Three jobs for one portfolio: Earn yield, borrow cash, stay invested

Most people think of their crypto portfolio as one thing: a collection of assets that rises and falls with the market. But a portfolio can do much more than simply track prices.

With the same pool of capital, you can earn yield on idle assets, access liquidity without selling, and stay invested for the long term.

It sounds complicated, but it isn't.

Let's look at how one portfolio can do all three jobs — and why that's often more effective than treating each one separately.

TL;DR

- Your portfolio can do more than one job. Earn yield, access liquidity, and stay invested using the same pool of assets.

- Savings put idle capital to work. Flexible savings prioritize access, while fixed savings reward longer commitments with higher rates.

- Credit lines provide liquidity without selling. Keep LTV low and some platforms even offer 0% APR.

- Staying invested preserves long-term upside. No forced sale, no taxable event in many jurisdictions, and no missing out on future gains.

- The three pieces work best together. Savings, credit lines, and long-term holdings complement each other rather than compete.

Job 1: Earn yield

The first job is the simplest: put idle cash and stablecoins to work.

The goal isn't to generate spectacular returns. It's to make sure cash isn't sitting idle. Even earning 5% is better than earning nothing.

Most platforms offer two approaches.

Fixed savings pay a higher rate in exchange for locking your funds for a set period. On Clapp, that's up to 8.2% APR for terms between one and twelve months. This works well for the portion of your portfolio you're confident you won't need anytime soon.

Flexible savings keep your funds available while still generating yield. You can withdraw whenever you need the money, making them ideal for emergency reserves or short-term opportunities. On Clapp, Flexible Savings earn up to 5.2% APY on stablecoins and EUR with daily compounding.

Job 2: Access liquidity without selling

The second job is giving your portfolio access to cash without forcing you to sell your assets.

A credit line isn't just something you open when you suddenly need cash. It can be a source of liquidity that's already in place whenever an opportunity or unexpected expense appears.

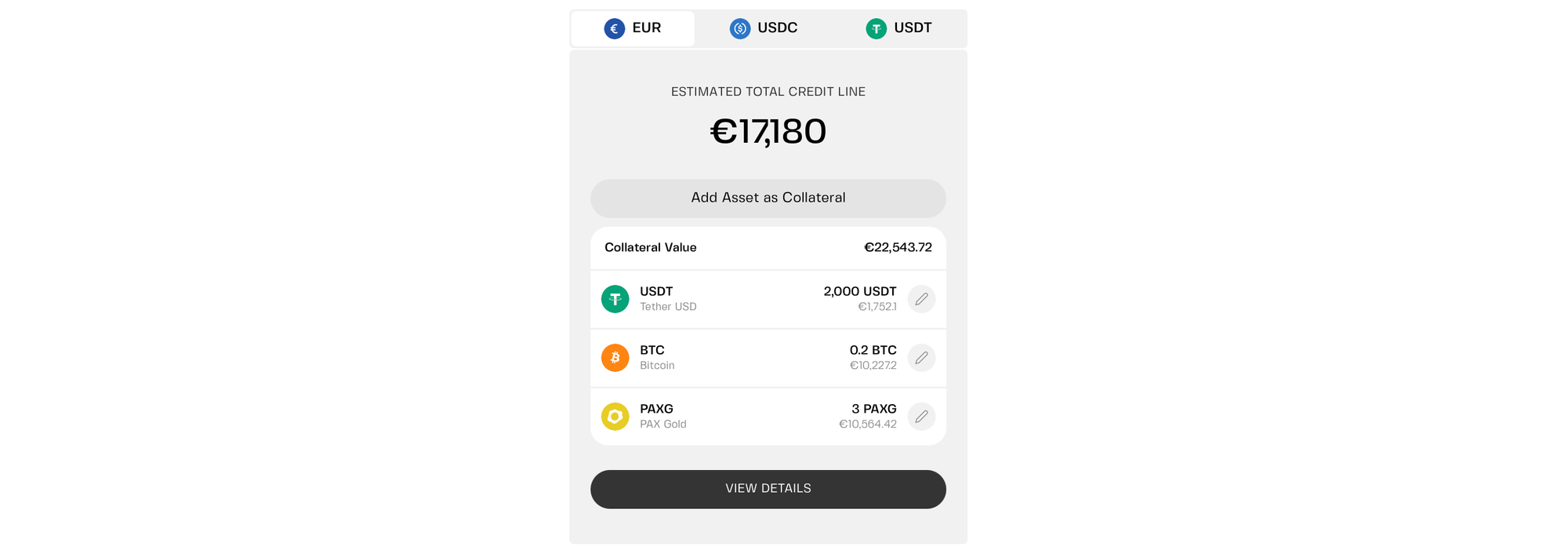

You deposit crypto as collateral and receive a credit limit. Unlike a traditional loan, you don't have to borrow the full amount. Draw only what you need, when you need it, repay on your own schedule, and borrow again later if necessary.

You pay interest only on the amount you've actually borrowed — not on the entire credit limit. On some platforms, including Clapp, maintaining an LTV of 20% or below also qualifies you for 0% APR.

That means your credit line can sit there, ready to use, without costing you anything until you decide to draw from it.

- So when do you borrow? When you need liquidity but don't want to sell your crypto — whether it's for an unexpected expense, a business opportunity, or another investment.

- And when don't you borrow? Most of the time. Simply having the credit line available gives you options when circumstances change.

Job 3: Stay invested

When you borrow against your crypto instead of selling it, you stay invested. Your position remains intact, and so does your exposure to future upside.

If the market rebounds, you're still holding your assets. You didn't sell at the bottom, and in many jurisdictions you also avoided triggering a taxable event.

That's where borrowing adds value. Not because it lets you take on more leverage, but because it gives you another way to access liquidity without giving up your long-term investment thesis.

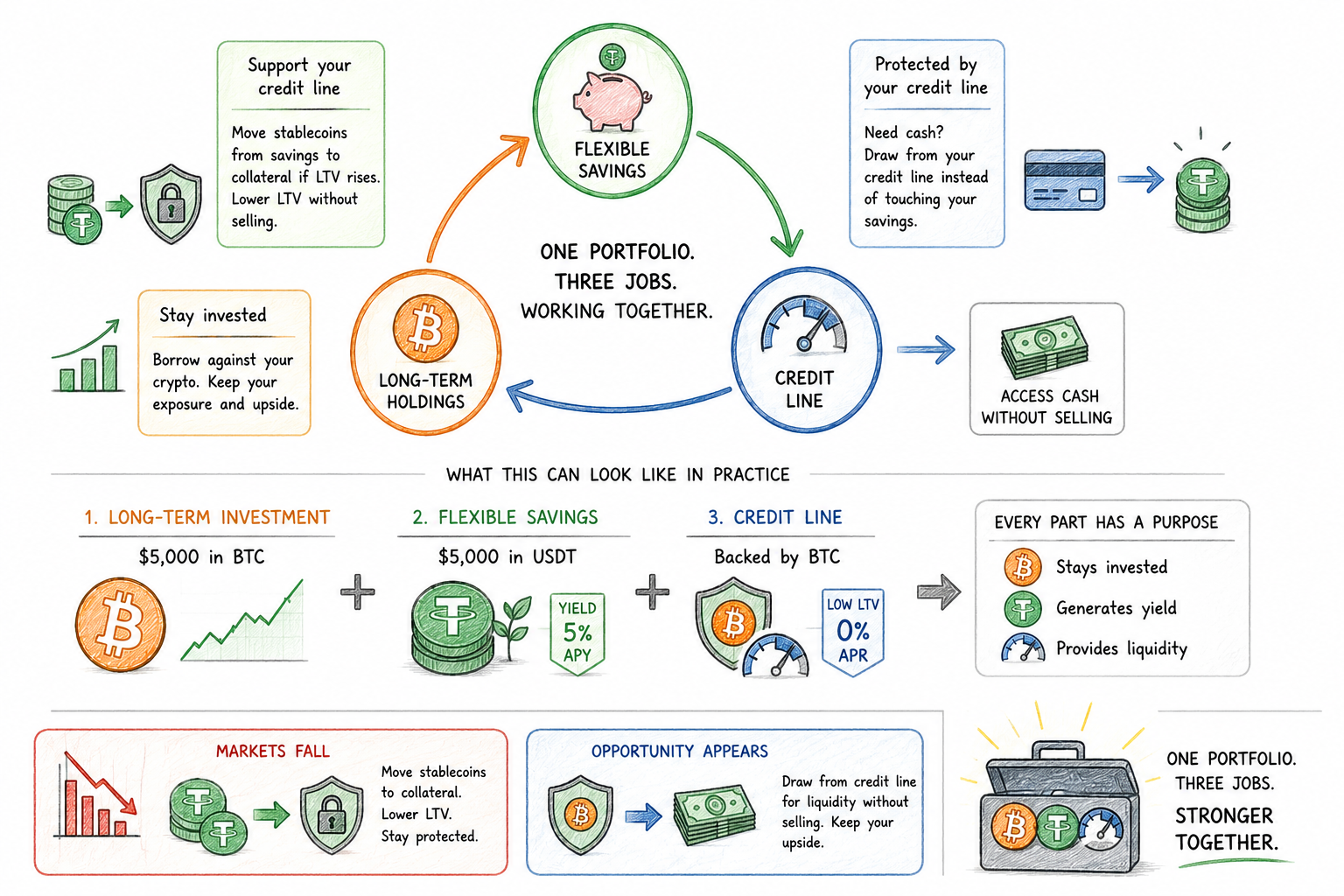

How the three jobs work together

The real advantage appears when all three parts support each other.

Flexible savings can support your credit line.

If your LTV rises during a market downturn, you can move stablecoins from flexible savings into your collateral pool in minutes. That lowers your LTV without forcing you to sell assets, helping you stay comfortably within your target borrowing range.

Your credit line can protect your savings.

When you need cash, you don't necessarily have to withdraw money that's earning yield. Instead, you can draw from your credit line while your savings continue compounding.

Your portfolio stays invested.

Instead of selling long-term holdings whenever you need liquidity, you borrow against them. That keeps your market exposure intact while giving you access to cash when opportunities or unexpected expenses arise.

Here's what that might look like in practice.

- Keep $5,000 in Bitcoin as your long-term investment.

- Allocate $5,000 in USDT to Flexible Savings, where idle stablecoins continue earning yield while remaining available if needed.

- Open a credit line backed by your Bitcoin at a conservative LTV, so liquidity is available whenever you need it.

Now every part of the portfolio has a purpose.

Your Bitcoin stays invested. Your savings generate yield. Your credit line sits ready in the background to provide liquidity whenever you need it.

If markets fall, your savings can strengthen your collateral. If an opportunity appears, your credit line can provide liquidity without forcing you to sell. Instead of relying on a single tool, your portfolio becomes a system where each part supports the others.

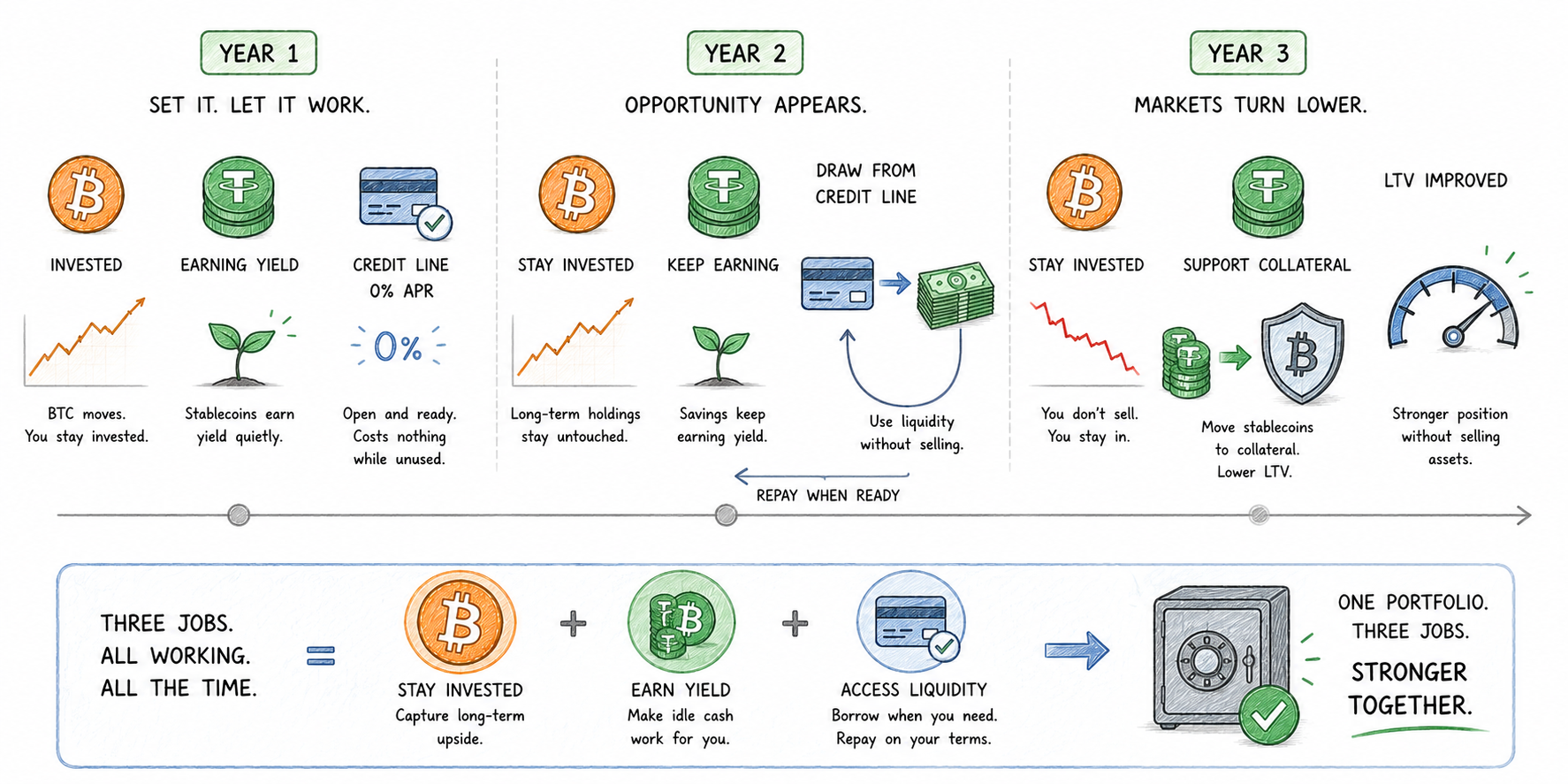

What this looks like over time

Now imagine you've put this strategy in place.

Year 1: Your stablecoins quietly earn yield. Your Bitcoin moves with the market, but you stay invested. Your credit line remains open, costing nothing while you don't use it.

Year 2: A new investment opportunity appears. Instead of selling your crypto, you draw from your credit line. Your long-term holdings remain untouched, your savings continue earning yield, and you repay the credit line when you're ready.

Year 3: Markets turn lower. As your LTV rises, you transfer stablecoins from flexible savings into your collateral pool, bringing your LTV back down and strengthening your position without selling your assets.

Throughout the entire period, the same portfolio has been doing three jobs at once: generating yield, providing liquidity, and staying invested for the long term.

Clapp: Triangle strategy in practice

Clapp brings these building blocks together in one ecosystem.

- Flexible Savings keep idle assets earning yield while remaining available whenever you need them.

- Fixed Savings offer higher rates for funds you're comfortable locking away for longer periods.

- Credit Lines provide liquidity without requiring you to sell your crypto.

And because Clapp supports multi-collateral credit lines, you can secure one credit line with a basket of up to 25 assets and adjust that collateral over time instead of relying on a single coin.

Instead of managing separate products across multiple platforms, you can build the entire strategy in one place.

Your portfolio doesn't have to serve just one purpose

One part can generate yield. Another can provide liquidity. Your long-term holdings can continue participating in the market.

Rather than choosing between earning, borrowing, and investing, you can combine all three into a single strategy where each part supports the others.

That's what makes a portfolio resilient — not just in bull markets, but across full market cycles. Your capital works harder without requiring you to take on additional risk.

Frequently asked questions

1. Can I really earn yield and borrow at the same time?

Yes. Your savings continue earning yield while your credit line remains available. If you decide to borrow, you're using your collateral—not the funds held in savings.

2. Do I need to lock my savings to open a credit line?

No. Your credit line is secured by your collateral, while your savings remain separate. You can use one without affecting the other.

3. What happens if my collateral falls in value?

If your LTV starts rising, you can add more collateral to reduce it. Keeping stablecoins in flexible savings makes that much easier because they're immediately available when needed.

4. Does borrowing reduce the yield on my savings?

No. Your savings continue earning yield independently of your credit line. The only exception is if you decide to move part of those savings into your collateral pool.

5. Is this strategy only for experienced investors?

Not at all. The idea is straightforward: keep part of your portfolio earning yield, maintain a conservative credit line for liquidity, and stay invested for the long term. The amounts can scale up or down depending on your portfolio.