DeFi vs. CeFi borrowing: Where should you put your crypto?

You want to borrow against your crypto. Great. But where do you actually do it?

Don't just google the cheapest rates, sign up for the first platform you see, and hope for the best. The place you put your collateral matters — a lot.

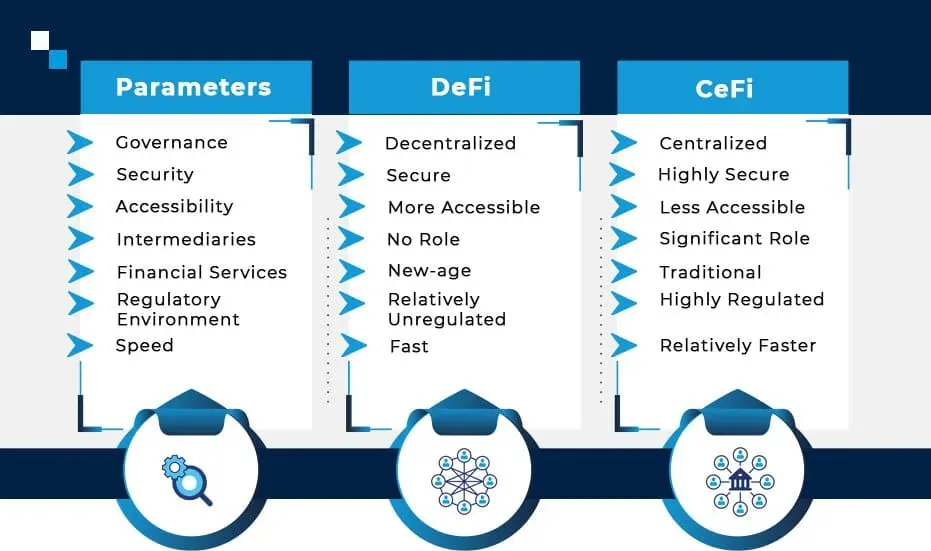

Two main options exist: centralized finance (CeFi) and decentralized finance (DeFi). Both let you borrow against digital assets, but they work very differently under the hood.

Here's what you need to know before choosing.

TL;DR

- CeFi is like a bank for crypto — user-friendly, regulated, customer support. But you hand over custody.

- DeFi is code-only — no middlemen, full control, but no safety net if something breaks.

- CeFi offers 0% APR at low LTV on some platforms. DeFi rates vary wildly.

- DeFi has more risk — smart contract bugs, hacks, no customer support.

- Your choice depends on your risk tolerance and how hands-on you want to be.

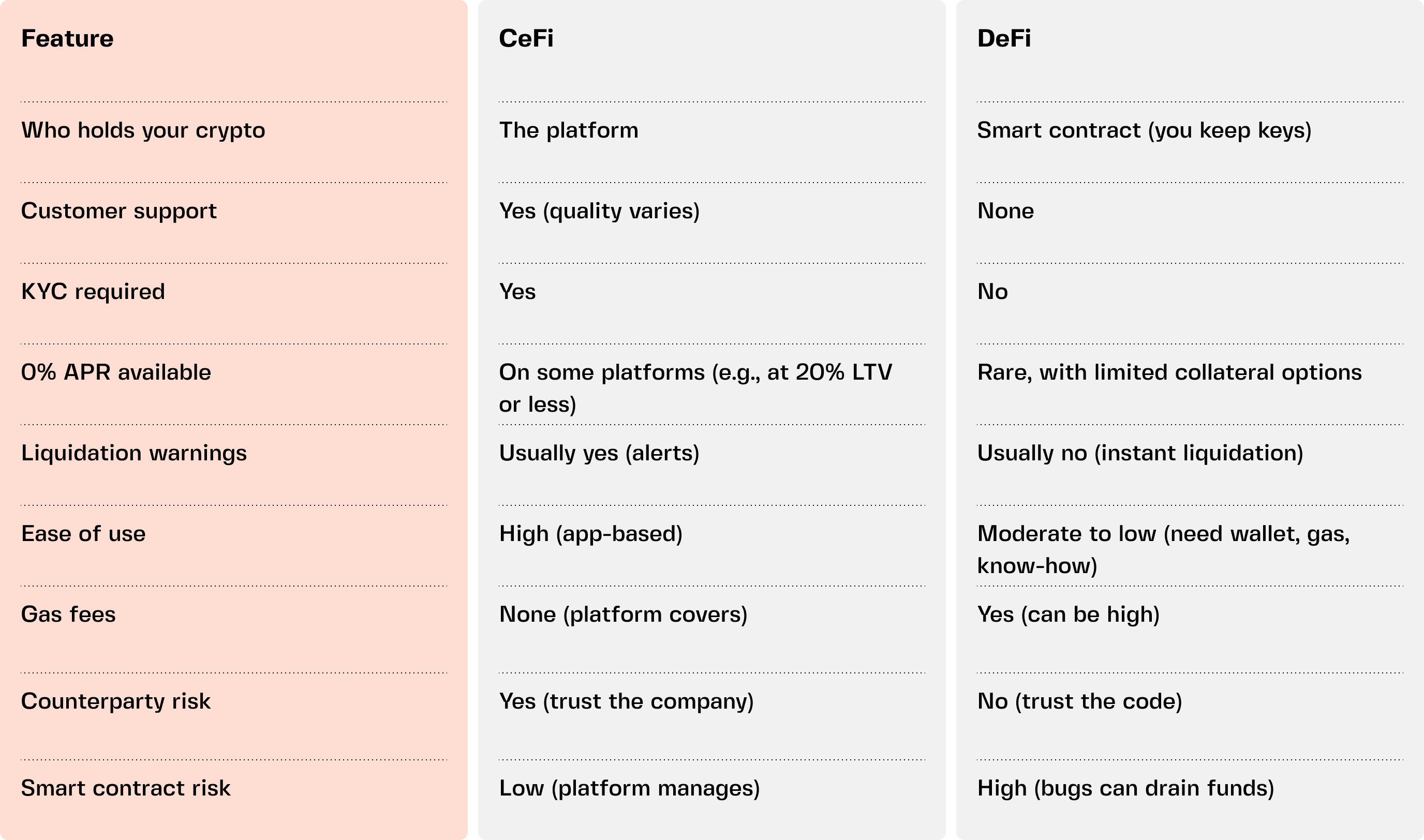

The big difference: Who holds your crypto?

"Not your keys, not your coins." We've all heard it. One cannot borrow without collateral, so be careful where you deposit. This debate still continues: should you choose self-sovereignty over convenience, support, and regulatory compliance?

CeFi (centralized finance): Put simply, you deposit your crypto into a platform's wallet. They hold it, manage it, and lend it out. You trust them to give it back when you repay. Think of it like a bank — with familiar fixed-terms loans and credit lines — but for crypto.

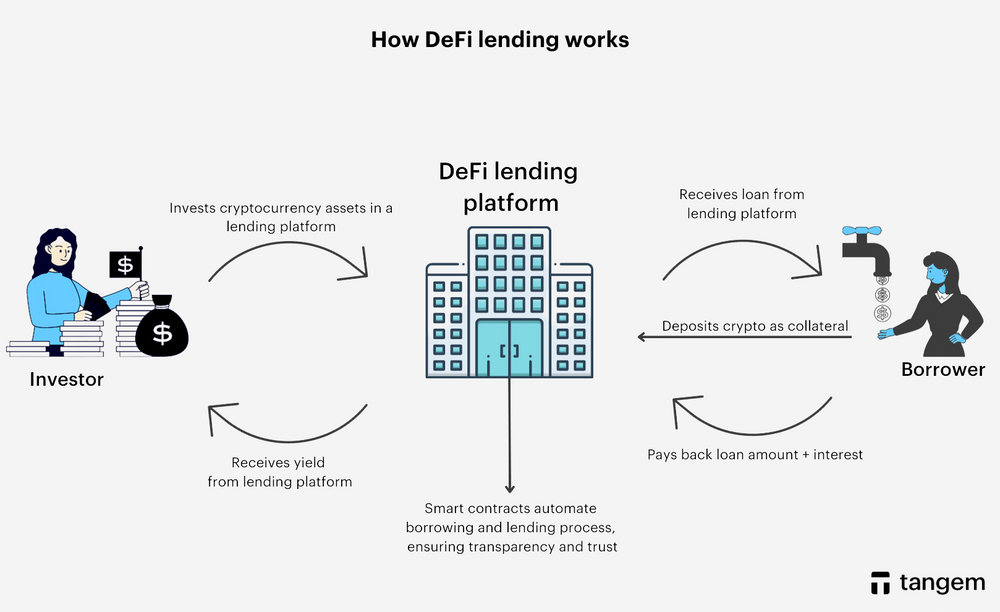

DeFi (decentralized finance): You deposit your crypto into a smart contract — a piece of code running on a blockchain. No company, team, or CEO controls it. No customer support number to call either. The code handles everything: lending, interest, liquidations.

Which to pick? Both work — one requires trust in people; the other requires trust in code.

CeFi: The user-friendly path

CeFi platforms look and feel like normal apps. You sign up, verify your identity, deposit crypto, and borrow. Customer support exists (quality varies). Interest rates are clear. The interface doesn't assume you're a developer.

Pros of CeFi

- Easy to use. No wallet setup, no gas fees, short learning curve (if any), combined with easier fiat-to-crypto onboarding. Platforms are often designed like traditional banking applications.

- Customer support. Someone to complain to when things go wrong — over email, live chat, or phone, depending on the provider.

- 0% APR options. Some platforms reward low-LTV borrowers with zero interest.

- Regulated in some jurisdictions. Not insured like a bank, but licensed. In case of a failure or dispute, there are established legal paths for enforcement and recovery.

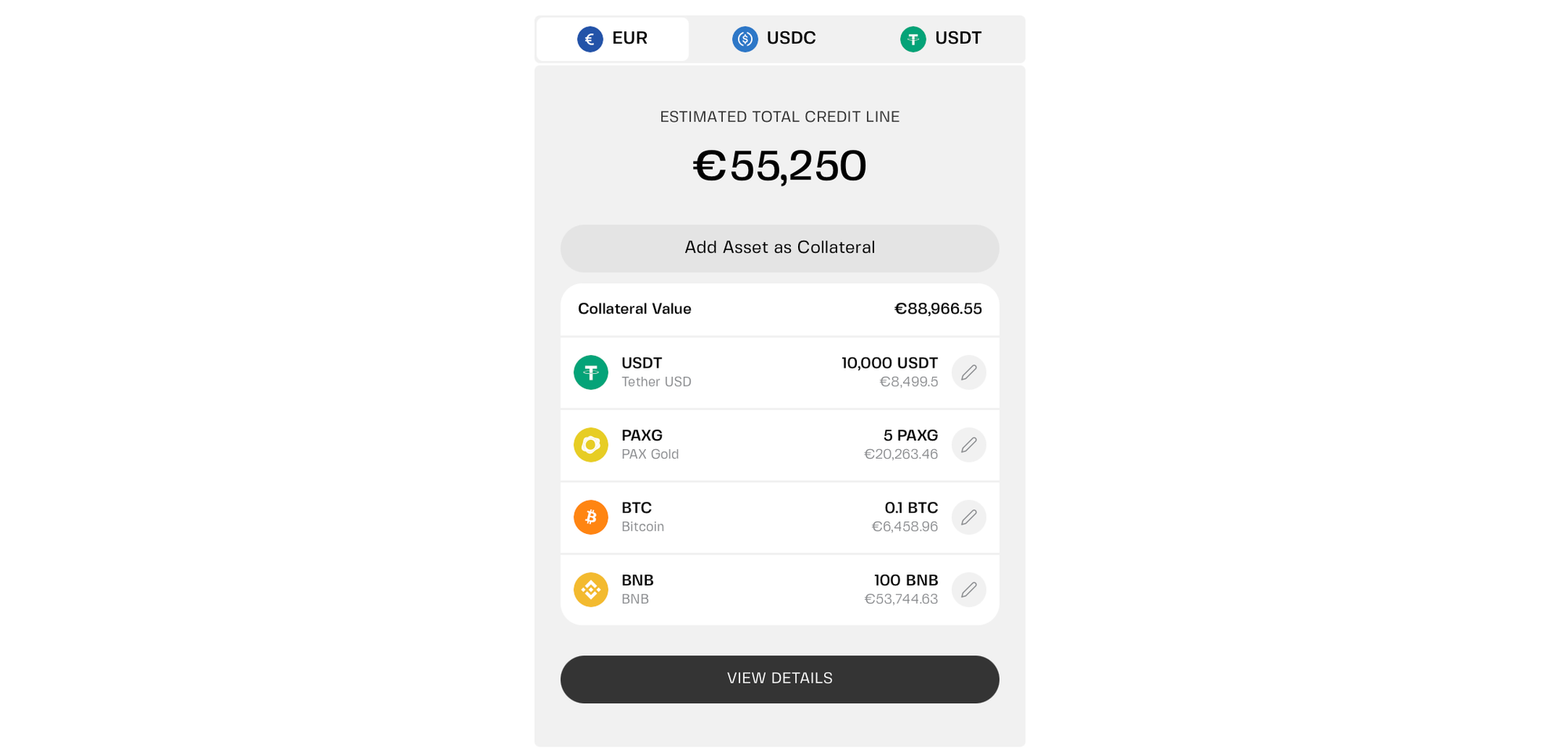

- Multi-collateral flexibility. Some CeFi platforms let you mix BTC, ETH, stablecoins, even fiat. You may also be allowed to swap collateral after borrowing.

Cons of CeFi

- You don't hold your keys. The provider controls your crypto. When you pledge crypto for a loan or credit line, you send it to a wallet managed by the platform — which essentially makes it an "IOU" from the lender.

- Counterparty risk. You're trusting a company and its security safeguards, so choose regulated platforms with multi-layered protections meeting global infrastructure standards.

- KYC required. They know who you are. This goes against crypto's original "cypherpunk" ethos, but also helps fight fraud, and verification could take minutes. Besides, borrowing does not trigger a tax event unless you fail to avoid liquidation.

- Limited asset support compared to DeFi. You might have to choose from a few dozen major assets, as opposed to hundreds of smaller tokens. Centralized lenders often focus on high-market-cap assets like Bitcoin (BTC) and Ethereum (ETH).

Best for: Beginners, people who want customer support, those borrowing larger amounts. The shift to fully collateralized loans after the 2022 credit implosions has made the CeFi lending space safer; established platfoms also implement layered protections and use trusted custody providers like Fireblocks.

Collateral is often locked — unless you pick more flexible CeFi models that don’t lock you into rigid loan structures. Otherwise, assets usually sit idle once you borrow.

DeFi: The code-is-law path

DeFi borrowing happens entirely on-chain. You connect a wallet like MetaMask, deposit crypto into a protocol like Aave or Compound, and borrow stablecoins. No ID. No waiting for approval. Just code.

Pros of DeFi

- Self-custody. Your crypto stays in your wallet until you deposit it into the smart contract. You control the keys.

- No KYC. Connect a wallet and go. No ID, no verification.

- Wider asset selection. Many DeFi protocols support dozens of tokens (for 0% APR, options are limited).

- Transparent. Everything is on-chain. Anyone can audit the code.

- No company can freeze your funds — unless the protocol has admin keys (some do).

Cons of DeFi

- No customer support. Smart contract bug? You lost funds. Period. No one to call, no guidance or assistance. That's the trade-off for maintaining more control.

- Gas fees. The era of paying hundreds of dollars for a single Ethereum transaction is effectively over — but gas fees may still fluctuate, as seen on Etherscan. On April 18, 2026, they surged roughly 579%, though the dollar difference was only 51 cents.

- Liquidation can be brutal. DeFi protocols don't usually send friendly warnings. If your LTV hits the threshold, you get liquidated instantly — and silently — often with a penalty. Another downside of zero manual oversight.

- Complexity. You need to understand wallets, gas, collateral ratios, and how to interact with dApps. The lack of user-friendly interfaces and the need for understanding blockchain mechanisms create a high barrier to entry.

- Oracle risk. DeFi protocols rely on price feeds to determine collateral's worth. If an oracle fails or gets manipulated, you could be liquidated unfairly. In March 2026, an oracle glitch on Aave triggered $26 million in unfair wstETH liquidations.

- No legal protections. You’re interacting with software. There's no legal contract or clear responsibility if something goes wrong due to a bug, exploit, or design flaw. Some specialized protocols offer insurance coverage for hacks, but this is not a standardized "safety net".

Best for: Experienced users, people who value privacy, those comfortable with risk. The appeal of self-custody, points farming, and airdrop programs helped DeFi capture two-thirds of the lending market in Q3 2025.

What about rates?

CeFi rates are usually predictable. Some platforms offer 0% APR at 20% LTV. Push higher, and rates climb to 6–12%.

DeFi rates vary by protocol, asset, and demand. You might find 2% one week and 8% the next. Flashy yields exist, but they often come with extra risk.

For conservative borrowers, CeFi's 0% APR is hard to beat. For those willing to shop around, DeFi can offer competitive rates — but with more volatility.

But beyond rates, flexibility is becoming just as important, especially for users who don’t want their collateral sitting idle during market moves.

Quick comparison

Which one should you choose?

There's no universal answer. It depends on you.

When to choose CeFi

- You're new to crypto borrowing

- You want customer support

- You prefer a simple app experience

- You like the idea of 0% APR at low LTV

- You're okay with KYC and trusting a company

When to choose DeFi

- You value self-custody and privacy

- You understand wallets and gas fees

- You're comfortable with smart contract risk

- You don't mind managing your own liquidations

- You want access to a wider range of assets

Best of both worlds: Go hybrid

Many people use both.

Keep your main borrowing on CeFi for simplicity and 0% APR. Use DeFi for smaller experiments or niche assets that CeFi doesn't support. Just don't put all your collateral in one basket.

Within CeFi itself, a newer category is emerging — more flexible credit-line models that behave less like rigid loans and more like dynamic portfolios.

Diversify across platforms and understand the risks of each. For time-tested guidelines, check out our guide to balanced crypto portfolios.

Most flexible borrowing: credit lines

Fixed-term loans resemble old-school banking products. Your collateral is locked, and you can't touch it until repayment.

This rigidity is one of the biggest limitations of traditional CeFi lending — especially in volatile markets where timing matters.

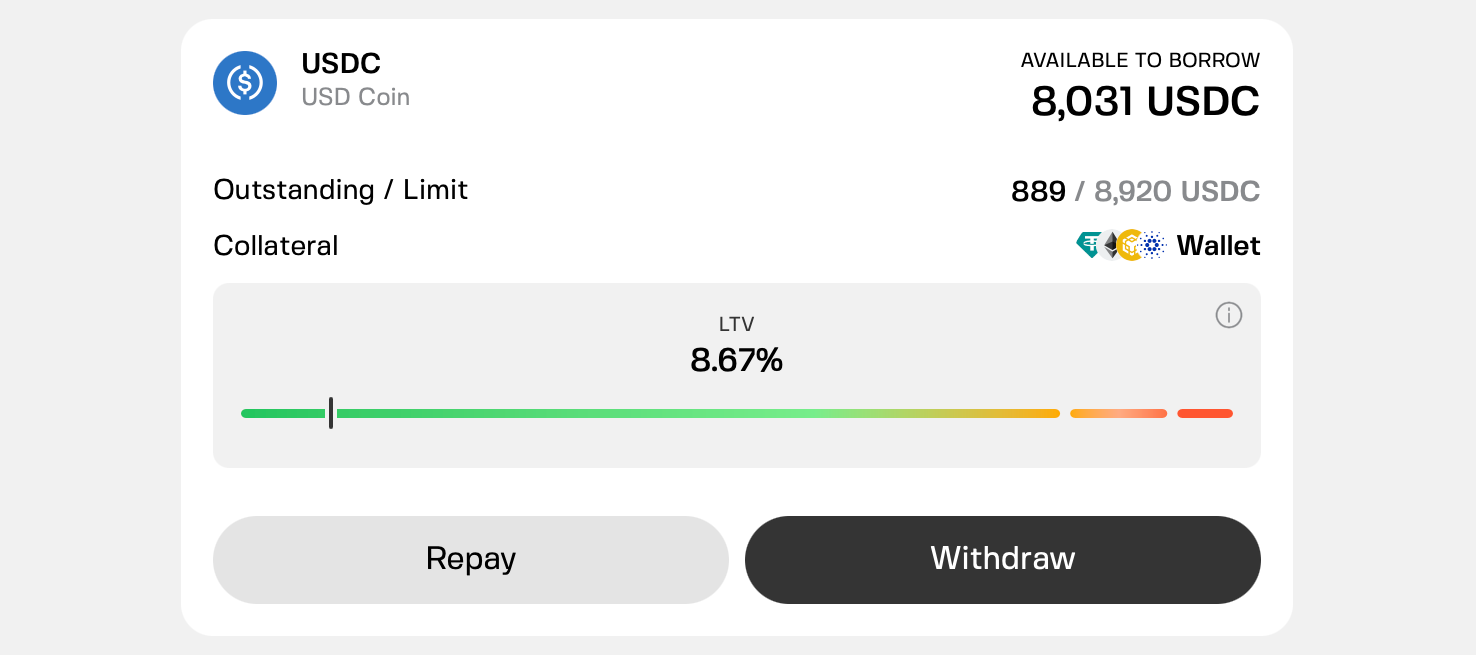

Credit lines offer a different approach. Instead of locking everything upfront, they let you borrow against a pool of collateral while keeping the ability to actively manage it.

Some platforms let you mix BTC, ETH, stablecoins, even fiat — and more advanced setups go further, allowing you to swap collateral without closing your position.

This is where newer credit-line models stand out. For example, Clapp's credit line lets you switch collateral at any time without repaying the loan first. This removes one of the biggest trade-offs in crypto lending: choosing between holding your assets and accessing liquidity.

You also only pay interest on what you actually use — and only if your LTV rises above 20%, with 0% APR below that threshold.

Combined with the ability to draw EUR via SEPA or stablecoins, this makes it closer to a flexible liquidity tool than a traditional loan.

Wrapping up

CeFi and DeFi both let you borrow against your crypto. Neither is objectively better.

CeFi is simpler and more predictable. DeFi gives you control and privacy but requires more expertise.

If you choose CeFi, it’s worth looking beyond basic loan products and considering platforms that offer flexible credit lines — especially if you want to actively manage your collateral instead of locking it away.

Start where you're comfortable. Borrow conservatively. And never put all your collateral in one place.

The best borrowing strategy is the one you actually understand.

Frequently Asked Questions

1. Is my crypto safe on CeFi platforms?

Safer than DeFi for most people — but not immune. CeFi platforms can be hacked or mismanage funds. Choose regulated platforms with transparent custody (e.g., Fireblocks) and segregated accounts. No platform is 100% safe, but CeFi offers more recourse than DeFi.

2. What happens if a DeFi protocol gets hacked?

If the smart contract has a vulnerability, funds can be drained. There's no insurance, no customer support, no "we'll make you whole." That's the risk of DeFi. Some protocols have bug bounties and audits, but nothing is guaranteed.

3. Can I get 0% APR in DeFi?

Rarely. DeFi rates are determined by supply and demand, not promotional tiers. You might find very low rates on stablecoin pairs during quiet markets, but 0% is uncommon. CeFi is a better bet for zero-interest borrowing.

4. Do I need to pay taxes when I borrow crypto?

In most jurisdictions, borrowing is not a taxable event — you haven't sold anything. But interest payments, liquidations, or swapping collateral could trigger taxes. Check local rules or ask a professional.

5. Which is better for a first-time borrower?

CeFi, without question. The learning curve is shallower, customer support exists, and you won't accidentally spend $200 in gas fees. Once you're comfortable, you can experiment with DeFi on the side.

{kind=link}