Don't sell your crypto. Borrow against it like the wealthy do.

Crypto price swings can leave even the most chill investor second-guessing everything. One month you're up, the next you're staring at a portfolio that's 30% lighter and wondering what to do next.

Macro drama is one thing — but what about when life throws its own curveball? A business idea. An emergency expense. Something you want to do without cashing out your future.

Should you sell?

Not necessarily. There's a way to use your crypto without giving it up.

The case against selling crypto

Selling is the obvious, knee-jerk move. Open your app, tap a few buttons, and poof. Your assets become cash. Simple.

Almost too simple.

Because selling feels final in a way that's easy to miss when you're in a hurry. That Bitcoin you sold at $60,000 might be worth $90,000 next year. To get back in, you'd have to buy back at a higher price.

Taxes also come into play. In most places, the moment you sell, your gains become taxable — even if you're just moving money around to cover life stuff.

Selling gives you immediate liquidity. But there's a catch.

Picture a farmer with a good piece of land. It's been in the family for generations. Produces every year, rain or shine.

A bad season hits. Bills stack up. The easy thought: sell the field. Walk away, start over somewhere else.

But farmers know better. They borrow against the land. They plant next year's crop. The field stays theirs, and when harvest comes, they're still there to bring it in.

Selling solves today's problem — but you lose what could've grown tomorrow.

Access cash, keep your coins

Wealthy individuals have known this trick for generations. When they need cash, they don't sell what they own. They borrow against it.

If a homeowner needs capital, they take out a home equity line — the house stays theirs. When an investor wants liquidity, they use stocks as collateral with a margin account. The asset keeps growing in the background while the cash flows in.

Crypto holders can do the same thing now, choosing between fixed-term loans and flexible credit lines.

When you borrow against crypto, you're locking it up as collateral. Think of it like putting your passport in a hotel safe during a trip. You can't carry it around while you're swimming, but it's still yours. When checkout comes, you open the safe and take it back — exactly as you left it.

How it works on Clapp

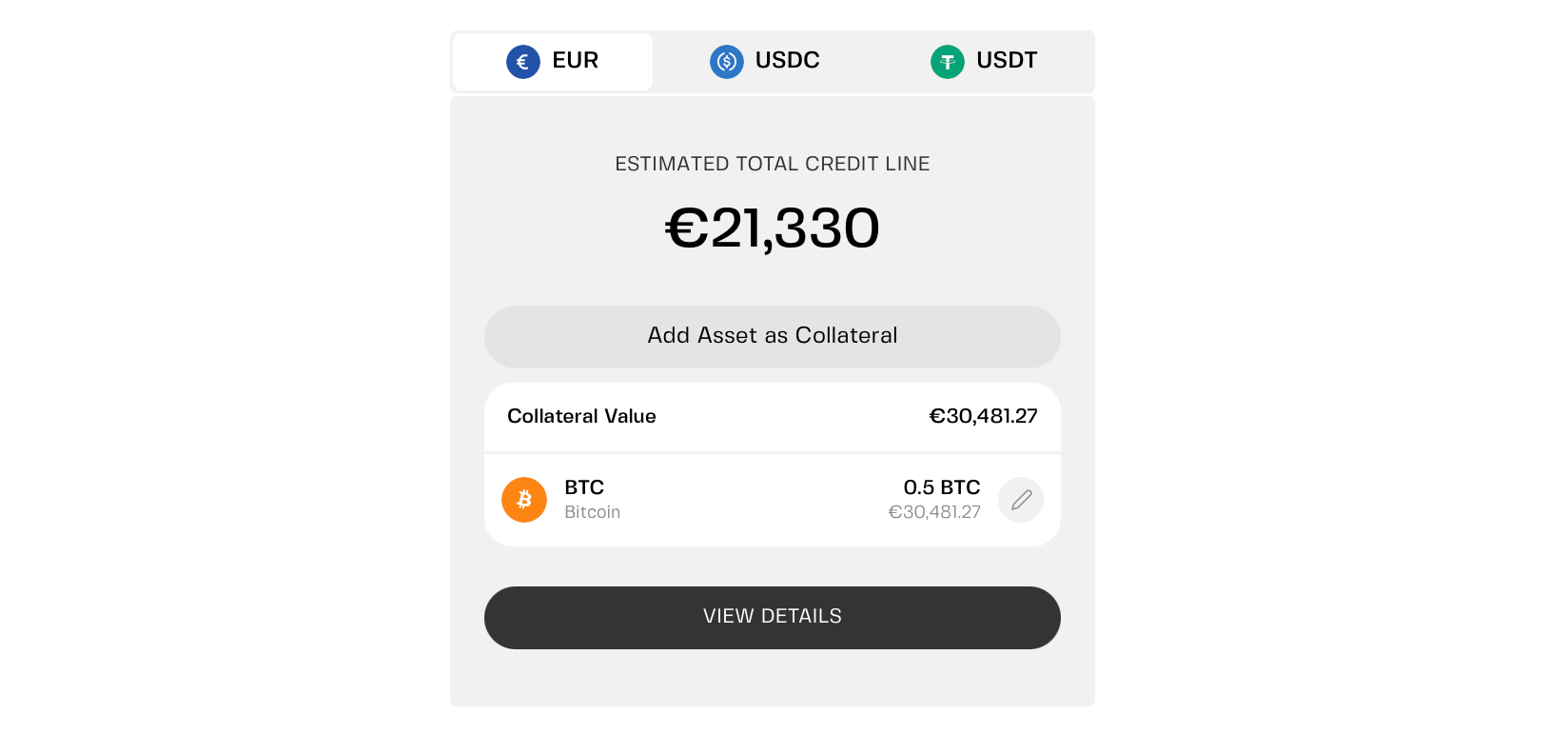

- Deposit crypto as collateral and choose your borrowing currency — fiat or stablecoins. The platform shows your estimated credit line. In this example, pledging 0.5 BTC (market value €30,481) unlocks €21,330.

- Activate your credit line, and funds are ready to use immediately. Keep them in your Clapp Wallet to trade or swap, or withdraw to your bank via SEPA — partially or in full, anytime.

Your BTC stays pledged but untouched, released back to you upon full repayment. Repay whenever you want, with no penalties for paying early.

No credit checks. No selling. No tax event.

But there's more. The credit line is multi-collateral, meaning you can pledge 1–25 assets and reshuffle that collateral whenever you want.

Pledged ETH but want to stake it natively? Swap it for SOL, BNB, or any other collateral asset — your credit line stays intact. Add or remove assets as you like. Just keep an eye on the LTV.

You can even put those borrowed funds right back to work in Savings. Borrow at 0% APR (if you keep LTV low) and earn competitive yield on stablecoins or euros. That's money on money borrowed — your liquidity generating yield while you hold your crypto.

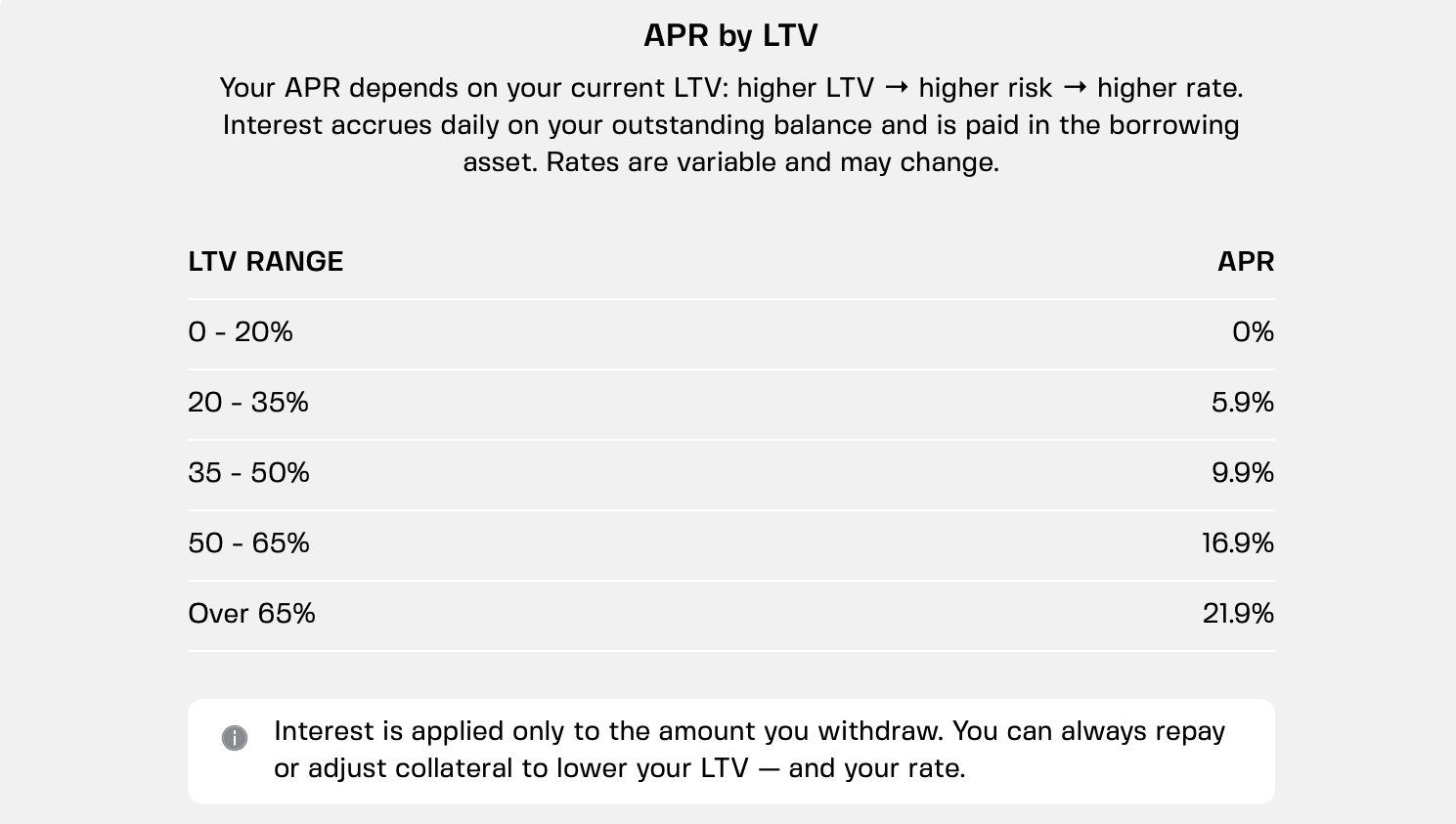

Your LTV, your interest rate

Every platform has a safety threshold. The loan-to-value ratio (LTV) measures risk — how much you've borrowed compared to what your collateral is worth. It determines two things:

- How much you can borrow

- How much it will cost

Like loans, credit lines are over-collateralized, so you always borrow less than you pledge.

APR (Annual Percentage Rate) — the actual cost of borrowing — scales directly with LTV. The safer your position, the less you pay. Rates typically range from 0% to over 20% APR depending on how much risk you're taking.

Say you borrow $10,000 and your collateral is worth $50,000. That's 20% LTV — very safe. On Clapp, you pay 0% interest at that level.

If BTC drops and your collateral falls to $20,000, your LTV jumps to 50%. You still owe the same $10,000, but your backing is thinner. Borrowing costs rise as the APR adjusts higher to reflect the increased risk.

What happens if my collateral value changes?

This is where people get nervous — and fair enough. Crypto moves fast.

- Market rises: You keep the upside. You can even borrow more later if you want.

- Market dips: You'll get a notification. Add more collateral or repay part of what you borrowed.

If you don't act and the price keeps falling, the system may auto-sell (liquidate) your collateral to protect the platform. That mechanism ensures your credit line stays backed — even when markets go wild.

Why this strategy clicks for HODLers

Borrowing against crypto isn't about taking reckless debt. It's about thinking like an asset owner.

You've built something valuable. Now instead of selling it off, you're learning to use it — without losing the future upside you bought it for.

It's the same principle wealthy families have followed for decades: keep assets working in the background, borrow when you need liquidity, never sell what you expect to grow.

This approach lets you stay invested in something you believe in while still having flexibility in your day-to-day life.

The catch? You have to pay attention

Every loan or credit line, even one backed by crypto, comes with responsibility. If the market drops sharply and your collateral loses value, you might need to step in — either by adding more or paying back a portion of what you borrowed.

That's why smart borrowers don't take out the maximum. They stay conservative, borrowing what they actually need — not what the calculator says is possible.

Borrow $10,000 against $50,000 in BTC, and your safety net costs you nothing. Zero interest. No monthly payments. Just liquidity, ready when you need it.

Need the funds for longer? You pay interest only on what you use, only as long as you use it. Repay anytime — no strings attached.

The long view

What started on the fringes is now the financial mainstream. Large asset managers hold crypto. Banks are building custody services. Regulators are setting clearer frameworks instead of blanket bans.

This shift changes how individuals think, too. Instead of treating crypto as something to time perfectly, more people now see it as an asset to manage — to borrow against, to earn on, and to hold as part of a long-term strategy.

Life doesn't stop while you hold. Now you have options beyond selling.

Frequently asked questions

1. Do I lose my crypto if I borrow against it?

No. Your crypto stays yours — it's just locked as collateral while your credit line is active. Think of it like putting down a deposit on an apartment. The landlord holds it, but it's still your money. Repay what you borrowed, and your crypto comes right back to you, same as before.

2. How much can I borrow?

It depends on what you pledge and which platform you use. Most lenders let you borrow a percentage of your collateral's value — typically 40–70%. The safer you play it, the more breathing room you have if markets dip. On Clapp, keep your LTV at 20% or below and you pay 0% interest. Not bad for a financial safety net.

3. What can I use the funds for?

Whatever you need. Business idea? Go for it. Emergency expense? Covered. Another investment opportunity? All yours. Funds typically land in your platform wallet — you can use them in-app, swap, or withdraw to your bank. With Clapp, for instance, you get a personal IBAN for easy SEPA transfers in and out.

4. Is this better than just selling?

Depends on your goals. Selling is simple and gives you instant cash — but it's permanent. If prices rally later, you're out of the game. Borrowing lets you have it both ways: liquidity now, upside later. Plus, no tax event when you borrow, since you haven't sold anything. For long-term believers, that's a game changer.

5. How much does it cost to borrow?

It depends on your loan-to-value ratio. The lower your LTV, the cheaper your borrowing. Rates generally range from 0% to over 20% APR depending on how much risk you're taking. On Clapp, keep your LTV at 20% or below and you pay 0% interest — your safety net costs nothing. Push LTV higher, and the rate adjusts accordingly. Always check the platform's rate table before you borrow.

6. How do I get started?

Sign up on a platform that offers crypto-backed borrowing, complete the verification, and deposit the crypto you want to use as collateral. From there, you'll see your available credit and can activate instantly. On Clapp, the whole process takes minutes — no credit checks, no paperwork, no waiting. Funds hit your wallet the moment you confirm.