The 3-question test: are you ready to borrow against crypto?

You've seen the tweets. "Just borrowed against my ETH, bought a boat, living my best life." Sounds simple, right? Deposit crypto and get cash without triggering a tax event.

But here's what those tweets don't show: the sleepless nights when markets drop 20% overnight. The moment of panic when you realize you borrowed more than you should have.

Borrowing against crypto isn't complicated, but doing it smartly takes a minute of honest self-reflection.

TL;DR

- Crypto loans aren't for gambling — be reasonable.

- LTV is everything — lower = safer; 20–30% is the sweet spot.

- Assume a 30% drop can happen overnight — have a backup plan.

- 0% APR exists — keep LTV low and borrow for free.

- Borrow what you need, not what they’ll give you.

Before you open that loan or credit line, ask yourself three questions.

Question 1. Why do I actually need this money?

This sounds obvious, but it's where most people trip up.

Legitimate reasons to borrow:

- You need cash for a planned expense (home repair, education, business opportunity).

- You want liquidity without selling — no tax event, no missed upside.

- You need funds fast, without credit checks or paperwork.

Questionable reasons to borrow:

- "I want to leverage up and gamble on a memecoin."

- "Everyone else is doing it."

Borrowing gives instant liquidity without a sale — which means no tax event. And if it's a credit line (not a term loan), you get 24/7 access with no fixed repayment dates. Pay back when it suits you, just as long as your collateral is sufficient.

The catch: Borrowing against crypto is for accessing value you already have, not for chasing bets you can't afford. If your reason makes you nervous to tell a friend, pause.

Question 2. How much can I really afford to borrow?

This is where math meets ego.

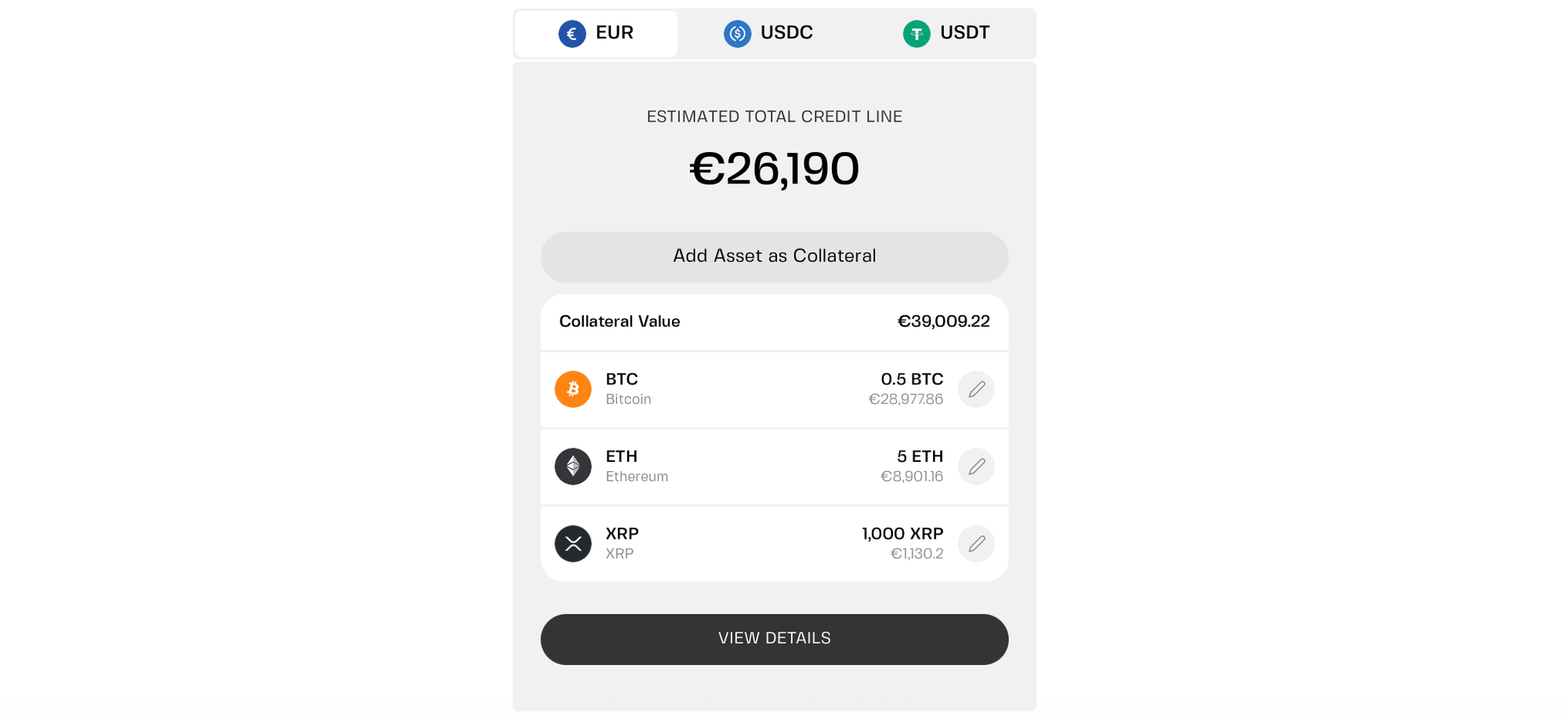

Most platforms will let you borrow up to 50–70% of your collateral's value. But just because you can borrow that much doesn't mean you should.

Here's a better way to think about it:

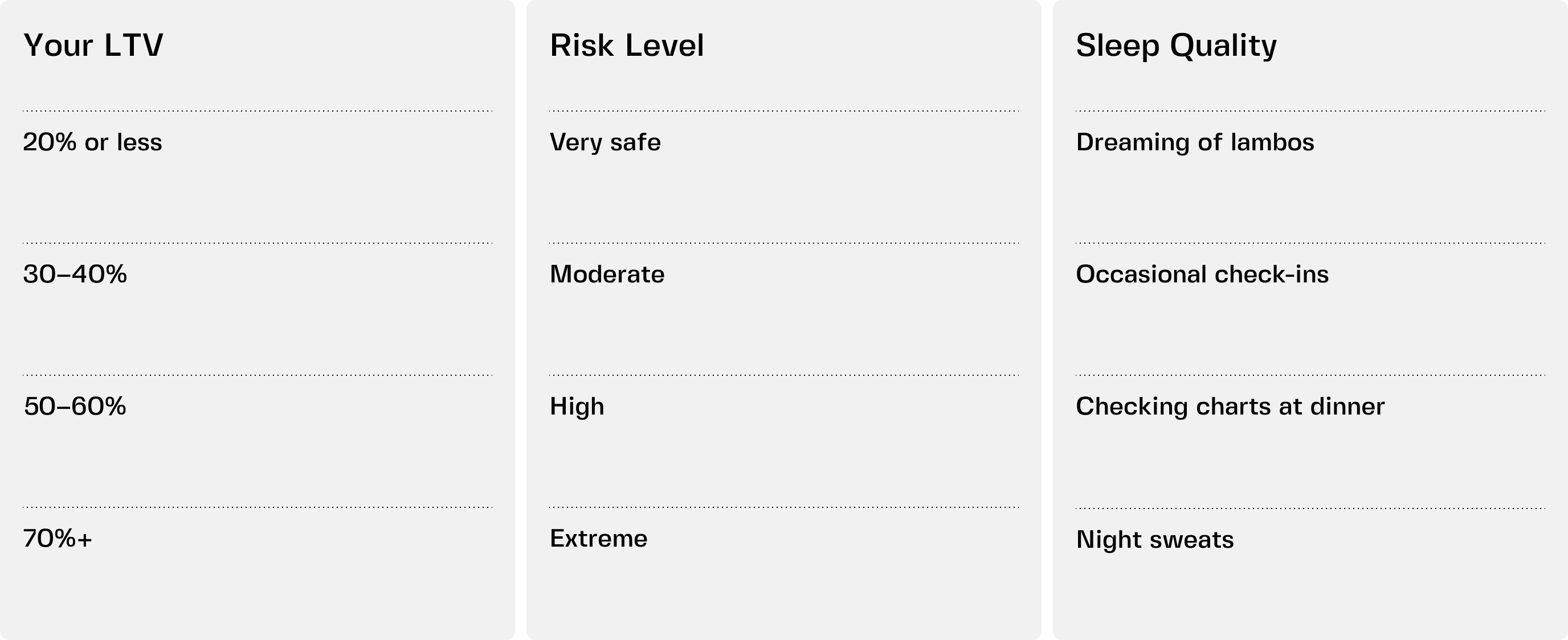

Conservative borrower (20–30% LTV): You borrow $10,000 against $50,000 in BTC. If Bitcoin drops 30%, your LTV barely moves. You sleep well. Some platforms even offer 0% APR at this level.

Aggressive borrower (50–60% LTV): You borrow $25,000 against $50,000 in BTC. A 20% drop puts you dangerously close to liquidation. You check prices every hour. Your sleep suffers.

Reckless borrower (70%+ LTV): You're basically praying the market goes up. One bad week and your crypto is gone.

Here's the rule of thumb: borrow what you need, not what they'll give you. If the thought of a 20% market drop makes you anxious, you're borrowing too much.

Question 3. What happens if the market drops 30% tomorrow?

This is the stress test.

Markets don't go up forever. The last five years have taught us that corrections and crashes can happen more often than anyone could imagine.

So close your eyes. Suppose you wake up tomorrow and your collateral is worth 30% less. Ask yourself:

- Do I have extra crypto to add as collateral?

- Do I have cash on hand to pay down part of the loan?

- Am I willing to do either of those things at 3 a.m. when the alert hits my phone?

If your answer is "I'll figure it out," you're not ready. If your answer is "Yes, I've got a plan," you're probably in good shape.

Smart borrowers don't just hope markets cooperate. They have a backup plan for when they don't.

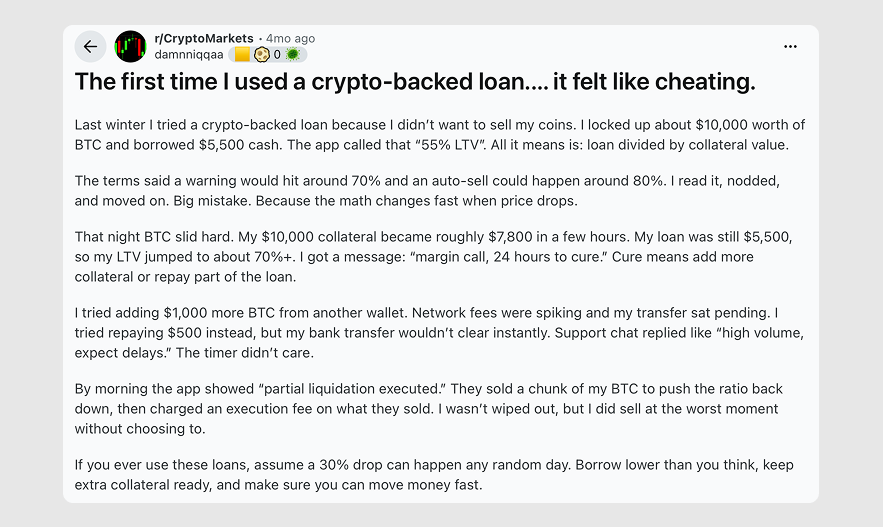

Cautionary tale from Reddit

Someone locked up $10,000 in BTC and borrowed $5,500. The app called that "55% LTV" — loan divided by collateral value. They read the terms, nodded, and moved on.

Then BTC slid hard.

Collateral became $7,800 overnight, and LTV spiked to 70%+. Margin call: 24 hours to add collateral or repay.

Tried adding more BTC — network fees spiked. Tried repaying — bank transfer was slow. Support was swamped.

The timer didn't care. By morning, "partial liquidation executed." The platform sold a chunk of their BTC at the worst possible moment — plus an execution fee on top.

That Reddit user learned the hard way: assume a 30% drop can happen any random day. Borrow lower than you think. Keep extra collateral ready. Make sure you can move money fast.

Let's simplify the framework

Think of it like this:

The sweet spot for most people is 20–30%. Low enough to survive a crash, high enough to actually get useful liquidity. And on platforms like Clapp, that 20% threshold comes with 0% APR — free liquidity, no strings attached.

What responsible borrowing looks like in practice

Let's walk through an example.

You hold $50,000 in Bitcoin. You need $15,000 for a business opportunity. You decide to borrow against your BTC instead of selling.

You open a credit line and keep your LTV at 30% ($15,000 borrowed against $50,000). You've got $10,000 in stablecoins sitting in your Flexible Savings as a buffer — just in case.

A month later, Bitcoin drops 20%. Your collateral is now worth $40,000. Your LTV climbs to 37.5%. You're still safe. But you get an alert anyway.

You have options:

- Transfer some of those stablecoins into collateral to bring LTV back down

- Pay down $2,000 of the loan from your earnings

- Do nothing — you're still well below the liquidation threshold

Markets recover. You repay the loan, so that Bitcoin never left your wallet. No sale means no tax event and no regret. And because you kept LTV low, your interest cost was minimal — or zero.

Finally, beware of crypto loan scams

There are a few schemes one could run into — unless they double-check their platform's trust score. One example is the "crypto fake loan unlock," which freezes victim's collateral and demands "fees," "taxes," or "more collateral" to unlock them (without ever doing it).

Scammers may use fake platforms, messaging apps (Telegram/WhatsApp), or phishing emails to lure you in. Always verify you're on the real platform before connecting your wallet or sending any crypto.

Bottom line

Borrowing against crypto can be a smart way to access liquidity without selling — but only if you manage risk properly.

Ask yourself the three questions. Borrow conservatively. Have a backup plan.

And aim to be the person who sleeps through the crash — not the one forced to sell at the bottom.

Frequently asked questions

1. What's the difference between a crypto loan and a credit line?

A loan gives you a lump sum. You repay on a fixed schedule, and interest starts on the full amount from day one. A credit line gives you a pre-approved limit. Draw only what you need, pay interest only on what you use, and repay anytime. Credit lines are more flexible — ideal for ongoing liquidity needs rather than one-time purchases.

2. Can I really borrow at 0% APR?

Yes — if you keep your Loan-to-Value (LTV) low enough (for example, 20% LTV or below, depending on the platform). It's a reward for responsible borrowing. Push LTV higher, and standard rates apply. Always check your platform's rate table before borrowing.

3. What happens if I can't repay the loan?

If you stop making payments or your collateral value drops too low, the platform may liquidate your assets to recover what you owe. You'll usually get warnings first — margin calls with 24–48 hours to add collateral or repay. Ignore them, and you could lose part of your crypto. Always have a backup plan.

4. Is borrowing against crypto better than selling?

Depends on your goal. Selling is permanent — you lose your position and trigger taxes. Borrowing lets you keep your crypto and avoid a taxable event. But borrowing comes with risk (liquidation, interest costs). If you believe in long-term upside and can manage LTV responsibly, borrowing often makes more sense than selling.

5. How do I avoid getting scammed?

Stick to regulated platforms with transparent terms and institutional custody (like Fireblocks). Never send crypto to "unlock" a loan. Never share your private keys. If a platform promises guaranteed returns or asks for upfront fees, run. Real crypto lending doesn't work that way. Check trust scores, read reviews, and if something feels off, trust your gut.