What if Bitcoin drops 50% tomorrow? Stress-testing your crypto loan

A 50% drawdown might sound extreme, but Bitcoin has been through much worse.

During the most recent market cycle, it lost roughly half its value from peak to trough. For anyone using crypto as loan collateral, it became a real-world stress test.

So what would have happened if you had borrowed against your Bitcoin before the decline?

Let's walk through it.

TL;DR

- Bitcoin is down roughly 50% from its October 2025 peak. This might be the shallowest bear market in Bitcoin's history, but it still wiped out billions in leveraged positions.

- LTV can change quickly. A 50% drop can turn a comfortable loan into one that's approaching liquidation.

- The decline happened in stages. Borrowers who prepared early had time to react. Those who waited got caught.

- Liquidation isn't instant on CeFi. You usually get warnings and a grace period. But if you ignore them, your collateral gets sold at the worst moment.

- Preparation beats reaction. Conservative borrowing, extra collateral, and understanding your platform's liquidation rules make a huge difference.

The market reality

This was a slow bleed with sharp moments of panic.

Bitcoin hit its all-time high of roughly $126,000 in early October 2025. On October 10, 2025, it dropped from roughly $122,000 to $102,000 in under an hour, wiping out over $19 billion in leveraged positions.

That was just the beginning. A deeper correction followed in early 2026, before prices continued sliding.

By March, it was trading near $70,000. By June, it had dipped below $60,000.

Between October 2025 and April 2026, $988 billion in market value simply evaporated.

If you're curious how previous bear markets unfolded, we've covered Bitcoin's biggest crashes and what investors learned from them in a separate guide.

Stress test: How different borrowers fared

Suppose you borrowed against BTC in early October 2025 — right before its all-time high — and did not add any new collateral. Would this plunge have wiped out your BTC by now?

This depends on the initial LTV (loan-to-value) ratio. The less you borrow relative to your collateral, the bigger your buffer when the market goes south.

Scenario A: Conservative borrower

You deposit $50,000 in Bitcoin and borrow $15,000. Your LTV is 30%.

Bitcoin drops 50%. Your collateral is now worth $25,000. Your loan is still $15,000. Your LTV climbs to 60%.

You're probably still safe, but your margin for error has almost disappeared. Most platforms have thresholds around 70-80%, so another meaningful drop could push you into liquidation territory.

Scenario B: Aggressive borrower

You deposit $50,000 in Bitcoin and borrow $30,000. Your LTV is 60%.

Bitcoin drops 50%. Your collateral is now worth $25,000. Your loan is still $30,000. Your LTV is now 120%.

Your collateral is liquidated to repay the outstanding debt. Depending on the platform and market conditions, you may receive any remaining balance after the loan is settled — but you've still been forced to sell at one of the worst possible moments.

Scenario C: Risk-averse borrower with a buffer

You deposit $50,000 in Bitcoin and borrow $10,000. Your LTV is 20%.

Bitcoin drops 50%. Your collateral is now worth $25,000. Your LTV climbs to 40%.

You're still well within safe limits. No margin call panic, no liquidation. Your coins are intact, you can ride out the volatility without being forced into action.

In the case of a credit line, that 20% LTV may also qualify you for 0% APR. If prices fall, you can maintain that low-LTV bracket by adding more collateral as needed.

What actually happens during a drop

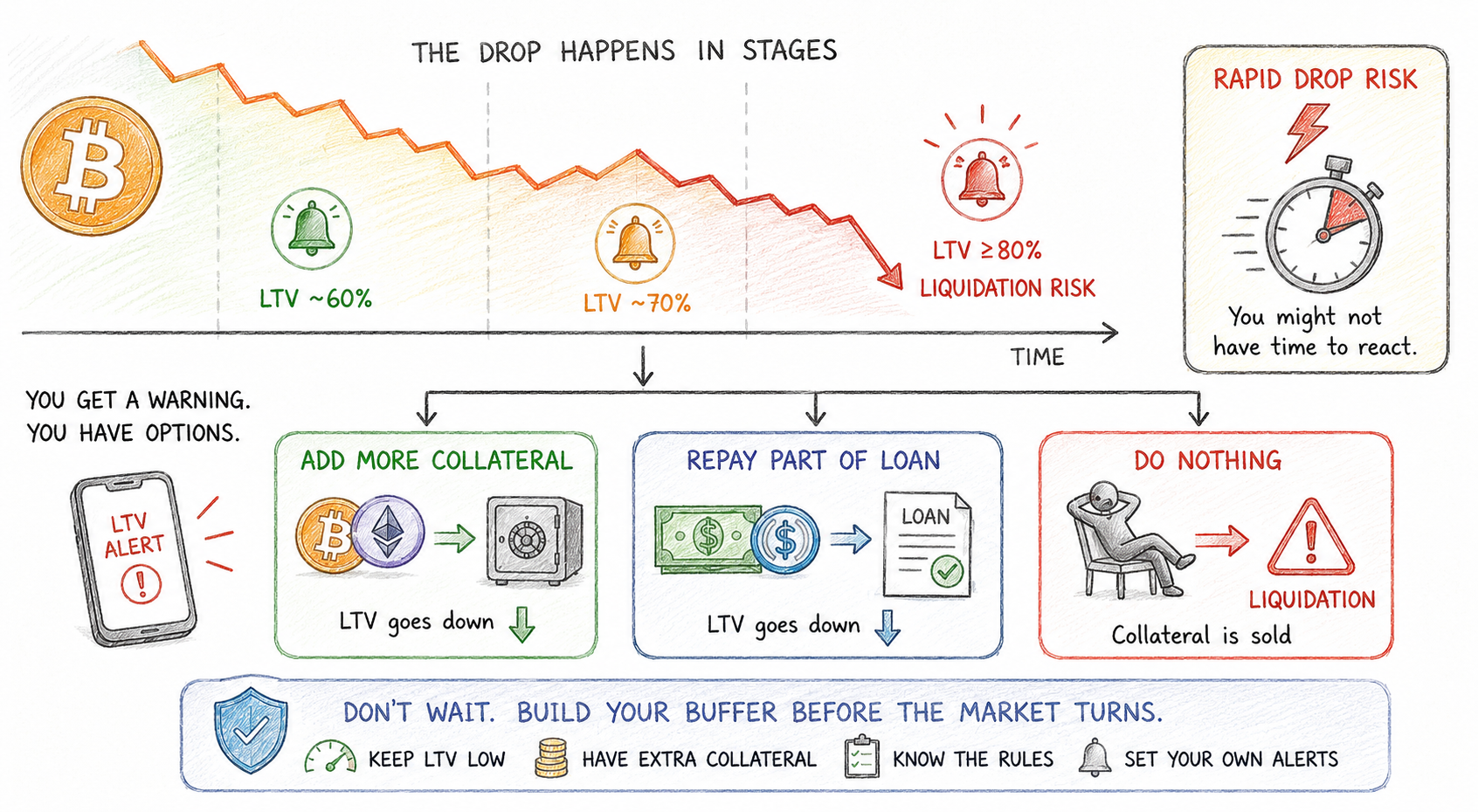

The decline didn't happen all at once. That's important.

If you had a loan during this period, you got warnings. On CeFi platforms, you usually get a notification when your LTV crosses a certain threshold — typically around 60-70%. These alerts are designed to give you a chance to act before liquidation becomes necessary.

Your options:

- Add more collateral. Transfer additional crypto to your collateral pool. This lowers your LTV immediately.

- Repay part of the loan. Pay down what you owe using cash or stablecoins.

- Do nothing. If you ignore the warnings and the market keeps dropping, the platform will liquidate your collateral.

The problem is that during a rapid drop like the one on October 10, 2025 — when Bitcoin fell $20,000 in under an hour — you might not have enough time to react even with a warning.

That's why waiting isn't really a strategy. The safest borrowers build their buffer before the market turns.

A shallow bear market — but still brutal

While this decline was smaller than several previous Bitcoin bear markets (with drops of 75-90%), it was still severe enough to liquidate thousands of leveraged positions.

But "shallow" doesn't mean "painless." Over 90,000 traders were liquidated in a single 24-hour period in June 2026. Leverage cuts both ways.

The key insight: The decline happened in stages, but the sharp moments of panic were what caught people off guard.

If you prepared early — kept LTV low, had extra collateral ready, knew your platform's rules — you survived. If you waited until the market was already down 30% to start thinking about your LTV, you were already behind.

How to prepare for the next drop

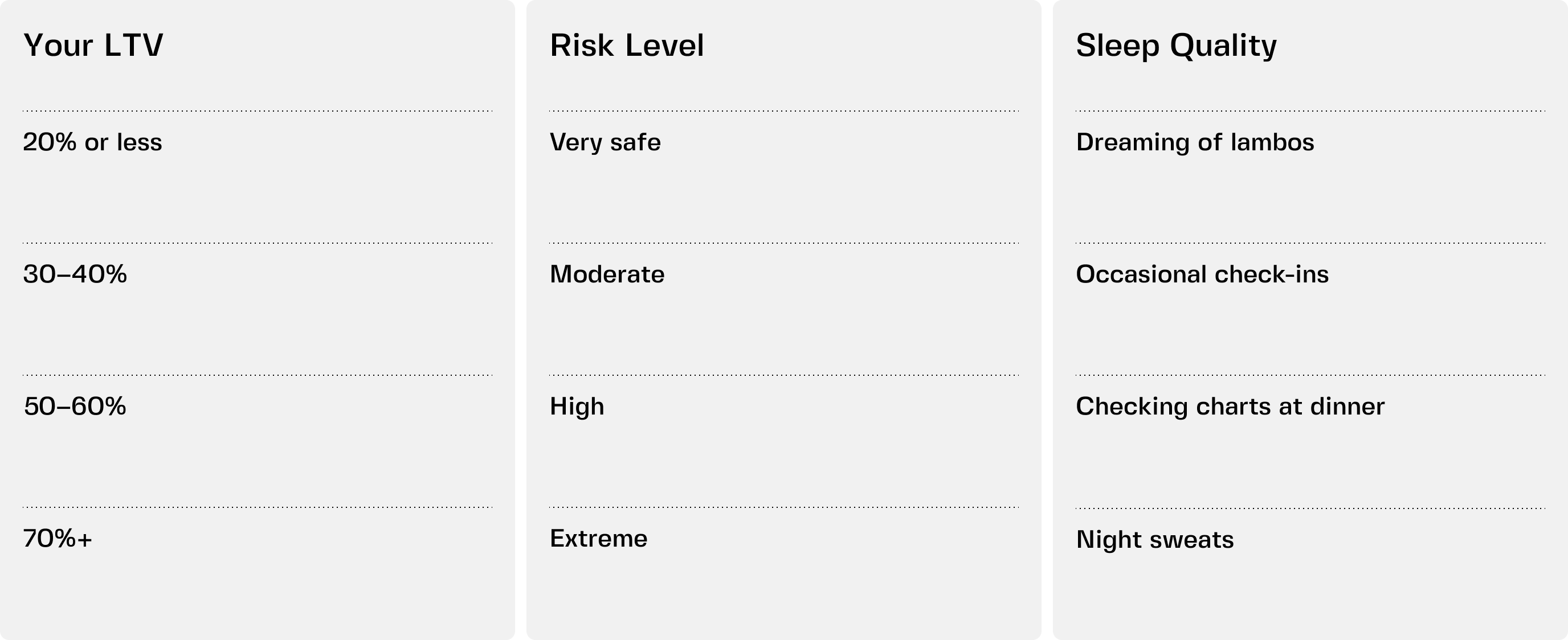

- Keep LTV low from the start. 20-30% LTV gives you a massive buffer. At 20% LTV, Bitcoin would need to drop roughly 75% to hit an 80% liquidation threshold.

- Keep extra collateral ready. Hold stablecoins in flexible savings or maintain unencumbered crypto that can quickly be added to your collateral pool. When the margin call comes, you'll be glad you planned ahead.

- Know your platform's rules. What's the LTV threshold for warnings? For liquidation? How long do you have to act? Read before you borrow.

- Set your own alerts. Don't rely on the platform alone. Set price alerts for your collateral assets. Know when you're getting close to danger before the platform tells you.

- Choose a multi-collateral credit line. Unlike a fixed crypto loan, it lets you add, remove, or swap collateral without closing your position. Backing your credit line with a basket of assets instead of a single coin gives you more ways to manage risk when markets become volatile.

What this looks like on Clapp

On Clapp, you can secure a single credit line with a basket of up to 25 assets rather than relying on just one cryptocurrency. BTC, ETH, stablecoins, and fiat can all sit in the same collateral pool.

That gives you more ways to manage risk. Instead of closing your loan and starting over, you can add, remove, or swap collateral as market conditions change.

Combined with 0% APR at 20% LTV or below, it gives borrowers considerably more flexibility than traditional fixed crypto loans.

Preparation beats reaction

Bitcoin has fallen 50% before, and history suggests large drawdowns are part of the asset's lifecycle. Whether a crypto loan survives those periods depends far less on luck than on preparation.

Conservative LTV, available backup collateral, and a flexible credit line can turn a market crash from a crisis into something you simply manage.

You can't control the next bear market. You can control how prepared you are when it arrives.

Frequently asked questions

1. How fast can a margin call happen?

On CeFi platforms, you usually get some time to act, depending on the lender. But during rapid drops like the October 10, 2025 flash crash — when Bitcoin fell $20,000 in under an hour — you might not have much time.

2. Can I lose more than my collateral?

No. In a standard crypto loan, your losses are limited to your collateral. The platform sells what you pledged to cover the loan. You don't owe anything beyond that.

3. What's the safest LTV to survive a 50% drop?

20% LTV is very safe. At that level, your collateral would need to drop about 75% to hit an 80% liquidation threshold. 30% is still reasonable. 50% or higher puts you at serious risk.

4. What happens if I get liquidated?

The platform sells your collateral at market price to repay the loan. Often during a crash, when prices are at their worst. You keep whatever is left after the loan is repaid, minus any fees.

5. Should I avoid borrowing altogether if I'm worried about crashes?

Not necessarily. You just need to borrow conservatively and have a plan. Many people borrow at 20-30% LTV, keep stablecoins as a buffer, and sleep fine through crashes. The problem usually isn't borrowing itself — it's borrowing too much against volatile collateral.