You have $10,000. Where should you park it for the next 5 years?

Under the mattress? In a bank savings account? High-yield online bank? Or somewhere else entirely?

It sounds like a simple question. But the answer can mean a difference of thousands of dollars — and more importantly, access to a whole ecosystem of financial tools.

Let's run the numbers on four very different options.

TL;DR

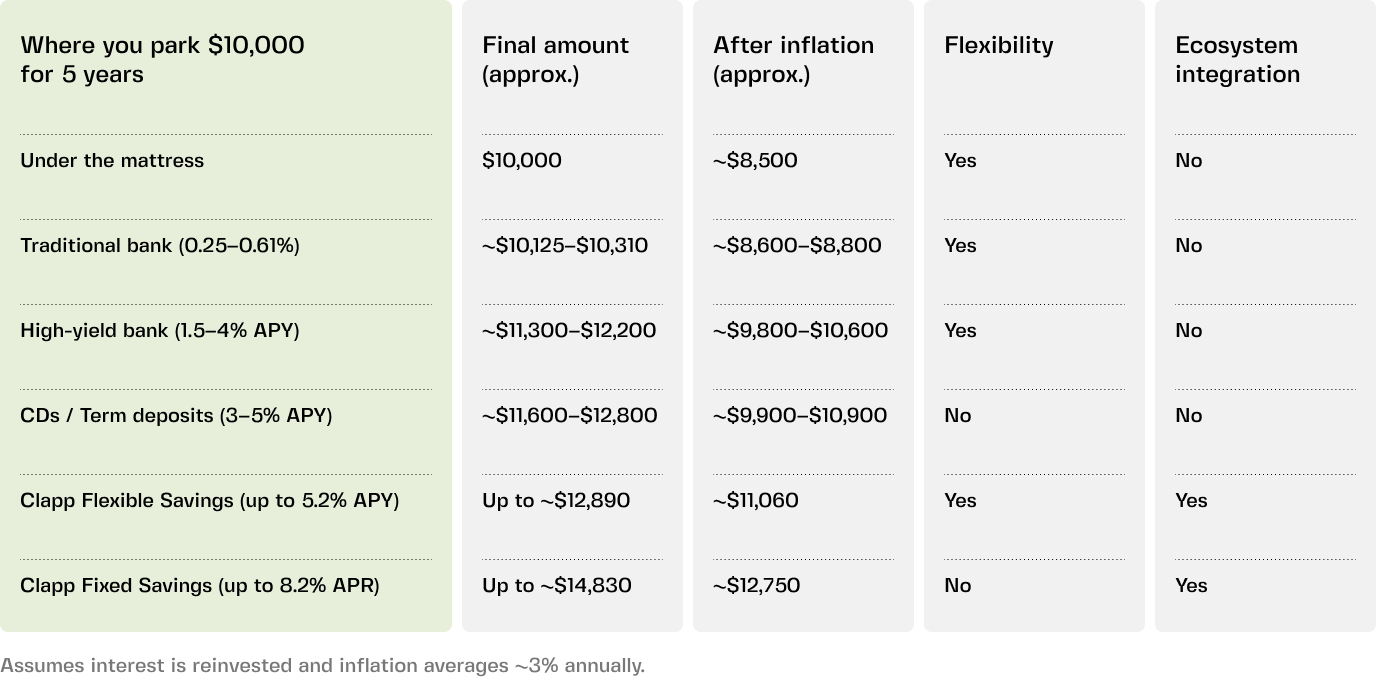

- Under the mattress: You lose to inflation every year. After 5 years, your $10,000 buys what $8,500 buys today.

- Traditional bank savings (0.25%–0.61% APY): You're barely moving. After 5 years, you have ~$10,150. Inflation eats you alive.

- High-yield online bank (1.5–4% APY): You keep pace. After 5 years, you have ~$10,800–$12,200. Not bad, but your money is siloed.

- Crypto savings on stablecoins (5–8% APY): Your money actually grows. At 5%, ~$12,800. At 8%, ~$14,700.

- The gap is real. Between a high-yield bank at 4% and crypto savings at 8%, you could be leaving ~$2,600 on the table.

The rates, clarified

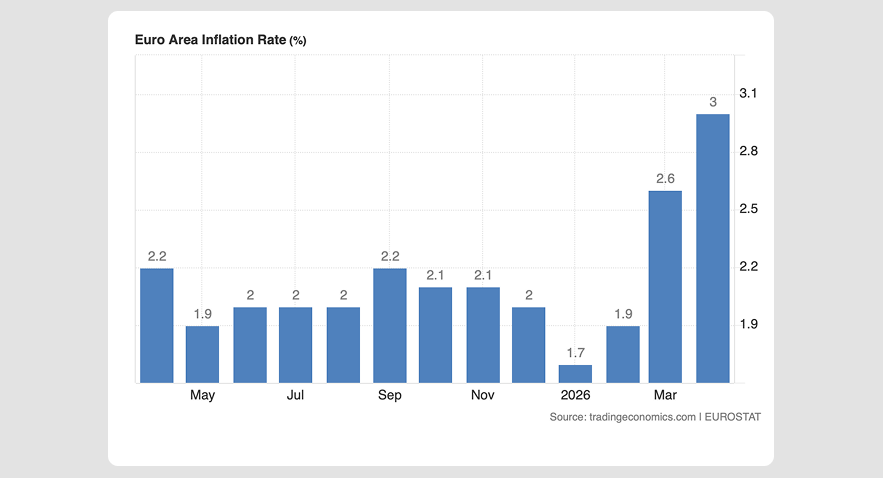

Before we compare, here's what's actually available to savers as of May 2026.

Traditional bank savings

- US national average: 0.61% APY

- Euro area overnight deposits: 0.25% APY

- US online banks: 4.00%–4.10% APY

- EU neobanks and savings platforms: 1.50%–3.50% APY

Certificates of Deposit (CDs) / Term deposits

Higher rates than regular savings (up to 4.00-4.20% APY in the US; 1.30%-2.20% APY in the EU), but your money is locked for a set period (6 months, 1 year, etc.). Withdraw early and you forfeit interest.

Crypto savings on stablecoins

5–8% APY: daily compounding without lock-ups (flexible) or higher yield for fixed terms

So the real comparison isn't between 0.01% and 8%. It's between 4% (HYSA) and 5–8% (crypto). The gap is narrower, but still significant.

Option 1: Under the mattress

Let's start with the worst option first.

You put $10,000 in cash somewhere safe. Just paper sitting there, zero interest or growth.

But inflation doesn't stop. In April 2026, inflation was running at 3.8% in the United States and 3% in the Eurozone — the latter its highest level since September 2023.

At 3% annual inflation, your $10,000 loses about $300 of purchasing power every year.

After 5 years, your $10,000 is still $10,000. But it buys what ~$8,500 bought today. You′ve lost $1,500 in real value — and you never touched the money.

In a nutshell: Zero growth, guaranteed loss to inflation.

Option 2: Traditional bank savings

Now let's look at a regular bank account — what most people actually use.

At 0.61% APY (US average) or 0.25% (Euro overnight), your money barely moves.

After 5 years: $10,000 becomes about $10,300–$10,150.

Factor in that 3% inflation — and you've lost purchasing power. Your money grew a tiny bit, but everything around you got more expensive faster.

Better than a mattress, but still losing.

Option 3: High-yield online bank (HYSA)

This is the real competition for crypto savings.

Online banks, neobanks, and savings platforms offer better rates than traditional banks. In the US, you can find 4.00%–4.10% APY. In the EU, rates typically range from 1.50% to 3.50% APY.

After 5 years at 4% APY (compounded monthly): $10,000 becomes about $12,200.

After 5 years at 2.5% APY (EU average): $10,000 becomes about $11,300.

The first scenario only slightly outpaces inflation. You preserved purchasing power, but not by much. With the average EU rates, you're actually losing ground.

The flexibility advantage. Like crypto savings, HYSAs let you withdraw anytime. That's a clear advantage over CDs (Certificates of Deposit), which lock your money for a set period — withdraw early and you forfeit interest.

But your money sits in a silo — it earns yield and that's it. Those savings aren't part of a broader system.

Overall, solid choice: safe, insured, with a decent return. But it’s still a standalone savings account.

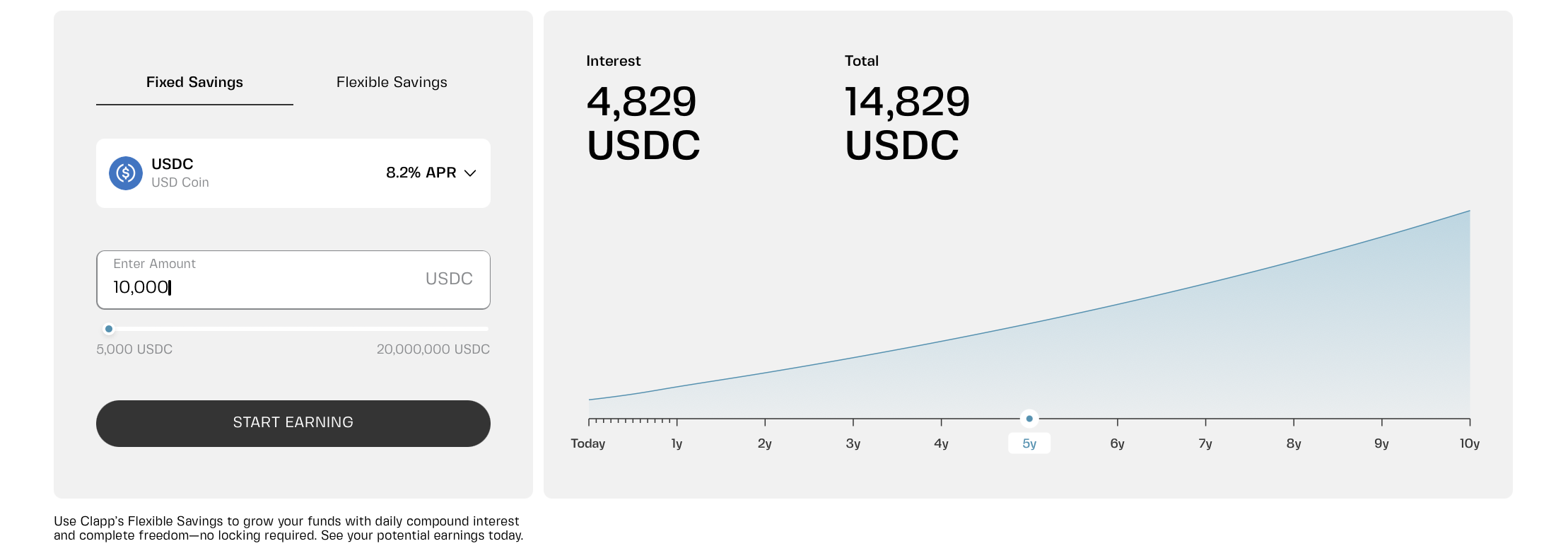

Option 4: Crypto savings on stablecoins

Now let's look at the alternative.

You put your $10,000 into a crypto savings account on stablecoins like USDC or USDT. Rates vary, but let's look at realistic ranges.

At 5% APY (daily compounding): After 5 years, you have about $12,840. At 8%, around $14,800.

After inflation at 3%:

- At 5% yield: ~$11,000 in today's dollars

- At 8% yield: ~$12,750 in today's dollars

Same flexibility as HYSA. With Flexible Savings, you can withdraw anytime — no lock-ups, no penalties. Need cash for an emergency or a sudden market opportunity? Your money is ready.

But here's where crypto savings separates itself.

Your savings don't have to sit in a silo. They can become part of a larger system.

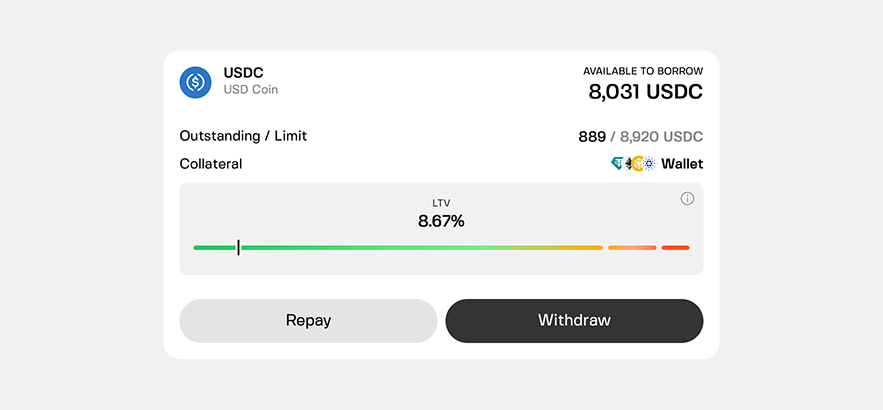

$10,000 in Flexible Savings can back your credit line

A credit line is a flexible source of on-demand liquidity backed by your crypto. Unlike loans, interest typically applies only to the amount you actually use, and APR may drop to 0% for low LTV (20% and below on Clapp). When the market drops and your LTV spikes, moving stablecoins from savings to collateral will restore balance.

Your savings become dry powder for opportunities

While everyone else is panic-selling, you have cash ready. Flexible savings are liquid — withdraw anytime without any penalties. This means you can buy the dip, capture the recovery, or just sleep better knowing you have dry powder on hand.

Get additional liquidity without selling your portfolio

Need cash for something urgent? Draw from your credit line, not your savings, so they can keep earning yield — for instance, 5.2% APY while you borrow at 0% APR (as long as LTV stays low). You avoid sacrificing yield or selling your portfolio, triggering an additional tax event.

How do Fixed Savings fit in?

Fixed-term savings offer higher rates (up to 8.2% APR) if you're willing to lock your money for 1–12 months. That's closer to a CD — but unlike a CD, when the term ends, those funds can feed into your credit line or portfolio.

That’s where flexibility and yield start working together within a broader system. Your savings can actually do something beyond sitting there.

Bottom line comparison

The gap, simplified

Between a high-yield bank account at 4% and crypto savings at 8.2% APR, the difference on $10,000 over 5 years is about $2,630. Not life-changing, but not nothing either.

And if you're parking $50,000 or $100,000, that gap scales.

But what about risk?

This comparison isn't complete without talking about risk.

Bank accounts (including HYSA) are insured — FDIC in the US up to $250,000, similar protections in the EU. Crypto savings accounts are not.

That doesn't mean crypto savings are unsafe, but you need to choose carefully. Look for regulated platforms with institutional custody (for example, Fireblocks), transparent terms, and segregated accounts.

The higher yield comes with higher responsibility to do your homework.

So where would you park your idle cash?

The mattress is out, and traditional savings rates can feel painfully low.

High-yield online banks are a solid, safe choice. You'll keep pace with inflation, maybe a little ahead.

Crypto savings on stablecoins offer higher returns — but with less insurance and more platform risk.

There's no single right answer. Some people split the difference: $5,000 in a HYSA, $5,000 in crypto savings. Others go all-in on one or the other.

The only wrong answer is doing nothing.

So what's your $10,000 doing right now? And could it be doing more?

Frequently asked questions

1. Is a high-yield online bank really safe?

Yes. As long as it's FDIC-insured (US) or covered by equivalent deposit insurance (EU), your money is protected up to the limit. The trade-off is lower returns than crypto savings.

2. Why would anyone use a traditional bank at 0.61%?

Convenience. Many people never switch because it's a hassle. But the math is brutal — over 5 years, you're leaving hundreds or thousands on the table.

3. Is crypto savings on stablecoins safe?

The stablecoins themselves are designed to hold their peg. The risk is platform failure. Choose regulated platforms with institutional custody. Don't chase 15% yields from unknown protocols.

4. Can I lose money in crypto savings?

If the platform fails or gets hacked, yes. That's why platform choice matters. Bank accounts have insurance. Crypto savings don't. The higher return comes with higher responsibility.

5. Should I put all my cash in crypto savings?

Probably not. Many people split between a high-yield bank account for safety and crypto savings for growth. The right mix depends on your risk tolerance and how much you trust the platform.