Daily compounding explained — with math that doesn't hurt your brain

You've seen the phrase "daily compounding" thrown around in crypto ads. It sounds technical, like something a banker made up to sound smart.

But daily compounding is actually simple — and once you understand it, you'll wonder why every savings account doesn't work this way.

Let's walk through what compounding means, why doing it daily matters, and how much extra money you could be leaving on the table.

TL;DR

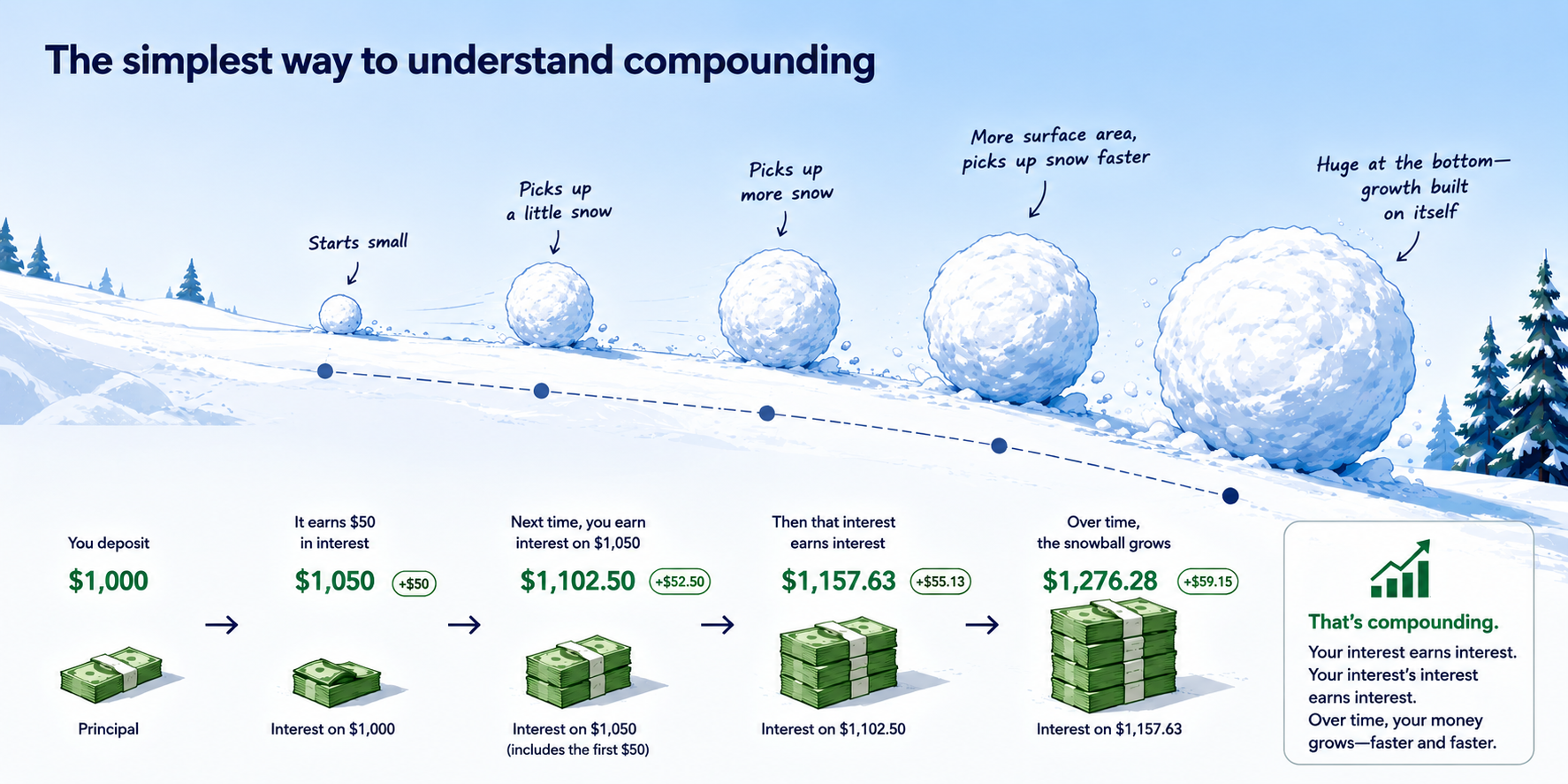

- Compounding means earning interest on your interest. Your money grows faster because earnings start earning their own returns.

- Daily compounding calculates interest every 24 hours. Monthly compounding does it once a month. The more frequent, the better.

- The difference starts small but grows over time. On $10,000 at 5% over 5 years, daily vs. monthly compounding is about $15 apart. Not huge. But add regular contributions and the gap widens over time.

- The real magic isn't the compounding frequency. It's letting your interest stay invested. Cashing out stops the snowball.

- You don't need to be a math person to benefit. Just set it and forget it.

What compounding actually means

Let's start with simple interest first.

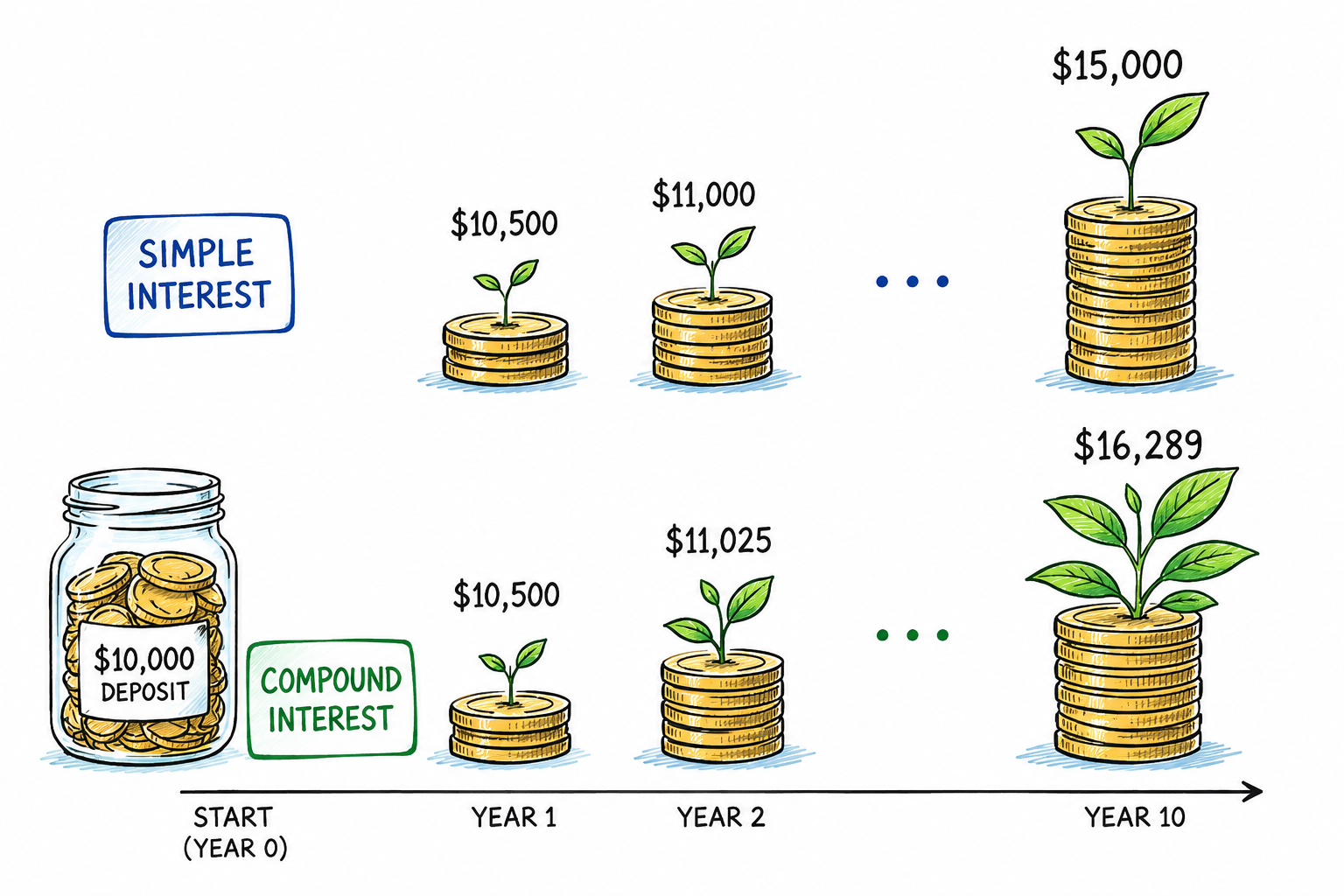

Suppose you deposit $10,000 into a savings account. The bank pays you 5% per year.

- One year later, you have $10,500.

- Two years later, you have $11,000.

- Ten years later, you have $15,000.

The interest is calculated only on the original $10,000 (the principal). That's simple, linear interest.

Compounding is different. It means you also generate earnings on earnings, not just the original deposit. Here's how Investopedia explains it:

"Compounding is the process where an asset's earnings, from either capital gains or interest, are reinvested to generate additional earnings over time."

Let's see compounding in action with the same $10,000 at 5%.

After one year, you have $10,500 (principal + $500 interest). So far, same as before.

But here's where it changes. Suppose your bank calculates compound interest annually. In year two, you earn interest on $10,500 — not just your original $10,000. That extra $500 you earned in year one now earns its own interest.

After two years, you have $11,025. That's $25 more than simple interest.

Let's extend to ten years.

- After ten years with compounding, you have about $16,289.

- With simple interest, you'd have $15,000.

- The difference is $1,289.

Now let's make it more compelling

Same $10,000 at 5%, but this time you add $500 every month, and compounding occurs every single day — which is more typical in crypto savings products than in traditional bank accounts.

- Without compounding, your returns stay perfectly linear. You’re essentially just earning a fixed rate on money as it arrives.

- With compounding, the picture changes. Interest starts earning its own interest, and the effect slowly builds in the background while your monthly deposits do most of the heavy lifting.

After 5 years, the difference is still modest. After 10 years, it becomes impossible to ignore — not because compounding suddenly dominates, but because time finally gives it room to work.

The key point isn’t that compounding replaces contributions. It doesn’t. It’s that over longer horizons, it quietly starts amplifying them.

Key distinction you need to understand: APR vs APY

APR (Annual Percentage Rate) shows the raw interest rate without accounting for compounding. It’s the simple “headline” rate.

APY (Annual Percentage Yield) includes the effect of compounding — meaning it assumes your interest is being reinvested at a specific frequency (daily, monthly, etc.).

So if two products both advertise 5%, the APY version will usually earn more over time, because your interest is being added back into the balance and generating its own returns.

In short:

- APR = simple interest

- APY = compounding included

This difference is why compounding frequency matters — and why “daily compounding” shows up so often in crypto savings products.

But that raises an obvious question: if compounding is already baked into APY, does the frequency (daily vs monthly) really matter that much?

So is daily compounding overhyped?

Compounding alone is slow. The real effect comes when you combine it with regular contributions.

Most people don't just deposit a lump sum and wait — they add money over time, just like in the example above.

The point isn't that daily compounding is dramatically better than monthly compounding — the difference between frequencies is real, but usually modest in isolation.

But that doesn't mean it doesn't matter. There's no reason to accept less.

The bigger insight

Daily compounding isn't the hero of the story. Letting your interest stay invested is what actually drives the result.

Consider the same example with a $10,000 deposit and two ways the balance can evolve over 10 years:

- If you cash out interest every month, your final balance is that original $10,000. (ignoring any interest reinvestment effect)

- If you let interest compound daily, your final balance is $16,486.

That's a difference of over $6,000 on the same deposit, rate, and time period. The only difference is whether your interest is allowed to keep earning — or is removed before it can compound.

The compounding frequency is secondary. The real question is whether you're letting your snowball roll — or stopping it every month to pick up the new snow.

A simple way to think about it

Imagine a snowball rolling down a hill.

If you stop every few feet to pick off the new snow, the snowball never grows. You end up with a pile of snow, not a rolling ball.

If you let it keep rolling, it picks up more snow, gets heavier, and accelerates. By the time it reaches the bottom, it's significantly larger.

Daily compounding is just letting the snowball roll without interruption. The frequency matters less than the fact that you're not interrupting it.

What this means for you

You don't need to be a math expert. You just need to understand three simple ideas:

First, choose a savings product that compounds daily. Even if the difference is small, it's still mathematically better than less frequent compounding.

Second — and more important — don't cash out your interest. Let it stay in the account so it can compound.

Third, add to your balance over time. Every new deposit starts earning interest immediately — and then earning interest on that interest.

The people who benefit most from compounding aren't the ones who started with the most money. They're the ones who started early and never interrupted the process.

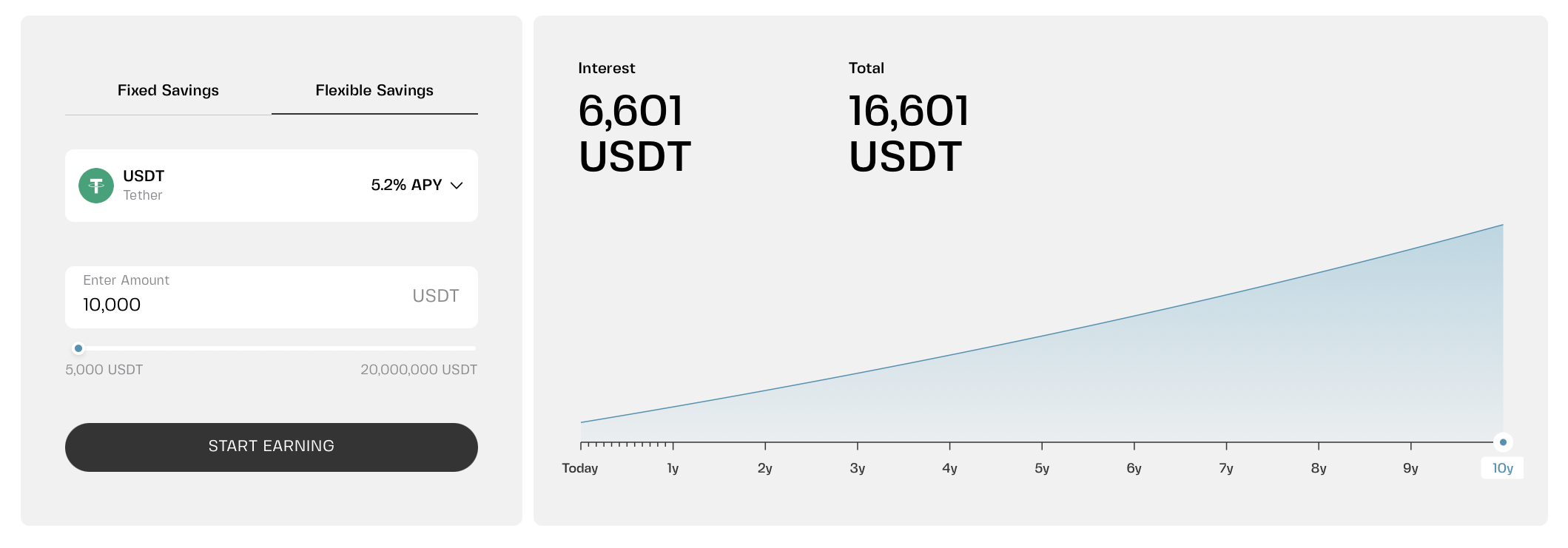

Example: Compounding in Clapp Savings

Clapp's Flexible Savings compounds daily. Your interest is calculated every 24 hours and added to your balance automatically. That interest then starts earning its own interest the next day — no manual reinvestment, no claiming rewards.

And because Flexible Savings has no lock-ups, your funds remain accessible. You can withdraw anytime if you need to. But if you don't, the compounding effect continues uninterrupted.

Fixed Savings works differently — it uses a fixed APR structure, where interest is calculated on the principal over the term. That means no intra-term compounding effect, but a higher annual rate (up to 8.2% APR). As a result,

- Flexible Savings is more suitable for continuous compounding,

- Fixed Savings is better when you want a predictable return over a defined period, regardless of compounding frequency.

Let the snowball roll

Daily compounding isn't magic that will turn $100 into a fortune overnight. But it is real math. And over time, it consistently beats leaving interest un-reinvested.

The more important decision isn't daily vs. monthly compounding. It's whether you allow your interest to stay in the system and keep working.

That’s all compounding really is — time plus reinvestment. Everything else is just implementation detail.

Frequently asked questions

1. Is daily compounding really that much better than monthly?

On its own, no. The difference over several years is small. But daily compounding is still better, and there's no reason to accept less frequent compounding if daily is available.

2. Why does everyone hype daily compounding then?

Because it sounds impressive. The real driver of growth is leaving your interest invested, not the compounding frequency. Daily is better than monthly, but monthly is much better than cashing out.

3. Does compounding work the same for stablecoins and volatile crypto?

For savings accounts, yes. The interest rate is applied to your balance regardless of the asset's price. For staking or lending, the APY can fluctuate, but the compounding mechanics are the same.

4. Should I move my money from a monthly compounding account to a daily one?

If the interest rate is the same, yes. Daily compounding gives you a slightly better return. But the rate itself matters more than the frequency. A 6% monthly account beats a 5% daily account.

5. How much do I need to start?

On Clapp, Flexible Savings starts at $10 equivalent. The habit matters more than the amount. Let small money roll, add to it regularly, and don't interrupt the snowball. That's how compounding actually works.