Fixed-term savings aren't just for whales — here's how to start with $250

Crypto savings are often the first thing people think about when they want their crypto to generate passive income. Beyond price appreciation, yield is one of the only ways to make your holdings work while you wait.

But here's what stops many: they assume you need serious money for it to matter. Locking away thousands of dollars for months sounds like something whales do — not regular people.

That assumption is wrong.

With careful planning, fixed-term savings can make sense even if you're starting with just $250. And the trade-off — locking your money for a set period — isn't as intimidating as it sounds once you understand how to use it.

Let's walk through how fixed-term savings actually work, why the minimums are lower than you think, and when locking your money makes sense.

TL;DR

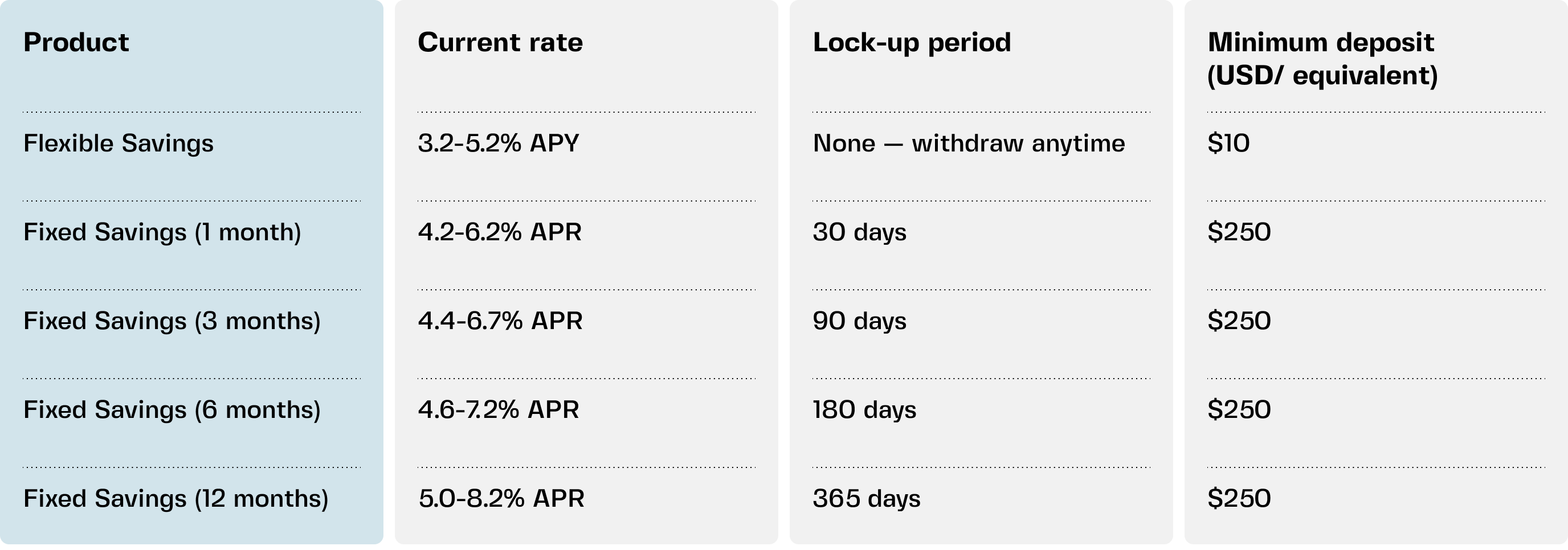

- Fixed-term savings lock your money for a set period. Usually 1, 3, 6, or 12 months. In return, you get a higher rate than flexible savings.

- Minimum deposits are often much lower than you'd expect. Clapp's Fixed Savings start at $250 equivalent — not thousands of dollars.

- Lock-ups aren't permanent. The term has to end eventually. You're not saying goodbye to your money forever.

- Higher rates for longer terms. Commit for 12 months and earn more than a 1-month term. Your patience gets rewarded.

- Use fixed-term savings for money you're sure you won't need. Keep your emergency fund in flexible savings. Lock the rest.

What fixed-term savings actually are

You deposit a set amount of crypto or fiat. You agree not to touch it for a specific period — 1 month, 3 months, 6 months, or a year. In exchange, the platform pays you a higher interest rate than their flexible savings product.

That's it. There's no hidden complexity.

The platform takes your deposit and puts it to work — lending it out, staking it, or deploying it across DeFi protocols. In return, you earn a portion of that yield and collect the interest at the end of the term.

That interest can be expressed as APR (Annual Percentage Rate) or APY (Annual Percentage Yield), depending on whether it includes compounding. With flexible accounts, your interest starts earning its own interest from day one, which slightly boosts the total. Fixed options typically show simple interest as APR, since compounding usually doesn’t apply during the lock-up period.

Why would you lock your money? Because higher rates come with commitment. The platform can offer better returns when it knows your funds won't disappear next week.

Traditional banks do the same thing. A 12-month certificate of deposit (CD) pays more than a regular savings account for exactly the same reason. The bank is willing to give you a higher rate because they know your money isn't leaving anytime soon.

The numbers that matter

Let's compare flexible vs. fixed on realistic rates.

Rates depend on both the asset and the term length. Fiat currencies and stablecoins typically earn higher rates than assets like BTC or ETH, since demand for dollar-based liquidity is usually stronger.

The term matters too. In most cases, the longer you commit your funds, the higher the rate becomes. A 12-month fixed term will generally pay more than a 1-month lock-up because the platform can plan around that liquidity for longer.

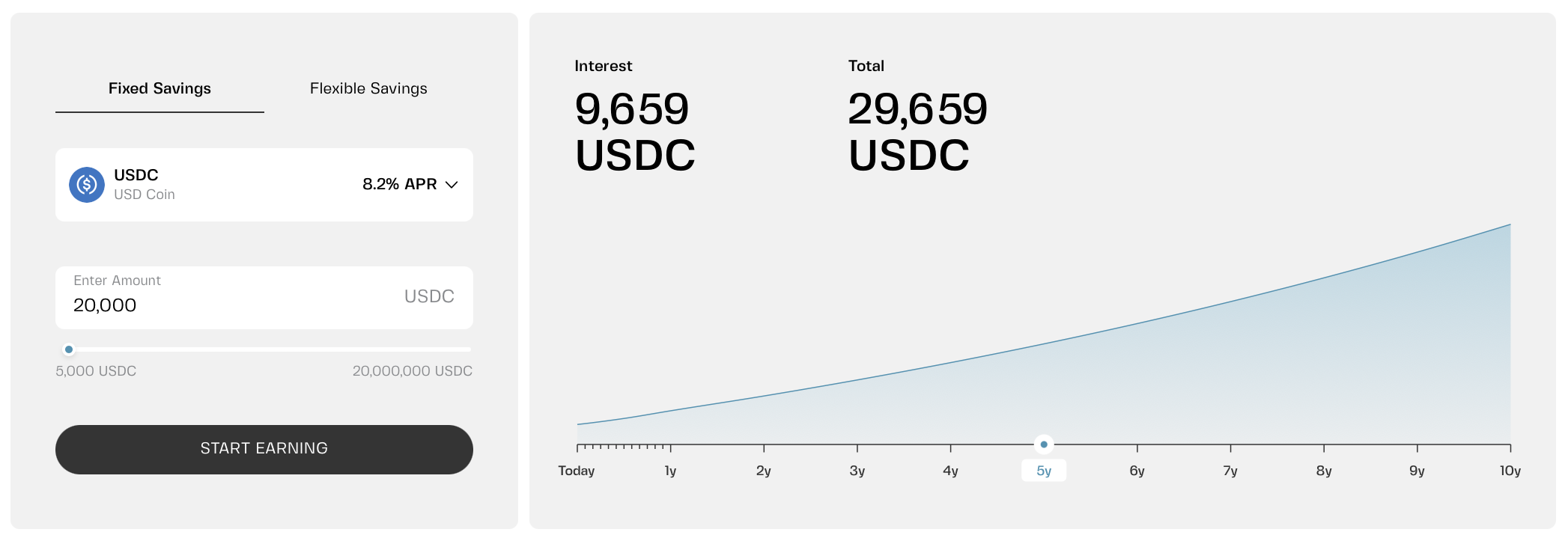

Flexible Savings are easier to enter — on Clapp, they start from just $10 equivalent and let you withdraw anytime. The trade-off is lower rates compared to fixed-term products.

Fixed Savings start at $250 equivalent. That's not pocket change, but it's also not a fortune. For context, that's less than a monthly car payment for many people.

The gap matters. The gap matters. On $10,000 over one year, the difference between 5% and 8% is $300. Scale it up or extend the term, and the gap widens.

Why the lock-up isn't as scary as it sounds

People hear "lock your money" and imagine kissing it goodbye forever. That's not how fixed-term savings work.

The term eventually ends. A 12-month deposit seems long until you realize how fast a year goes by. Six months sounds long — until you realize how quickly it passes.

- You're not trapped indefinitely. You know exactly when your money becomes available again. Mark it on your calendar. When that date arrives, your deposit plus interest lands back in your wallet.

- Some platforms offer monthly interest payouts. You can receive your earnings each month while the principal stays locked. That turns fixed savings into a passive income stream instead of money sitting untouched until maturity.

- Early withdrawal is possible in some cases. You usually forfeit the interest, but you can get your principal back if there's a real emergency. That's not a total lock-up with no exits.

How to use Fixed Savings without stressing

The key is to only lock money you're confident you won't need.

Step 1: Build your flexible buffer first.

Keep at least 3-6 months of expenses in Flexible Savings. That's your emergency fund. If something comes up, you have cash ready.

Step 2: Choose a term that matches your timeline.

Match the lock-up to when you'll actually need the funds:

- Saving for a vacation in 6 months? Pick a 6-month term.

- Have money set aside for next year's tax bill? Go with 12 months.

Step 3: Start small.

Don't lock your entire savings in one go. Try a 1-month term with $250. See how it feels. When the term ends and the interest lands in your account, the lock-up suddenly feels much less intimidating.

Step 4: Ladder your deposits.

Put some money in a 3-month term, some in a 6-month term, some in a 12-month term. As each term matures, you get access to a portion of your savings. That way you're not waiting a full year to see any of your money.

How to leverage it

Suppose you have $10,000 in USDT saved. You know you won′t need $4,000 of it for at least 6 months.

You keep the remaining 6,000 USDT in Flexible Savings (for emergencies) and put 4,000 USDT into a 6-month fixed term at 7.2% APR.

Important note: 7.2% APR is the annual rate. For a 6-month term, you earn about half of that — roughly 3.6% for the six-month period.

After six months, your 4,000 USDT becomes about 4,144 USDT. You earned $144 for doing nothing. Meanwhile, your Flexible Savings stayed accessible the whole time.

The habit of putting idle cash to work is worth more than any single interest payment.

Where Fixed Savings fit into a larger strategy

Fixed savings aren't an either-or choice. They work alongside other products.

- Flexible Savings for your emergency fund and short-term goals.

- Fixed Savings for money you're sure you won't need for months.

- Credit lines for liquidity without selling your crypto.

- Portfolios for long-term growth.

You don't have to pick one — many people use all of them. The right mix depends on your goals and how much access you need.

Bottom line: You don't need to be a whale

Fixed-term savings aren't just for people with six figures to spare.

The minimums are lower than you think. The lock-ups are shorter than you imagine. And the extra yield adds up over time.

Start small, even with $250. Try a 1-month term. See how it feels. When your money comes back with interest, you'll probably wonder why you didn't start sooner.

You don't need a fortune to make your money work harder. You just need to start.

Frequently asked questions

1. What's the minimum deposit for fixed-term savings?

It varies by platform. On Clapp, Fixed Savings start at $250 equivalent in USDC, USDT, EUR, BTC, or ETH. Flexible Savings have a much lower minimum ($10 equivalent) if you want to start smaller, but the yield rate is slightly lower.

2. Can I withdraw my money from fixed-term savings early if I really need it?

In most cases, yes — but you'll usually forfeit some or all of the interest. Some platforms allow early withdrawal of your principal only. Others charge a penalty. Read the terms carefully before locking your holdings into any savings product.

Flexible Savings let you withdraw anytime without penalties, which is why many people split their holdings between flexible and fixed-term products instead of locking everything at once.

3. What happens when the term ends?

You usually have two options. Withdraw the full amount (principal plus interest) to your wallet. Or let it auto-renew into a new fixed term at the current rate. Some platforms (including Clapp) let you turn auto-renewal on or off.

4. Are fixed-term savings safer than flexible savings?

The risk is generally the same — it depends more on the platform than the product itself. Both carry platform risk. Neither is insured like a traditional bank account. Choose a regulated platform with transparent custody, clear terms, and proven security measures beyond basic account protection.

5. Should I lock all my savings into fixed terms?

No. Keep at least 3-6 months of expenses in flexible savings. That's your emergency fund. Lock only the portion you're confident you won't need. A mix of both is the smartest approach for most people.