Four stablecoin business models — what's really changing?

Stablecoins have quietly become one of the highest-margin businesses in crypto — and the competition is no longer just about scale. It’s about who controls distribution, captures yield, and integrates into real-world financial flows in a $300B+ market.

Think of stablecoins as crypto's engine. They're dry powder for traders and a bridge to the real world, all in one. While USDT and USDC account for most of the market share, fresh entrants are introducing new issuance models to carve out their own slice of the pie.

State of stablecoin market in 2026

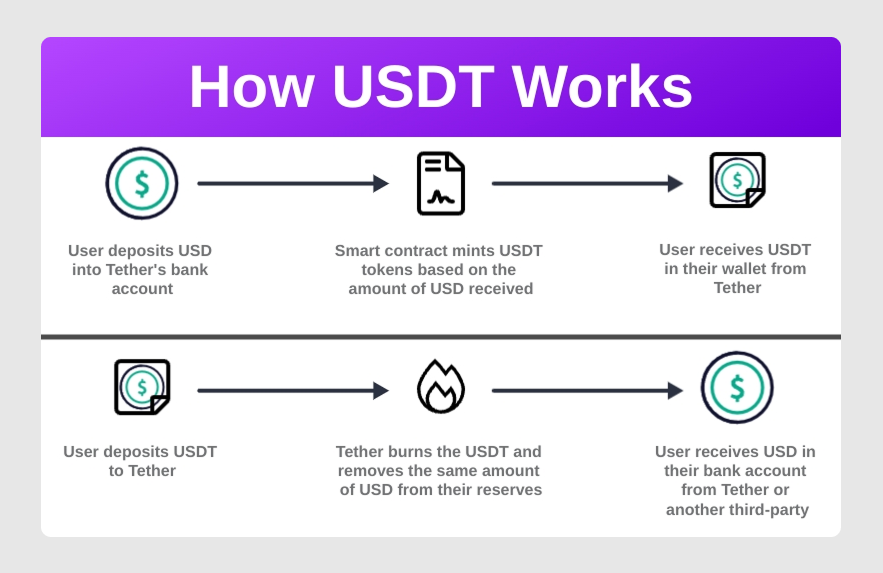

Stablecoin issuance is one of the most profitable business models in the industry. Tether, with its core reserve-yield model, was first to dominate the space, becoming the primary liquidity provider in early trading markets.

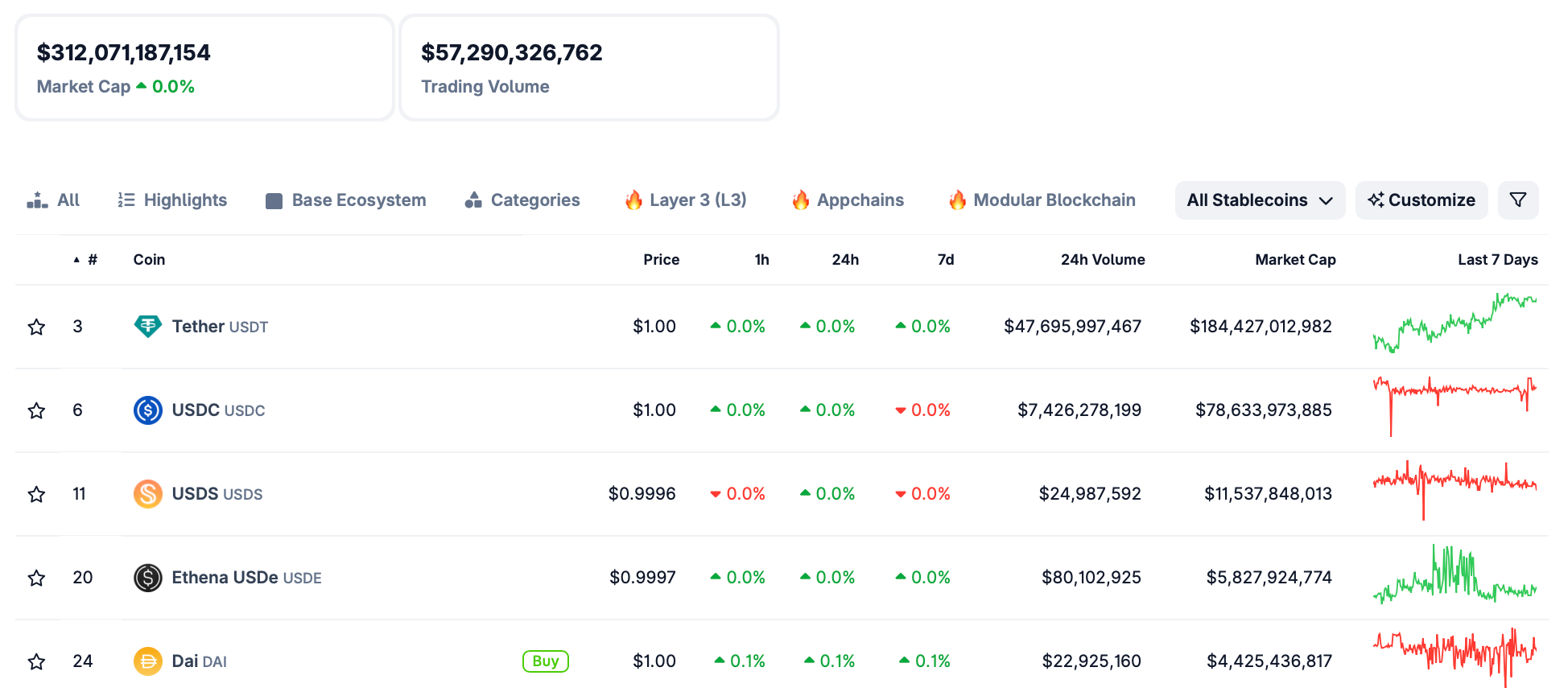

Since its launch in 2014, USDT's market cap has ballooned beyond $184 billion — over 62% of the total $312 billion market at press time, according to CoinGecko data. The stablecoin category includes nearly 400 assets.

Circle followed suit, launching USDC in 2018 with a strong focus on regulatory compliance. In 2025, it expanded its reach into TradFi through a NYSE listing.

Just like Tether, Circle's bread and butter comes from putting those deposits to work, not from issuing USDC itself:

- For every $1 deposited by users, the issuer mints 1 USDT or USDC.

- The dollars are deployed into low-risk assets like US Treasuries or money market funds.

- As supply grows, so does the reserve base — and the interest it generates.

Other entrants followed, with diverse revenue strategies tailored to their scale and positioning. As the market cap exploded, major jurisdictions kicked off a full-scale global regulatory arms race.

The GENIUS Act — the first US federal framework for payment stablecoins — arrived in July 2025, introducing stricter requirements around reserves, audits, and issuer registration. Meanwhile, the EU enforced MiCA, and Hong Kong passed its Stablecoin Ordinance.

USD-pegged stablecoins dominate the space ($307 billion); EUR-backed assets account for a modest $913 million. Aside from fiat-backed tokens (USD, EUR, JPY, GBP), assets fall into the following top categories:

- Synthetic dollar

- Crypto-backed stablecoins

- Algorithmic stablecoins

- US Treasury-backed stablecoins

- Commodity-backed stablecoins

#1 Tether: Reserve giant

Tether holds a decade-long grip on the market, with reserve management still at its core. Whenever it issues USDT, it takes in an equivalent amount in US dollars and parks it in low-risk assets — US Treasuries, reverse repos, and money market funds.

According to Tiger Research, "reserve management income appears to make up the substantial majority of total profit." But the Tether of today is a far cry from the Tether of 2014. Deliberate structural shifts have brought in multiple revenue streams:

- A complete overhaul of its reserve composition

- Moving from commercial paper toward US Treasuries

- Setting up a quarterly external attestation framework

- Shifting to a diversified model that reinvests stablecoin profits into AI, energy, education, and communications

The core logic still holds: as issuance grows, so does the pool under management — and the interest it accumulates. Apart from US Treasuries, Tether keeps a portion of its reserves in gold and Bitcoin; price gains in either asset contribute to mark-to-market gains. Other revenue streams include transaction fees and protocol integration fees.

The GENIUS Act framework created headaches for Tether, as it mandates 100% cash-equivalent reserves, strict auditing, and federal registration. To keep the American audience, it launched a separate stablecoin — USAT — built for local regulation. USDT remains its global workhorse.

Tether publishes quarterly reserve attestation reports verified by BDO Italia. In March 2026, it formally engaged a Big Four accounting firm for a full audit of USDT reserves. The USDT and USAT markets are structurally split and pursued side by side.

#2 KRWQ: Won peg

The first stablecoin pegged to the Korean won launched in October 2025. Built by IQ in partnership with Frax, it targets offshore markets where investors want to hedge or bet on KRW exchange rate moves. The end goal is to become the first regulation-compliant KRW stablecoin.

At present, South Korea has no domestic rules for won-denominated tokens — that legislation is still under deliberation in the National Assembly. The fiat won is legally traded only inside the country — hence the "offshore before onshore" game plan.

KRWQ's growth strategy has three phases:

- Offshore capture

- Onshore migration

- Expansion across Asian currencies like INR (Indian rupee), TWD (Taiwan dollar), and IDR (Indonesian rupiah)

Foreign shareholders of South Korean businesses — think Samsung Electronics shares — are fully exposed to KRW swings but have no direct way to hedge from abroad. Right now, this need is met by the NDF (Non-Deliverable Forward): a contract settled in US dollars for the difference between an agreed rate and the actual rate.

One of the largest NDF markets, the KRW NDF market has opaque pricing, high transaction costs, and counterparty risk since it's OTC-based. It's built around bilateral bank negotiations, with liquidity and the pool of eligible participants kept severely tight.

KRWQ addresses these flaws through perpetual futures, similar to NDFs but without expiry. Holders can hedge or take directional bets on KRW rate movements — no direct exchange, settlement in US dollars based on price differences.

Key differences between KRWQ and the traditional NDF market (recently launched through EDXM International):

- No maturity

- Runs 24/7 on-chain

- Lower cost

KRWQ is building its offshore liquidity lead ahead of competitors, aiming to team up with domestic regulated banking institutions once regulation is in place. This final stage will enable direct KRW deposits and withdrawals for issuance and redemption.

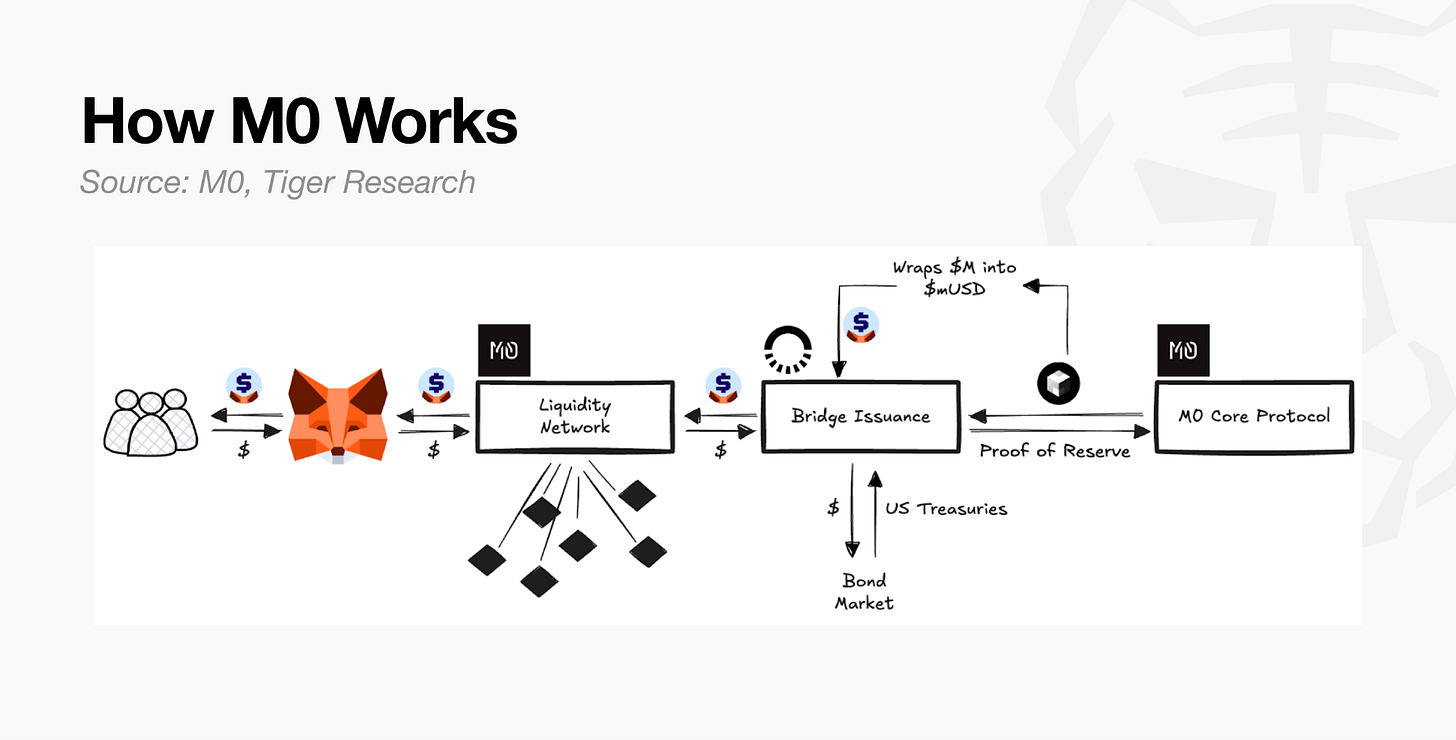

#3 M0: Shared infrastructure

M0 gives businesses a common technical foundation to launch their own stablecoins and issuing institutions. Backed by Bridge (a Stripe company), MoonPay, and 1Money, it tackles two core problems:

- Market fragmentation: each issuer uses an independent stack, making cross-coin compatibility a mess.

- The "cold-start" problem: on launch day, issuers must build liquidity, partnerships, and network effects from scratch.

M0's shared layer ensures all newly minted assets — think MetaMask's mUSD, Exodus XO Cash, KAST's USDK, Noble's USDN, Usual's UsualM — share standards and technology. From the get-go, they are redeemable 1:1 with every other stablecoin and tap into existing liquidity.

So M0's model has two core participants — the issuer and the builder. These roles are completely separate.

- Issuer (e.g., Bridge): A regulated institution parks reserves (e.g., US Treasuries) as collateral to mint and burn stablecoins via M0's infrastructure. The platform gets a cut from the interest earned on those reserves.

- Builder (e.g., MetaMask): The owner of a specific use case uses M0 to launch and control its own stablecoin (e.g., mUSD). It never touches the collateral — it just captures the economics and tweaks behavior within its product.

Using M0's infrastructure does not replace regulatory responsibility — it only handles compliance at the technology layer (allow-listing, pausing, and freezing). The issuer is fully responsible for the actual operation of these functions, along with licensing, AML, KYC, and any other regulatory boxes to check.

M0's current circulating supply sits at just over $278 million. As more issuers and builders join the network, this figure is expected to grow — a key metric at this stage.

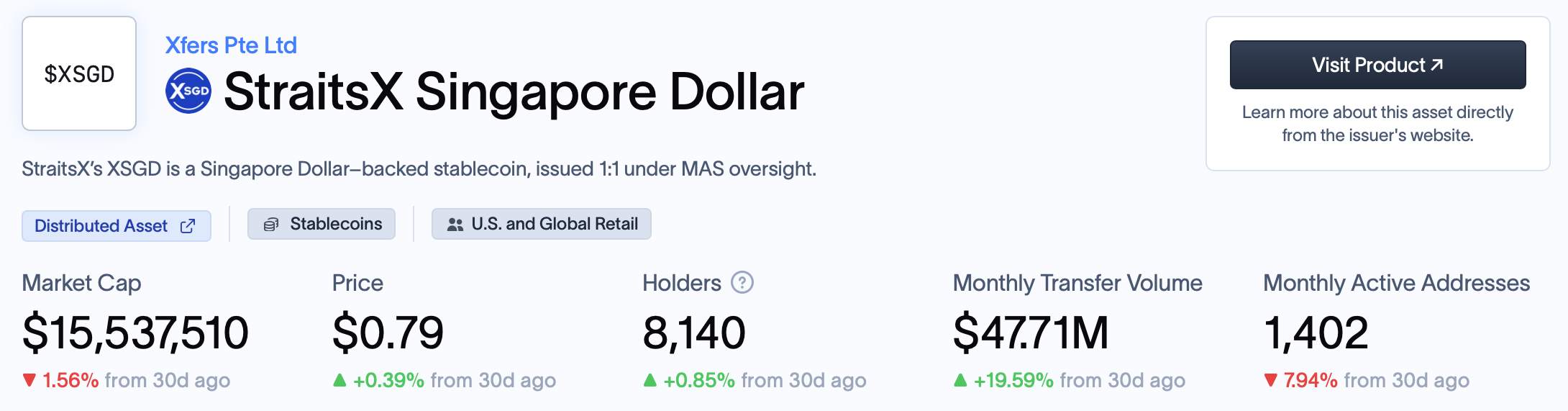

#4 StraitsX: ASEAN commerce play

Headquartered in Singapore, this issuer powers XSGD (SGD-pegged) and XUSD (USD-pegged). Its expansion into top ASEAN fiat currencies — like the Indonesian rupiah (XIDR) — is supported by proprietary payment infrastructure tied directly to the region's real economy.

StraitsX's absolute asset size and turnover pale next to Tether — currently, just around $39.9 million in monthly XSGD transfer volume, which is roughly 2.5x its market cap (around $15.5 million), according to RWA.xyz. For XIDR, the total market cap is a mere $120,501.

Unlike giants like USDC that trade on crypto exchanges, StraitsX tokens serve a totally different use case — everyday commerce. They keep moving, supported by robust B2B payment network integrations including Alipay+ and global exchanges like Binance and Bybit using StraitsX's fund settlement facilities.

The revenue model revolves around payment fees tied to transaction volume — letting it scale alongside business growth. Interest on reserves, while also in the mix, is limited by external variables like circulating supply and interest rates.

- Reserve interest: StraitsX parks reserves backing the circulating XSGD and XUSD in trust accounts at DBS, Standard Chartered, and CIMB. Under MAS regulations, interest goes to the company, not token holders.

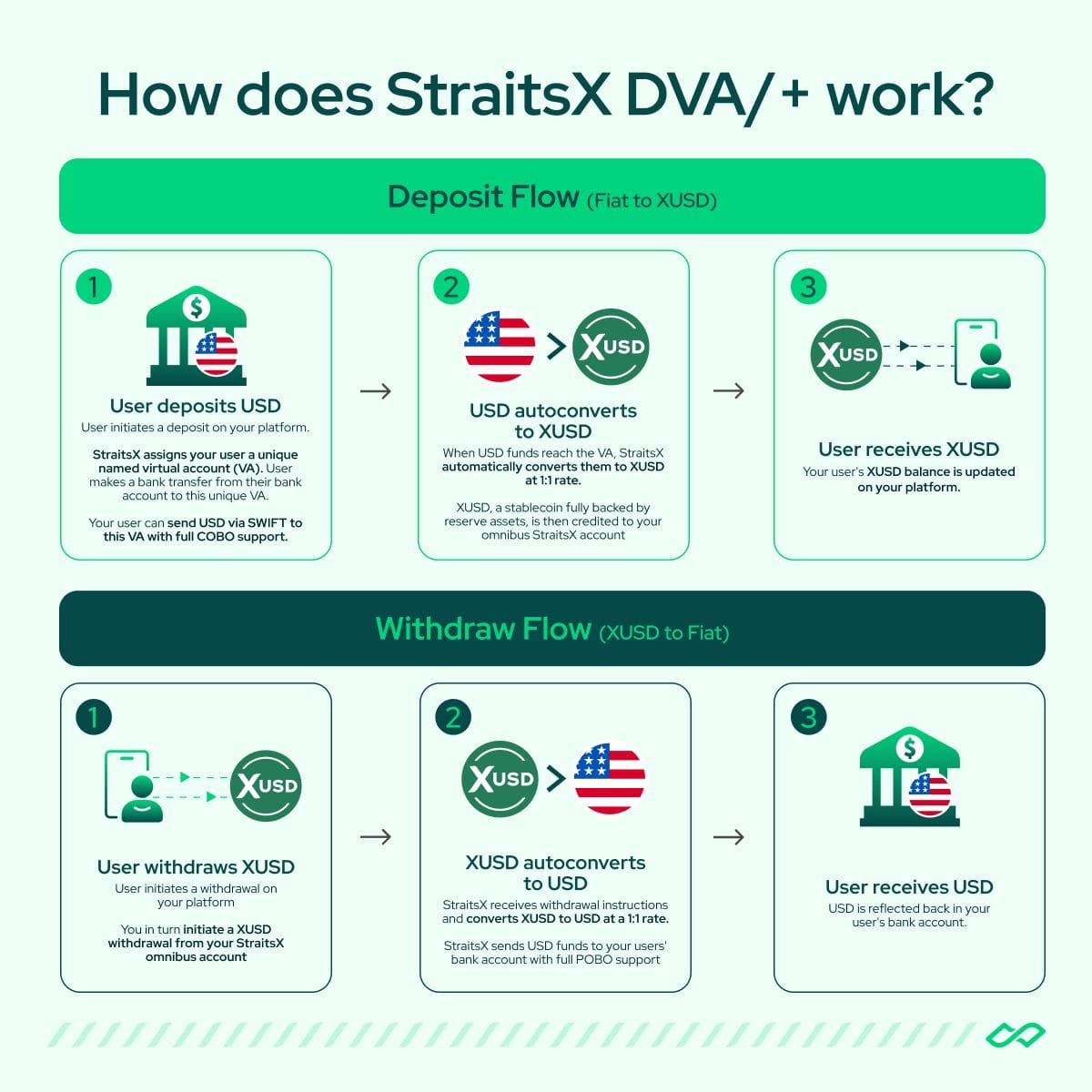

- Payment processing fees: These are paid every time stablecoins are used for payment or settlement — from on-ramp/off-ramp (DVA) to QR payment networks like Alipay, to Visa card issuance. The latter has grown 40x in volume over the past year.

- OTC and FX swap spreads: Stablecoin-to-stablecoin swaps, buy/sell transactions, and large OTC trades all involve spreads.

StraitsX holds a Major Payment Institution (MPI) license from the Monetary Authority of Singapore (MAS), using the framework as a competitive shield. Beyond coin issuance, it can legally handle cross-border remittance, foreign exchange, merchant payments, and account issuance all under one roof.

Both XSGD and XUSD are recognized as substantially compliant with the MAS Single-Currency Stablecoin (SCS) regulatory framework.

StraitsX has also teamed up with regulators to co-develop a next-generation cryptography-based identity verification system — a crucial step to catch institutional funds once they start flowing in at scale. Real-world asset (RWA) settlement is seen as the primary long-term growth driver.

Wrapping up

The stablecoin market is top-heavy, with USDT and USDC gobbling up over 85% of total supply. Going head-to-head on the same reserve-interest model isn't a realistic path for newcomers — but the cases above show there's more than one way into the game.

Latecomers are unlikely to win on reserve scale alone, so they focus on differentiation — whether through payment networks, issuance infrastructure, or niche market access. As the market continues to grow, so does the range of strategies.

The industry is evolving into a landscape where multiple models coexist. The next wave of entrants will need to identify problems that incumbents have not addressed.

The market has moved beyond “who has a new model?” to “who can execute effectively?” The stablecoin issuers that endure will be those that consistently execute and solve increasingly complex challenges as they scale.