Beyond Bitcoin ETFs: Your cheat sheet to crypto ETPs

Crypto ETPs have pulled digital assets from the fringes of finance into the beating heart of global capital markets. What started as a niche experiment is now one of the clearest signals that institutional adoption is already here.

Yes, spot Bitcoin ETFs dominate the headlines. But they're just one piece of a much bigger puzzle. In 2026, the global crypto ETP market is diversifying fast. So what else is out there — and how do these products actually work?

TL;DR

- Spot ETFs dominate. BlackRock's IBIT became the fastest-growing ETP in history, proving institutions want simple, physical exposure.

- Europe plays by different rules. Single-asset crypto products there are called ETCs or ETNs, not ETFs, due to stricter diversification rules.

- Futures products found a niche. They lost the cost battle to spot ETFs but still appeal to income-focused investors via monthly distributions.

- Staking yields can work. But only if fees don't eat the advantage. Bitwise BSOL showed the formula: low fees + integrated staking = market dominance.

- The spot foundation is set. The next phase is building on top: options, structured products, and a deeper ecosystem for institutional capital.

What is a crypto ETP?

A decade ago, the idea that the world's largest asset managers would hold Bitcoin (BTC) and ether (ETH) on behalf of everyday investors sounded like science fiction. Crypto markets were fragmented, lightly regulated, and viewed with suspicion by anyone wearing a suit.

Fast forward to 2026, and over 2,000 US advisory firms allocate to crypto ETPs, with custodians holding roughly 5%–7% of all BTC in circulation. The 2024 SEC approval of spot Bitcoin ETFs — followed by ether ETFs later that year — opened the floodgates.

An ETP (Exchange-Traded Product) is an umbrella term for any exchange-listed financial instrument that trades in real time — ETFs, ETNs, ETCs all fall under this roof. They let investors gain exposure to crypto without holding the coins, managing private keys, or navigating decentralized exchanges.

But not all ETPs are built the same. Some hold actual coins in custody. Others are debt instruments backed by issuer promises. Some can't use the ETF label at all depending on where they're listed.

Products divided by regulation: ETF, ETC, ETN

If you're in the US, "crypto ETF" sounds like the standard everywhere. Across the Atlantic, the rules flip.

ETF (Exchange-Traded Fund) — a fund that trades on exchanges, tracking a specific index or asset. In the US, this includes single-asset crypto products like spot Bitcoin ETFs. These offer direct ownership, SEC approval, and high liquidity.

In Europe, stricter UCITS regulations require ETFs to hold diversified assets (5/10/40 rule) — so single-asset crypto products use different labels. That's where ETCs and ETNs come in.

- ETC (Exchange-Traded Commodity) — treats Bitcoin like gold or oil. Physically backed — the issuer holds the coins in custody. This eliminates issuer credit risk but carries custody risk.

- ETN (Exchange-Traded Note) — an unsecured debt instrument. You're lending money to the issuer in exchange for a promise to pay based on asset performance. The coins aren't yours — credit risk applies.

The US largely sidesteps this complexity. Spot Bitcoin and ether ETFs dominate, following the familiar fund structure Americans already know.

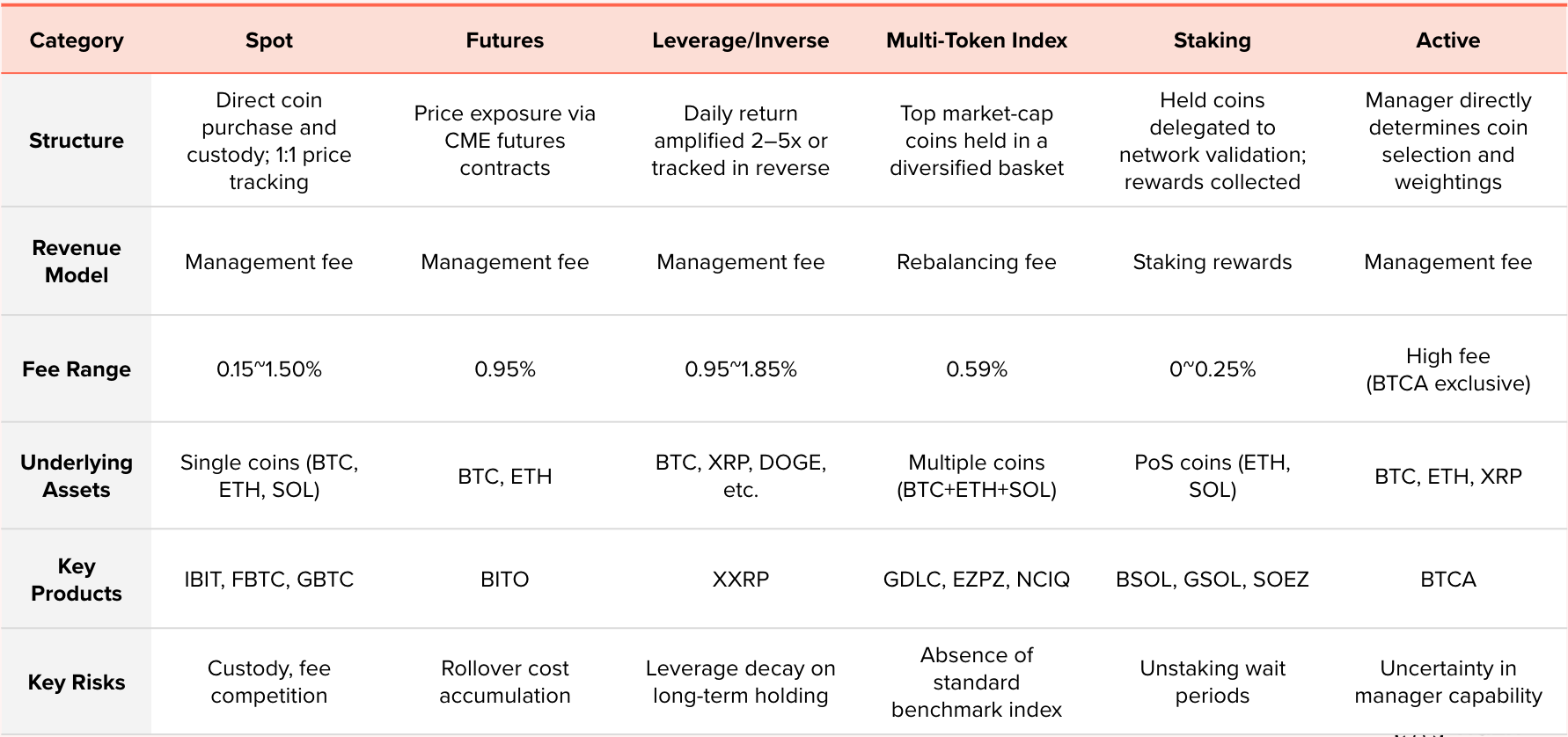

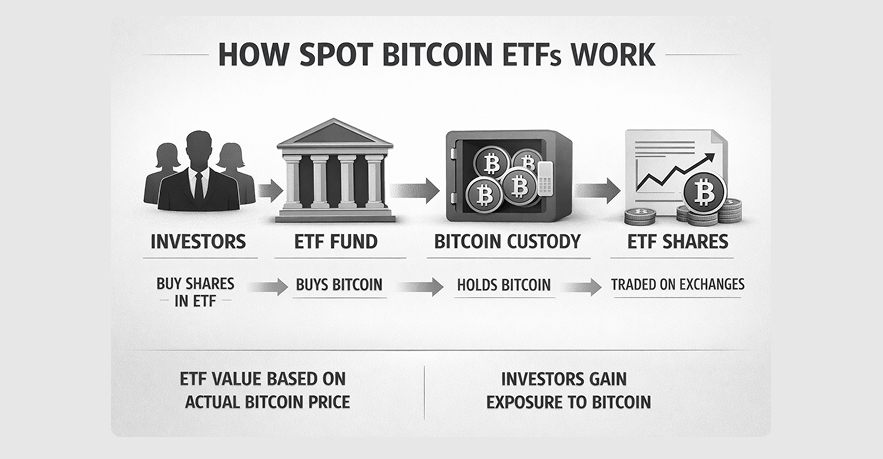

Spot ETPs: The heavyweights

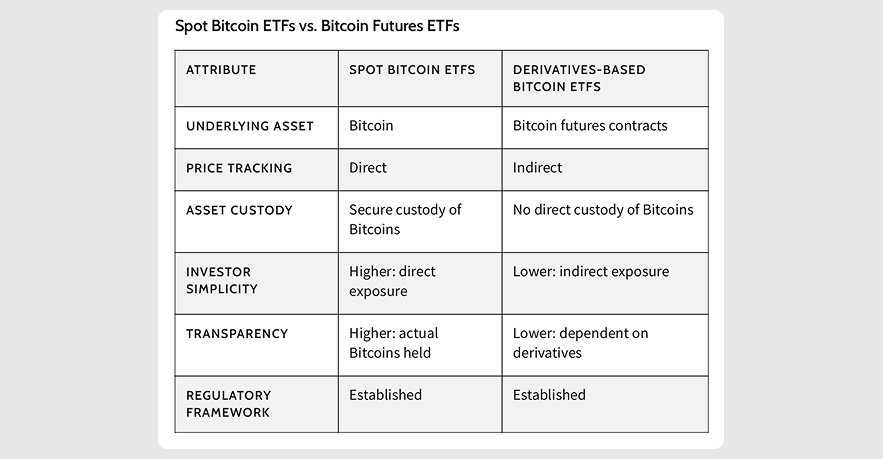

Spot crypto ETFs dominate for one simple reason: they hold actual coins — BTC or ETH in institutional custody, tracking the price 1:1. No derivatives. No roll costs.

Upon its 2024 launch, BlackRock's IBIT became the fastest-growing ETP by AUM in history. Fidelity, Franklin Templeton, Invesco, VanEck — names that once watched crypto from a distance — now manage tens of billions in spot products.

Why spot ETFs won the race:

- Direct ownership — actual crypto, clean tracking

- Institutional trust — BlackRock and Fidelity don't need to explain custody to pension funds

- Regulatory clarity — SEC approval opened the floodgates

- No friction — bought on the same brokerage accounts as stocks

- Fee wars — 0.25% at BlackRock, 0.19% at Franklin, some temporary fee waivers

The two titans:

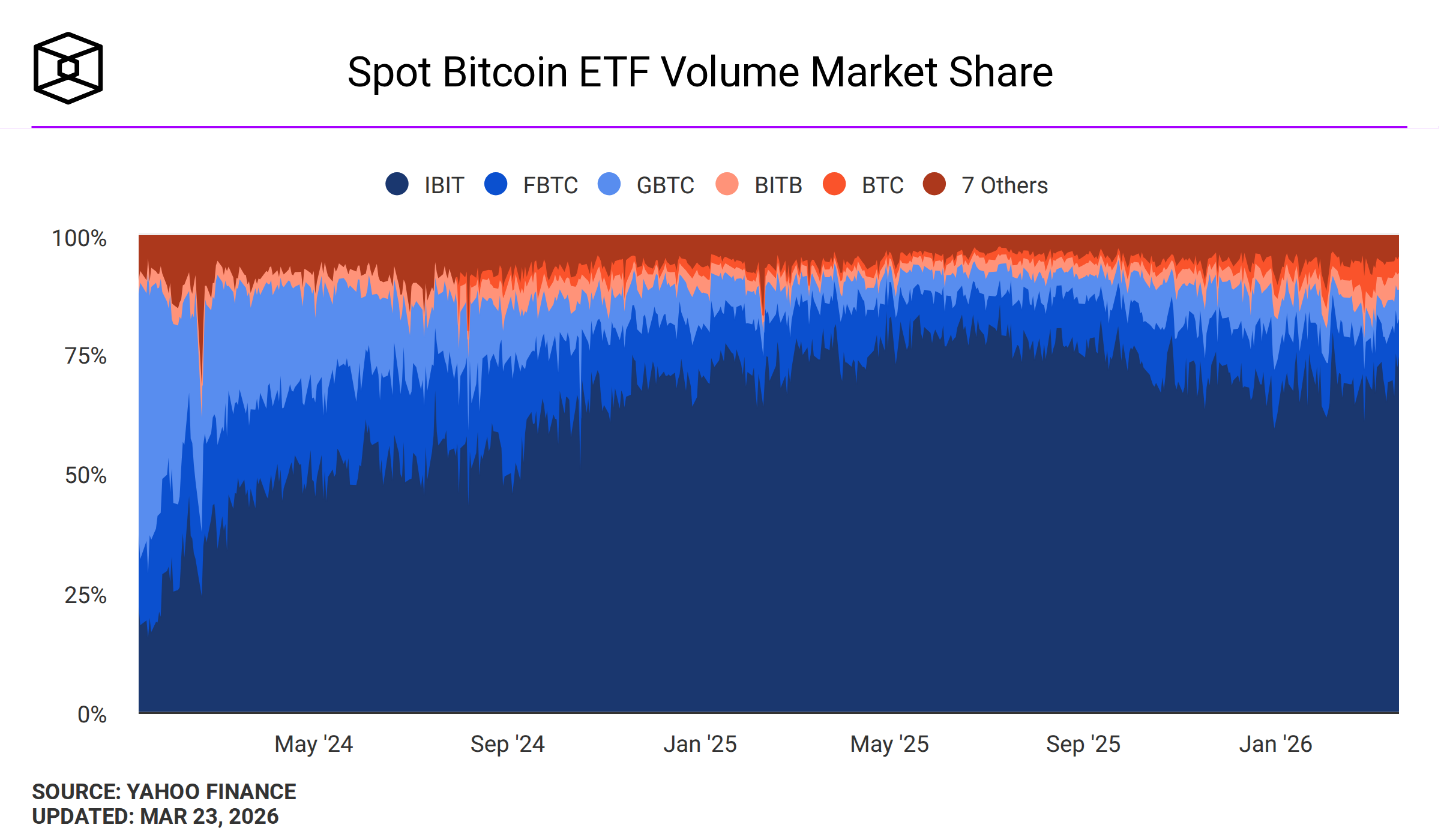

- BlackRock (IBIT) — Runs only two crypto products but integrates them into the existing iShares network. A 0.25% fee on over $54 billion AUM generates industry-leading revenue. IBIT holds over 70% market share.

- Grayscale — The original crypto asset manager, founded in 2013. Offers the broadest lineup: BTC, ETH, SOL, XRP, DOGE, LINK, SUI, plus a multi-token index. But converting its legacy 1.5% trusts into spot ETFs triggered over $25 billion in outflows to cheaper rivals. A 0.15% Mini Trust followed, but the lead had already shifted.

Futures ETPs: Pre-spot era holdouts

Before spot ETFs, futures-based products were the closest thing to regulated crypto exposure. ProShares BITO launched in 2021 with roughly $1 billion in first-day volume — the second-highest in ETF history.

Then spot ETFs arrived. And the game changed.

Futures ETPs don't hold physical coins. They use CME futures contracts. No custody risk, but no direct ownership either. On the downside, monthly contract rolls may bleed performance.

When spot ETFs launched in 2024, capital migrated fast. BITO became a case study in how spot approval can gut a futures product's competitive edge. But futures ETPs found a niche: monthly distributions from trading gains appeal to income-focused investors.

Leveraged & inverse ETPs: Not for the faint of heart

Some investors want to amplify bets or profit when prices drop. That's where leveraged and inverse ETPs come in.

These are short-term tools, not buy-and-hold vehicles. They use futures and swaps to deliver 2x, 3x, or even 5x daily returns. Leverage works both ways — amplifying both gains and losses. The products reset daily, so holding through volatile periods can erode value even if the underlying ends flat.

Inverse ETPs work in reverse — rising when the underlying drops. Traders use them to hedge or bet against the market without shorting futures directly. For instance, SBIT ProShares UltraShort Bitcoin ETF targets -2x the daily performance of BTC.

Teucrium XXRP was the first 2x leveraged XRP ETP, setting the template. Since late 2025, the space has expanded beyond BTC and ETH to memecoins like DOGE, BONK, and TRUMP.

Today, Volatility Shares manages BITX (2x Bitcoin), ETHU (2x Ether), and SOLT (2x Solana). ProShares offers BITU (Ultra Bitcoin) and ETHT (Ultra Ether).

Multi-token index ETPs: Crypto equivalent of S&P 500

The S&P 500 bundles 500 stocks into one trade. Crypto index ETPs do the same with digital assets — a diversified basket of top cryptocurrencies in one product.

For institutions, that's an easier risk management sell than concentrated single-coin exposure. Crypto indexes vary by methodology, weighting, and coverage.

Some track large-cap leaders. Others drill into sectors like DeFi. A few go broad — the CMC 200 covers the top 200 coins by market cap.

No single index has claimed the crown. But as institutional adoption grows, the push for a standardized crypto benchmark will only get louder.

Staking ETPs: When your crypto works for you

A spot ETP sits on coins. A staking ETP puts them to work.

For proof-of-stake networks like Ethereum and Solana, staking generates yield — roughly 3%–5% for ETH, 5%–7% for SOL. Staking ETPs capture that.

In theory, they're compelling alternatives to spot products. In practice, fees matter.

BlackRock's spot ether ETF (ETHA) holds AUM roughly 3.6x larger than Grayscale's staking version (ETHE). Why? The spot product charges 0.25%. The staking version carries 2.5% — eating most of the yield.

Bitwise BSOL flipped the script. Launched as the first US spot Solana ETP, it surpassed $500 million AUM in 18 days. The formula: 0.20% management fee plus integrated staking (5%–7% yield). It captured over 80% of the US Solana ETF market.

The lesson seems simple: staking yield is attractive. But if the fee structure eats the advantage, investors will stick with the cheaper, simpler spot option.

Active ETPs: Can managers beat the market?

Most crypto ETPs are passive — tracking an index or single coin. Active ETPs are different. Managers choose which coins to hold, when to rebalance, and how to position.

In theory, active management could add value. In practice, it's unproven. Crypto markets trade 24/7, move fast, and correlations run high. Outperforming a simple buy-and-hold is harder than it sounds.

The US leans heavily passive, with spot ETFs dominating. Europe has been more open to active strategies — managers can tap staking rewards or adjust weightings without rigid index constraints.

FiCAS AG BTCA, launched July 2020, was the world's first actively managed crypto ETP. It holds the top 15 coins by market cap. The fee structure is steep: 2% management plus 20% performance fee.

Over one year, it's underperformed bitcoin on both return and volatility. The bar remains high — and so far, no one's cleared it consistently.

Spot era and what comes next

The crypto ETP landscape in 2026 is a spot story. BlackRock's IBIT rewrote the record books. Grayscale proved early mover advantage doesn't last when fees don't compete.

Futures products like BITO now serve a narrower niche: income-focused investors who value monthly distributions. Leveraged and inverse products cater to short-term traders comfortable with daily resets. Index ETPs offer diversification but lack a dominant benchmark. Staking products promise yield, but fee structures often cancel the rewards. Active management remains an experiment with more questions than answers.

The next phase isn't about more spot products. It's about what gets built on top: options for hedging, structured products for sophisticated strategies, and a deeper ecosystem to support institutional capital.