Your stablecoin yield may not last forever — CLARITY Act explained

Stablecoin yield has become a primary battleground in debates over the US CLARITY Act. Regulators are drawing a line between passive payouts and rewards tied to platform activity — and the difference could ignite a boom in new compliant strategies.

Here's what this distinction means for the average user and which rewards will likely remain legal.

TL;DR

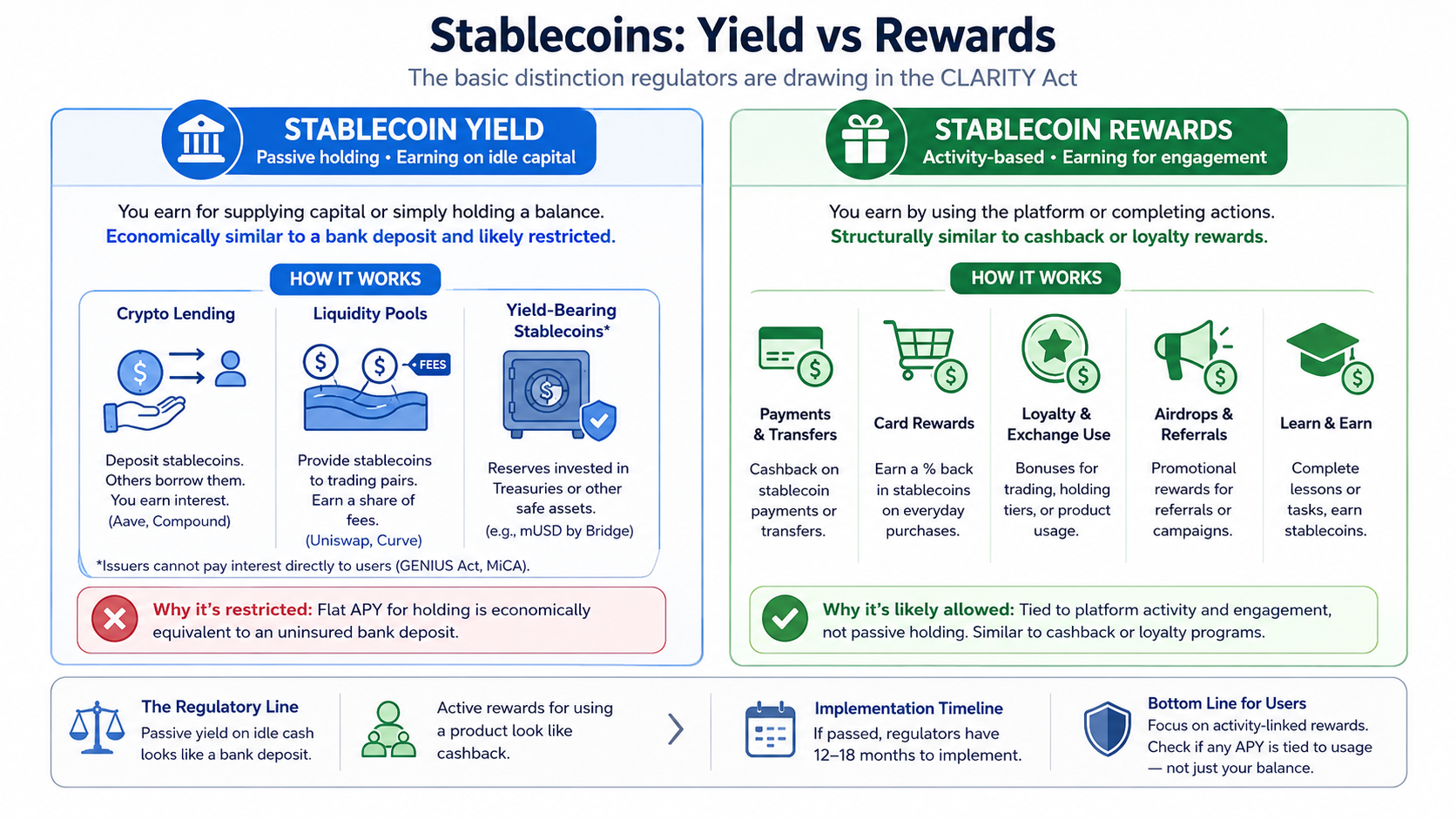

- Yield is passive. You park stablecoins, you earn interest. Think bank account, but crypto. The CLARITY Act wants to restrict this.

- Rewards are active. You do something — swipe a card, complete a course, refer a friend — and get paid in stablecoins. These are likely safe.

- The GENIUS Act already banned issuers (Tether, Circle) from paying yield. Now the CLARITY Act may extend that ban to exchanges.

- The "affiliate loophole" lets users earn yield through third-party DeFi protocols. The CLARITY Act aims to close it.

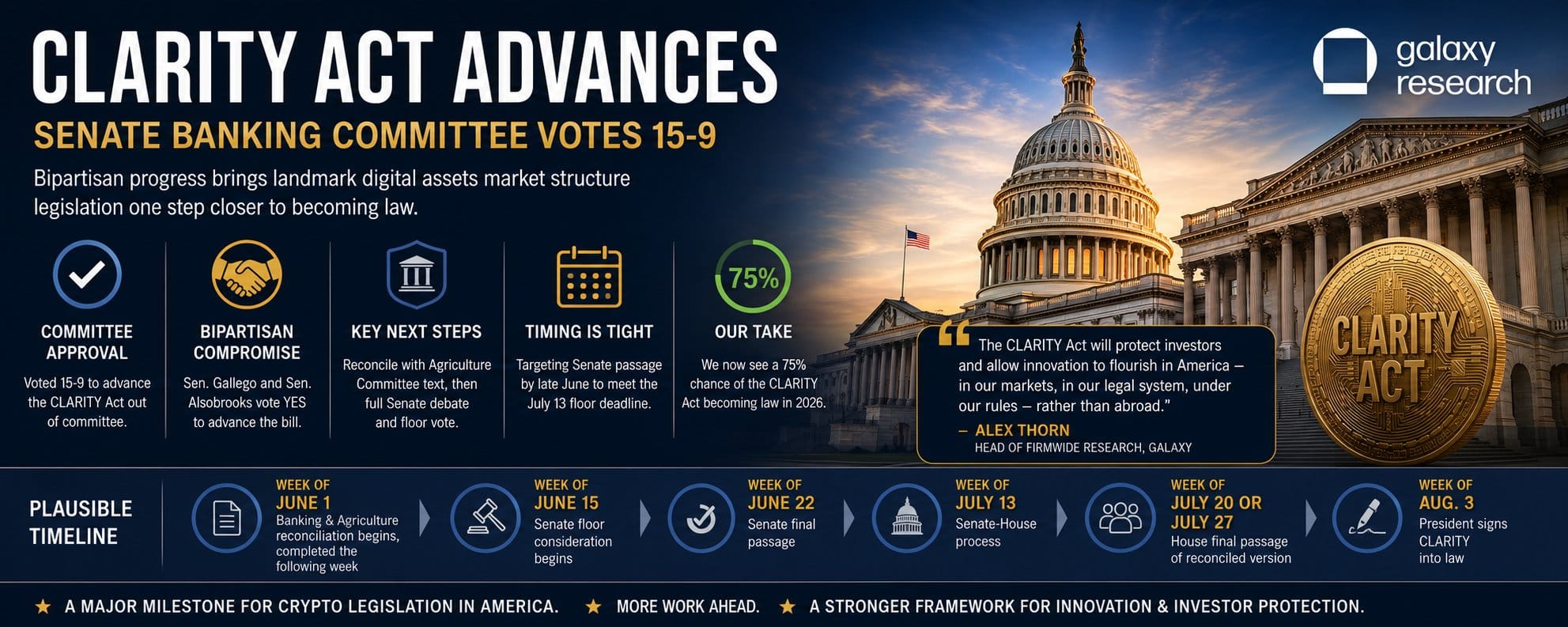

- The bill cleared the Senate Banking Committee (15–9). Final signing could come by July 4 — or slip to fall due to bank lobbying.

The problem with stablecoin payouts

Currently, users can tap into stablecoin payouts in a few ways. First, passive balances can generate yield, or interest on idle funds. The second way to earn is through activity — platforms reward specific actions like payments, transfers, or loyalty use.

In July 2025, President Trump signed the GENIUS Act — the first federal framework for stablecoins in the United States. This law bars issuers like Tether or Circle from paying interest to holders of their tokens. However, users can still earn interest by depositing stablecoins into third-party DeFi protocols or centralized crypto platforms.

Now, the proposed rules for the Digital Asset Market Clarity (CLARITY) Act may extend those restrictions to yield products on exchanges. Section 404 would prohibit Digital Asset Service Providers (DASPs) from offering yield simply for holding a stablecoin.

According to a separate compromise introduced in May 2026, rewards linked to platform activity would likely be exempt. The framework would only prohibit rewards offered "in a manner that is economically or functionally equivalent to the payment of interest or yield on an interest-bearing bank deposit."

But bank trade groups are pushing for stricter limits.

Critics argue that some exchange programs could still resemble passive yield — especially when payouts hinge on balances, account status, or loosely defined activity requirements. The boundary will eventually be defined through joint rulemaking by the SEC, CFTC, and Treasury.

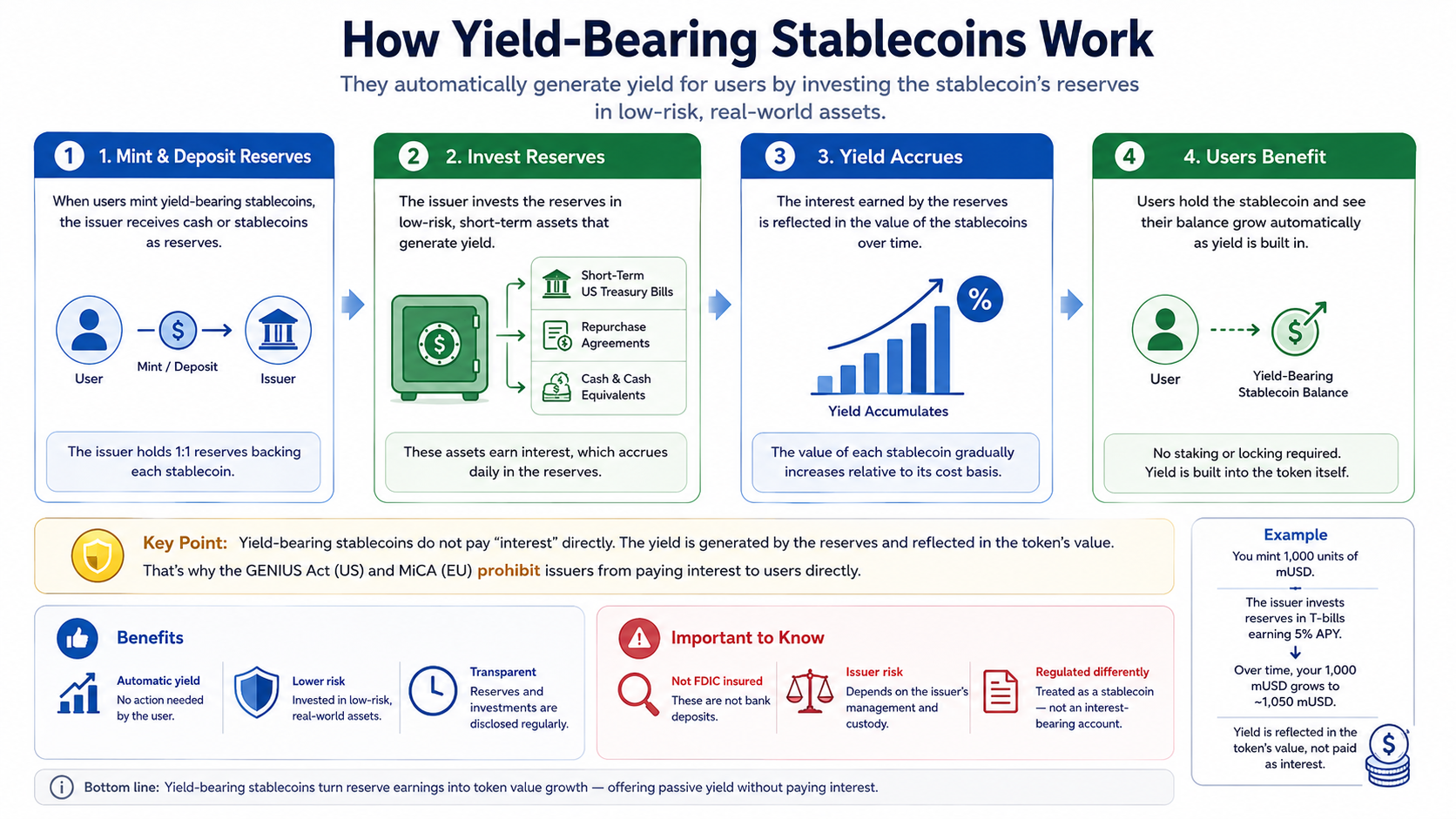

How stablecoin yield is generated

Stablecoins are designed to maintain a one-to-one peg to real-world assets, so they don't appreciate in value like Bitcoin or other cryptocurrencies. The tokens themselves don't generate interest or return, but users get compensated for providing capital to the market.

Yield is earned by depositing stablecoins into yield-generating accounts, lending protocols, or liquidity pools.

Crypto lending

DeFi protocols like Aave and Compound pay yield to users who deposit assets that are then borrowed by others. The interest paid on those loans is distributed to depositors.

Liquidity pools

Decentralized exchanges like Uniswap pay users for supplying stablecoins to trading pairs. The yield comes from a cut of the platform's transaction and swap fees.

Yield-bearing stablecoins

Some assets have yield built directly into their design. For example, mUSD issued by Bridge automatically invests its fiat reserves into short-term US Treasury bills. But the GENIUS Act in the US and MiCA in the EU explicitly ban issuers from paying interest to users directly.

A stablecoin paying passive interest is economically identical to an uninsured bank deposit. However, third-party platforms offer workarounds — yield on third-party or affiliate platforms is not directly prohibited. That's the "affiliate loophole," which the CLARITY Act seeks to close.

In bankers' eyes, platform yield products create the same deposit flight risk, just through a different structure. Banking groups argue that such rewards could pull deposits from TradFi, making loan funding harder for smaller institutions.

How stablecoin rewards work

Stablecoin rewards are tied to platform activity rather than passive holding, making them structurally closer to cashback or loyalty programs. Common examples include:

- Cashback on stablecoin payment transactions

- Bonuses for on-chain payments and transfers

- Loyalty rewards for exchange use

- Rebates tied to payment activity

- Promotional airdrops and referrals

- Learn & Earn campaign rewards

Many crypto-backed Visa or Mastercard cards (debit and credit) let users earn rewards for everyday purchases. When a card is swiped, the issuer may provide a percentage of the purchase back in crypto. With some products, holders can pick stablecoins as their reward asset.

DeFi protocols, networks, and DEXs (emerging and established) may distribute free tokens to boost adoption. Promotional airdrops incentivize users to take part in specific activities, such as referral programs. The rewards — often in USDT, USDC, or DAI — are sent directly to users' wallets.

Compared to volatile native tokens, stablecoins let airdrop organizers avoid sudden sell-offs and provide steady value to supporters.

In the case of Learn & Earn campaigns, stablecoin rewards are designed to drive engagement and attract new users to centralized platforms. Upon successfully completing a course, participants receive stablecoins (for example, 2–5 USDT) to their CEX wallets.

What this means if you hold stablecoins

For users, the bigger issue is timing and interpretation rather than immediate disruption. The proposed rules mainly focus on flat APY products that offer fixed returns simply for holding a stablecoin balance, without any meaningful usage requirements. These products are the most likely to face restructuring or removal.

Meanwhile, rewards tied to platform activity will likely remain in place and may even expand. Some platforms have already argued that users should still be able to earn rewards based on real engagement with crypto platforms rather than passive holding. In DeFi, most yield strategies also appear largely unaffected in the near term.

As rules are finalized, platforms may adjust how they present existing products, reclassifying fixed-yield offers as activity-linked rewards. In practice, the safest approach is to check whether any advertised APY is genuinely tied to usage, or simply a repackaged form of passive return.

From “hold-to-earn” to active strategies

Drawing the line between passive and active payouts is nothing new. US finance law makes a clear distinction between compensating activity and parking capital — for example, card rewards and merchant rebates are treated differently from interest payments.

If the proposed CLARITY Act restrictions become law, they could spark a tectonic shift toward compliant yield infrastructure — a positive scenario envisioned by experts like Joe Vollono, Chief Commercial Officer at STBL.

A brand new infrastructure layer might emerge, powered by AI-driven treasury, lending, and collateral tools — in ways that would eventually push banks to adapt rather than resist.

Clearer rules for issuers, exchanges, brokers, and DeFi are crucial for institutional capital to enter the market. Traditional finance firms would gain a compliance framework for developing crypto products and services in the US, while users would enjoy improved consumer protections with reduced legal risk for all parties involved.

State of CLARITY Act

At press time, the bill has cleared the Senate Banking Committee — a major roadblock — with a bipartisan 15–9 vote. It is now expected to advance through the final stages of the US legislative process.

The House originally passed the bill (H.R. 3633) with a strong bipartisan vote of 294 to 134. The Banking Committee's draft is now being merged with the Agriculture Committee's companion bill (the Digital Commodity Intermediaries Act) to create a single bill for the full Senate floor.

The White House and crypto advocates are aiming for a final presidential signing by July 4. But it could be delayed until late summer or September due to limited legislative floor time and intense pushback from the traditional banking sector.

After the bill passes, regulators would have 12 to 18 months to implement the framework.

Wrapping up

The CLARITY Act isn't trying to kill stablecoin rewards. It's trying to draw a line that's existed in traditional finance for decades: passive yield on idle cash looks like a bank deposit. Active rewards for using a product look like cashback. The former gets regulated like interest; the latter gets a pass.

Where that line lands will determine whether exchanges can keep offering yield-like products or have to push users toward third-party protocols. Either way, clearer rules are coming — and for an industry that's spent years navigating gray areas, that's not necessarily bad news.

For users who just want to earn something on their stablecoins without breaking the law, the next 18 months will finally bring some answers.