest rate, origination, liquidation

- Understand the warnings — margin call thresholds, notification methods

- Plan for repayment — timeline, source of funds

Do this, and you're ahead of most first-time borrowers.

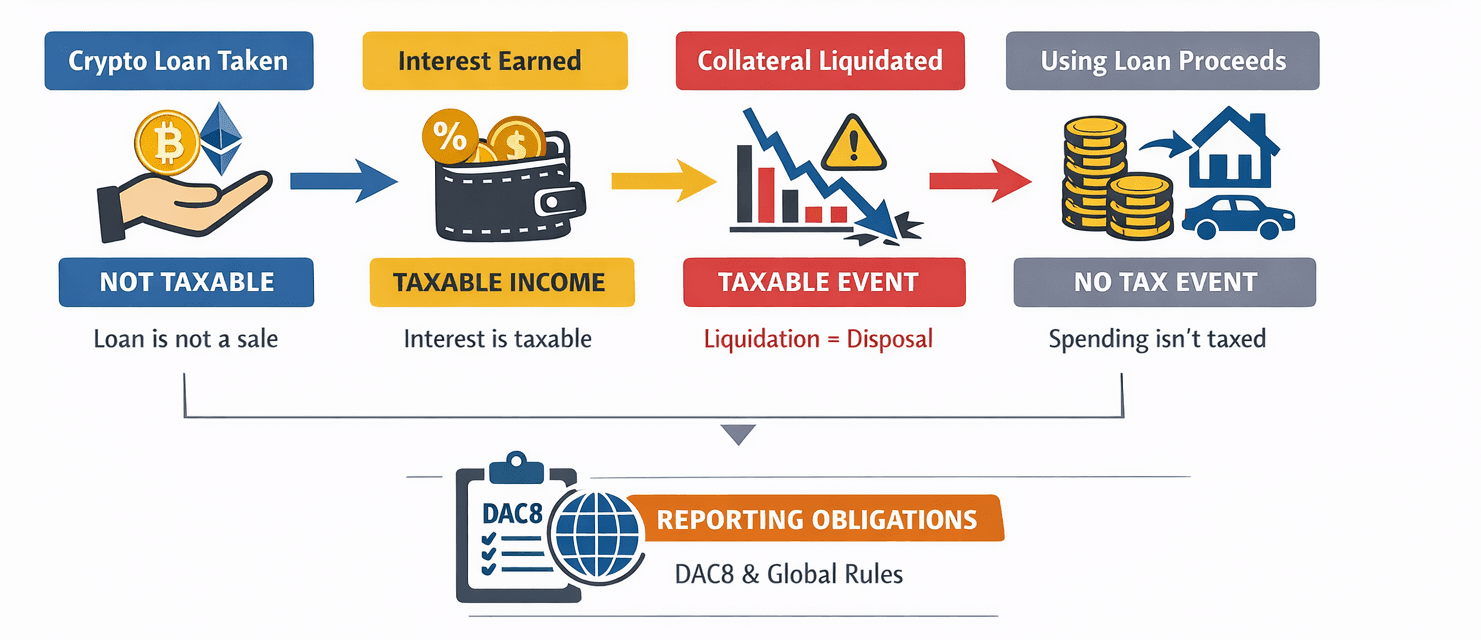

Plus, remember that getting liquidated not only hurts — it is also a taxable event like any crypto sale.

Crypto loans aren't magic

They let you access cash without selling your conviction. But the hidden risks — volatile LTV, margin calls, liquidation fees — catch first-time borrowers off guard.

They don't have to catch you.

Borrow conservatively. Keep LTV low. Have a backup plan. Read the fine print.

Some lending models give you more breathing room. That's worth understanding before you choose.

Frequently asked questions

1. What's the difference between a crypto loan and a credit line?

A loan gives you a lump sum with fixed repayments. A credit line gives you a pre-approved limit — draw what you need, pay interest only on what you use. Credit lines are more flexible for ongoing liquidity needs.

2. Can I lose my crypto if I borrow against it?

Yes — if you ignore margin calls and get liquidated. But if you borrow conservatively (low LTV) and stay on top of notifications, you can avoid it. Most liquidations happen to people who borrowed at high LTV and didn't act when markets moved.

3. Do I have to pay taxes when I borrow?

In most jurisdictions, no. Borrowing against crypto isn't a sale, so it's not a taxable event. But interest payments, liquidations, or swapping collateral could trigger taxes. Check local rules.

4. What happens if I can't repay?

You have options. You can add more collateral, repay part of the loan, or in some cases, request an extension. If you do nothing and your LTV climbs too high, the platform may liquidate your collateral to cover the debt.

5. Is borrowing against crypto better than selling?

Depends on your goals. Selling is permanent — you lose your position and trigger taxes. Borrowing lets you keep your crypto and defer taxes. But borrowing comes with risk (interest, liquidation). For long-term believers who need short-term liquidity, borrowing often wins.