What if you could borrow money for free?

Borrowing money usually costs something.

Interest rates, origination fees, fine print. Even a "good" bank loan hits you with 6–12% APR. Credit cards charge 20% or more. Traditional lending is costly and often outdated.

Borrowing cash without paying interest sounds like clickbait (and often is). But some crypto lenders make it real. This market hit a record high in 2025 for a reason.

Is there a catch? Yes. Let’s dive into a different way of thinking about borrowing, one that's only possible with crypto.

TL;DR

- 0% APR exists — but you have to borrow responsibly.

- Keep your LTV low (e.g., 20% or below) and pay nothing in interest on some platforms.

- Your crypto stays yours — no sale, no tax event.

- Use a credit line, not a loan — pay interest only on what you use.

- Have a backup plan — markets move, and LTV can change fast.

How free borrowing actually works

Here's the concept. The safer you play it, the less it costs. Borrow conservatively, and your loan or credit line can be effectively free. Borrow aggressively, and you pay like everyone else.

Here are the basics:

You deposit crypto as collateral — say, $50,000 worth of Bitcoin (BTC) or ether (ETH). You then borrow against it. If you keep your loan amount low enough relative to your collateral, certain platforms offer 0% APR tiers (Annual Percentage Rate).

That's it. No hidden fees or "after six months" surprises. Pure zero for being a responsible borrower.

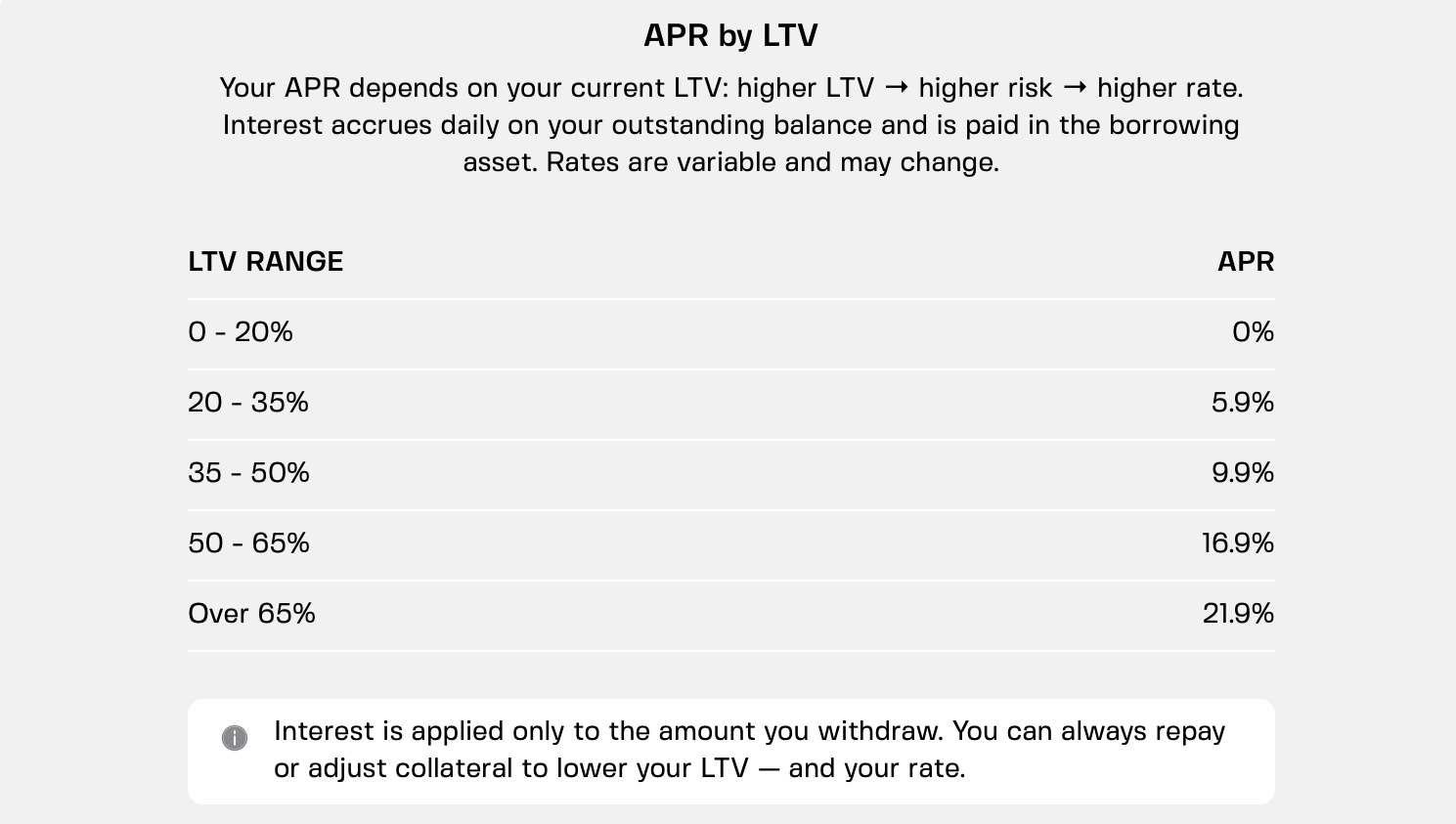

The magic LTV number

LTV stands for Loan-to-Value. It's the ratio of what you borrow to what your collateral is worth.

Borrow $10,000 against $50,000 in ETH? That's 20% LTV.

On platforms that offer 0% APR, that threshold is usually around 20%. Stay at or below that, and you may pay no interest. Push above it, and standard rates kick in.

Example:

Basics of crypto loans

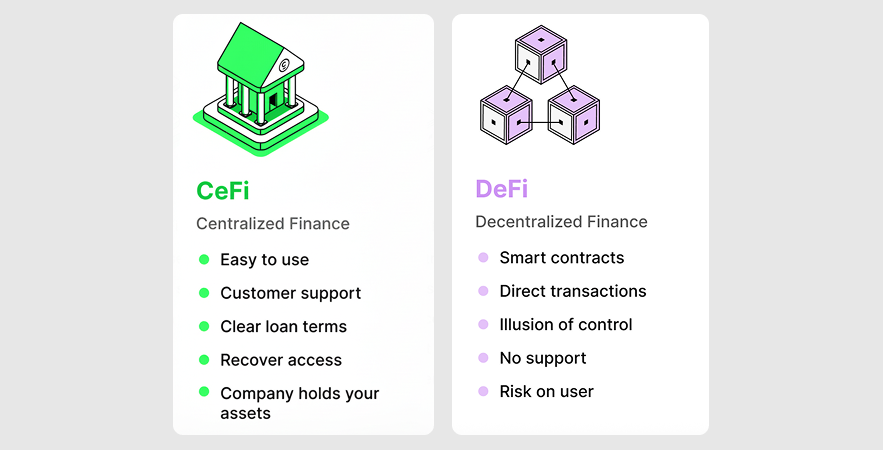

Crypto lending comes in many shapes and sizes, from familiar fixed-term loans on centralized platforms to DeFi's riskiest flash loans. No credit checks either way. Your collateral is the only thing that matters.

This market has come a long way from the earliest lending models of 2017–2018. According to a 2025 report by Galaxy Research, the total crypto lending market reached $73.6 billion in Q3 2025 — up 38.5% from the previous quarter.

Since loans are over-collateralized, lenders can afford to ignore credit history.

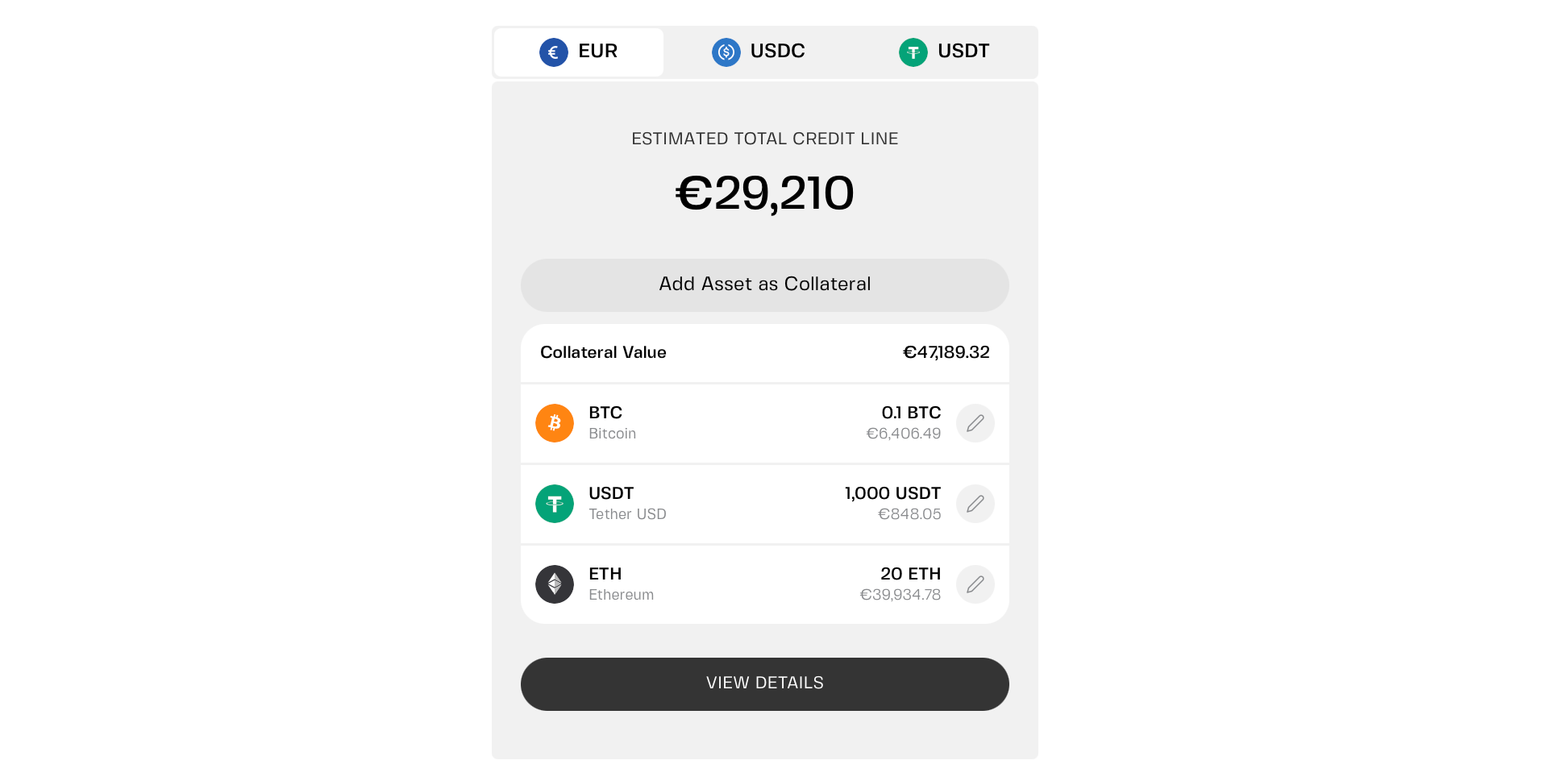

All you need to do is deposit crypto (e.g., BTC, ETH) as collateral into a platform's wallet or smart contract to receive a loan in stablecoins (e.g., USDC) or fiat, typically at a 50%–60% LTV.

Loans that are truly 0% interest exist in both CeFi and DeFi.

The latter introduces unique risks like smart contract vulnerabilities and total loss of funds — making you solely responsible for assessing them. One-time transaction or redemption fees may also apply (e.g., 0.5% flat fee), while collateral ratios may start from over 100% (e.g., 110% or higher).

Why would a platform do this?

That LTV threshold is your lender's protection against high price volatility.

Most borrowers aren't conservative. They borrow more — 50%, 60%, even 70% of their collateral — and pay standard interest rates. That revenue helps subsidize the safe, low-LTV borrowers.

Typically, lending platforms leverage a mix of yield-generation strategies — including DeFi protocols — by reusing deposited collateral. This is known as rehypothecation.

Plus, many centralized finance (CeFi) platforms are integrated exchanges. They generate revenue through transaction fees when users buy, sell, or convert assets in-app.

Why borrowing beats selling

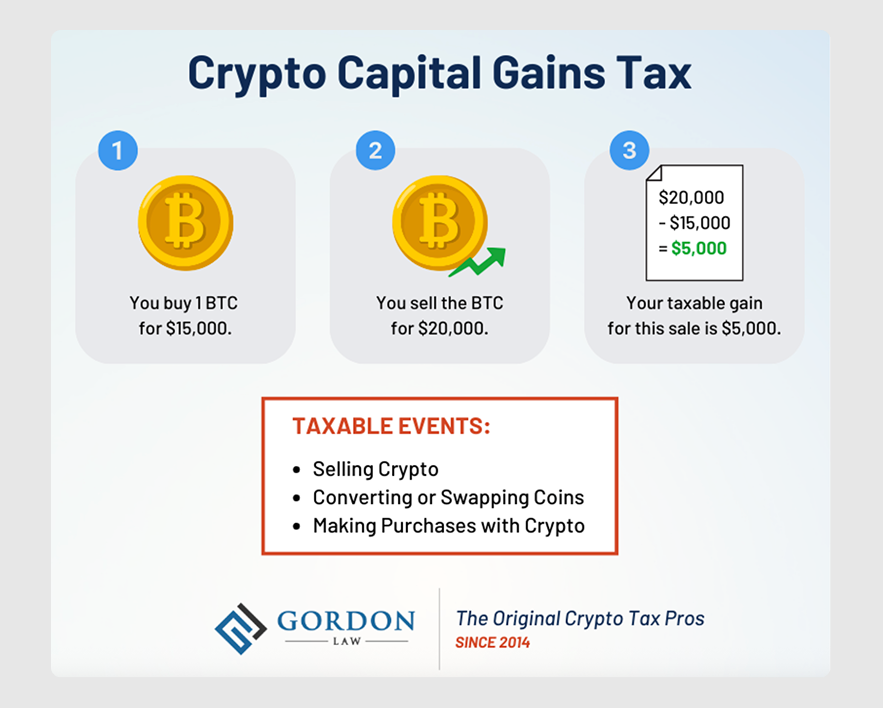

For most people, selling crypto is their first impulse when they need instant cash. That triggers a taxable event in most jurisdictions, from the US to the Netherlands.

It also means you lose your position. If the price rallies next month, you're left out, watching from the sidelines.

It’s no surprise more holders are looking for alternatives — a 2025 survey by GoMining found that 42% of Bitcoin holders want access to liquidity without selling.

Borrowing turns that script on its head. It gives you liquidity without selling, 24/7/365, often with flexible repayment schedules and competitive interest rates.

Whether to pay bills or explore other opportunities, you can keep your crypto while your portfolio strategy remains intact. You may defer taxes, depending on your jurisdiction. You get the cash you need without mind-numbing paperwork.

There's no regret — and if the market rallies, you're still HODLing.

Example:

You need $10,000 for a business opportunity. You have $50,000 in Bitcoin.

- Sell: You trigger capital gains tax. If Bitcoin doubles next year, you missed it.

- Borrow: You may qualify for 0% APR (at ~20% LTV). Your collateral coins stay yours. No sale.

Credit lines vs. loans

Not all borrowing is the same.

- A traditional crypto loan gives you a lump sum with a fixed repayment schedule. Interest begins accruing on the full amount from day one; your collateral is locked until it's paid off. Simple, rigid, predictable.

- A crypto credit line gives you a pre-approved limit. Draw only as much as you need, when you need it — and pay interest only on what you actually use. Repay anytime, then borrow again.

For free borrowing, a credit line makes more sense. You're not forced to borrow a lump sum. You can draw $2,000 today, another $3,000 next week, and pay interest only on what's actually out.

And if you keep LTV low (e.g., 20% or less, depending on the platform)? That interest is zero.

So, what is the downside?

0% doesn’t mean risk-free — you’re not paying with interest, you’re paying with exposure to volatility. Here's what to keep an eye on.

- Crypto doesn't stand still. That 20% LTV assumes your $50,000 in ETH holds steady. But if ETH drops 30% overnight, your collateral shrinks to $35,000. Your LTV climbs to about 22.8% — still safe, but closer to the line. Drop 50% and you're at 40% LTV. Now you're paying interest and may face liquidation risk if it rises further.

- You need a backup plan. Most platforms ping you when LTV gets uncomfortable. Add more collateral. Pay down part of the loan. Ignore the warnings, and the platform may sell some of your crypto to cover itself. No one wants that.

- It's still debt. Free borrowing isn't free money. You borrowed it, so you owe it back. The only difference is you're not bleeding interest as long as you stay within the required thresholds.

A quick example

Suppose you hold $50,000 in BTC. You set up a credit line with a 20% LTV limit — meaning you can borrow up to $10,000 at 0% APR.

You don't need cash right now, but you want the option. The line sits there — always on hand, costing nothing until you actually use it.

Three months later, an opportunity appears. You need $8,000. You draw it from your credit line. Your total borrowing stays under 20% of your collateral, so the cost is zero.

Six months after that, you repay the $8,000 from your business earnings. Your credit line resets. If your LTV stayed below the threshold the entire time, you paid nothing in interest.

That's free borrowing.

But markets move — here's how you stay safe

That 20% LTV assumes your $50,000 in ETH holds steady. But what if it drops 30% overnight? Your collateral shrinks to $35,000. Your LTV climbs to about 23% — still under 20%? Actually, $8,000 borrowed against $35,000 is 22.8%. Still safe, but creeping up.

If ether drops 50%, your collateral is $25,000. Now your $8,000 loan is 32% LTV — and you're paying interest.

This is where multi-collateral flexibility changes the game.

On most platforms, you're stuck with whatever you pledged.

- If LTV climbs too high, your only option is to add more of the same asset.

- Withdrawing collateral usually means paying off the entire loan first.

- Partial withdrawals might be possible for "excess collateral" when markets move in your favor.

On Clapp, you can reshuffle your collateral pool even after borrowing. BTC, ETH, stablecoins, even fiat — mix and match up to 25 assets. That means you're not locked into a single asset's performance.

BTC sliding? Add some USDC to bring your LTV back down. Too much ETH exposure? Swap it for BTC without closing your line. Adapt as the markets move.

Keep total borrowing low enough relative to total collateral so you never cross that LTV threshold. A flexible collateral pool gives you more ways to make that happen.

The bottom line

0% APR crypto borrowing is real. In specific cases, these loans and credit lines reward conservative borrowing — the kind where you leave plenty of buffer between your debt and your collateral.

With a bit of discipline, you can keep your crypto while potentially avoiding taxes and paying nothing in interest.

The catch is to borrow responsibly. Stay under 20% LTV, have a backup plan for market drops, and actually pay the loan back. Do that, and you've discovered something most people miss: a way to borrow money at effectively zero cost under the right conditions.

Frequently asked questions

1. Is 0% APR really free? No hidden fees?

On some platforms that offer it, yes — as long as you keep LTV at or below the threshold (usually 20%). Always read the fine print, but the model is legitimate.

2. What happens if the Bitcoin in my collateral drops 30%?

Your LTV climbs. You might go from 20% to 28% — still safe. But if it drops 50%, you could hit 40% LTV and start paying interest. Most platforms send alerts well before that happens. You can add more collateral or pay down part of the loan to bring LTV back down.

3. Can I lose my crypto?

Only if you ignore the warnings. If your LTV climbs too high (say, 70–80%) and you do nothing, the platform may liquidate some of your collateral to protect itself. Stay on top of it, and you're fine. Borrow conservatively, and you'll never get close.

4. How is this different from a bank loan?

Banks check your credit, income, employment history. Crypto credit lines check your collateral. That's it. No paperwork, no waiting, no "we'll get back to you in 7–10 business days." Just deposit, borrow, and access funds within minutes or even seconds.

5. Can I use the borrowed money for anything?

Yes. There's no restriction. Business opportunity? Go for it. Emergency expense? Covered. Another investment? Your call. Just remember — you have to pay it back eventually. Borrow responsibly.

{kind=link}