Stop letting your crypto sleep. Here's how to make it work 24/7.

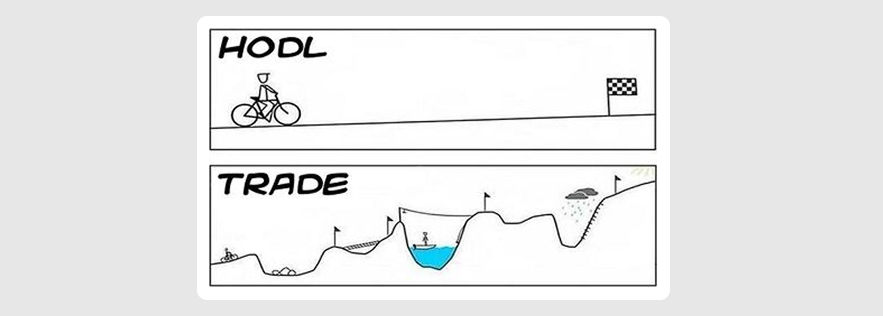

You've heard it a thousand times. "Just HODL."

Buy crypto. Wait. Hope. Repeat. Simple advice that worked for those who bought Bitcoin a decade ago.

But HODLing is just holding. It's not using. Your crypto sits there, doing nothing, while you wait for a price that may or may not come.

What if your assets could work around the clock?

Old way: Buy, hold, pray

Let's give HODLing its due. You buy coins, tuck them away, and ignore the daily chaos. Some people buy a little every month, maybe use a hardware wallet, and check the price once a quarter.

The upside: You don't lose sleep over a 20% dip. No transaction costs as coins sit idle.

The downside: Your crypto isn't earning anything. When a project fades or a crash drags on, your capital stays locked. No profits taken at the peak or liquidity for opportunities.

In practice, it's also emotionally harder than it sounds. When every X feed screams "bloodbath," staying calm takes real discipline.

So what's the alternative?

You don't have to choose between holding and trading. Let's look at ways to make your crypto earn its keep.

#1: Staking rewards — get paid to secure the network

Instead of letting coins gather dust, lock them up to help secure the native blockchain. The network pays you. Think of it like being a night watchman for a building you already own — except the building pays you in crypto.

How it works: Stake your coins with a validator or run a node of your own. Your assets help process transactions. In exchange, you earn rewards — usually 5%–15% annually.

Why people stake

- Passive income. Not trading, timing, or guessing.

- Energy efficient. A fraction of mining's environmental impact.

- Lower barrier than mining. Stake with a few taps (unless you run your own validator).

The trade-offs

- Volatility still applies. An 8% yield doesn't erase a 30% drop.

- Lock-ups. If the market crashes during a lock period, you can't sell.

- Slashing risk. If your validator messes up, you could lose part of your stake.

- Complexity. Running your own validator is a whole project. For the rest of us, it's about picking one with solid uptime and reputation.

#2: Crypto savings accounts — high yield, no fuss

If staking sounds too inflexible, here's something simpler.

Crypto savings products work like bank savings — except interest rates are higher. Instead of 0.01% APY (or 4% for some high-yield accounts), you're looking at 5%–8%.

How it works: You deposit crypto. The platform lends it out or stakes it. A slice of revenue comes back to you as interest. You do nothing.

Why people use crypto savings

- High rates. 5%–8% on stablecoins vs. 0.2% at a bank.

- 24/7 access. No bank hours. Funds available when you need them.

- Flexibility. Withdraw anytime or lock for higher rates.

- Passive income without complexity. Just deposit, earn, repeat. No DeFi jargon.

The trade-offs

- No FDIC insurance. Choose a transparent, regulated platform.

- Volatility still applies. ETH down 40%? Your 8% yield softens but doesn't erase it.

- Lock-ups. Higher rates often mean less access.

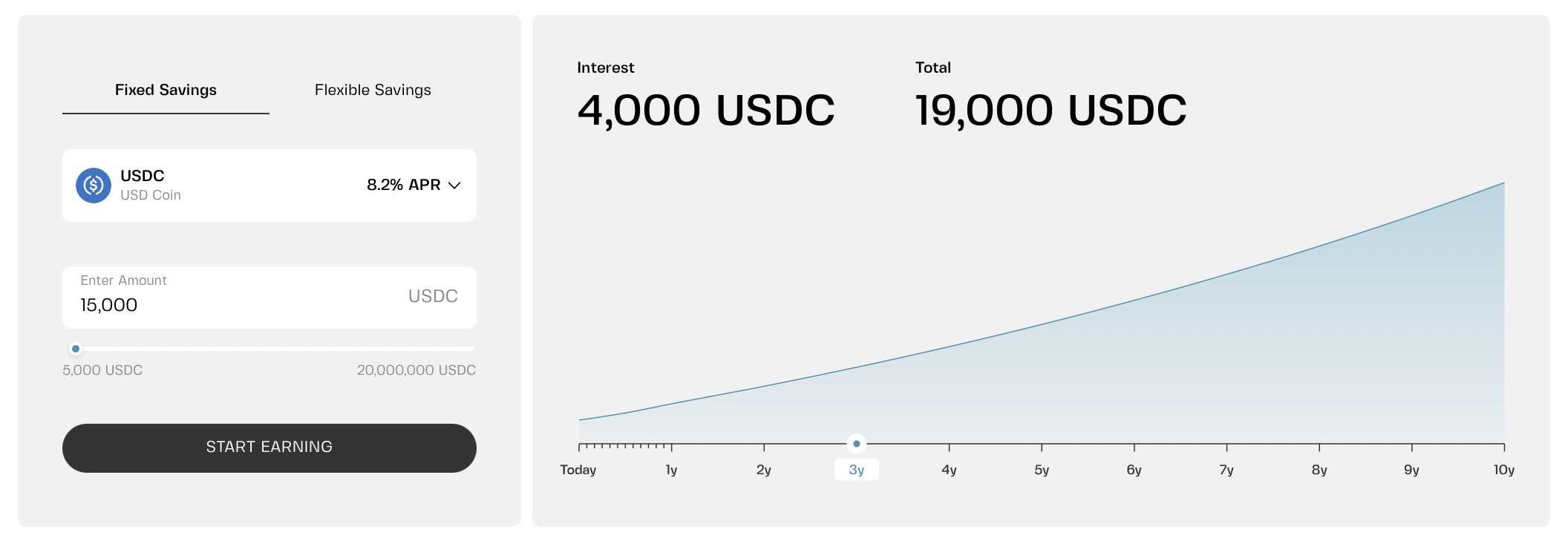

How to choose a savings product

- Flexible savings — withdraw anytime. Lower rates, liquid.

- Fixed savings — lock funds for 1–12 months. Higher, guaranteed rates.

On Clapp, Flexible Savings earns up to 5.2% APY on stablecoins and EUR — daily compounding, instant withdrawals. Fixed Savings locks in up to 8.2% APR for longer terms, rate guaranteed.

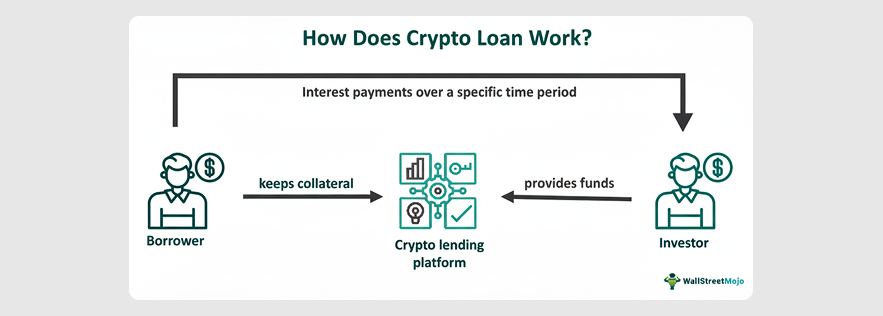

#3: Borrow against crypto — keep your coins, get the cash

When an art collector needs cash, they don't sell the masterpiece. They use it as collateral. Crypto finally caught up.

How it works: Deposit crypto as collateral. Borrow cash or stablecoins against it. Keep your crypto. When you repay, it comes back.

No sale means no tax event, and no regret when the price rallies without you.

Why people borrow

- Instant liquidity. No credit checks. Collateral is all that matters.

- Avoid capital gains tax. Borrowing isn't a sale.

- Keep your upside. If Bitcoin doubles, you're still holding.

- Lower rates. Over-collateralized loans can be competitive. 0% APR possible with low LTV (e.g., 20% on Clapp).

The trade-offs

- Liquidation. If collateral drops, the platform may sell to protect itself. Get warnings first — add collateral or pay down.

- Over-collateralization. Want $10,000? You might need $20,000–$30,000 in crypto.

- Platform risk. Choose a transparent, regulated provider.

Loans vs. credit lines

- Crypto loans — lump sum, fixed repayment, collateral locked. Simple, rigid.

- Crypto credit lines — pre-approved limit. Draw what you need. Pay interest only on what you use. Repay anytime. Flexible, adaptable.

On Clapp, open a multi-collateral credit line using up to 25 assets. Swap collateral anytime without closing your line, while paying nothing until you use it.

#4: DeFi yield farming — for the adventurous

If staking is a steady job and savings accounts are a reliable side hustle, yield farming is like playing poker where the rules change every hour. The upside can be spectacular; the downside can be brutal.

How it works: You deposit crypto into a liquidity pool — a shared pot that powers decentralized exchanges. When people trade, you get a cut of fees. Sometimes you also earn governance tokens that might become valuable later.

In bull markets, yields can hit 100% APY or more. In bear markets, you can lose money even if the token price goes up. This is not an emergency fund.

Why people farm

- High potential returns. Double or triple-digit APY.

- Passive income on steroids. Your crypto works across multiple protocols.

- Governance tokens. Extra upside if they appreciate.

The trade-offs

- Impermanent loss. Deposit two tokens. If one moons relative to the other, you end up with less of the winner.

- Smart contract bugs. DeFi code may have bugs. No customer support if exploits happen.

- High gas fees. Entering and exiting pools can cost hundreds on Ethereum.

- Complexity. You need to monitor, chase yields, move funds.

So which one is right for you?

Your crypto doesn't have to sit idle. Whether you're a "set it and forget it" type or someone who enjoys chasing opportunities, there's a way to make your assets work while you wait.

Some people keep the bulk of their holdings in savings — earning steady yield without lifting a finger. Others stake a portion for network rewards. The "right" strategy depends on your goals, risk tolerance, and how hands-on you want to be.

Frequently asked questions

1. Is staking better than crypto savings?

Depends what you want. Staking usually offers higher yields (5%–15%) but may come with lock-up periods and slashing risk. Savings accounts are simpler, often more flexible, and you're not tied to a specific blockchain's performance. Many people do both.

2. Can I lose my crypto if I stake or save?

Yes — but the risks are different. With staking, your assets are locked and could be slashed if the validator misbehaves. With savings, the main risk is platform failure. That's why choosing a transparent, regulated platform matters. Neither is risk-free, but they're far safer than yield farming.

3. What's the catch with 0% APR credit lines?

You need to keep your Loan-to-Value (LTV) low — usually 20% or below. Borrow conservatively and your credit line costs nothing. Borrow more aggressively, and interest kicks in. It's a reward for responsible borrowing.

4. Do I have to pay taxes on staking and savings rewards?

In most countries, yes. Staking rewards and interest earned are typically treated as taxable income. The rules vary by jurisdiction, so check with a local tax professional. Keep records — you'll thank yourself later.

5. Which strategy should a beginner start with?

Crypto savings is the simplest entry point. No lock-ups (with Flexible Savings), no technical knowledge required, and you can start with as little as €10. Once you're comfortable, explore staking. Leave yield farming until you've got serious experience and risk tolerance.