Your savings, your credit line, and your portfolio — why they work better together

Most people treat their crypto like separate buckets.

Savings in one, credit line in another, portfolio somewhere else entirely. That way, each component is its own thing, never talking to the others. That's not wrong — but the real advantage comes when those pieces work together.

Savings feeding your credit line. Your credit line protecting your portfolio. Your portfolio continuing to work while you borrow against it.

Let's walk through how these pieces actually work as a system.

TL;DR

- Your savings can back your credit line. Use stablecoins in Flexible Savings as dry powder for margin calls.

- Your credit line protects your portfolio. Borrow instead of selling during dips. Keep your upside.

- Your portfolio keeps you diversified. One asset crashing doesn't wipe you out.

- The pieces amplify each other. Together, they're stronger than any single product alone.

- A little planning turns three tools into one strategy.

The problem with silos

Let's say you have $80,000 in crypto. You split it:

- $20,000 in savings earning 5% APY

- $40,000 in a portfolio of BTC and ETH

- $20,000 in BTC backing a fixed-term crypto loan

You think you've done things right. A portion generating yield. A portion capturing market upside. A loan covering emergency needs — say, $10,000 for home repairs.

Holding, earning, and borrowing. Three separate buckets.

But the real magic happens when these three things work together on the same platform.

First, swap that fixed-term loan for a credit line

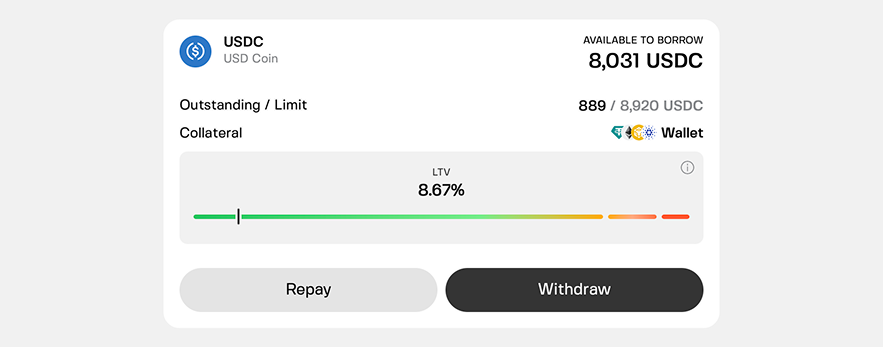

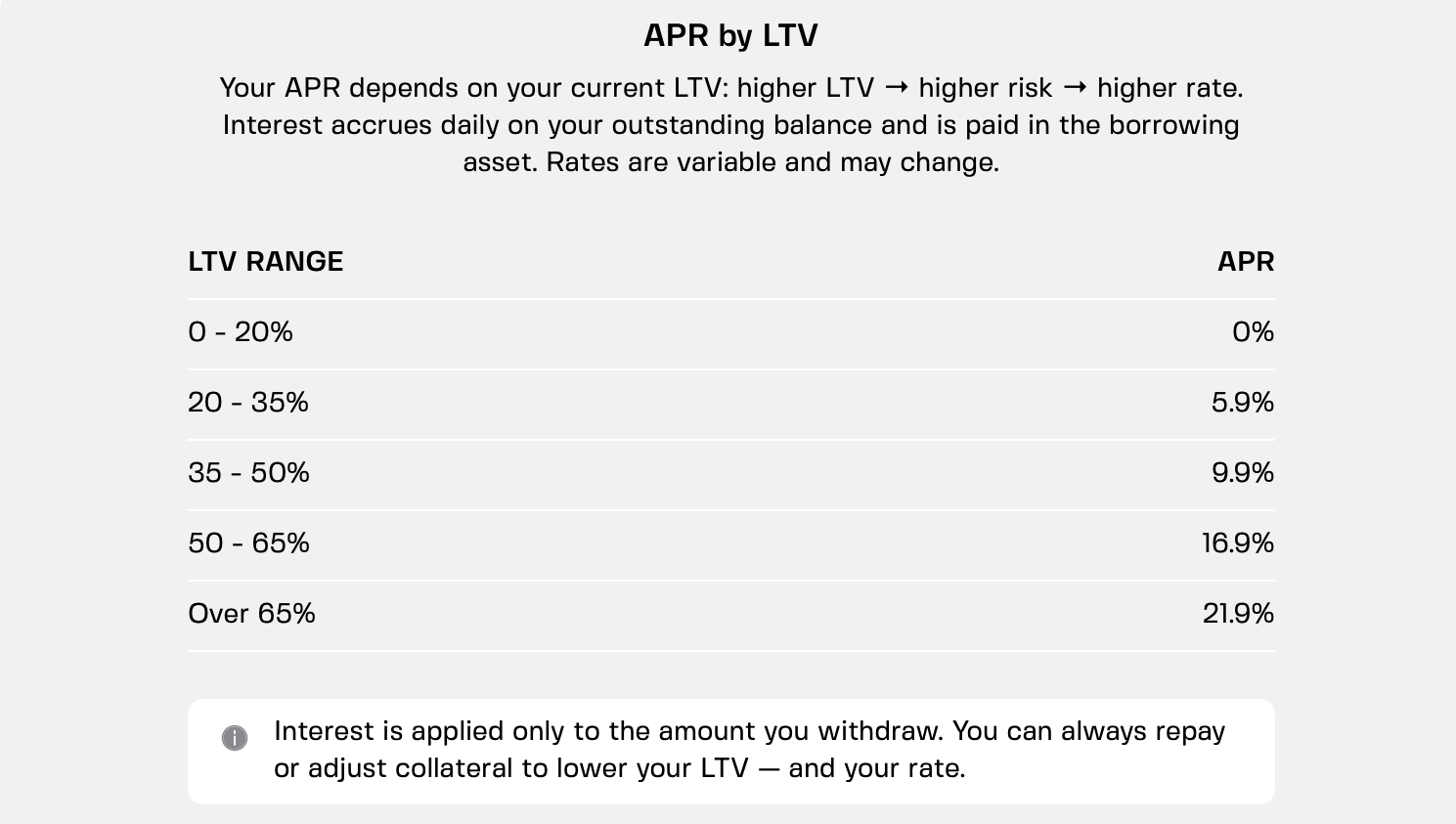

Credit lines offer liquidity on demand, whenever you need it. Like loans, they still rely on LTV — but without a fixed repayment schedule.

You pay interest only on the portion you draw. Repay on your own terms. And every time you repay, the limit replenishes. You can use it again like an emergency fund that resets itself.

Keep your LTV low — below 20% — and the annual percentage rate drops to 0% on some platforms. Clapp also lets you mix multiple tokens into a collateral basket. You can add, remove, or swap those assets after drawing funds.

Compare these two options.

- 12-month loan backed by BTC. Fixed monthly schedule. Late fees. No way to move that collateral until full repayment. Paying interest on the full amount from day one.

- Flexible credit line, backed by the same BTC. Paying interest only on what you've drawn. Keep LTV below 20% and the APR is zero. Multi-collateral backing gives you more flexibility to manage LTV during market swings.

Credit lines have no late fees — there's no schedule. Just watch your LTV to minimize interest and avoid liquidation. The logic is similar to a loan, but you have more ways to respond. Not just by adding collateral, but also by replacing it — partially or fully — with more stable assets.

Your savings can back your credit line

Here's the first connection.

Your credit line requires collateral. That collateral is usually your portfolio — BTC, ETH, other crypto. But if the market drops, your LTV rises, raising the risk of a liquidation. Once it reaches a critical threshold (e.g., 80%, depending on the platform), you get a margin call.

Add collateral or repay part of the loan. Otherwise, the lender could sell your assets to cover the debt.

Where does that extra collateral come from?

Your savings.

That $10,000 in Flexible Savings is earning yield; it's also your emergency dry powder. When prices plunge in the next market cycle, you can move stablecoins from savings into your collateral pool instantly. No selling, no panic — with enough stablecoins, you can bring your LTV back to safety in no time.

- Without savings: Margin call hits. You scramble to find cash. Maybe you sell other crypto at a loss. In DeFi, it's even worse: bots usually liquidate your collateral without any warning.

- With savings: Transfer stablecoins. LTV drops. Problem solved. You keep your portfolio intact.

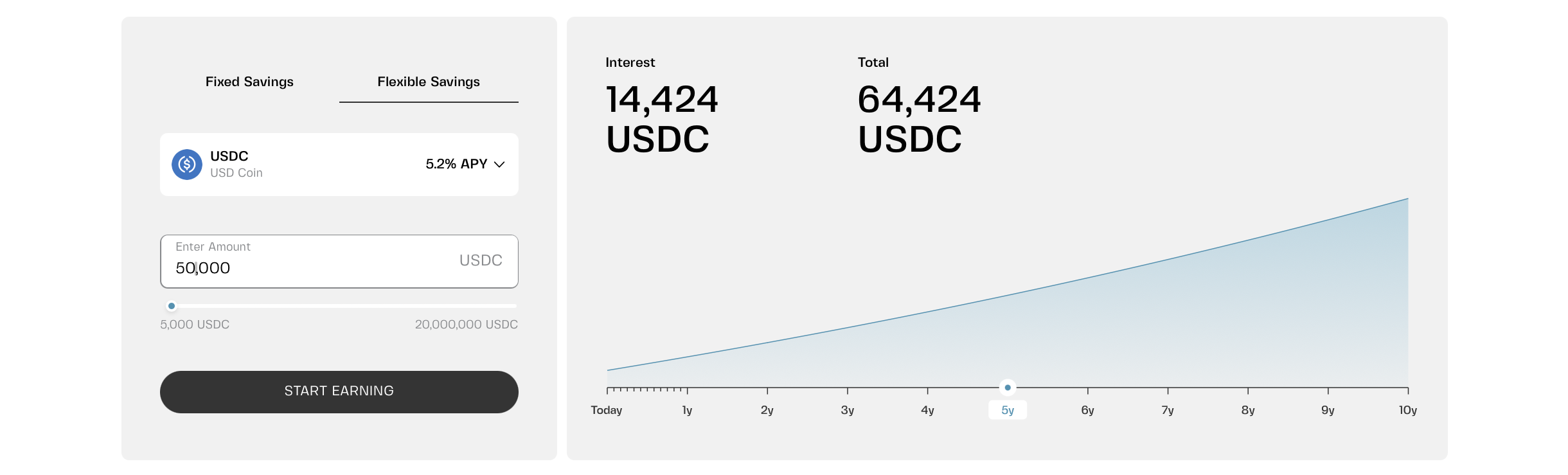

One catch with Fixed Savings. That locked portion earns a higher rate, but you can't touch it until the term ends. That's fine for long-term goals, but don't count on it as your emergency buffer — that's what Flexible Savings is for.

Your credit line protects your portfolio

Here's the second connection.

Crashing markets drag your portfolio down 30%. You need cash for something urgent. What do you do?

Most people sell, locking in losses and triggering capital gains tax. And if the market rebounds next month, they're left as anxious observers.

Your credit line gives you another option.

Instead of selling, you draw from your credit line, where your collateral stays put. Your portfolio stays intact. No tax event.

When the market eventually recovers, you're still holding. You repay the loan from your savings or future income.

- Without credit line: Sell low. Lock in losses. Miss the rebound.

- With credit line: Borrow. Wait. Repay. Keep your upside.

Your portfolio keeps you diversified

Here's the third connection.

If all your collateral is one asset — say, Bitcoin — your credit line's health depends entirely on Bitcoin's price. Drop 40% and you're scrambling.

A diversified portfolio spreads that risk.

Hold BTC, ETH, and stablecoins. Maybe some SOL. Maybe some USDC earning yield in savings.

When one asset drops, others can buffer your LTV. Your credit line stays safer, while savings stay intact.

- Without diversification: One coin crashes. Your LTV spikes. Margin call hits.

- With diversification: The dip hurts, but your whole world doesn't collapse.

How they work together in real life

Let's walk through a hypothetical example.

Your setup:

- $40,000 portfolio (60% BTC, 30% ETH, 10% other)

- $10,000 in Flexible Savings (earning 5.2% APY)

- Credit line with 20% LTV limit (0% APR)

Month 1: No issues. Savings earns yield while portfolio sits and credit line stays ready.

Month 3: BTC drops 30%. Your LTV climbs toward 25%. You're not in danger, but creeping closer.

You have options:

- Move $2,000 from savings to collateral. LTV drops back to 20% or lower — bringing the APR back to 0%.

- Do nothing — you're still safe.

Month 6: Opportunity appears. You need $8,000 for a business expense.

Instead of selling BTC at a loss, you draw from your credit line at 0% APR because LTV stays below 20%.

You use savings to cover interest costs or partial repayments if needed. Your portfolio stays untouched.

Month 12: Your buckets are back in balance.

- Business expense pays off.

- You repay the credit line from revenue.

- Your Flexible Savings have earned 5.2% APY the whole time.

- Your portfolio has recovered.

Without the system: You'd have sold BTC at a loss, triggered taxes, and missed the recovery.

With the system: You kept everything, paid zero interest as you borrowed responsibly, and earned savings yield on top. Came out ahead.

Wait — could you borrow to earn?

Here's a thought that sounds clever at first.

Borrow at 0% APR, then park those funds in savings to earn yield. Free money, right?

Here's what actually happens.

If you borrow and then deposit the funds into savings, you've used a portion of the credit limit — so your LTV may climb above that 20% threshold. Either you add more collateral or continue paying interest — and that interest eats into whatever yield your savings are earning.

You also end up committing more crypto as collateral. That larger portion of your holdings stops earning yield. It just sits there backing your loan.

So when does this make sense?

Sometimes you hold smaller-cap tokens that aren't accepted for savings but are accepted as collateral. You can't earn yield on them directly. But you can use them to borrow stablecoins or BTC, then put those assets into savings.

On Clapp, you can mix up to 25 different assets as collateral. Savings support BTC, ETH, USDT, and USDC. So you can pledge those smaller tokens, borrow supported assets, and earn yield on them instead of leaving the smaller tokens idle.

Watch your LTV. If the smaller tokens drop in value, your LTV rises. You might need to add more collateral or repay part of the loan. But as long as you keep LTV low, the borrowing costs stay at 0% — and your savings yield becomes incremental upside.

Why this isn't complicated

You don't need to be a finance expert to make this work.

- Keep savings in Flexible Savings — earns yield, ready for emergencies.

- Open a credit line with low LTV — 0% APR, available when you need it.

- Build a diversified portfolio — don't put everything in one coin.

- Connect the dots — use savings as collateral buffer, credit line instead of selling.

That's it. Three tools. One strategy.

Where Fixed Savings fits

You've noticed this article talks more about Flexible Savings than Fixed. There's a reason.

Flexible Savings is your operational buffer — money you can move, withdraw, or use as collateral at any time. Fixed Savings is for money you're sure you won't need.

Use Fixed Savings for:

- Long-term goals (1–12 months out)

- Money you want to lock away for a better rate

- Yield you don't need to touch until maturity

The bottom line

Your savings, your credit line, and your portfolio aren't separate products. They're parts of one system: a buffer, a source of liquidity without selling, and diversification. Alone, each is useful — but together, they're a strategy.

Don't let your crypto live in silos. Connect the dots.

Frequently asked questions

1. Can I really use my savings as collateral for a credit line?

On some platforms, yes — you can move funds between savings and your collateral pool instantly. On Clapp, Flexible Savings can be withdrawn anytime and added to your credit line collateral within seconds.

2. Does my credit line cost anything if I don't use it?

On platforms with 0% APR at low LTV, your credit line doesn’t accrue borrowing interest until you draw funds. Keep LTV at 20% or below (depending on the lender) and you pay zero interest — even if the line sits there for years.

3. What if my portfolio drops and my LTV spikes?

You have options. Add collateral from savings, repay part of the loan — or, if you left enough buffer, do nothing. The key is planning before the crash, not during.

4. Should I keep all my savings in Flexible Savings or split between Flexible and Fixed?

A mix often works best — for instance, you could keep 3–6 months of expenses in Flexible Savings for emergencies and put longer-term savings in Fixed Savings for higher rates. Use the Flexible portion as your credit line buffer.

5. Is this strategy only for large portfolios?

No. The math works at any scale. $5,000 in savings, $20,000 in portfolio, and a credit line with low LTV could give you the same structural advantages. Start where you are, because the system scales with you.