Borrowing without credit checks — how crypto lending works

Credit scores can be frustrating. If you've never borrowed before, building credit takes time. And if you've missed payments in the past, repairing your score can take months or even years.

So what happens if you need cash, but your credit profile doesn't meet a lender's requirements?

In traditional finance, that's often where the conversation ends. No credit score, no loan.

But in crypto, it works differently. Lenders only look at the assets you're willing to pledge as collateral. Your income and employment history are irrelevant.

What matters is what you own.

Let's look at how borrowing against crypto compares to the alternatives — and why skipping the credit check is only part of the story.

TL;DR

- Crypto loans don't check your credit. Your collateral is all that matters. No FICO score, no income verification, no employment history.

- Traditional alternatives exist — payday loans, cash advance apps, secured loans — but they come with high fees, low limits, or strict terms.

- Crypto loans are over-collateralized. You borrow less than you pledge. That's the trade-off for no credit checks.

- The barrier is assets, not credit history. If you hold crypto, you can borrow. Period.

- Rates can be lower than unsecured loans. Because your loan is secured by collateral, lenders can offer competitive terms — sometimes even 0% APR at low LTV.

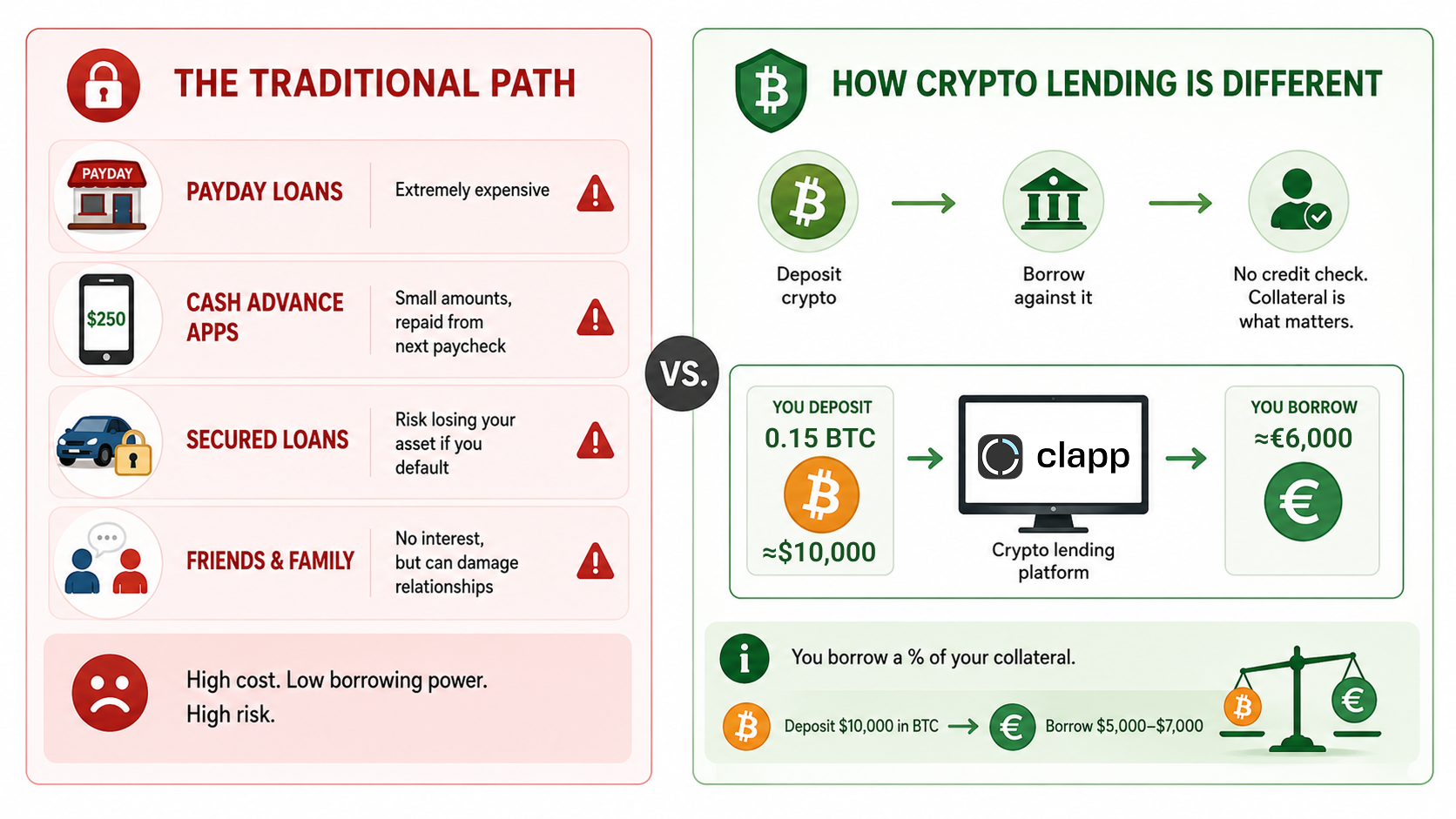

The traditional path (and why it's limited)

If you need cash and don't have great credit, your options are limited. None of them give meaningful borrowing power without taking on significant risk.

- Payday loans (expensive). Fast cash, predatory APRs of 400% or higher. The fees alone can trap you in a cycle of debt. What starts as a $500 emergency can turn into thousands in interest.

- Cash advance apps (modest amounts). Some apps advance you money based on your direct deposits. But the amounts are small — usually $25 to $750 — and they take repayment from your next paycheck. Fine for a quick fix, but not real borrowing.

- Secured loans (risk of collateral loss). You pledge an asset like a car or savings account as collateral. The lender doesn't check your credit because the asset guarantees the loan. But if you default, you lose the asset. Your car, your savings, your safety net — gone.

- Friends and family (emotional baggage risk). No interest, but personal relationships can sour when money is involved.

How crypto lending is different

Crypto lending skips the credit check entirely.

You deposit crypto as collateral. The platform lets you borrow against it — without pulling your credit score, requiring income verification, or checking employment history.

Your collateral is all that matters.

The trade-off is that you can only borrow a percentage of what you deposit. That's called over-collateralization. If you deposit $10,000 in Bitcoin, you might borrow $5,000 or $7,000 — not the full amount.

Because cryptocurrencies are volatile, this buffer protects the lender. If the market drops, there's still enough collateral backing the loan.

On the upside, your crypto does the talking. You can borrow without a credit check, paperwork, or long approval times.

On the downside, you need to have that crypto in the first place. If you don't hold digital assets, this isn't an option. But if you do, it's one of the fastest ways to access cash without selling.

Who benefits most from this model

- Long-term holders. You believe in crypto for the long term, but you need cash now. Borrowing lets you keep your position while accessing liquidity. In addition, unlike selling, it does not trigger a taxable event in most jurisdictions.

- Speed-focused borrowers. No paperwork, no waiting for approval. Deposit collateral, borrow funds — often within minutes.

- Crypto users with limited credit history. Young investors, immigrants, or anyone who hasn't built a traditional credit score can still borrow.

- Privacy-conscious borrowers. Not everyone wants their credit pulled. Crypto lending offers an alternative.

The real trade-off

No credit check doesn't mean no risk.

You still have to repay the loan. If you don't, the platform liquidates your collateral. You don't lose your credit score, but you lose your crypto.

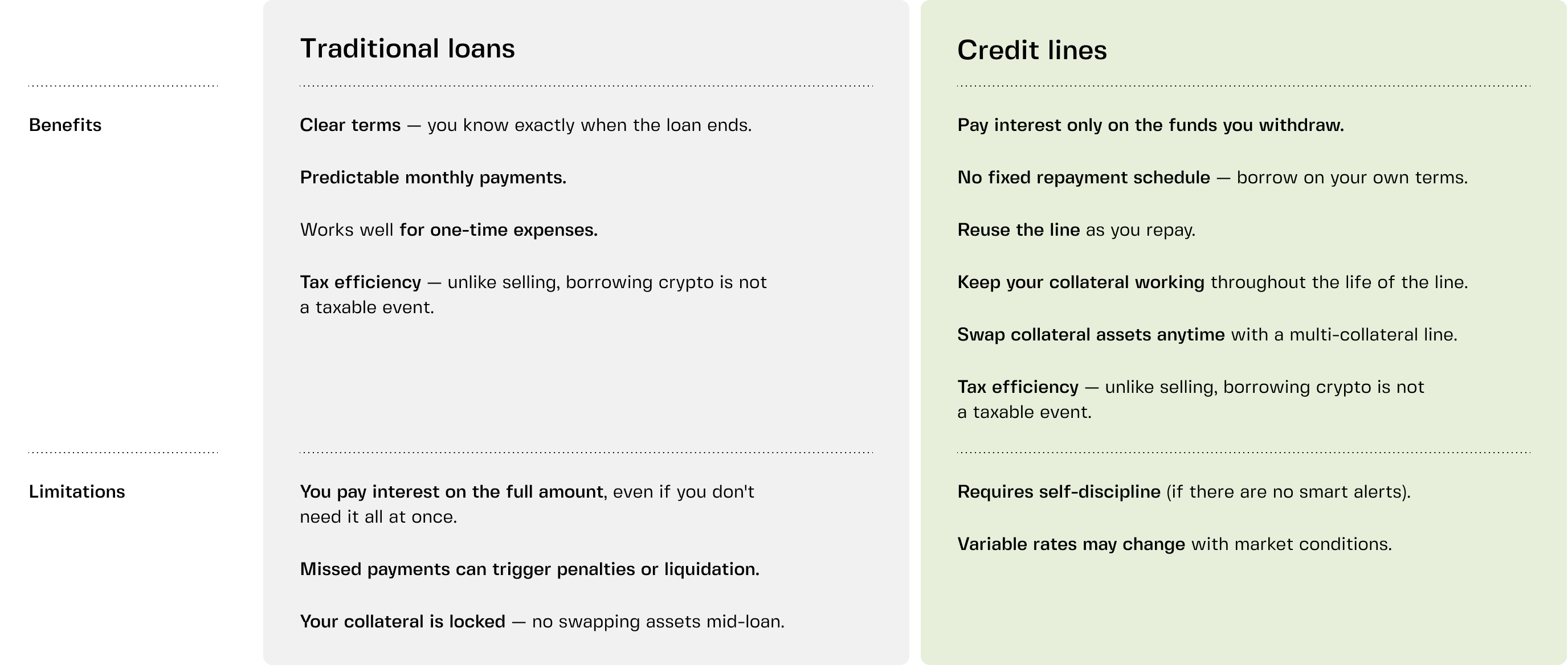

Some products offer more flexibility than others. Fixed-term loans resemble traditional fiat loans — there's a repayment schedule and penalties for paying late. Credit lines work differently — they remain available as long as your collateral supports the position.

LTV still matters. Borrow at 20% LTV and you're relatively safe. Borrow at 60% LTV and a sharp market decline could put your collateral at risk. No credit check doesn't mean no responsibility.

Platform and smart contract risks exist. Your collateral is locked in a smart contract (in DeFi) or held by a lending platform (in CeFi). DeFi remains largely unregulated, so there’s no customer support, no intermediary, and no meaningful consumer protections if something goes wrong. In CeFi, look for regulated lenders that use qualified custodians and multiple layers of account security.

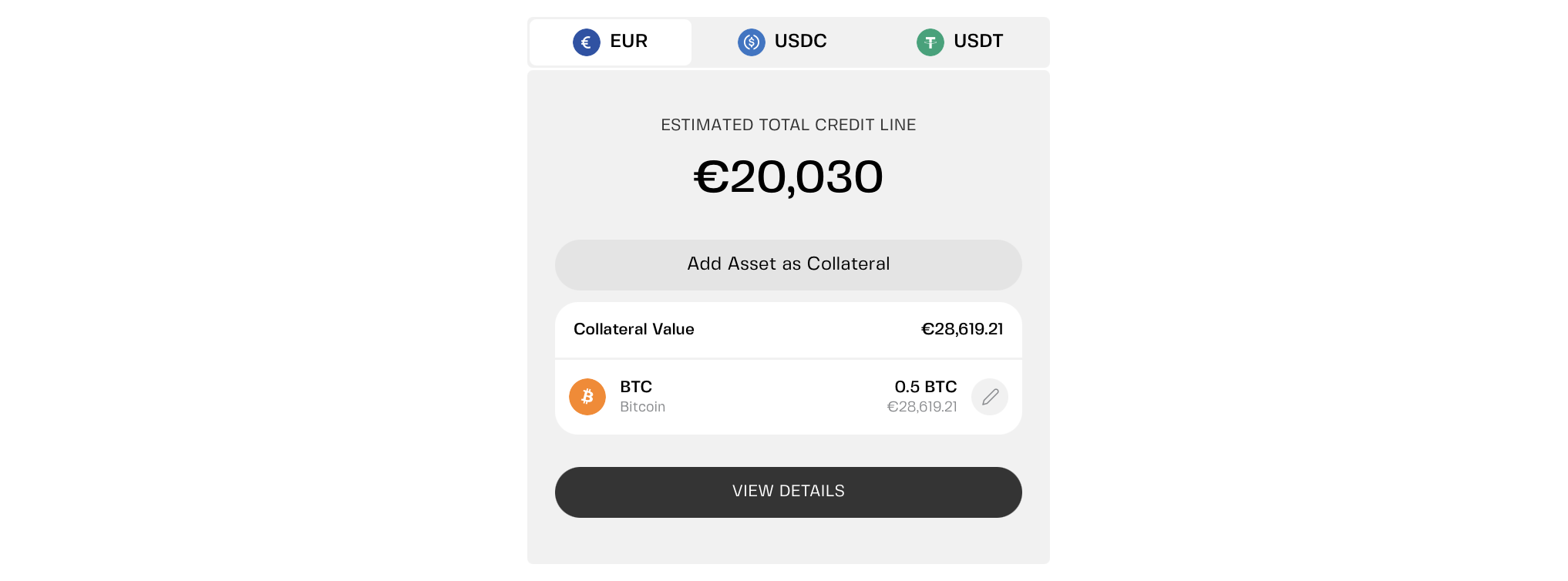

How credit lines add flexibility

Credit lines offer the same no-credit-check access, but with a borrowing limit instead of a one-time loan.

- Draw what you need.

- Pay interest only on what you use.

- Repay anytime.

- Your available credit replenishes as you repay.

On some platforms, keeping your LTV at or below a certain threshold can reduce borrowing costs significantly. On Clapp, for example, APR drops to 0% at 20% LTV.

Some lenders also let you mix multiple assets in your collateral pool — for instance, BTC, ETH, stablecoins, and fiat. Your borrowing power is based on the total value. With Clapp, you can even add, remove, or swap collateral assets without closing your credit line.

To sum up

Borrowing without a credit check is one of the most attractive features of crypto lending.

No FICO score or income verification. Just your crypto.

That said, it's not free money. You borrow less than you pledge. You're exposed to market volatility. And if you don't manage your LTV, you risk losing your collateral.

For people who hold crypto and need liquidity, it's a powerful option. Just borrow conservatively and keep an eye on your LTV.

Frequently asked questions

1. Do crypto lenders check my credit?

No. Crypto-backed loans don't rely on credit scores, income verification, or employment history. Your collateral is what matters.

2. Can I borrow if I have bad credit?

Yes. Crypto loans don't check credit. If you have crypto to deposit as collateral, you can borrow — regardless of your credit score.

3. How much can I borrow?

It depends on your collateral's value and the platform's LTV limit. Typically up to 50–70% of your collateral's value. Some platforms allow higher LTV ratios for stablecoins.

4. What happens if I can't repay?

You don't "default" the way you would with a bank loan. Instead, the platform liquidates your collateral to cover the loan. You lose your crypto, but you don't owe anything beyond that.

5. Is this better than a payday loan?

For many borrowers, yes. Payday loans have APRs of 400% or higher. Crypto loans at low LTV can offer 0% APR. Even at standard rates, they're usually far cheaper than payday loans. The main catch: you need crypto to borrow.