How much crypto do you actually need before savings products become worth it?

How much do crypto yield rates really add to your portfolio?

8% APR sounds great — but if you're sitting on a modest stack, you might wonder whether it actually moves the needle.

Do you need $50,000 before crypto savings start making a difference? $10,000? Or can smaller amounts still compound into something meaningful over time?

Marketing aside, let’s look at the real numbers across different balances, timeframes, and savings products.

TL;DR

- You don't need a fortune to start. Small amounts grow over time. $100 earning 5% becomes about $128 after five years. Not life-changing, but better than leaving it idle.

- The habit matters more than the amount. Starting early and adding regularly usually beats waiting until you have "enough."

- Fixed savings can offer higher returns. The minimum deposit is often lower than people expect (on Clapp, $250 for Fixed Savings and $10 for Flexible Savings).

- Time matters more than size. The longer your assets stay invested, the more compounding works in your favour.

- Waiting for the "right amount" often means waiting too long.

First, zoom out

Most people focus on the interest rate. An advertised 8% sounds attractive, but the more practical question is whether the amount you actually earn is worth it.

If you put $100 into savings earning 5% a year, you'll make about $5 in the first year. That's hardly life-changing.

But looking only at the first year misses the bigger picture.

Savings products aren't just about today's yield. They're about putting idle assets to work, letting returns compound over time, and building liquidity that remains available for future opportunities. Even modest amounts become more meaningful when you give them enough time.

Let’s run the numbers

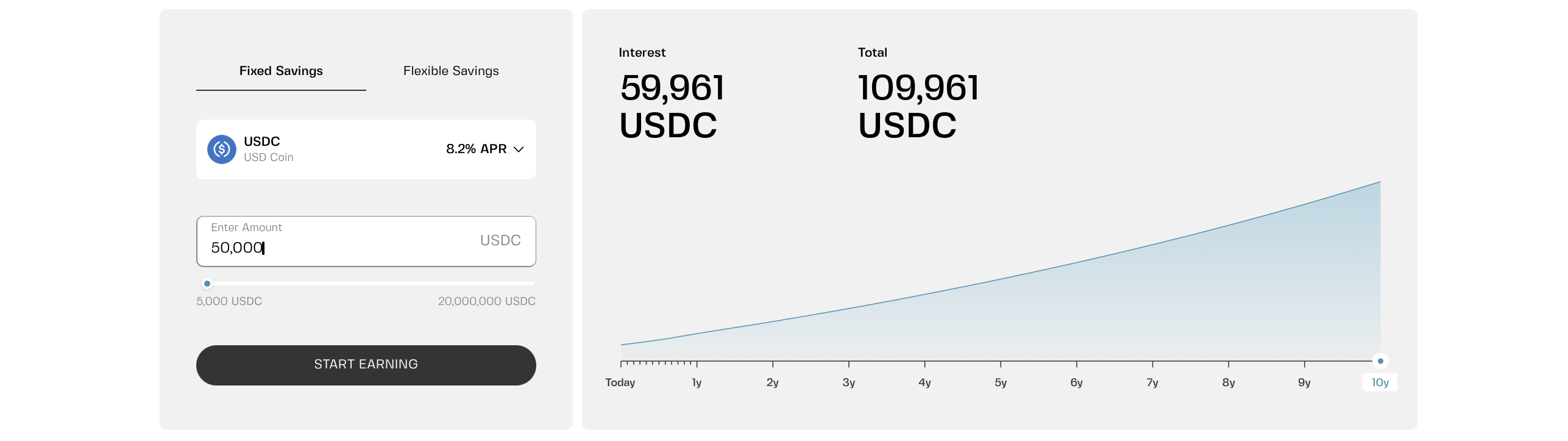

Here’s what different starting amounts look like at Clapp’s 8.2% APR over time.

On $100, the numbers stay small — about $8 in year one, $48 after five years, and roughly $120 after ten.

On $5,000, it starts to feel more meaningful — around $410 in year one and close to $6,000 after ten.

Scale that 10x, and you’re looking at roughly $4,100 in year one and about $60,000 over ten years.

APR or APY?

Yield on crypto products is usually shown in two ways: APR or APY.

- APR is the base rate — simple interest applied to your deposit. No compounding during the term.

- APY includes compounding. That means you earn interest not only on your initial deposit, but also on previously earned interest. Compounding can happen daily, weekly, or monthly depending on the product.

With fixed APR savings, there is no compounding during the term. Interest is calculated on principal only and paid at maturity. If you want to maximize returns over time, you can reinvest both principal and interest when each term ends — effectively creating compounding across cycles.

The habit matters more than the amount

Starting early matters just as much as starting big. Even small monthly deposits can compound into something meaningful over time.

Someone who starts with $1,000 and adds $20 every month will often end up ahead of someone who waits until they have $5,000 and never starts.

The difference isn’t the starting amount — it’s time in the market and consistency.

That’s where compounding actually shows up.

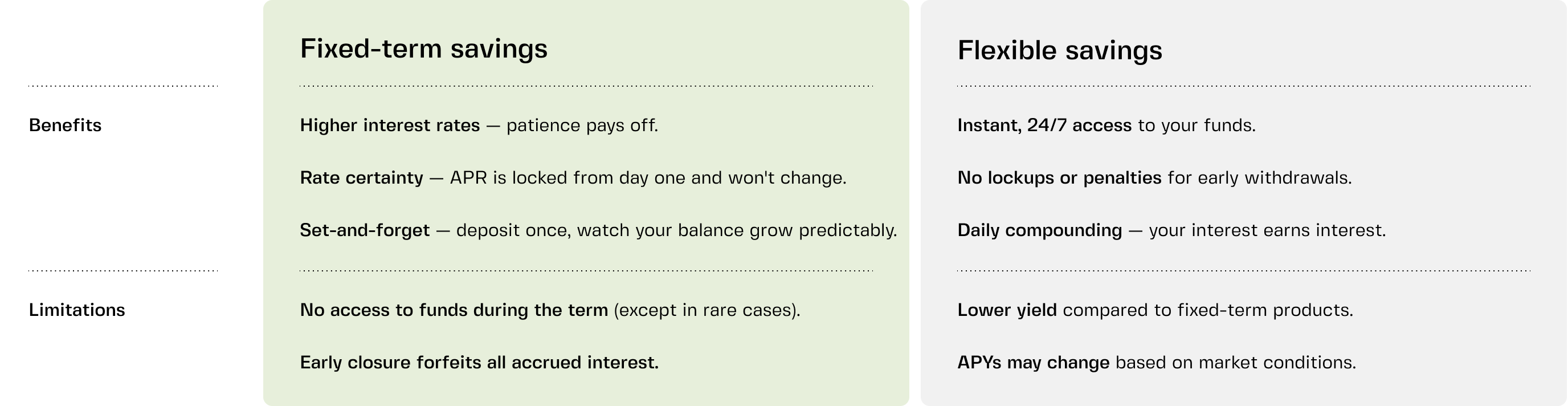

Fixed vs. flexible: different minimums, different purposes

Not all savings products are built the same — and the entry point isn’t either.

- Flexible savings usually have very low minimums. On Clapp, you can start from as little as 1o EUR or 10 USD equivalent (USDC, USDT, BTC, or ETH). Your funds stay accessible 24/7 while earning up to 5.2% APY with daily compounding.

- Fixed savings require a higher starting amount, because you’re committing funds for a set period — typically anywhere from a few months to a year. On Clapp, fixed savings start at 250 USD equivalent.

The trade-off is simple. Flexible savings prioritise access and instant liquidity, with low minimums and no lock-up. Fixed savings prioritise yield, offering higher rates (up to 8.2% APR) in exchange for time commitment and reduced access.

Explore our in-depth guide for a detailed comparison of these products.

Flexible savings: yield + liquidity

That $1,000 in Flexible Savings isn’t only earning ~5% APY. It’s also usable capital. It stays productive while remaining ready for whatever comes next.

- If a market opportunity appears, you can deploy it immediately.

- If your credit line LTV increases, you can move it into collateral in seconds.

- If you need cash fast, you can withdraw it without penalties or delays.

The yield is only one part of the equation. The real advantage is that your capital never sits idle — and never becomes inaccessible when you actually need it.

What's worth it?

“Is it worth it?” depends on what you're comparing it to.

- Compared to a bank account earning 0.01% APY, even $100 earning 5% makes a meaningful difference. You're earning hundreds of times more on idle capital.

- Compared to leaving assets unproductive, any positive yield improves capital efficiency.

- Compared to spending that $100 today, the answer depends entirely on personal priorities.

The real question isn't whether that yield on $100 in isolation. It's whether you're building a system where idle capital consistently works for you over time.

So, how much crypto do you really need?

There’s no magic number.

Whether you start with $100 or $100,000, the mechanics are the same. Bigger balances earn more, but the habit is what actually matters.

If you have $10, you can begin immediately. Flexible Savings has no meaningful entry barrier. Start small, add over time, and let compounding do its work.

If you have around $250 or more, fixed savings becomes relevant. Locking funds for 3–12 months typically offers higher yields — but only makes sense for money you’re confident you won’t need during that period.

Wealth isn’t built by waiting for the perfect amount to invest. It’s built by putting idle assets to work consistently over time.

Frequently asked questions

1. What's the minimum to start with crypto savings?

It depends on the platform. On Clapp, Flexible Savings starts at 10 EUR or the equivalent of 10 USD in USDC, USDT, BTC, or ETH. Fixed Savings starts at 250 USD equivalent.

2. Is it worth putting $100 in crypto savings?

Yes. The habit matters more than the amount. And 5% APY is better than 0.01% at a bank. Over time, that gap widens.

3. Should I wait until I have more money to start?

No, you can start with what you have and add regularly. Time in the market beats timing the market.

4. Can I add to my savings later?

Yes, because Flexible Savings lets you deposit anytime. Fixed Savings is a one-time deposit per term — you open a new term for additional funds.

5. Is there any risk to starting small?

Platform risk exists regardless of the amount. Choose a licensed, regulated platform with institutional custody and multi-layered security. The asset risk is the same whether you have $10 or $10,000.