Why most crypto borrowers care about the wrong number

When comparing crypto loans, the first thing most people look at is the interest rate.

4% APR. 6% APR. Maybe even 0% if you deposit enough collateral. It feels like the number that decides whether you're getting a good deal.

In reality, another percentage matters much more: your loan-to-value (LTV) ratio.

APR determines what you pay; LTV determines how much room you have before your position is at risk. That's why experienced borrowers tend to think about LTV first — and interest rates second.

TL;DR

- Interest rate tells you what you pay. LTV tells you how much room you have before liquidation.

- A low rate doesn't help if you get liquidated. Borrowing at 5% APR with 60% LTV is riskier than 8% APR with 20% LTV.

- LTV is your buffer against volatility. The lower your LTV, the more room you have for market drops.

- Some platforms offer 0% APR at low LTV. That aligns incentives — responsible borrowing costs nothing.

- Focus on LTV first. Interest rate second. The rate won't matter if you lose your collateral.

Look beyond APR

A low rate looks attractive, so you borrow more than you otherwise would — perhaps at 50% or even 60% LTV.

Then the market drops 30%. Suddenly your comfortable-looking loan becomes stressful. Your LTV jumps toward 70–80%, and you're scrambling to add collateral or repay part of the debt.

On most CeFi platforms, you'll usually receive margin-call alerts that give you a chance to react. In DeFi, however, there are often no warnings at all. Once your position crosses the threshold, smart contracts liquidate it automatically.

Meanwhile, another borrower accepted a slightly higher APR but started at just 20% LTV.

The same market drop barely changes their position. Their LTV rises to roughly 28%, leaving them comfortably below liquidation levels.

Same market. Same asset. Completely different experience.

All because of the size of that safety buffer.

This isn't just theory

One Redditor shared how they lost part of their ETH collateral after borrowing against it on a DeFi lending platform. The interest rate wasn't the problem. Their collateral value fell, their loan-to-value ratio deteriorated, and a liquidation bot closed the position before they had time to react. As they put it: "I never pressed sell."

That's exactly why seasoned crypto borrowers tend to watch their LTV more closely than APR. The interest rate affects how much your loan costs over time; LTV determines whether you get to keep your collateral in the first place. The more room it gives you, the less likely you'll have to deal with margin calls on CeFi platforms — or automatic liquidations on DeFi protocols.

Decoding your LTV

LTV is your loan amount divided by your collateral value.

- Borrowing $10,000 against $50,000 worth of Bitcoin gives you an LTV of 20%.

- Borrowing $30,000 against the same collateral starts you at 60%.

The higher your LTV, the smaller your safety buffer.

Liquidation thresholds vary between lenders. Suppose it's the common 80%.

At 20% LTV, your collateral would need to drop about 75% to hit that liquidation threshold. At 60% LTV, a 25% drop puts you in danger.

Interest rate is secondary

Interest rate matters — because who wants to overpay? But interest rate only matters if your loan survives, which is only possible if your LTV stays safe.

Interest rates affect the cost of borrowing. LTV determines which APR bracket you fall into on platforms with tiered pricing, and whether you get to keep your collateral.

Saving a few percentage points on APR won't matter if an aggressive LTV leaves you exposed during a market correction.

That's why risk comes first; cost comes second.

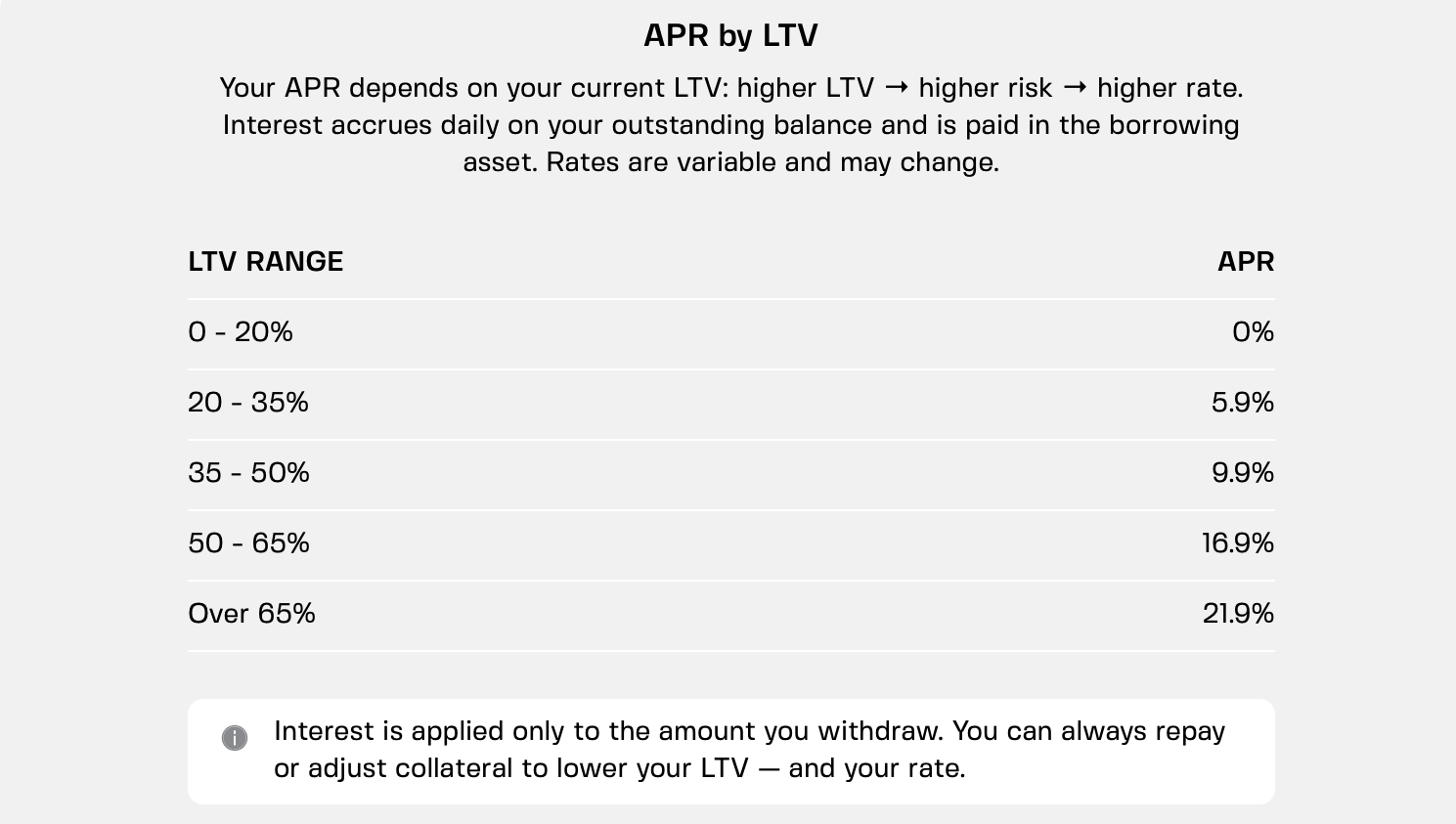

The 0% APR exception

Some platforms reward conservative borrowing. On Clapp, maintaining an LTV of 20% or below qualifies for 0% APR.

The idea is simple: lower risk for the platform means lower borrowing costs for you. This mechanism aligns your incentives with the platform's.

Borrow responsibly and you pay nothing. Borrow more aggressively and standard rates apply.

The best deal is the lowest rate at the safest LTV.

LTV vs. APR

Many borrowers know their APR to two decimal places but couldn't tell you their current LTV without opening the app.

That's backwards.

Depending on the lender, APR may stay the same. But LTV changes every time the market moves. It's the number that tells you how close you are to liquidation — and on some platforms, it also determines how much interest you pay.

One simple rule

There's no universal "perfect" LTV, but one principle works for anyone: lower is safer.

Around 20% is widely considered a conservative starting point. At that level, Bitcoin would have to lose roughly three quarters of its value before reaching an 80% liquidation threshold.

If you need to borrow substantially more than a 20% LTV allows, it's worth asking whether you're borrowing too much — not whether the interest rate is low enough.

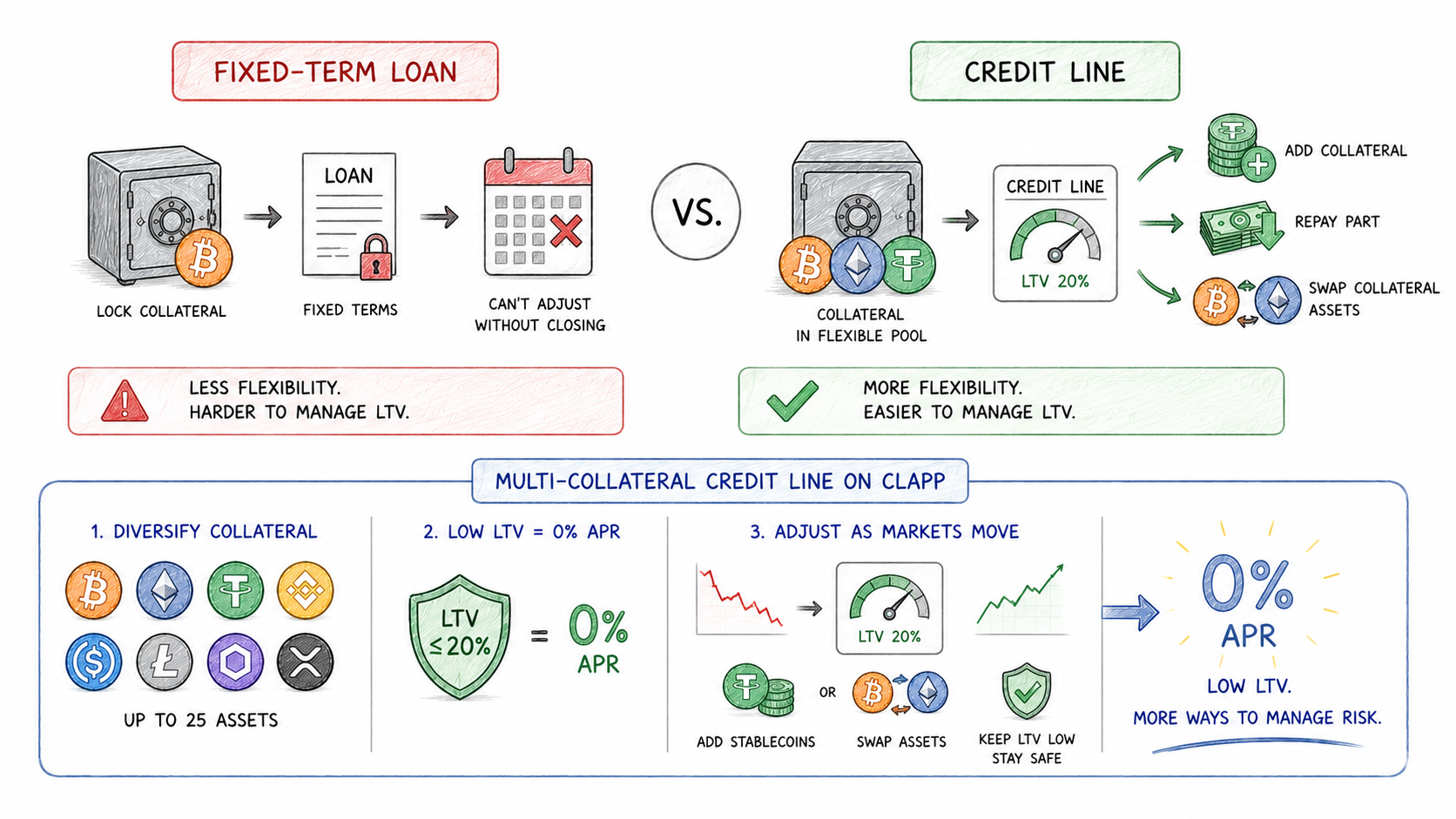

How credit lines help

Fixed-term loans generally leave you with fewer options once they're opened.

Credit lines give you more flexibility after you've borrowed. You can repay part of the balance, add more collateral, or — on some platforms — even swap collateral assets without closing the position.

That makes managing your LTV much easier when markets become volatile.

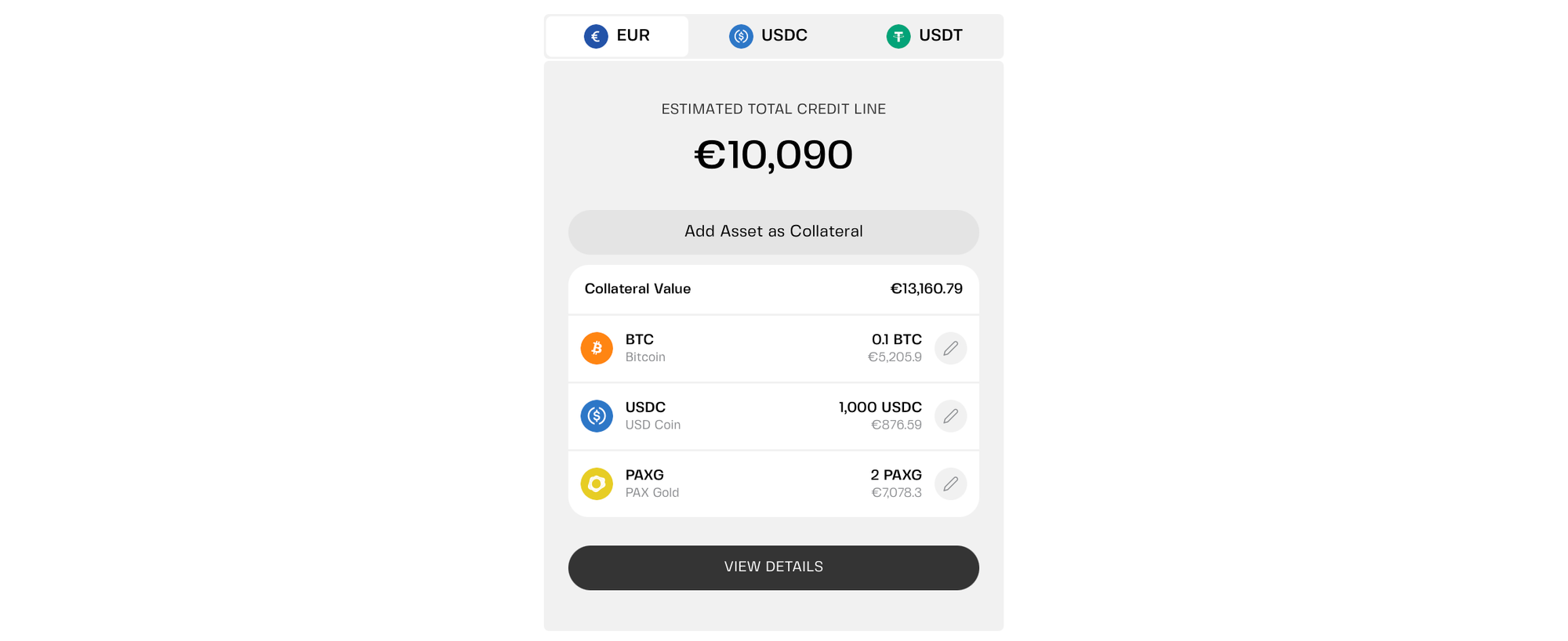

Example: Zero-interest borrowing with low LTV

On Clapp, you can keep your LTV at 20% or below and pay 0% APR.

You can also mix up to 25 assets in your collateral pool. That means you can stabilize your LTV by adding stablecoins to your collateral basket.

If your LTV starts to creep up, you can swap collateral assets — BTC to stablecoins — without closing your credit line.

The system is designed to help you focus on the right number. And because one credit line can be backed by a basket of up to 25 assets, you have more ways to manage risk as markets change.

In short, don't obsess over interest rates

Most crypto borrowers focus on the wrong number, shopping around for the lowest APR and comparing fractions of a percent. Seasoned borrowers compare safety buffers.

APR determines the cost of borrowing. LTV determines how resilient your position is during a market downturn. That's why conservative borrowing starts with the right LTV, not the lowest advertised rate.

Frequently asked questions

1. What's the safest LTV for a crypto loan?

20% LTV is very safe. At that level, your collateral would need to drop about 75% to hit an 80% liquidation threshold. 30% is still reasonable. 50% or higher puts you at serious risk.

2. Can I lower my LTV after borrowing?

On credit lines, yes. You can add more collateral, repay part of the drawn amount, or swap to more stable assets. On fixed loans, you usually can't adjust without closing the loan.

3. Why would I borrow at 8% APR when another platform offers 5%?

Because the 5% platform might require higher LTV. Or it might have hidden fees. Compare the full package — not just the rate.

4. How often does LTV change?

Every time your collateral's price moves. If the market is volatile, your LTV can change significantly in a single day.

5. Is 0% APR at 20% LTV a good deal?

Yes. It's the best combination of safety and cost. You get a massive buffer and zero interest. It's available on some platforms — including Clapp. Not all platforms offer it.