Borrowing against Bitcoin vs. Ethereum: Does the asset matter?

Suppose you want to borrow against your crypto to get cash. You have both Bitcoin and Ethereum. Which one should you use?

Most people would just pledge the bigger bag, so whichever holds more value becomes the collateral. Simple, right?

But different assets behave differently. And when you're borrowing against them, those differences matter.

Let's compare Bitcoin and Ethereum side by side. Volatility, LTV limits, staking income, and what happens when the market turns. Then you can decide which asset actually works better as collateral for your situation.

TL;DR

- Bitcoin is less volatile than Ethereum. Historically, BTC moves more slowly. ETH can swing harder in both directions.

- Higher volatility means lower LTV limits. Platforms often let you borrow less against ETH than BTC because the price swings are bigger.

- Ethereum offers staking opportunities that Bitcoin doesn't. But if you're using ETH as collateral, that same ETH generally can't be staked at the same time.

- The best collateral depends on your goals. Stability? Bitcoin. Extra yield? Ethereum.

- You don't have to choose one. Multi-collateral credit lines let you use both.

The volatility gap

Bitcoin (BTC) and Ethereum's ether (ETH) don't move the same way. Ether often sees stronger price swings because it has a different risk profile and broader set of use cases.

- Bitcoin is often viewed as "digital gold" — a store-of-value asset with a relatively straightforward investment thesis.

- Ether also powers thousands of DeFi applications, underpins DeFi lending and NFTs, and lets holders earn passive income through staking.

There's no universal pattern, though — volatility works both ways. At times, ETH outpaced BTC during periods of strong network activity, rising DeFi usage, and increased demand for on-chain applications. Other times, BTC forged ahead, leading the market when uncertainty drove investors toward more established assets.

Bitcoin is the big ship. It turns slowly, takes time to change direction, and generally moves with less drama. Ether tends to move faster. It can rally sharply during bullish periods — and fall just as quickly when sentiment turns.

What this means for borrowing. Lenders care about volatility. The more an asset swings, the more risk they take. So they often assign different LTV limits.

Many platforms allow higher maximum LTVs for BTC than ETH, although the exact limits vary by lender (more below).

The staking factor

Ethereum runs on proof-of-stake. You can lock your ETH to help secure the network and earn yield in return. The rate usually sits somewhere between 3% and 6% APY, depending on network activity and how many people are staking. Right now, about 30-32% of all circulating ETH is staked — roughly 36 to 39 million coins locked up for rewards.

There are also alternatives to staking directly. Services like Lido give you a tradable token in return — stETH — that represents your staked position. Your money isn't completely tied up if you need access. But that's a more advanced setup with its own risks.

Here's the catch. You cannot stake your ETH and use the same ETH as collateral for a CeFi loan at the same time. Liquid staking tokens are an exception, but those usually only work as collateral in DeFi, not on centralized platforms.

- If you want to borrow against your ETH, your ETH stays locked as collateral. It won't earn staking yield.

- If you want staking yield, your ETH is locked in a validator. It won't be available as collateral.

Pick one or split your holdings — some for staking, some as collateral.

With Bitcoin, there's no decision to make. No staking yield either way. Your BTC just sits there.

What happens during a crash

Bitcoin and ether don't fall the same way. The speed of the drop determines how quickly your loan could get liquidated — unless you add more collateral in time.

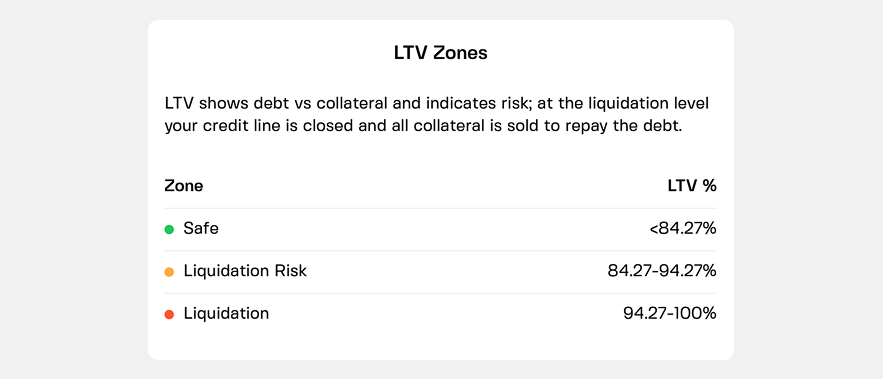

It all comes down to your LTV

The loan-to-value ratio is the key number for any crypto loan. It tells you how much you've borrowed compared to what you put up. Crypto loans are always over-collateralized — you borrow less than you deposit — to account for volatility.

Still, a fast price crash can wipe out your position. Lenders liquidate collateral once LTV reaches a platform-specific threshold, which is often significantly higher than the recommended borrowing range. The more volatile your pledged assets, the faster your LTV can climb past the safe zone.

Bitcoin tends to hold up better during market stress. It still owns the "digital gold" narrative. It's the oldest, most established cryptocurrency. When panic hits, a lot of investors rotate into Bitcoin as a perceived safe haven.

We've seen this play out recently. Ongoing US-Iran tensions, rising energy prices, and broader market fluctuations pushed the ETH/BTC ratio downward. When the going gets rough, capital still flows toward Bitcoin.

Ether can drop harder and faster. In the 2022 bear market, ETH fell about 75% from its peak. Bitcoin dropped about 65%.

What this means for borrowing. Your LTV is tied directly to your collateral's price. If ETH drops faster than BTC, your LTV spikes faster. You get closer to liquidation sooner.

If you're borrowing against ETH, you need a bigger buffer. That means starting with a lower LTV or keeping extra backup collateral ready.

How much can you borrow?

This also reflects the difference in volatility. The maximum LTV allowed for ether is usually around 60%. For Bitcoin, it's closer to 70%.

Example. You have $50,000 in BTC and $50,000 in ETH. Against BTC, you might borrow $35,000. Against ETH, maybe only $30,000. That's a real difference.

Maxing out your loan is rarely a good idea. The smaller your initial LTV, the more protected you are from liquidation. But you can always add more collateral later to bring your LTV down. Just pay attention to the lender's policies and know where the safe zone ends.

Choose credit line for more flexibility

- A fixed-term loan locks up your collateral for a set period — usually 1 to 12 months.

- A credit line has no fixed duration. It's revolving credit. Borrow when you need it, repay when you want. It's always on hand.

A credit line acts like an emergency fund that replenishes itself as long as you watch your LTV. No need to reapply for credit every time you need money. Some lenders also offer 0% APR for keeping your overall LTV at 20% or below, regardless of which eligible asset you pledge.

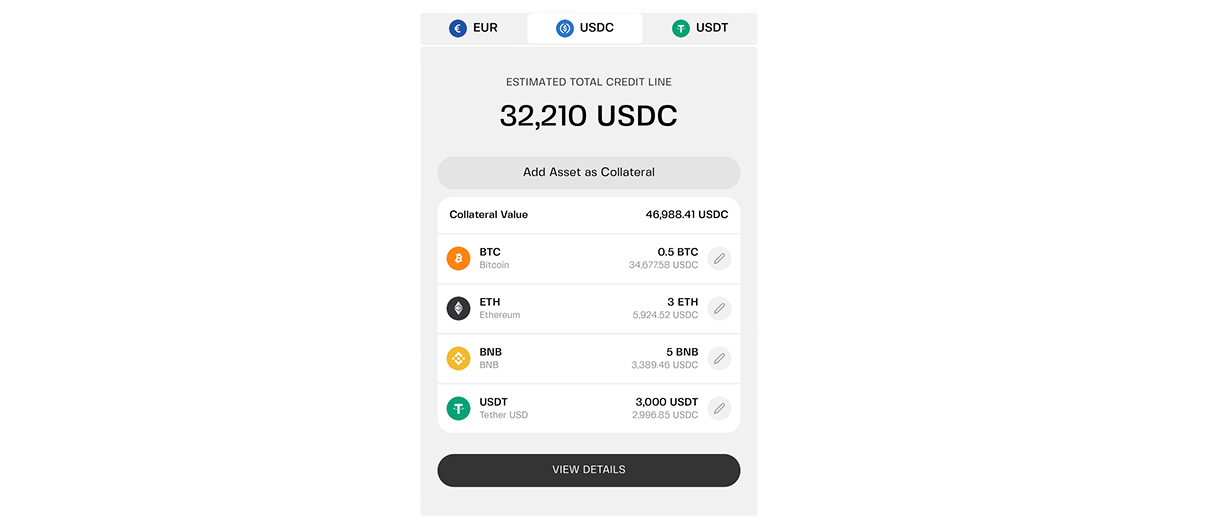

But there's another advantage — the ability to add, remove, or even swap collateral assets (up to 25 on Clapp) at any time. On such platforms, you don't have to make a final choice between BTC and ETH. Your borrowing power is based on the blended value — replace one coin with another as you see fit.

Swap some BTC for ETH — or vice versa — to capture market upside. Pull ETH out, replace it with another asset, and stake it however you like. Your credit line stays open the whole time.

Putting it together

If you want stability and higher borrowing power, Bitcoin is the safer bet. You'll get a higher LTV limit, your loan won't swing as wildly during market turbulence, and you won't have to watch the charts every day. The trade-off is that your BTC just sits there — no staking yield, no passive income.

With ether, you'll need to:

- Keep your LTV lower to account for bigger price swings.

- Accept that you can't stake the same ETH you're borrowing against.

- Split your holdings or use liquid staking tokens if you want staking yield as well.

For many people, a mix of both assets makes the most sense. Combine BTC and ETH — and add more — to maximize your borrowing power. A multi-collateral credit line lets you deposit BTC and ETH into one pool. Together, they can create a more balanced collateral pool.

You don't have to choose one. You just have to understand how each asset behaves — and plan accordingly.

Frequently asked questions

1. Is Ethereum riskier than Bitcoin as collateral?

Yes, because ETH is more volatile. Your LTV will fluctuate more, and you could get closer to liquidation during sharp drops. To compensate, borrow at a lower LTV against ETH than you would against BTC.

2. Can I stake my ETH while it's locked as collateral?

No. The same ETH generally can't be staked and pledged as collateral at the same time. Staked ETH is committed to a validator, while collateral ETH is locked with a lender. Some platforms accept liquid staking tokens (like stETH) as collateral, but that's a different product with its own risks. For most borrowers, you pick one: stake or borrow.

3. Which asset lets me borrow more?

Generally, Bitcoin. Platforms assign higher LTV limits to BTC because it's less volatile. You can borrow a larger percentage of your BTC's value compared to ETH.

4. Why would staking yield matter if my collateral ETH isn't staked?

Your loan terms don't change. But if part of your ETH strategy relies on staking income elsewhere in your portfolio, lower staking rewards reduce that benefit. That's one reason not to rely solely on staking yield when planning a borrowing strategy.

5. Should I convert my ETH to BTC for better loan terms?

Probably not. You'd trigger a taxable event by selling. And you'd lose exposure to ETH's upside. A better approach is to use a multi-collateral credit line. Keep both assets, borrow against the pool, and let your BTC provide stability while your ETH works for growth and yield.