What would happen if you never touched your crypto for 10 years?

We've all heard the stories. Someone bought Bitcoin years ago, forgot about it, and came back a decade later to discover it had become a fortune.

It's the ultimate HODL story: buy, wait, don't touch anything.

But here's a question that's more relevant today: If you were investing for the next 10 years — not the last 10 — would simply doing nothing still be your best strategy?

Holding can be powerful. But price appreciation isn't the only way a portfolio can grow, and it's certainly not the only thing that matters over a decade.

Let's compare three different approaches and see how each one performs over the long run.

TL;DR

- Holding crypto can deliver strong returns — but you're relying entirely on price appreciation.

- Savings generate steady yield while keeping part of your portfolio productive.

- Credit lines provide liquidity without forcing you to sell during difficult markets.

- The strongest long-term strategy isn't choosing one approach — it's combining all three.

- Over a decade, flexibility can be just as valuable as returns.

Scenario 1: Buy crypto and do nothing

Suppose you buy $10,000 worth of crypto today and don't touch it for the next ten years.

What happens next depends entirely on what you own. Some assets may outperform dramatically. Others may barely move. Some may not survive the next market cycle.

Bitcoin offers a useful example. Over the past decade, it has returned more than 8,000% overall. A $10,000 investment made ten years ago would be worth roughly $850,000 today.

But hindsight is easy.

The real question isn't just about uptrends. It's whether your assets do anything for you while you wait. If your strategy is simply to buy and hold, every dollar of your return depends on market appreciation alone. This means:

- Your assets aren't generating additional income.

- You don't have liquid reserves if an opportunity appears.

- If you suddenly need cash, your main option is to sell — potentially giving up future upside and triggering a taxable event in many jurisdictions.

Holding can be a perfectly valid long-term strategy. But it isn't the only way to put your portfolio to work.

Scenario 2: Prioritize steady growth

Now imagine taking the same $10,000 and allocating it to stablecoins earning around 5% APY. Unlike Bitcoin or ether, stablecoins aren't designed to appreciate. Their value stays close to the underlying fiat currency.

Instead, the return comes from yield. After ten years, $10,000 earning 5% APY grows to roughly $16,500 through compounding alone. Add regular monthly contributions and the difference becomes even more meaningful.

The upside is predictable growth with significantly lower price volatility. The downside is equally obvious. If Bitcoin has another exceptional decade, you'll miss much of that upside.

If you choose this route, you'll usually have two options.

- Flexible savings let you withdraw your assets whenever you need them while continuing to earn yield.

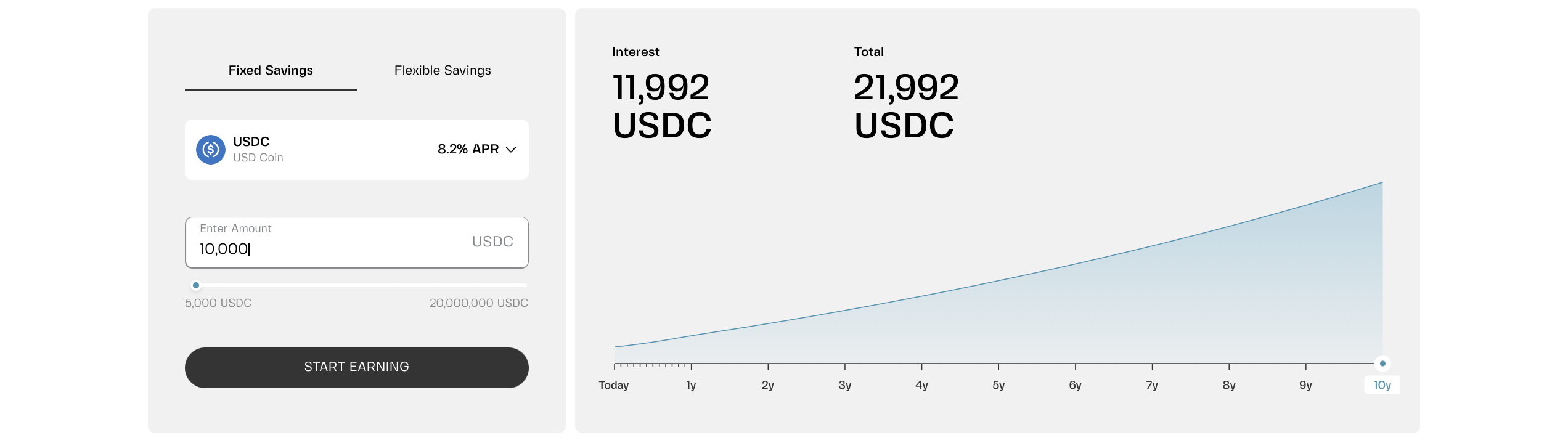

- Fixed-term savings typically offer higher rates (for example, up to 8.2% APR on Clapp) in exchange for locking your funds for a predefined period. Although interest doesn't compound during each term, you can reinvest principal and interest when the term ends.

Many investors use both: flexible savings for liquidity and fixed savings for money they know they won't need anytime soon.

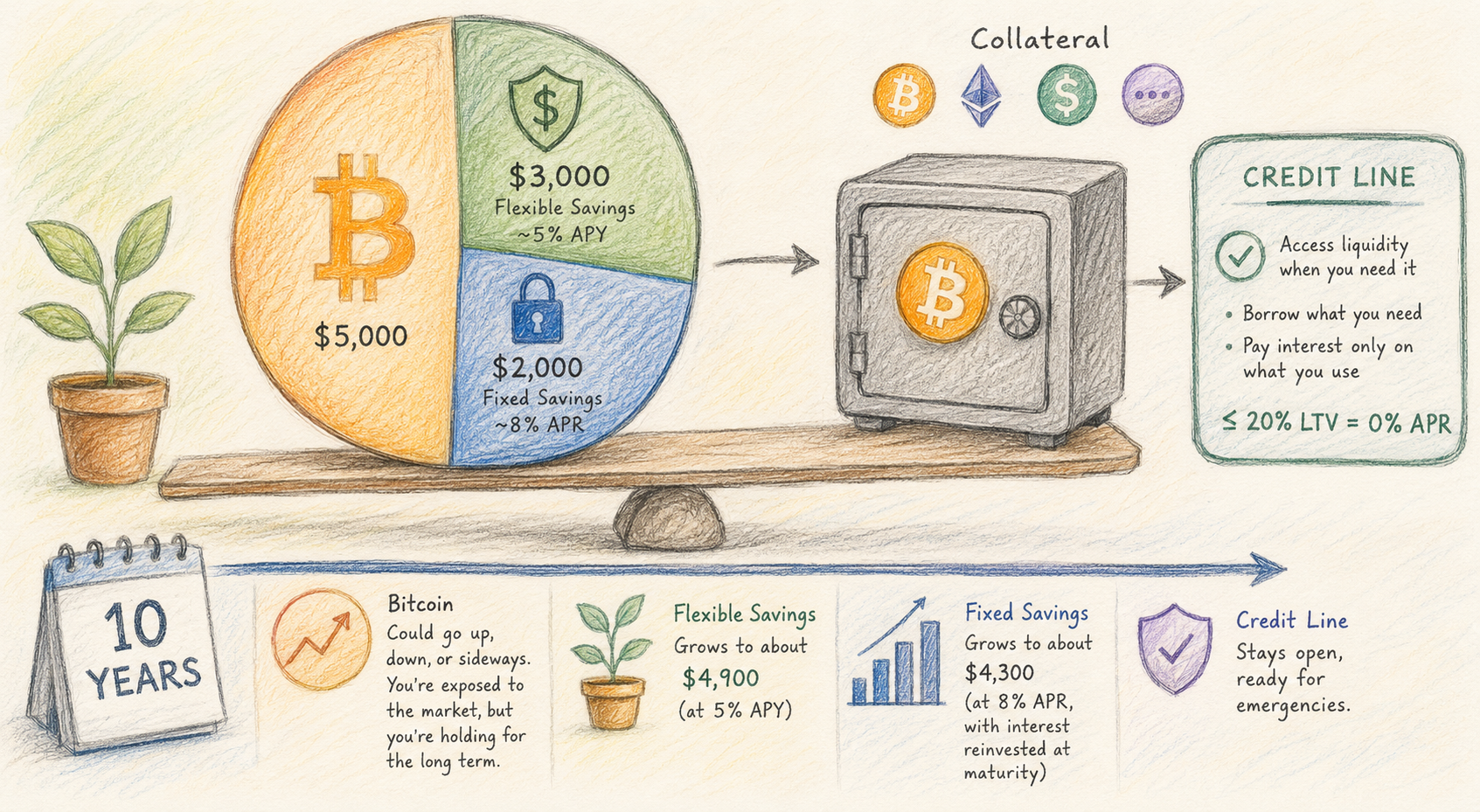

Scenario 3: Build a balanced portfolio

Instead of choosing between growth and stability, you combine both. For example:

- Keep $5,000 in large-cap coins like Bitcoin for long-term upside.

- Allocate $3,000 to flexible savings earning around 5% APY (buffer).

- Place another $2,000 into fixed-term savings for a higher yield (8% APR).

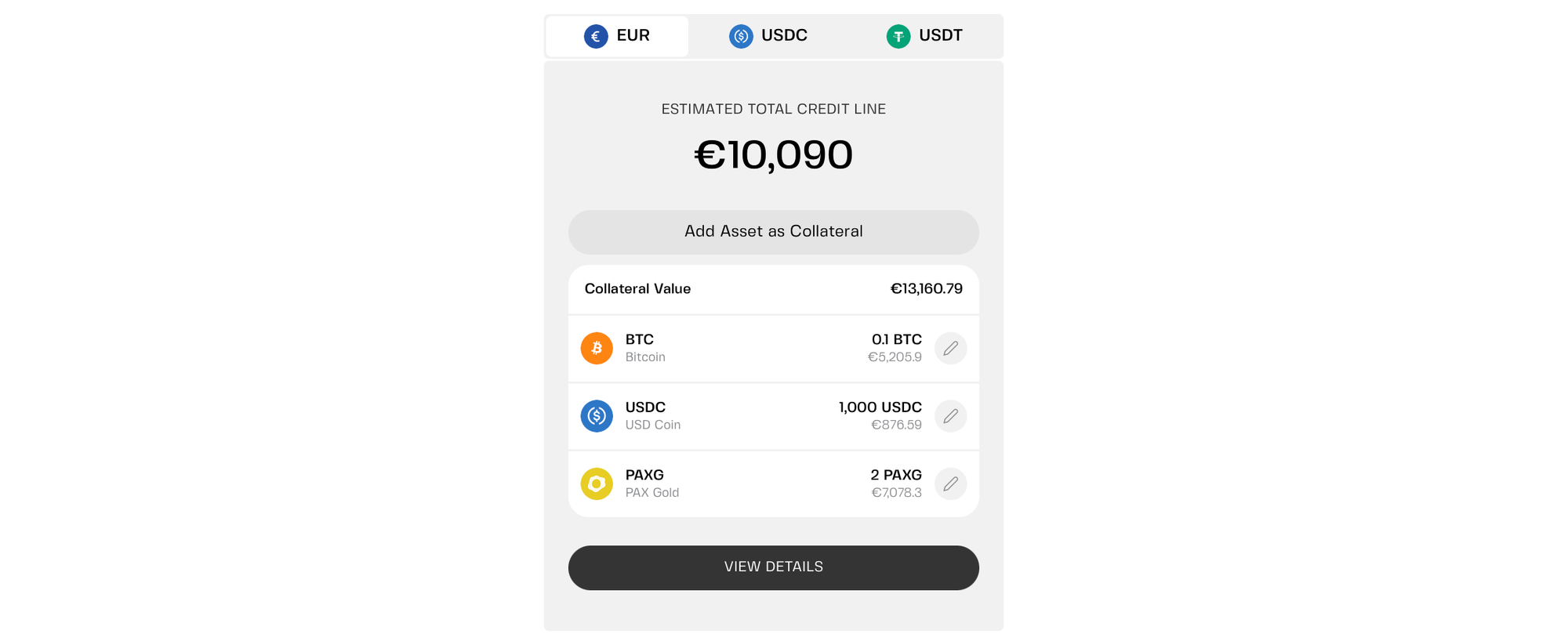

- Open a credit line backed by your Bitcoin at a conservative LTV.

What happens over 10 years?

- Your Bitcoin could go up, down, or sideways. You're exposed to the market, but you're also holding for the long term.

- Your flexible savings grow to about $4,900 (at 5% APY).

- Your fixed savings grow to about $4,300 (at 8% APR, with interest reinvested at maturity).

- Your credit line stays open, ready for emergencies.

Total value (excluding Bitcoin price changes): You've grown your cash portion from $5,000 to over $9,200. You still hold your Bitcoin and have a credit line available if you ever need liquidity.

That's the advantage of a balanced approach. Instead of relying on a single outcome, you're combining three different sources of value: long-term upside from Bitcoin, steady growth from savings, and on-demand liquidity through a credit line.

Why a credit line?

Your Bitcoin serves as collateral, giving you access to liquidity without selling. You don't have to borrow immediately — but the liquidity is there if you need it.

Unlike a traditional crypto loan, a credit line doesn't lock you into a fixed repayment schedule. You draw only what you need, repay on your own terms, and pay interest only on the amount you actually use.

On Clapp, borrowing at 20% LTV or below comes with 0% APR. And if it's a multi-collateral credit line, you can add, remove, or swap collateral assets without closing your position.

One note on collateral. Relying on Bitcoin alone for your credit line puts your entire position at the mercy of BTC's price swings. A more resilient approach is to mix assets — stablecoins, BTC, ETH, or other supported tokens — in your collateral pool. That way, if one asset drops, others can help stabilize your LTV.

Comparing the approaches

Each strategy optimizes for something different.

Do nothing

- Maximum exposure to Bitcoin's price

- No yield

- No dedicated liquidity buffer

Yield only

- Predictable compounding

- Lower volatility

- Limited exposure to crypto upside

Balanced approach

- Exposure to long-term appreciation

- Ongoing yield

- Liquidity available without selling

- Greater flexibility during market swings

None of these approaches is universally "best." They simply prioritize different outcomes.

Why flexibility matters

Ten years is a long time. Markets rise and fall. Emergencies happen. New investment opportunities appear.

A portfolio built entirely around long-term appreciation may eventually produce excellent returns. It can also leave you with difficult decisions whenever you need liquidity.

Keeping part of your portfolio accessible while another part compounds can make those decisions much easier.

This way, you build a portfolio that can adapt regardless of what happens. That's the ultimate goal, because nobody can predict the next decade.

How this can work on Clapp

Clapp combines the building blocks in one ecosystem.

- Flexible Savings lets idle assets earn yield while remaining available for withdrawal.

- Fixed Savings offers higher rates for funds you're comfortable locking for longer periods.

- Credit Lines provide liquidity without selling your crypto, while multi-collateral support makes collateral management more flexible.

You don't have to choose just one product. Many investors use them together as different parts of the same long-term strategy.

What this means for you

Time is one of the most powerful forces in investing. Whether your portfolio benefits from that time depends on more than just price appreciation.

The do-nothing approach leaves you entirely at the mercy of the market. The balanced approach gives you growth, protection, and optionality.

Holding long-term assets can provide upside. Savings can generate predictable yield. Credit lines can provide liquidity without forcing you to sell.

Used together, they create a portfolio that's better prepared for whatever the next decade brings.

Frequently asked questions

1. Is Bitcoin a good 10-year hold?

That depends on your conviction. Historical returns have been strong, but past performance doesn't guarantee future results. The best approach is to hold Bitcoin as part of a diversified strategy — not your entire portfolio.

2. Should I put all my money in stablecoin savings?

That's safer than Bitcoin in terms of price volatility, but you'll miss out on potential upside. A mix of both gives you growth potential and steady yield.

3. What's the best way to earn yield without locking my funds?

Flexible savings. No lock-ups, withdraw anytime. On Clapp, that's up to 5.2% APY on stablecoins and EUR.

4. How do I protect my crypto during a crash?

Keep LTV low on your credit line, have dry powder in savings, and don't panic-sell. A balanced approach is your best protection.

5. Do I really need a credit line if I have savings?

Yes. A credit line gives you liquidity without selling your assets. Savings give you yield and a buffer. They work together — not instead of each other.