Borrowing against crypto, explained simply

You have crypto, but need cash. Selling feels wrong.

Maybe you've been holding for years and don't want to trigger taxes. Maybe you believe the price will go higher. Or maybe you just don't want to lock in a loss.

Whatever the reason, there's another way: borrowing against that crypto instead of selling it.

This guide skips the confusing terms and fine-print traps. Here's what actual beginners need to know.

TL;DR

- Borrowing isn't selling. No tax event triggered, and you also keep your coins. If the price goes up, you still benefit.

- You must deposit more crypto than you borrow. That's called over-collateralization. It's what lenders do to protect themselves from price drops.

- LTV is the only number you really need to understand. It stands for loan-to-value — how much you borrow compared to what you put up as collateral.

- Keep LTV low. 20% is very safe. 50% is risky. 70% is gambling.

- You'll get warnings if your LTV gets too high. Don't ignore them. Add more collateral or pay back some of the loan.

- Some platforms offer 0% APR at low LTV. That means your credit line costs nothing until you use it.

What actually happens when you borrow

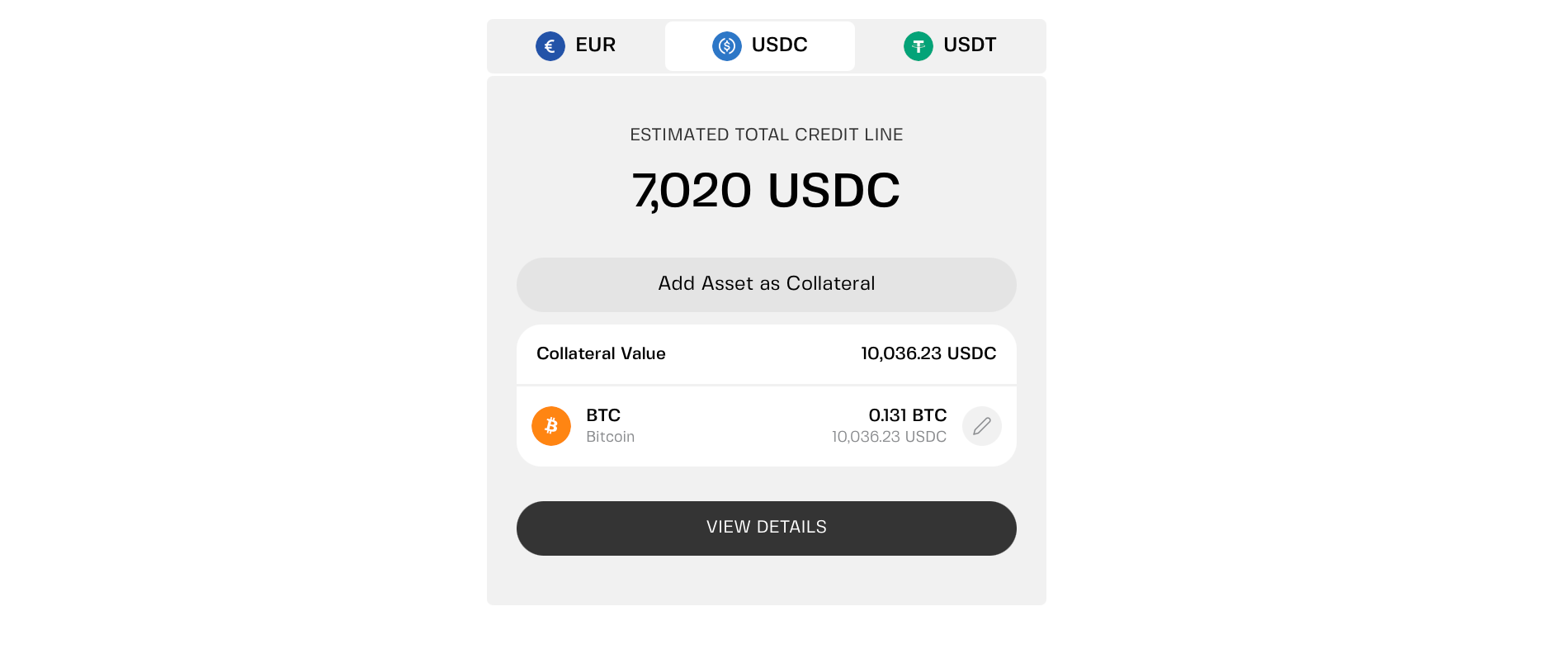

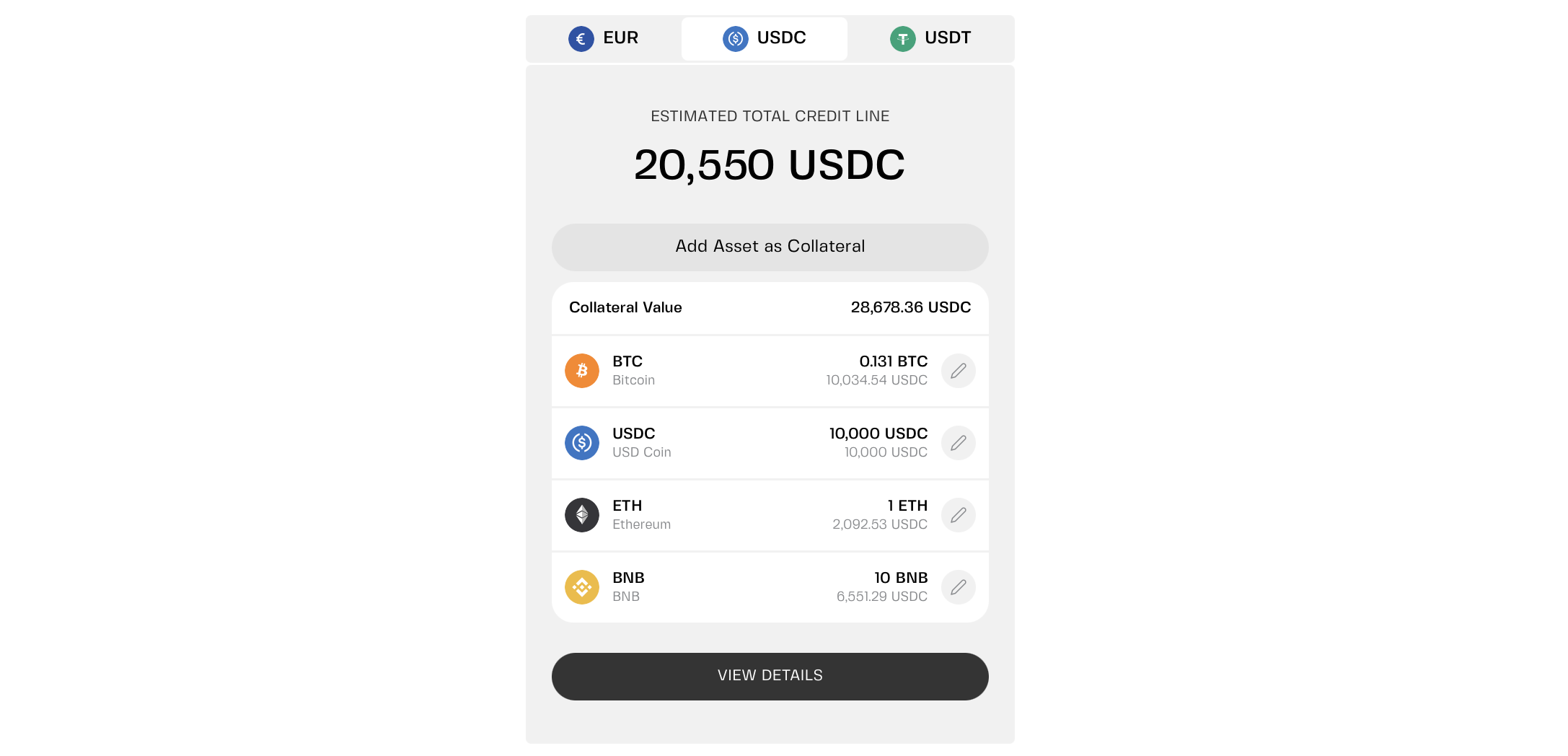

You deposit crypto into a platform. That's your collateral. Based on the asset and its value, the platform will let you borrow up to 50–70% of its value in fiat or stablecoins (for instance, USDT or USDC).

That percentage is called LTV, or loan-to-value.

Example: You deposit $10,000 in Bitcoin. The platform lets you borrow up to $7,000 at 70% LTV. You decide to borrow only $2,000. Your LTV is 20%.

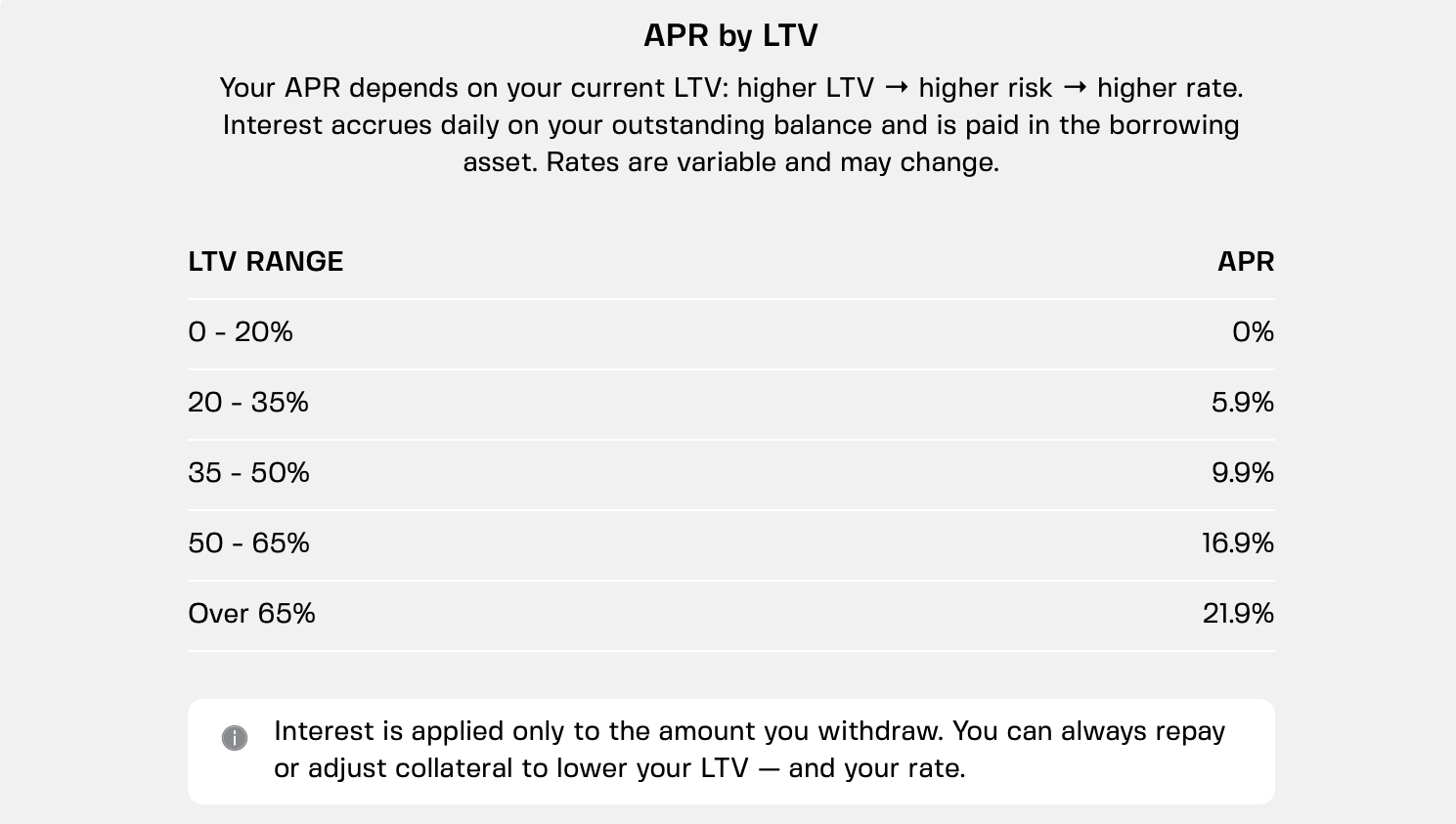

Why would you borrow less than the max? Because lower LTV means lower risk. If the market drops, your loan is still safe. Plus, platforms like Clapp even give you 0% APR for keeping LTV within a low tier.

You don't sell anything, so your Bitcoin stays in the platform's custody. When you repay the loan, your collateral is released. You keep your upside exposure, and in most jurisdictions borrowing itself isn't a taxable event.

The one number you need to understand

LTV is simple. It's just your loan amount divided by your collateral value.

- Borrow $2,000 against $10,000 in Bitcoin? That's 20% LTV.

- Borrow $5,000 against $10,000? That's 50% LTV.

- Borrow $7,000 against $10,000? That's 70% LTV.

Lower is safer. At 20% LTV, Bitcoin would need to drop about 75% to put you in danger. At 70% LTV, a normal 30% market drop could wipe you out.

Lower is also cheaper. Modest LTV means lower risk for the lender, which is why they incentivize responsible borrowing with lower interest for specific thresholds — sometimes, as low as 0%.

What happens when the market drops

This is where beginners get into trouble.

- You borrow $2,000 with BTC worth $7,000. Your loan is still $2,000. Your LTV climbs to about 28%. You're still safe. But you're closer to the danger zone.

- If Bitcoin drops 50%, your collateral is $5,000. Your LTV is 40%. Still safe, but getting higher.

The platform will warn you. Most centralized platforms send alerts when your LTV approaches 70-80%. You'll have time — usually 24-72 hours — to add more collateral or pay back part of the loan. When market plunges dramatically, that gap shrinks fast.

If you ignore the warnings and the prices keep dropping, the platform may sell some of your collateral to cover the loan. That's called liquidation. It might happen at the worst possible moment, you lose part of your crypto — and as it is sold, taxes may apply.

Your best protection against liquidation is disciplined borrowing. Borrow less, keep LTV low, and have extra collateral ready just in case.

How to borrow without stress

Here's a simple plan that works for most beginners.

- Keep LTV at 20% or below. That means borrowing $2,000 for every $10,000 in collateral. You won't get rich overnight, but you also won't lose sleep — and your costs may remain at 0% APR.

- Have extra collateral ready. Keep some stablecoins in a savings account or more Bitcoin on the side. If the market drops and LTV climbs, you can add collateral instantly.

- Use a credit line, not a fixed loan. Credit lines let you borrow only what you need, pay interest only on what you use, and repay on your own schedule. Fixed loans charge interest on the full amount from day one.

- Use multi-collateral products. If needed, you can free up collateral assets by swapping them — without closing your credit line. On Clapp, you can deposit up to 25 different assets, even fiat. Pledged ETH but want to switch to BTC? No problem.

- Set price alerts. Don't rely on the platform alone. Set alerts for your collateral asset. Know when you're getting close to danger before the platform tells you.

- Read the fine print. Some platforms charge origination fees, liquidation fees, or hidden spreads.

When borrowing makes sense

Borrowing is for people who believe in their crypto long term but need cash now.

Good reasons to borrow

- You need liquidity for a planned expense without selling your position

- You want to avoid a taxable event

- You spotted an opportunity and need funds fast

- You want a safety net that doesn't cost anything until you use it

Bad reasons to borrow

- You want to gamble on leverage

- You need money and don't have other options

- You're borrowing just because everyone else is

Borrowing is a tool for bridging a gap. Do not use it to chase bets you can't afford — that's a recipe for disaster, not outsmarting the market.

Keep LTV low. Have a backup plan. Don't ignore margin calls.

Do those three things, and borrowing can be a smart way to access cash without selling your crypto. Ignore them, and you could join the long list of people who learned these lessons the hard way.

Borrowing against crypto isn't complicated. But it's also not something you should rush into without understanding the basics.

Borrow conservatively, plan for the worst, and keep your upside.

Frequently asked questions

1. Do I need good credit to borrow against crypto?

No. Your collateral is all that matters. No credit checks, no income verification, no paperwork. You deposit crypto as collateral and borrow against it.

2. What's the difference between a loan and a credit line?

A loan gives you a lump sum with fixed repayments. A credit line gives you a limit — draw what you need, pay interest only on what you use, and repay on your own schedule.

3. Can I lose my crypto if I borrow against it?

Yes — if you ignore margin calls and get liquidated. But if you borrow conservatively (low LTV) and stay on top of notifications, you can avoid it.

4. Do I have to pay taxes when I borrow?

In most places, no. Borrowing isn't a sale, so it's not a taxable event. But interest payments, liquidations, or swapping collateral could trigger taxes. Check local rules.

5. How much should a beginner borrow?

Start with 20% LTV or less. That means borrowing $2,000 for every $10,000 in collateral. It's safe, gives you useful liquidity, and costs 0% APR on platforms that offer it. Once you're comfortable, you can adjust from there.