5 hidden risks of borrowing against crypto

Many people don’t think about taking a crypto loan until they see the option in an app.

Borrow against your Bitcoin and get cash instantly.

On paper, it makes sense. You don’t sell or trigger taxes (in most cases), and your crypto position stays intact.

But that’s only the surface level.

The part you don’t really think about is what happens when the market moves against you — or when you realize your collateral is tied to rules you don’t fully control.

This isn’t about whether crypto loans are good or bad. It’s about the trade-offs that don’t show up in the marketing.

Here are five of them.

TL;DR

- Volatility can liquidate you fast. A 30-40% market drop can wipe your collateral if you borrowed at 50% LTV.

- Your locked crypto can't earn anything. No staking yield, no savings interest, no upside while your loan is active.

- Platforms fail. So do smart contracts. CeFi can go bankrupt. DeFi can get hacked. Know the risk.

- Interest isn't the only cost. Origination fees, liquidation penalties, and compounding interest add up.

- Tax rules vary by where you live. Borrowing is usually not a taxable event. But some structures can trigger taxes anyway.

1. The market can liquidate you faster than you expect

Crypto loans work perfectly when prices go up. When they go south, it's a whole different story. That's when the trouble starts.

Suppose you borrow $15,000 against $50,000 in Bitcoin. That's a 30% LTV (loan-to-value ratio), a safe choice — the less you borrow relative to your collateral, the lower the liquidation risk.

A market shock out of the blue causes the price to drop 40% overnight. That's similar to what happened with Bitcoin and ether during the March 2020 crash.

Your Bitcoin is now worth $30,000, meaning your LTV zooms to 50%. There's still a decent buffer separating you from the liquidations threshold (75-90% on some platforms). But...

Drop another 20% and you're at 75% LTV. Liquidation territory.

Don't 'set it and forget it.' Lenders don't wait for the market to recover — and DeFi protocols won't even send you a warning. Once your LTV crosses their threshold — usually around 70-80% — they sell your collateral automatically. At the worst possible moment, without asking.

A CeFi platform will usually alert you before liquidation, giving you time to react — but you still need to move fast. There are three options: repaying the loan, adding collateral, or swapping collateral assets (if it's a credit line that allows it).

The fix. Borrow at 20% LTV or less. Keep extra collateral ready. And don't assume "safe enough" means safe forever. Many Redditors recommend maintaining massive collateral ratios (e.g., 200% to 400%) to survive market crashes.

Liquidation won’t affect your traditional credit score. Crypto lending isn’t tied to credit bureaus, and defaults aren’t reported. But selling collateral still has tax implications in many jurisdictions (more on this below).

2. Your locked crypto stops working for you

When you pledge crypto as collateral, it's locked. You can't trade it, stake it, or earn yield on it.

That Bitcoin that could have earned 3-5% in a savings account? It's just sitting there, backing your loan.

Consider the opportunity cost. The advertised interest rate isn't your only expense — you're also losing whatever your crypto could have earned if it wasn't locked.

If you borrow at 6% APR but your collateral would have earned 4% in savings, your real cost is closer to 10% — the interest you pay plus the yield you miss.

The fix. If your crypto can still earn a meaningful yield elsewhere, borrowing might not be worth it unless you really need the liquidity.

If you do borrow, set aside an "emergency fund" — assets that can be used as additional collateral in a downturn — in flexible savings products. That way, you’re able to withdraw anytime without a penalty while still making the most of your holdings.

3. Weigh up platform and smart contract risks

Your loan is only as safe as the platform you're using.

- DeFi platforms remove the middleman, but they introduce another risk: smart contract bugs. If the code has a vulnerability, hackers can drain funds. There’s no customer support or legal recourse in the traditional sense. Until regulation catches up, you’re largely relying on the code.

- CeFi platforms hold your collateral — preferably with qualified custodians like Fireblocks. Even with such regulated, bank-grade infrastructure, choose licensed lenders with multiple layers of security beyond basic 2FA.

The interest rate isn't the only thing to compare. Platform security matters just as much.

The fix. Use regulated platforms with transparent custody. Look for institutional-grade security. And don't put all your collateral on one platform — diversify.

4. Interest isn't the only fee

The advertised rate is the starting point, not the final cost. You may see "6% APR" and think that's it, but there's often more hidden in fine print.

Make sure your lender is upfront about:

- Origination fees. Some platforms charge 0.5-2% just to open the loan.

- Liquidation fees. If you get liquidated, some platforms add a penalty on top of selling your collateral.

- Compound interest. Unlike simple interest, compound interest adds to your balance over time. You end up owing more than you expected.

- Withdrawal fees. Moving funds in or out might cost you.

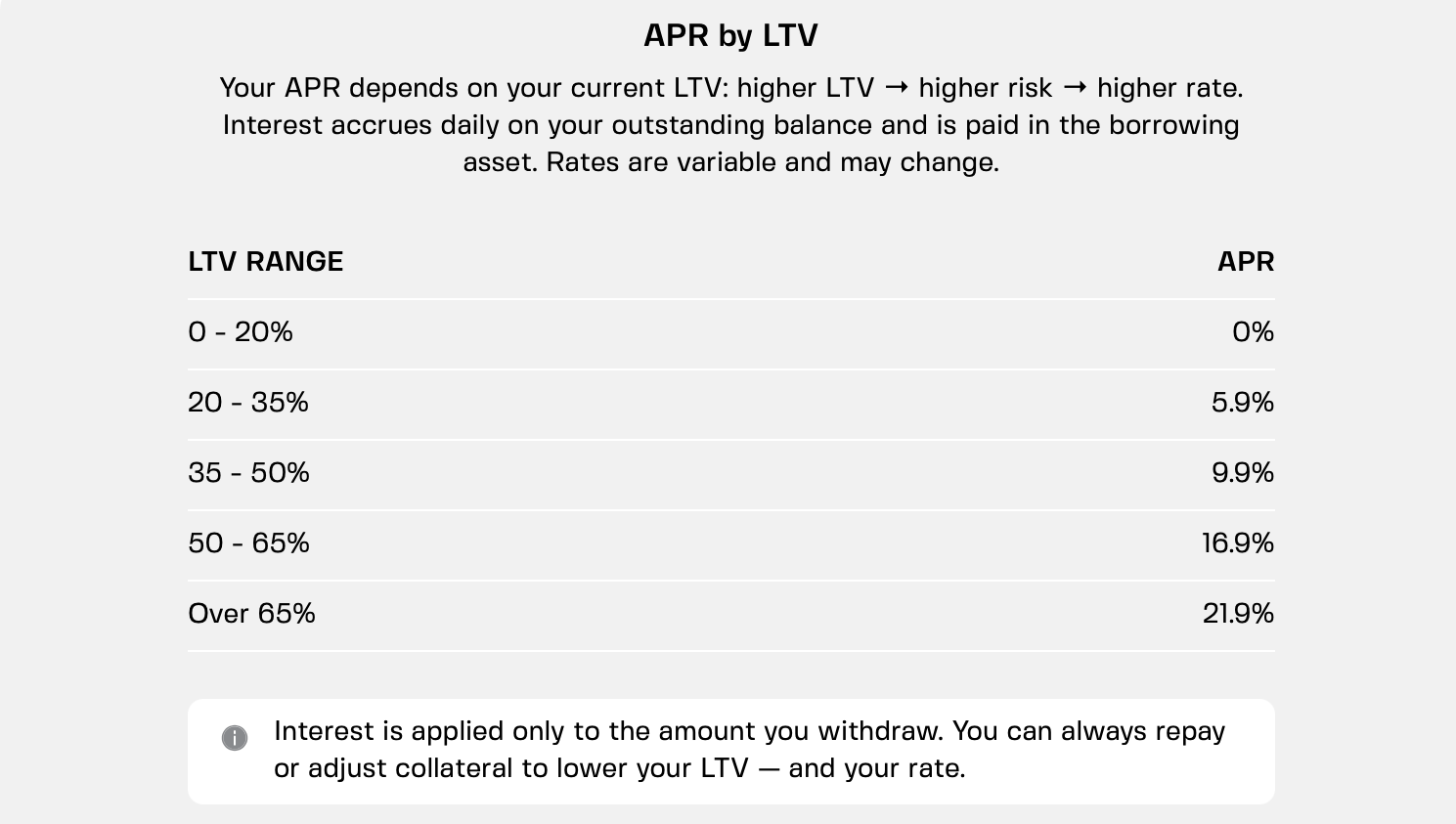

- LTV vs. APR. Your interest rate may also increase as your LTV rises. Higher-risk loans are typically priced higher, which encourages more conservative borrowing.

The fix. Read the full fee schedule before you borrow. Ask about origination fees, liquidation penalties, and how interest is calculated. On platforms like Clapp, you see all costs upfront — no hidden surprises.

5. Tax rules aren't the same everywhere

In most places, borrowing against your crypto isn't a taxable event as you're not selling. So no capital gains tax.

But liquidation is selling, and repaying a loan with appreciated crypto may also trigger taxable events in some jurisdictions. The same is true for some lending structures — like repo agreements where ownership temporarily shifts.

Crypto loans aren't taxable by themselves. But that doesn't mean nothing in the process is taxable.

The fix. Talk to a tax professional who understands crypto. Don't assume the rules in one country apply to yours.

How to borrow without the regrets

These five lessons aren't meant to scare you away from borrowing. They're meant to help you borrow smarter.

- Keep LTV low. 20% is safe. 30% is okay. 50% is risky. 70% is gambling.

- Understand your real cost. Interest plus lost yield plus fees equals your true borrowing cost.

- Choose your platform carefully. Regulated CeFi with transparent custody, or DeFi with audited code. Don't chase the lowest rate without checking security.

- Have a backup plan. Keep extra collateral ready. Set price alerts. Know your platform's liquidation threshold.

- Maximize flexibility. Make sure you can free up assets quickly to save your collateral from liquidation. Flexible savings beat fixed products in this regard.

- Talk to a tax pro. One conversation could save you a nasty surprise next April.

Consider credit lines over fixed-term loans

A lot of people still take fixed-term loans, but not all crypto borrowing works the same way.

Credit lines are more flexible. You can borrow, repay, and adjust your position as conditions change, without having to close and reopen a loan each time. That matters most during volatility, when you need flexibility instead of being locked into the original structure of your loan.

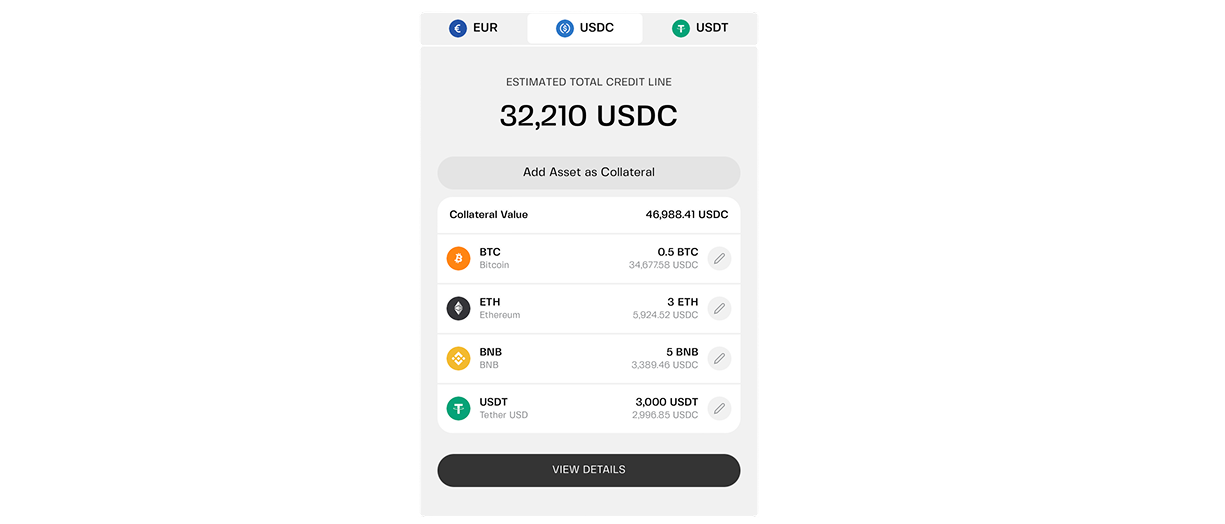

Some platforms, like Clapp, also let you use multi-collateral credit lines. Instead of relying on one asset, you can pledge a basket of cryptocurrencies and adjust it over time — adding, removing, or swapping assets as conditions change. That flexibility can make the difference between reacting to a crash and being prepared for it.

Borrow conservatively, read the fine print

Crypto loans are powerful tools. They let you access cash without selling your conviction. But they're not magic. They come with risks that aren't always obvious from the marketing materials.

The people who get hurt are the ones who borrow without understanding what happens when things go wrong. Consider all the risks, and always have a plan for the crash you don’t see coming — and the flexibility to act when it does.

Frequently asked questions

1. What's the safest LTV to avoid liquidation?

20% LTV is very safe. At that level, your collateral would need to drop about 75% to liquidate you — which has never happened in a single crash. 30% is still reasonable. 50% puts you at serious risk during a normal bear market.

2. Can I lose more than my collateral?

No. In a standard crypto loan, your losses are limited to whatever you pledged. The platform sells your collateral to cover the loan. You don't owe anything beyond that.

3. How do I know if a platform is safe?

Look for regulated status (VASP licenses), institutional custody partners (Fireblocks), transparent fee schedules, and proof of segregated accounts. Avoid platforms that promise unrealistic yields or have unclear terms.

4. Do I have to pay taxes when I borrow?

In most jurisdictions, no. Borrowing isn't a sale, so it's not a taxable event. But interest payments, liquidation sales, or swapping collateral could trigger taxes. Check local rules.

5. Is borrowing against crypto worth it?

For long-term believers who need short-term liquidity, yes — if you borrow conservatively and understand the risks. For anyone trying to gamble on leverage or borrow without a repayment plan, probably not. The tool works well. But misusing it gets expensive fast.