Is crypto a bubble? Here's what's really going on

People have been calling crypto a bubble since Bitcoin traded for pocket change. Over a dozen years later, it's still here. That doesn't mean implosions don't happen — but labeling the entire asset class as a one-off mania misses the point.

Before you panic at the next dip, let's walk through how financial bubbles actually work and where crypto fits in.

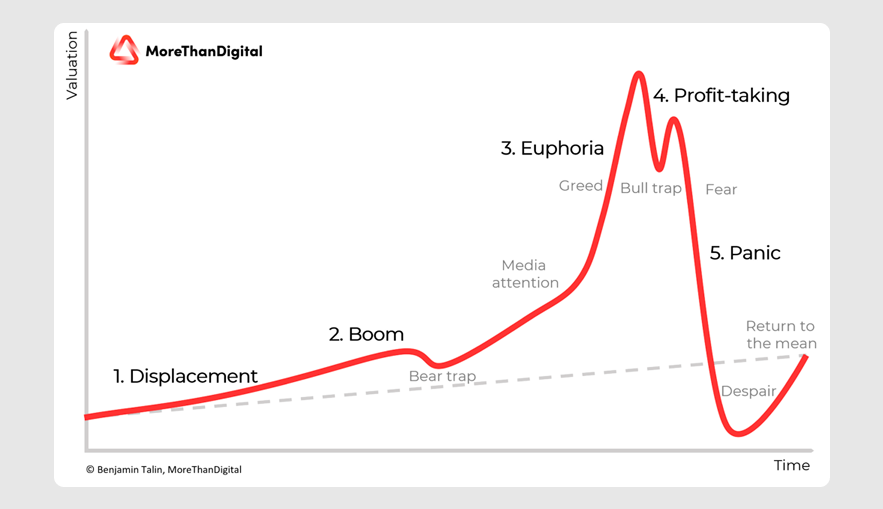

Anatomy of a financial bubble

Financial bubbles don't just happen overnight — they build, then burst. First, an asset's price soars beyond its real value, fueled by speculation and herd mentality as hype drowns out fundamentals. Sooner or later, confidence cracks. Prices collapse. Investors get crushed.

A typical bubble plays out in five stages.

#1 Displacement: The spark that starts the fire

A fresh, promising innovation or paradigm grabs investors' attention — from technological breakthroughs to policy shifts to new financial tools. Even lower interest rates can qualify as a trigger — Fed rates falling from 6.50% to 1.20% between mid-2000 and mid-2003 laid the groundwork for the housing bubble.

#2 Boom: When FOMO meets easy money

As investors pile into the new market darlings, prices start climbing and gain steam. Increased media coverage, often paired with easy credit access, fuels more buying pressure. Asset prices begin to outpace their underlying value, but most participants still think their optimism is justified.

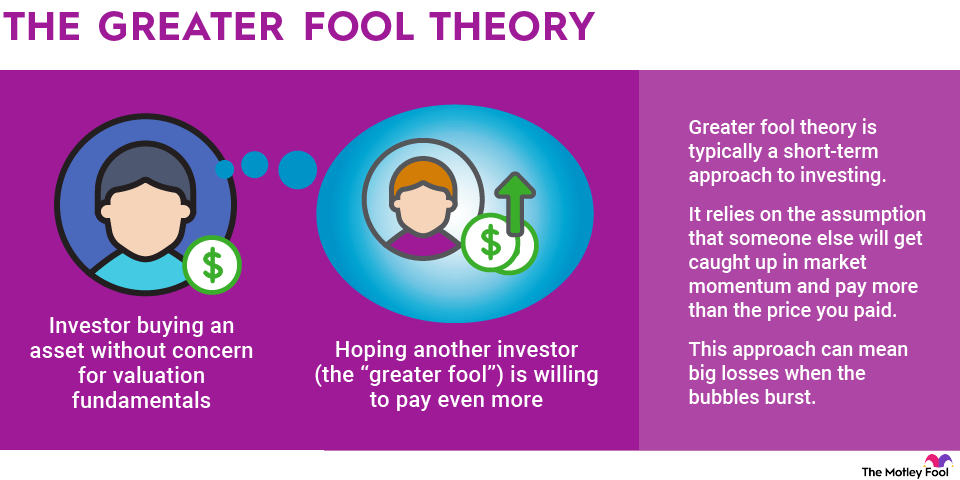

#3 Euphoria: The 'greater fool' takes the wheel

As optimism hits its peak, valuations go parabolic while investors bet the bull market will never end. The fear of missing out drowns out any caution as fresh and inexperienced participants flood in.

That's when the "greater fool" theory kicks in — the belief that wherever the price moves, there will always be someone else willing to buy. Prices completely detach from reality, but experts' warnings get ignored.

At the peak of the dot-com bubble in March 2000, all tech stocks on the Nasdaq were collectively valued above the GDP of most nations. Over a decade earlier, during the Japanese real estate bubble, Tokyo prime office space sold for a staggering $139,000 per square foot.

#4 Profit taking: Smart money heads for the exits

Seasoned, savvy participants start smelling a reversal, so they begin cashing out to lock in gains. Momentum starts to fade and volatility heats up, yet the rest of the crowd seems unbothered.

Nobody can predict the exact moment that will pop the bubble. "The markets can stay irrational longer than you can stay solvent," as John Maynard Keynes put it.

Take the 2008 financial crisis, triggered by the American subprime mortgage crisis. In 2007, French Bank BNP Paribas paused withdrawals from three investment funds exposed to those mortgages because it couldn't value their holdings. The markets got rattled, but only for a couple of months before global stock markets hit new highs.

#5 Panic: The stampede nobody can stop

Once the bubble pops, it cannot inflate again. Prices tumble as sharply as they had soared, and confidence evaporates. The remaining participants scramble to sell, this time driven by fear of even deeper losses. Faced with margin calls and dwindling holdings, they will liquidate at any price.

Amid drying liquidity, prices keep falling, and the bubble eventually implodes. The meltdown can send shockwaves through the broader economy — from financial stress all the way to recession.

Panic swept the market in October 2008, shortly after the bankruptcy of Lehman Brothers and the near-collapse of Fannie Mae, Freddie Mac, and AIG. The S&P 500 lost nearly 17% in a single month.

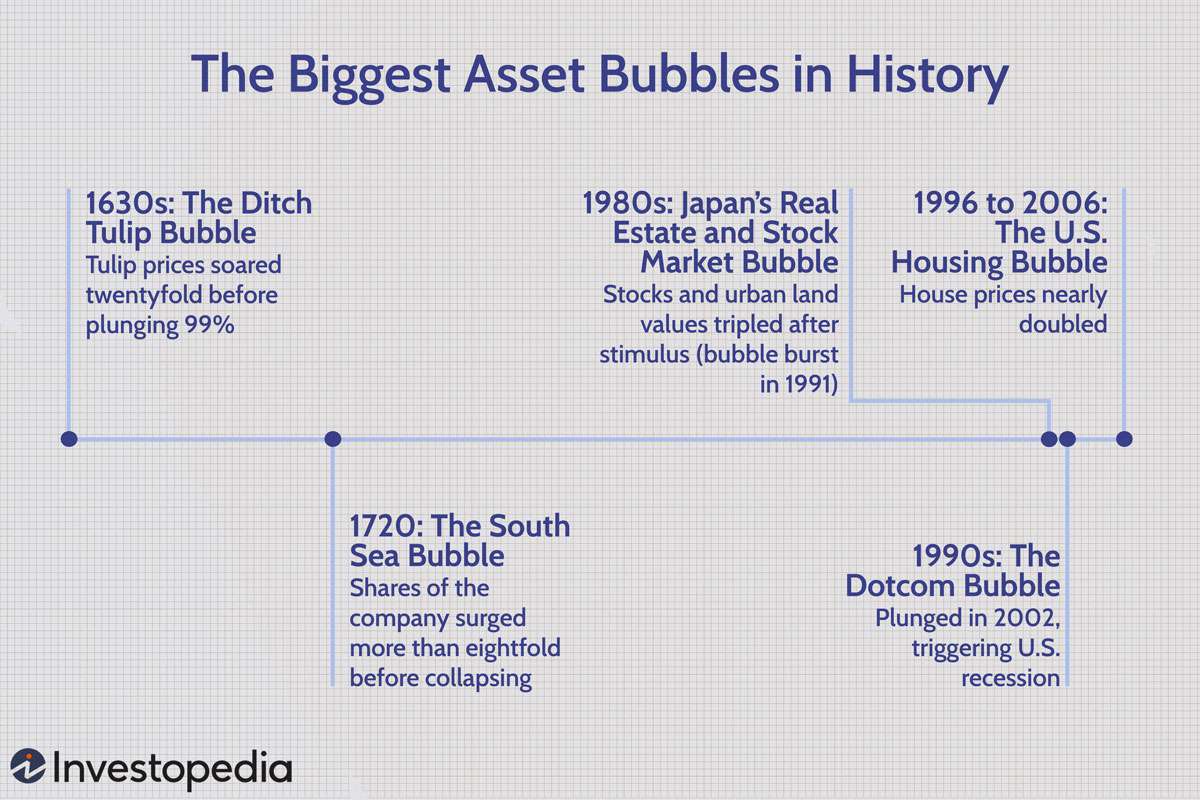

Top 5 bubbles in history

1630s: Tulipmania in Holland

During the Dutch Golden Age, tulips — recently introduced to the country — became so fashionable that contract prices for bulbs went parabolic. The speculative bubble ignited in 1634 and burst suddenly in 1637.

Unlike the bubbles that followed, this was more of a cultural phenomenon than an actual financial crisis — the Dutch Republic's prosperity remained largely intact. But since then, "tulip mania" has become shorthand for any economic bubble where prices detach from intrinsic value.

1720: Britain's South Sea bubble

This one has been called the first financial crash — and the first Ponzi scheme in history. Unlike tulip mania, it wrecked massive economic havoc.

The South Sea Company, a British joint-stock entity, won a trading monopoly — including the right to trade enslaved Africans to Spain and Portugal. Since the slave trade had been profitable for centuries, investors expected success similar to the East India Company.

But the trade explosion never came as Spain tightened trade restrictions. Then King George took over the company in 1718, which inflated the stock price further. Unable to deliver the promised profits, the company ended up trading its own stock — with staff pumping it up and even bribing friends to buy in.

In 1720, disaster struck. Stocks crashed 80% from their peak. Investors were ruined. A wave of suicides followed.

1980s: Japan's economic bubble

In the early 1980s, the Japanese yen soared by a staggering 50%, which triggered a recession in 1986. To halt the slowdown, the government rolled out a program of monetary and fiscal stimulus. It worked so well that it sparked rampant speculation.

Between 1985 and 1989, both Japanese stocks and urban real estate values tripled. At the peak, the Imperial Palace grounds in Tokyo were valued higher than the entire real estate of California. The crash in 1991 ushered in Japan's "Lost Decade" — a stretch of deflation and economic stagnation.

1990s: Dot-com bubble

The explosive popularity of the internet sparked a massive wave of speculation in so-called "new economy" companies. Hundreds of businesses went public with multi-billion dollar valuations.

The tech-heavy NASDAQ Composite index climbed from roughly $750 at the start of the decade to over 5,000 in March 2000. By October 2002, it had plunged 78%, sparking a US recession. It took the index over 15 years to hit a new high again.

While many companies disappeared, others — like Amazon and Google — went on to define the next era of the internet.

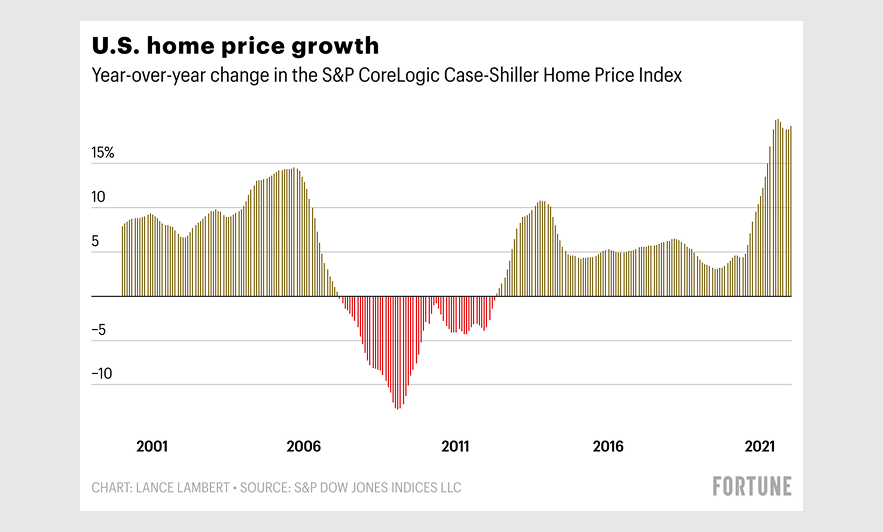

2006–2013: US housing bubble

Spooked by the dot-com meltdown, US investors turned their sights to real estate, convinced it was safer. House prices rose at a record pace, doubling from 1996 to 2006 — with two-thirds of that gain happening in the final three years.

Meanwhile, mortgage fraud ran rampant, subprime borrowers bought houses they couldn't afford, and condos were "flipped" — investors snapped up undervalued units, renovated them quickly, and resold for a profit.

After prices peaked in 2006, the average US house lost one-third of its value by 2009. The ripple effects through mortgage-backed securities triggered the Great Recession — the deepest economic contraction since the 1930s Depression.

How does this apply to crypto?

The parallels are hard to ignore. Crypto's boom-and-bust cycles mirror bubble theory in more than a few ways.

That said, there are also crucial differences that make a string of smaller bubbles more likely than the classic blow-up — a single, terminal collapse.

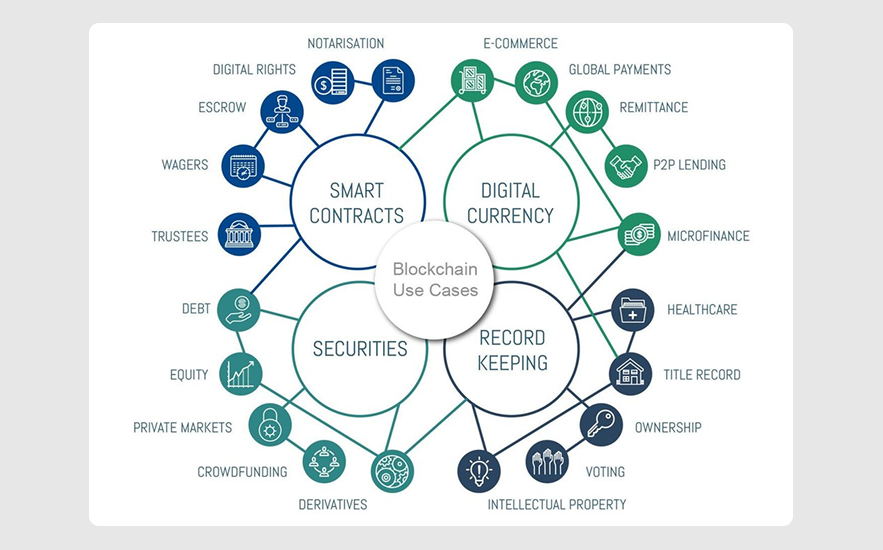

Crypto's real-world muscle

Skeptics question the tangible value of digital assets, pointing out that gold and silver have been around for centuries. But blockchain technology already powers a wide range of live use cases:

- Cross-border payments: fast, low-cost international transfers and remittances — a lifeline for emerging economies and countries battling high inflation.

- Tokenization of real-world assets: from art and commodities to property, fractional ownership makes trading faster, more liquid, and more efficient. Property deals close faster, leases run on autopilot.

- Supply chain management: businesses tap blockchain to track shipping and logistics, cutting fraud and adding transparency from factory to doorstep.

- Identity and security: distributed ledgers can securely store personal IDs and medical records.

- Intellectual property: blockchain handles IP rights and automates royalty payouts via smart contracts — think platforms like Mediachain.

Example: Dubai's paperless future

The Dubai government is a global leader in adopting blockchain tech. Its goal: a fully paperless, highly efficient, digital-first economy. That means everything from visa applications to bill payments to license renewals moves on-chain.

Its Dubai Blockchain Strategy aims to run all eligible government transactions on-chain — saving millions of productive hours and boosting government efficiency.

Bottom line: cross-border payments, smart contracts, tokenized assets, digital identity — the use cases are real and multiplying.

So beyond the price charts, crypto markets are also driven by fundamentals. Assets built on blockchain technology — not just hype — tend to hold up better over time.

Where the bubble signs show up

That said, not all cryptocurrencies run on strong fundamentals. Tokens driven purely by speculation shoot up and crash just as fast — creating localized "mini-bubbles" within a broader market that is still evolving and maturing thanks to underlying growth. These days, meme coins fit squarely into this bucket, alongside some NFTs and gaming tokens.

Case in point — NFT bubble (2021-2022)

The NFT market went parabolic in 2021, but valuations largely crashed by late 2022. Researchers from The Centre for Economic Policy Research (CEPR) suggest the downturn may have appeared later than expected because of the "disposition effect" — investors holding losing assets while selling winners.

This behavior distorted visible returns, making the market look healthier than it actually was.

Take SuperRare. According to CEPR, between 2018 and 2024, nearly 97,000 NFTs were minted there. The median realized return on resold items was $170 in dollar terms — yet only 6.2% of all NFTs were ever resold. That's a textbook case of selection bias.

Shifting regulation: From Wild West to guardrails

Since Bitcoin's launch in 2009, the market has gone from Wild West to a playing field where the world's biggest asset managers now compete. Regulation has been a driving force behind that shift.

By March 2026, US spot Bitcoin ETFs held roughly $90 billion in net assets — about 6.4% of Bitcoin's entire market cap — with cumulative inflows since launch topping $56 billion. BlackRock's IBIT alone now manages over $60 billion, commanding nearly 60% of the category.

Take MiCA in the EU, the GENIUS Act in the US, and the recent crypto classification from the SEC and CFTC. Together, they've delivered the clarity that boosts investor confidence and accelerates market maturation.

DeFi is still largely uncharted territory. But centralized providers? They stick to strict AML and KYC rules depending on local laws. Does that kill fraud? No. But the legal landscape is far more organized and transparent than it used to be.

With the GENIUS Act now set to clear the remaining legislative hurdles, the industry has been officially brought into the global financial fold. The US government has even set up a Bitcoin strategic reserve after Trump took office again in 2025.

This does not eliminate fraud or systemic risk — as seen in high-profile failures like FTX — but it does mark a shift toward greater oversight compared to earlier cycles.

Crypto crashes aren't like bubble bursts

When the dot-com bubble popped in 2000, Pets.com and Webvan never came back. However, the broader sector eventually recovered in a more mature and sustainable form.

Bitcoin has now weathered four major bear markets — in 2011, 2015, 2018, and 2022 — and each time, it has eventually climbed to new all-time highs.

- The pattern is driven by real mechanics. Halvings cut mining rewards roughly every four years, reducing new supply. Historically, these events have preceded bull markets, though they're not a guaranteed trigger.

- Monetary policy also plays a role. Crypto has tended to rally when the Fed cuts rates or injects liquidity, as seen during the 2020-2021 stimulus-fueled run.

- Investor psychology completes the loop. Optimism and greed drive prices to euphoric tops. Panic and fear send them crashing. But unlike a one-off bubble, the cycle resets.

- Adoption keeps building through the noise — institutions, ETPs, and regulatory frameworks have taken root even during downturns.

None of this guarantees the next rally. But history suggests writing off crypto after a downturn is usually the wrong move — here is our overview of top 10 Bitcoin crashes and rebounds.

Bottom line

Tulips, dot-coms, housing went bust and never came back in the same form — but in many cases, the underlying sectors continued to evolve long after the speculative excess faded. Crypto has crashed four times. And every time, it's climbed to new highs.

That doesn't rule out the possibility of a larger-scale bubble. Speculative assets with little utility will continue to rise and fall quickly. But the broader ecosystem has so far shown resilience through multiple cycles.

The key question isn’t whether crypto will crash again — it likely will — but whether the underlying networks continue to gain adoption, utility, and relevance over time.

{kind=link}