Borrowing to buy more crypto: Genius move or gambling?

"Why doesn't everyone just borrow against their crypto to buy more crypto? Easy money, right?"

It's a fair question. On paper, the logic seems flawless: borrow cheap, buy more, get rich. So why isn't everyone doing it?

Let's break down the math, the psychology, and the very real risks. Because this move can work — but it can also wipe you out.

TL;DR

- Borrowing to buy more crypto is leverage. It amplifies gains — and losses.

- Works great when prices go up. Hurts badly when they don't.

- Keeping LTV low gives you a buffer. Borrowing at 20% LTV leaves room to breathe.

- Have a liquidation plan. Know your exit before you enter.

- It's not gambling if you manage risk. But most people don't.

The basic math

First, a quick refresher. All crypto loans are overcollateralized — you borrow less than you deposit. That ratio is called LTV (Loan-to-Value). The higher your LTV, the more risk you take and the more interest you pay.

Borrow $10,000 against $50,000 in crypto? That's 20% LTV — very safe. At that level, some platforms even offer 0% APR.

So here's the obvious question: if you can borrow cheaply against your crypto, why not use that money to buy more crypto and capture more upside?

This exact question pops up on Reddit a lot.

The logic sounds simple: borrow at 5%, earn 10–20% in price appreciation, pocket the difference. Easy money, right?

Not quite.

Let's say you have $50,000 in Bitcoin. You believe it's going to $100,000. You borrow $25,000 at 50% LTV and buy more BTC. Now you hold $75,000 worth of BTC.

But the BTC price can move either way:

- If it doubles, you make $75,000 instead of $50,000. That's the upside.

- If it drops 30%, your $75,000 worth of BTC becomes $52,500. You still owe $25,000 (plus interest), leaving you with about $27,500. That’s a ~45% loss on your original $50,000 — even though the market only dropped 30%.

The math works fine when prices go up. The problem is, nobody knows when they'll go down. And when they do, the losses accelerate.

Even if the price doesn’t drop, a flat market can still hurt you — interest keeps accumulating while your position goes nowhere. Time is not on your side.

At 20% LTV, you'd survive. But most people chasing "easy money" don't borrow that conservatively. That's why everyone doesn't do this.

How this works for the Reddit scenario

Suppose the ETH price is at roughly $2,000.

You have 5 ETH worth $10,000. You borrow at 40% LTV — that's $4,000 in USDT at 5% APR (depending on the platform). You use that $4,000 to buy 2 more ETH. Now you hold 7 ETH total.

Scenario A: ETH goes up 30% over the next year.

Your 7 ETH is now worth $18,200. You sell, repay the $4,000 loan plus $200 in interest. You're left with $14,000. Your original 5 ETH would have been worth $13,000. You made an extra $1,000. Great.

Scenario B: ETH drops 20% over the next year.

Your 7 ETH is now worth $11,200. You still owe $4,000 plus interest. Your net is about $7,000. Your original 5 ETH would have been worth $8,000. You lost an extra $1,000. Not great.

Now add liquidation risk. ETH drops 50% → collateral falls to $5,000 → LTV approaches liquidation threshold depending on platform rules → liquidation is triggered.

You don’t choose when to sell. The platform sells your ETH into a falling market, often locking in large losses at the worst possible time.

When it can work (the disciplined approach)

If you're going to do this, here's how to do it without becoming a cautionary Reddit post.

- Borrow conservatively. 20–30% LTV, not 50–60%. Gives you room to breathe. On platforms like Clapp, you can keep LTV at 20% and pay 0% APR.

- Have a thesis. Not "number go up." What specific catalyst? What timeline?

- Use a credit line, not a loan. That way, you will only pay interest on what you use. Draw as you go.

- Set a stop-loss. Know at what price you're wrong. Before you borrow.

- Keep dry powder. Have extra collateral ready for margin calls (stablecoins in savings, more BTC on the side, etc.).

- Don't borrow your whole limit. Just because they'll lend you $50k doesn't mean you should take it.

Keep it simple: lower leverage, more time to react, fewer forced decisions.

Example: You borrow $10,000 at 20% LTV against $50,000 in BTC. You buy more BTC. If Bitcoin drops 30%, your LTV climbs to about 25%. Still safe.

No margin call and no panic. There’s time to adjust — that’s what calculated risk looks like.

With a credit line at low LTV, you're not bleeding interest while you wait. And if markets move against you, you have time to add collateral or pay down the loan — not instant liquidation.

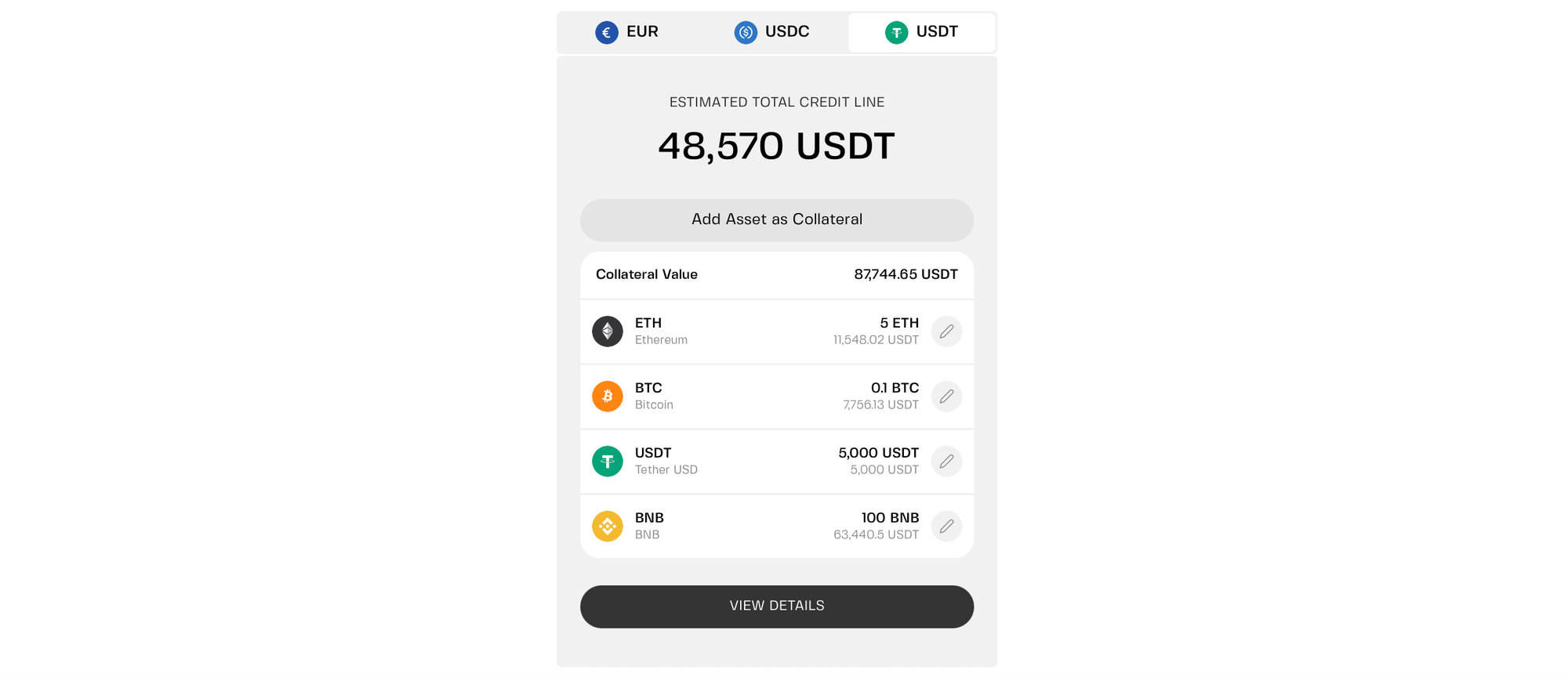

Multi-collateral credit lines give you even more room to maneuver. Bitcoin sliding? Add stablecoins to your collateral. Ethereum ripping? Swap into it without closing your line. You're not stuck waiting for liquidation — you can adapt as markets move.

When it's straight gambling

The "genius move" crowd only tweets about the wins.

When you borrow to buy more, you're now financially committed to a certain direction. Downward moves hurt more, margin calls add stress — and emotions run high.

People make bad decisions under stress.

They add more collateral when they shouldn't. They hold too long. They panic-sell at the worst moment. Or they get liquidated and lose everything.

- If you can't afford to lose what you borrow, you're gambling.

- If you don't have a clear exit plan, you're gambling.

- If you're borrowing because of FOMO, you're gambling.

Weigh up your liquidation risk

You borrow $25,000 at 50% LTV. Bitcoin drops 40%. Your collateral is now worth $30,000. Your LTV climbs to 83%. Liquidation happens.

The platform sells your collateral at market price — often during a crash, when liquidity is thin and prices are at their worst.

You lose your Bitcoin. The liquidation covers the loan, but you get nothing back — plus a taxable event from the liquidation.

That's the worst-case scenario. It happens every day in crypto.

Lower LTV changes the game

Here's why conservative borrowing matters.

At 20% LTV, you survive most crashes. At 60% LTV, a normal correction wipes you out.

The same trade and opportunity, but completely different risk profiles.

The bottom line

Borrowing to buy more crypto isn't genius or gambling. It's leverage. The outcome depends entirely on how you use it.

Use low LTV, have a plan, and keep reserves. That's calculated risk.

Max out your borrowing power with no backup plan? That's gambling.

Borrow conservatively and have a plan. Stay in the game long enough to see the next cycle.

Frequently asked questions

1. Isn't borrowing to buy more crypto just leveraged trading?

Basically, yes. But with a credit line, you're not forced to use all the leverage at once. You can draw gradually, pay interest only on what you use, and add collateral if needed. It's more flexible than a futures trade.

2. What's the safest LTV for this strategy?

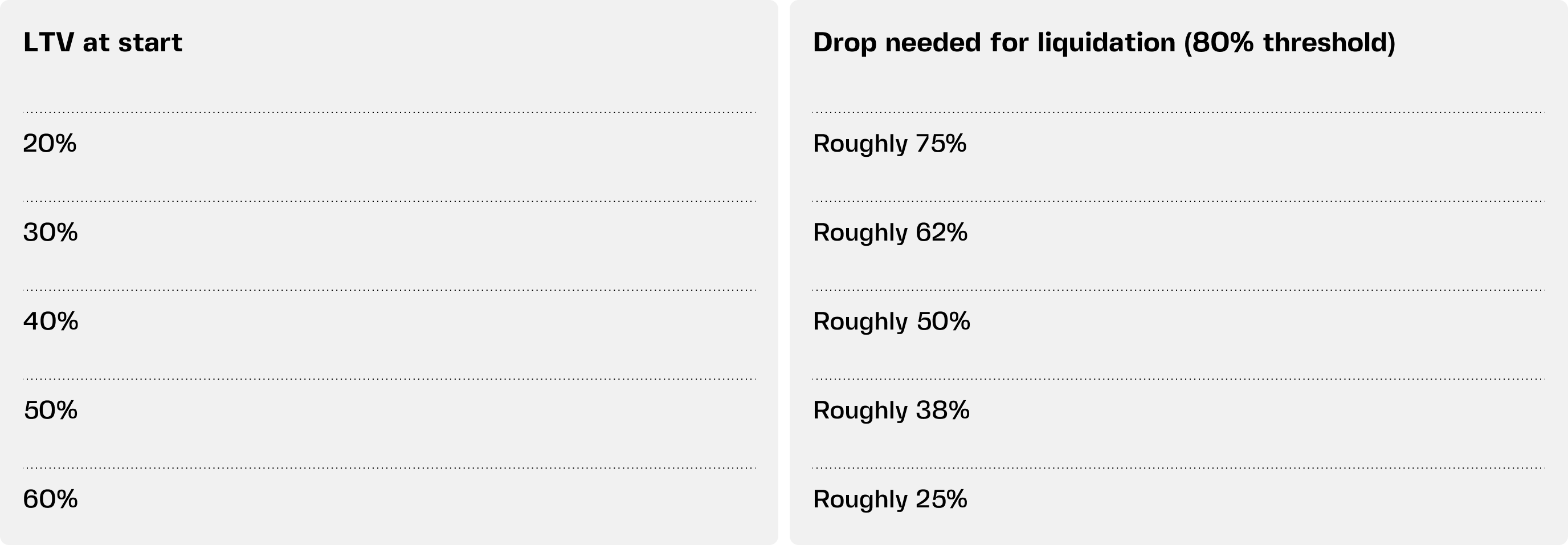

Generally, 20% or below. At 20% LTV, Bitcoin would need to drop about 75% before liquidation. That's survived every crash except an apocalyptic one. Higher LTVs get wiped out in normal bear markets.

3. Can I use the borrowed funds to buy different assets?

Yes. You're not forced to buy more of your collateral asset. Some people borrow against BTC to buy ETH, or against stablecoins to buy altcoins. Just remember — now you have two correlated risks.

4. What happens if I get liquidated?

The platform sells your collateral at market price to repay the loan. You get nothing back. It's a total loss of whatever you pledged. Plus, in most jurisdictions, liquidation counts as a taxable event.

5. Is this strategy worth it for small amounts?

The math works the same at any scale. But the emotional toll is different. Losing $500 hurts less than losing $50,000. Start small if you're experimenting. Learn the mechanics before you size up.