The snowball effect: Why $50 a month can beat waiting for $10,000

One of the biggest investing myths is that you need large sums of money before it's worth getting started.

So people wait, telling themselves they'll invest when they've saved $5,000. Or $10,000. Or after the next bonus.

Meanwhile, someone else starts with $50 a month. Years later, that second person may end up ahead simply because they started earlier.

That's the snowball effect. The amount matters, but time matters even more.

Let's see why.

TL;DR

- Starting early matters more than starting big. Time is the biggest driver of compounding.

- Small deposits add up surprisingly fast. Consistency beats waiting for the "perfect" moment.

- Compound interest rewards patience. The longer your money stays invested, the faster it grows.

- Good saving habits matter as much as good returns. Automating small deposits often works better than chasing large ones.

- You don't need thousands to begin. Starting today usually beats waiting another year.

The biggest mistake isn't investing too little

It's investing too late. Many people postpone saving because they think the amount isn't worth it.

"$50 won't change my life."

"$100 isn't enough."

So they wait until they can invest "properly."

The problem is that while they're waiting, they're losing something much more valuable than money. They're losing time — and time is the one thing you can never deposit later. This is often called opportunity cost, and it applies in any market, be it stocks, crypto or anything else.

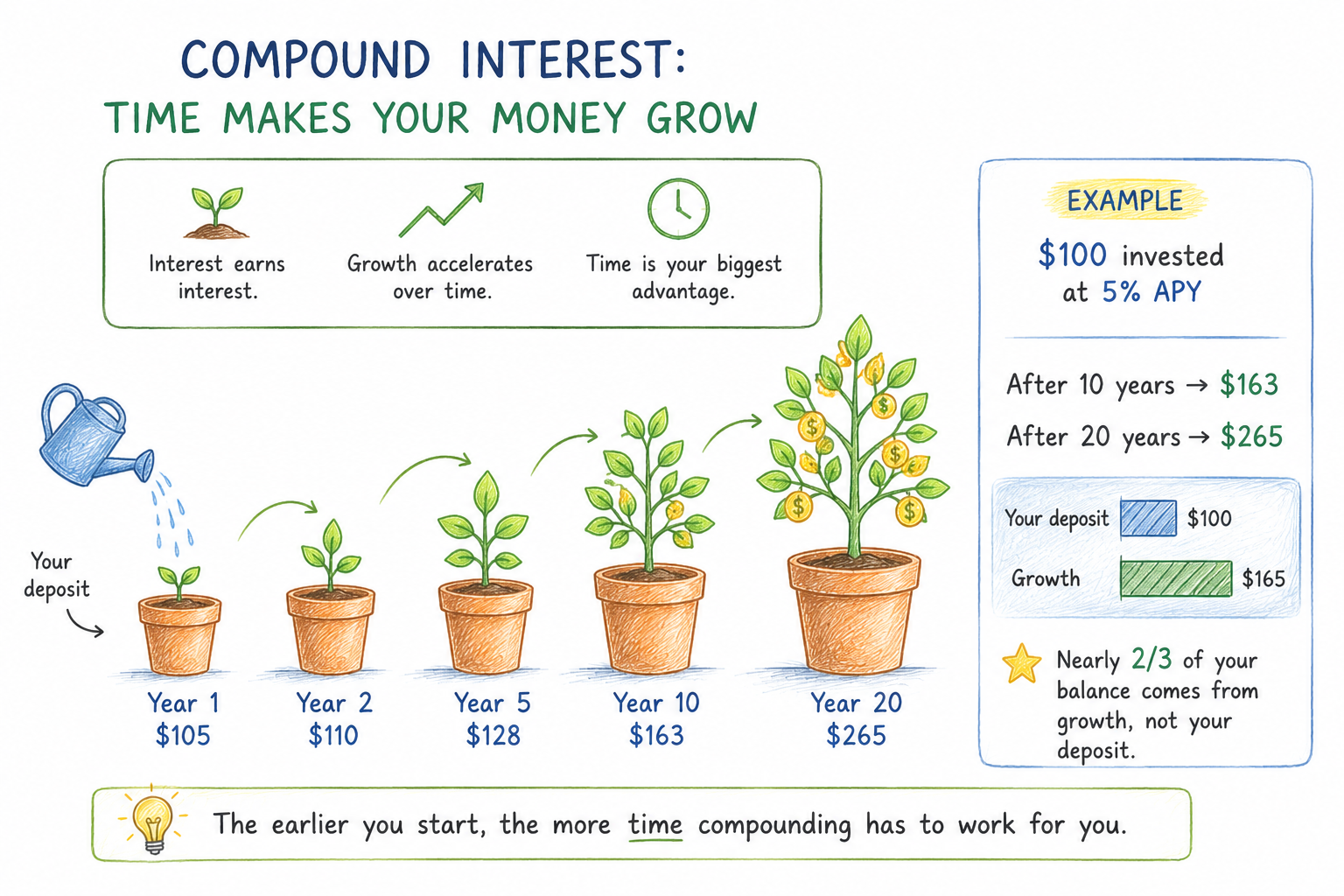

The ultimate cost of delay is losing out on the exponential power of compound interest — "interest on interest." With many savings products, it's just your original deposit (the principal) working — accumulated interest from previous periods also earns its own interest.

This means your savings can grow at an accelerating rate over time.

Every year you delay means you'll likely need to save considerably more later to reach the same financial goal.

Simple comparison

Imagine two people.

- Alex waits five years until they've saved $10,000.

- Sam starts today with $100 and adds $50 every month.

Both eventually earn the same 5% annual yield. Who finishes ahead depends largely on when Alex finally puts that money to work.

If Alex invests immediately, the lump sum usually wins. But if Alex spends years saving before investing, Sam's money has already been compounding the entire time.

That's why starting early often beats waiting for the "perfect" amount.

Regular investing isn't inherently better than lump-sum investing. The key difference is that money can't compound while it's sitting in your future plans.

The snowball gets bigger

Compounding is slow at first — that's why so many people underestimate it. The first few years don't look particularly exciting.

But then something changes.

- Interest starts earning interest.

- Your previous gains begin generating new gains.

- The snowball gets larger, and every rotation adds more than the last.

That's why long-term savers often see more growth in the second decade than in the first, even if they never increase their monthly deposits.

Consider another scenario:

Suppose you invest $100,000 earning an average annual return of 8%, compounded yearly.

In 10 years' time, your balance could approach $215,892. Now imagine waiting five years before investing that same $100,000. After ten years of growth, it would reach only about $147,010.

In this example, waiting five years costs nearly $69,000 in potential growth.

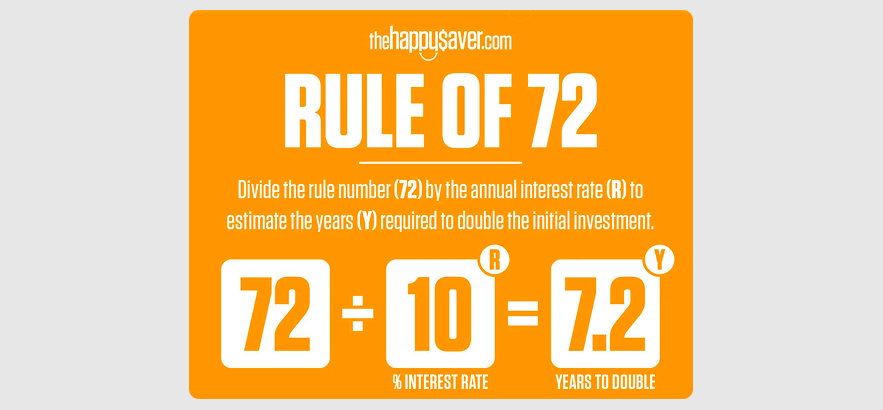

Rule of 72

One useful mental shortcut is the Rule of 72. Divide 72 by your annual return to estimate how many years it takes your money to double, regardless of the amount invested. For instance, at an 8% APR, your money will double in roughly 9 years (72 / 8 = 9). At a 4% return, it would take about 18 years (72 / 4 = 18).

Time in market beats market timing

Predicting future price movements is as alluring as it is notoriously risky. While timing the market is theoretically possible, it is widely considered impossible to do consistently. Crypto markets never sleep, are highly volatile, and are often driven as much by investor sentiment as by fundamentals.

In contrast, time in the market emphasizes a long-term view. It’s about staying the course through ups and downs, and understanding that the market has historically trended upward over long periods, though past performance never guarantees future returns.

$100,000 invested in the S&P 500 Composite for 30 years — from 1994 to 2024 — would have grown to $1,817,633. However, if you had tried to time the market instead and missed 10 of the best trading days, the total would be only $832,721. That's nearly $1 million in missed growth.

The same logic applies to crypto. Market timing depends on repeatedly making the right short-term decisions. Time in the market relies on staying invested long enough for long-term growth to work in your favor.

That's why many long-term investors use dollar-cost averaging (DCA): investing smaller amounts on a regular schedule instead of trying to guess the perfect entry point.

Consistency beats motivation

There's another advantage to starting small. It builds a habit.

Which is easier to repeat — saving $50 every month or trying to save $10,000 all at once? People who wait for the "right moment" often discover that the right moment never arrives.

Life happens. Unexpected expenses appear. Plans change.

People who automate even small deposits rarely have to think about it again.

Once the habit is automated, consistency requires much less effort than relying on motivation every month.

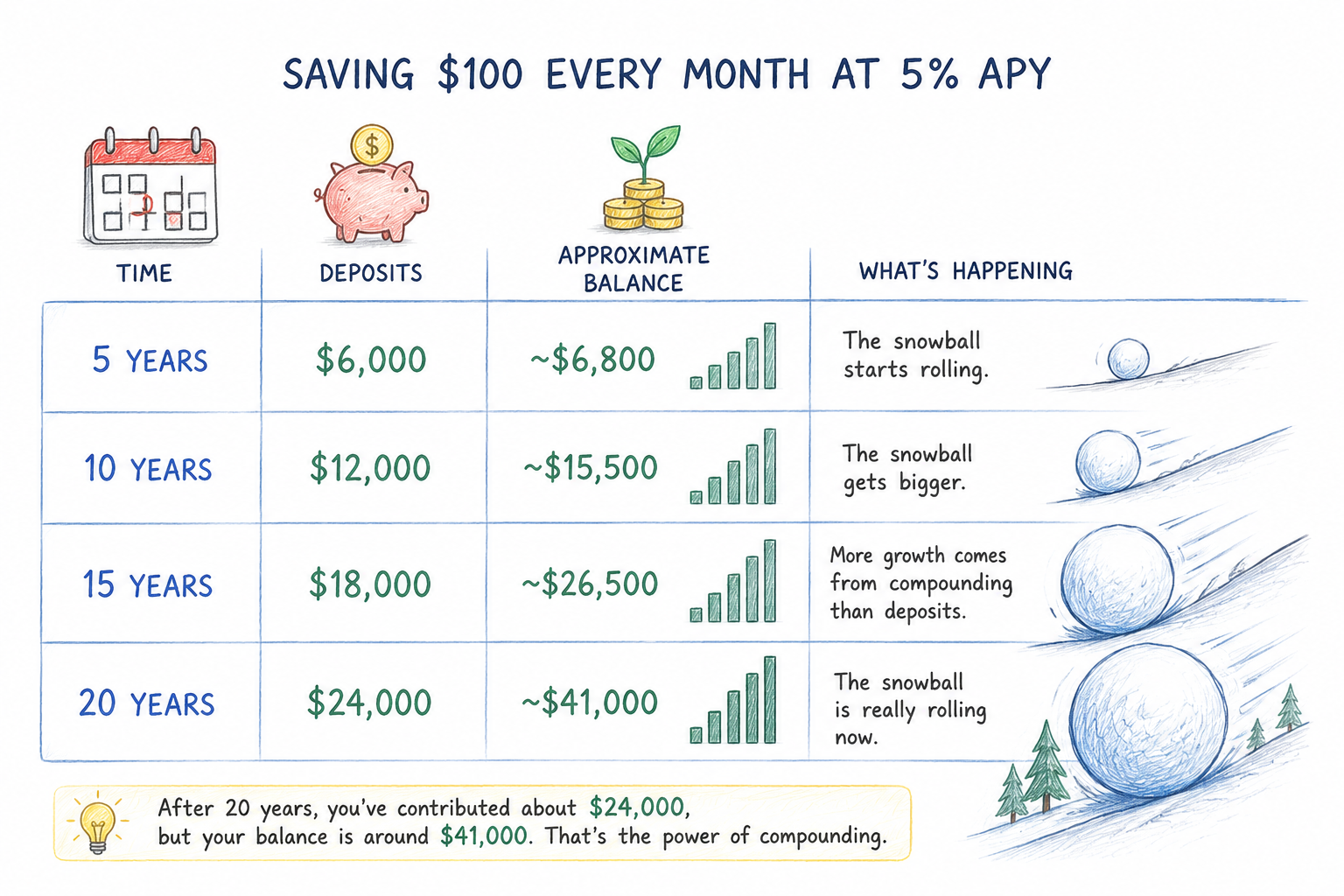

What this looks like over time

Imagine saving $100 every month at 5% APY. Notice something interesting: after twenty years, you've contributed about $24,000, but your balance is around $41,000.

Nearly half of the final balance comes from growth rather than your own contributions. That's the snowball effect.

What this means for your savings

In reality, waiting until you have "enough" often delays the one thing compounding needs most: time.

Even modest deposits can build meaningful savings if they're consistent. You can always increase your contributions later — but recovering the years you never invested is impossible.

Here's what happens when you delay investment until you have a significant lump sum:

- Eroded purchasing power, as inflation quietly diminishes your money's value. Investments that earn more than inflation help preserve your purchasing power over time.

- Heavier financial burden when you eventually invest, as you must contribute a much higher percentage of your income for longer periods.

- More pressure to take risk, because shorter investment horizons leave less time to recover from market downturns.

Getting started (with very little)

You don't need thousands of dollars to start building that habit.

On Clapp, Flexible Savings starts from the equivalent of $10, making it easy to begin with small, regular deposits while keeping your funds accessible with daily compounding. This is ideal for "dry powder" — stablecoins you're keeping available for future investment opportunities or unexpected expenses.

If you already have money you know you won't need for a while, Fixed Savings offers higher rates (up to 8.2% APR) in exchange for committing your funds for a fixed term.

Whether you start with $10 or $1,000, the important part is getting your money working instead of leaving it idle.

The earlier you begin, the longer compounding has to work

Building wealth rarely starts with one big deposit. More often, it starts with a small one — and another one the following month.

The habit of saving consistently is often more valuable than waiting for the perfect amount.

Start small, stay consistent, and let time do the heavy lifting.

Frequently asked questions

1. How much do I need to start?

On Clapp, Flexible Savings starts from the equivalent of $10.

2. Is $50 a month really enough to make a difference?

Yes. On its own, $50 may not seem significant, but consistent monthly deposits combined with compounding can grow into meaningful savings over time.

3. Should I wait until I've saved more?

Generally, no. If your money would otherwise sit in cash while you're saving, starting earlier gives compounding more time to work.

4. What if I can only afford $10 a month?

Start there. You can always increase your contributions later. Time is harder to replace than money.

5. Does this only apply to savings accounts?

No. The same principle applies broadly to long-term investing: consistent investing over many years is usually more important than trying to begin with a large amount.