Credit line: Safety net every crypto investor needs

Crypto holders hate selling at the wrong time. Markets move fast, and liquidating assets for emergency cash can mean missing the next rally — and triggering a taxable event.

With credit lines, you don’t have to sell. They unlock liquidity on demand, ready whenever opportunity or necessity strikes.

Flexible and revolving, credit lines act as a smart safety net — whether you need fiat for a purchase, want to diversify your portfolio, or simply seek peace of mind. Unlike fixed-term loans, they take borrowing several steps further.

TL;DR

- A crypto credit line lets you borrow against your crypto without selling it.

- Unlike a fixed loan, it’s revolving — draw, repay, and reuse anytime.

- It helps you access liquidity, react to market opportunities, or fund real-world expenses.

- Approval is collateral-based — no credit checks or paperwork.

- Main risks include liquidation if collateral drops and interest costs if overused.

- Used responsibly, a credit line acts as a financial safety net.

What are crypto credit lines?

A crypto credit line lets you borrow against your digital assets by using them as collateral. Instead of selling BTC, ETH, or other holdings, you deposit them into a secured account and receive access to stablecoins (like USDC or USDT) or fiat currency

Where credit lines beat crypto loans

While both products let you borrow against crypto, there are important differences.

- Crypto loans allow you to borrow a fixed amount for a specific term, with a repayment schedule to follow.

- Crypto credit lines open ongoing access to capital. You control when and how much you borrow and repay.

Unlike a loan, a credit line is revolving. You’re approved for a limit and can draw funds when you need them and repay at your own pace. Borrow again anytime without reapplying.

Think of a loan as a one-time transaction. A credit line is a tool you keep in your back pocket. Read our full guide for an in-depth comparison.

Main uses of crypto credit lines

Access liquidity without selling

Instead of selling crypto to raise cash, you collateralize it and borrow against it. This preserves long-term exposure while freeing up capital for fresh opportunities.

React to market opportunities

Markets don’t wait. A revolving credit line lets you buy the dip, rotate into new assets, or diversify — without liquidating your core positions. You stay invested while staying agile.

Safety net, always on hand

A revolving credit line is always on, available 24/7 for unexpected expenses and time-sensitive investments. With platforms like Clapp, it’s capital on standby. Once your line is activated, you can draw funds instantly — no new approvals required.

Tax management

Selling crypto can trigger capital gains tax. Borrowing against it is generally not considered a taxable event. For long-term holders, this can be a more tax-efficient way to access liquidity. (Always check local regulations.)

Leveraged trading

Some traders use borrowed funds to increase exposure, aiming to amplify returns. While this strategy increases risk, a credit line provides controlled access to leverage without fully exiting existing positions.

Business operations

Corporate products give businesses flexible access to capital while keeping digital assets on the balance sheet. Entities and professional investors can fund working capital, equipment purchases, or expansion without liquidating treasury holdings.

Key advantages of crypto credit lines

Collateral is all you need

Approval is based on collateral, not your traditional credit score. If you have eligible assets, you unlock liquidity. No lengthy paperwork or income verification.

Instant access after pre-approval

Traditional bank loans can take days or weeks. Crypto credit lines can be activated in minutes. Once your line is pre-approved, you can draw funds immediately and use them however you see fit.

Swap, add, or rebalance anytime

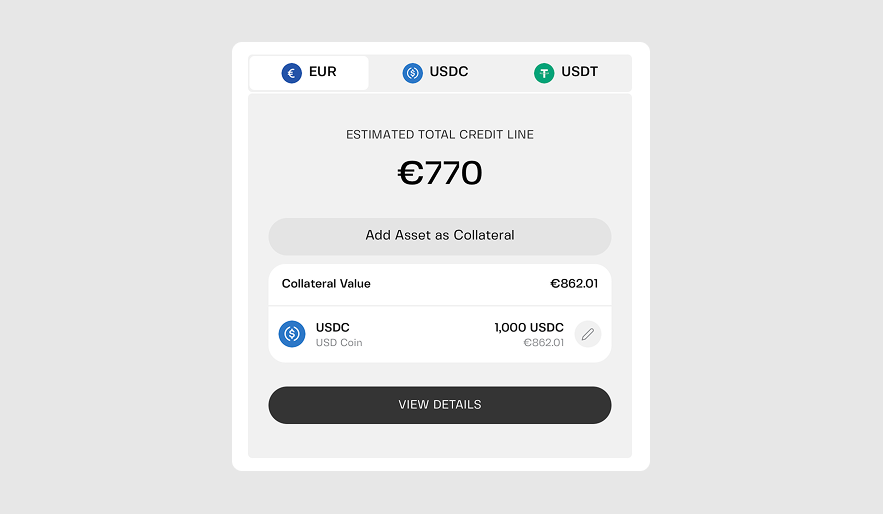

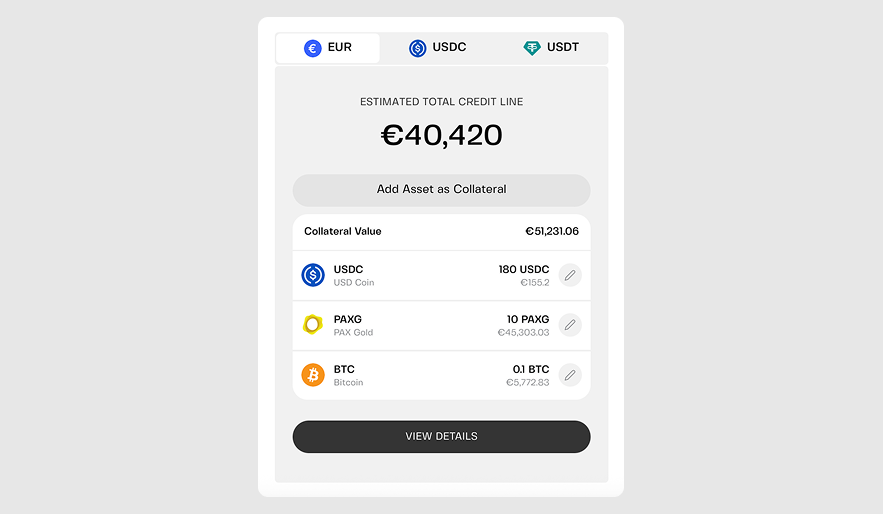

With Clapp's multi-collateral lines, your collateral doesn’t have to be static. Build a basket of assets — up to 25 — and add, remove, or replace them anytime. Lock in gains on one asset, rebalance exposure, or strengthen your position without refinancing the entire line.

Repay at your pace, no fixed deadlines

Repay any amount, anytime. Whether you want to clear the balance quickly or manage it gradually, you stay in control.

Your cost falls automatically as you repay

With floating rates, your borrowing costs decrease automatically as your outstanding balance shrinks. You only pay interest on what you actually use.

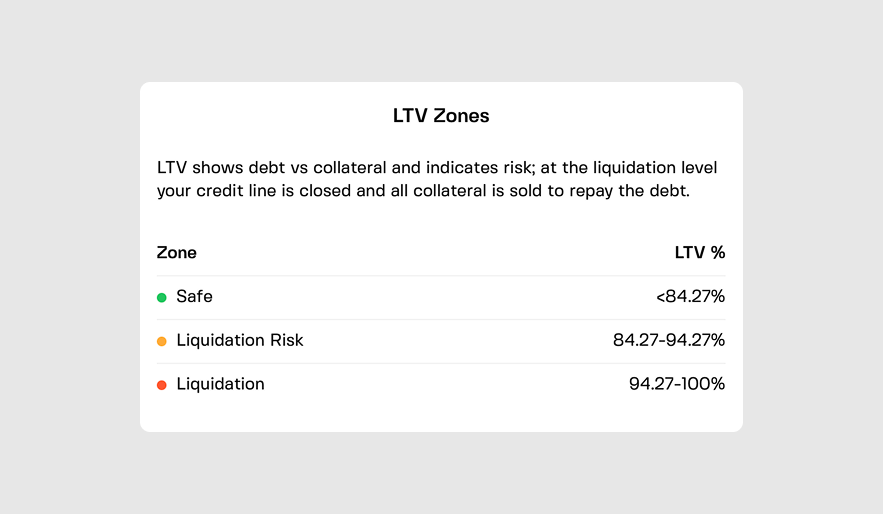

On Clapp, responsible borrowing is rewarded — keep your Loan-to-Value (LTV) below 20%, and you can effectively borrow at 0% interest, making it one of the most cost-efficient ways to access liquidity.

Put borrowed capital to work — even in savings

A credit line isn’t just for spending, as you can deploy the capital strategically. For instance, allocating part of it to savings products (fixed or flexible) or yield opportunities while keeping your core crypto holdings intact. Instead of selling assets to free up cash, you maintain exposure and let your liquidity work elsewhere within your broader financial strategy.

Risks to understand

Crypto credit lines come with important considerations, as no financial tool is risk-free.

Liquidation risk

If the value of your collateral drops significantly, part of it may be liquidated to repay the loan. That’s why monitoring your Loan-to-Value (LTV) ratio is critical. Smart platforms provide margin call alerts, giving you time to top up collateral or repay part of the balance before liquidation happens.

Interest costs

APR rates across the industry can range widely — from around 3% to 19% or more. Your effective rate depends on your LTV and usage. Always understand the cost structure before borrowing and avoid overleveraging.

Used responsibly, a credit line is a tool. Used recklessly, it magnifies risk.

How to open a crypto credit line

Opening a credit line should be simple. With Clapp, it takes three steps:

1. Activate & deposit

Activate your credit line and choose assets like BTC, ETH, or SOL for your collateral basket.

2. Draw funds, instantly

Withdraw USDT, USDC, or EUR up to your approved limit directly to your Clapp Wallet or your bank account via SEPA using your personal IBAN.

3. Repay flexibly

Repay on your own schedule. Add or remove collateral anytime to manage your LTV ratio and optimize borrowing costs.

No applications or waiting periods. Just instant access to a revolving line of credit when you need it.

Use your credit line on your terms

In volatile markets, flexibility is power. A crypto credit line lets you stay invested while staying liquid — protecting long-term exposure and giving you room to act.

Frequently asked questions

1. Should I use a crypto credit line instead of selling my crypto?

It depends on your goals. If you believe in the long-term value of your holdings, selling during a dip can lock in losses and trigger taxes. A credit line lets you access liquidity while maintaining exposure. However, irresponsible borrowing introduces liquidation risk.

2. What happens if the price of my collateral drops?

If this happens and your Loan-to-Value (LTV) ratio rises too high, you may face a margin call. That means you’ll need to add more collateral or repay part of the borrowed amount. Unless you act in time, part of your crypto could be auto-liquidated to cover the balance. Monitoring LTV and platform alerts is essential.

3. Do I need a credit score to open a crypto credit line?

No. Approval is based on the value of your collateral, not your personal credit history. That means no traditional credit checks, paperwork, or income verification. If you hold eligible crypto assets, you can typically activate a line within minutes or even seconds, depending on the platform.

4. Are crypto credit lines taxable?

In many jurisdictions, borrowing against crypto is not considered a taxable event because you’re not selling the asset. Yet tax rules vary by country, and interest payments may have different implications. It’s always smart to consult a tax advisor before making large financial decisions.

5. Can I repay early or partially?

Yes. Unlike traditional term loans, most crypto credit lines are flexible and revolving. You can repay any amount at any time, reducing your outstanding balance and interest costs. The more you repay, the lower your borrowing costs — since you only pay interest on what you use.

6. Is using a credit line for leveraged trading risky?

Yes — significantly. A credit line works best as a liquidity tool or safety net, not as a shortcut to outsized returns. Borrowing to increase market exposure can amplify gains, but it also magnifies losses. If markets move against you, your collateral could be liquidated.