Using borrowed crypto to earn yield: Double-dip strategy

You borrow at 0% APR. You deposit the borrowed funds into a savings account earning 5% APY. You pocket the difference without deploying fresh cash.

Sounds like free money, right? Just using the system to squeeze out a little extra yield.

It's a strategy that gets tossed around in crypto forums a lot, and it does look brilliant on paper. But like most things that seem too easy, the reality is more complex.

Let's walk through how this actually works, where it can go wrong, and when it might still make sense.

TL;DR

- The idea is simple: Borrow at low or zero interest, deposit into savings, earn the spread.

- The catch is LTV. The more you borrow, the higher your LTV climbs — potentially pushing you out of the 0% APR tier.

- You need extra buffer. If you borrow $10,000 at 20% LTV, your collateral needs to be large enough to absorb that.

- Market drops hurt twice. Your collateral loses value while your loan balance stays the same.

- It works best when you borrow against stablecoins. No volatility means no surprise LTV spikes.

First, the basic math

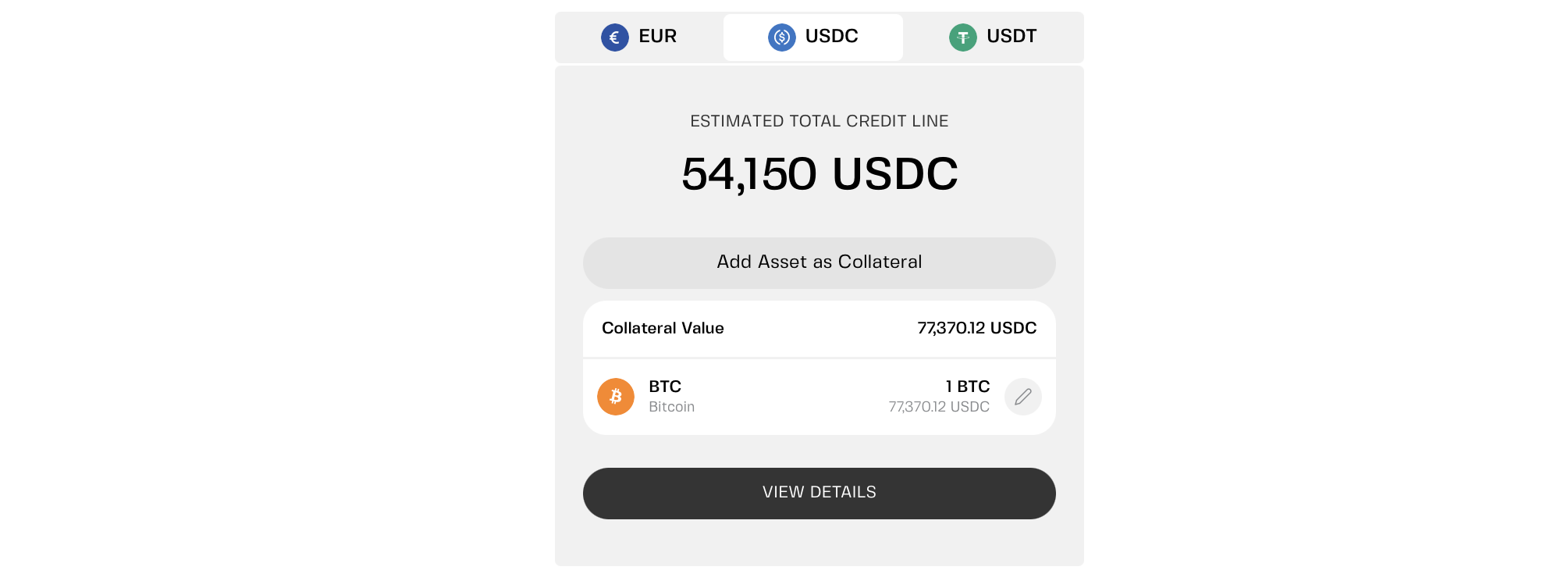

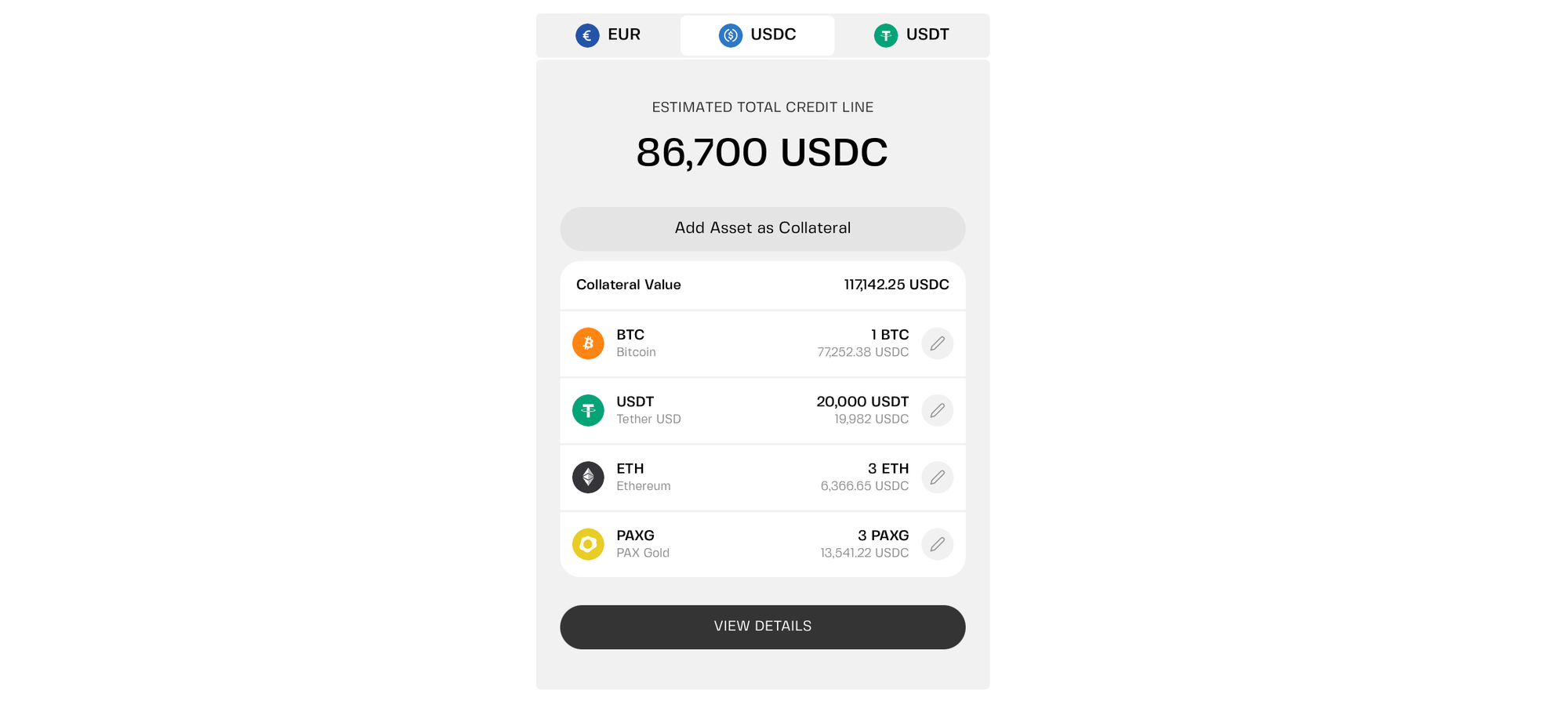

Suppose you open a loan or credit line to borrow 15,400 USDC, backed by 1 BTC as collateral ($77,370.12 at press time). Next, you deposit that amount at 8.2% APR in Fixed Savings — say, for 12 months.

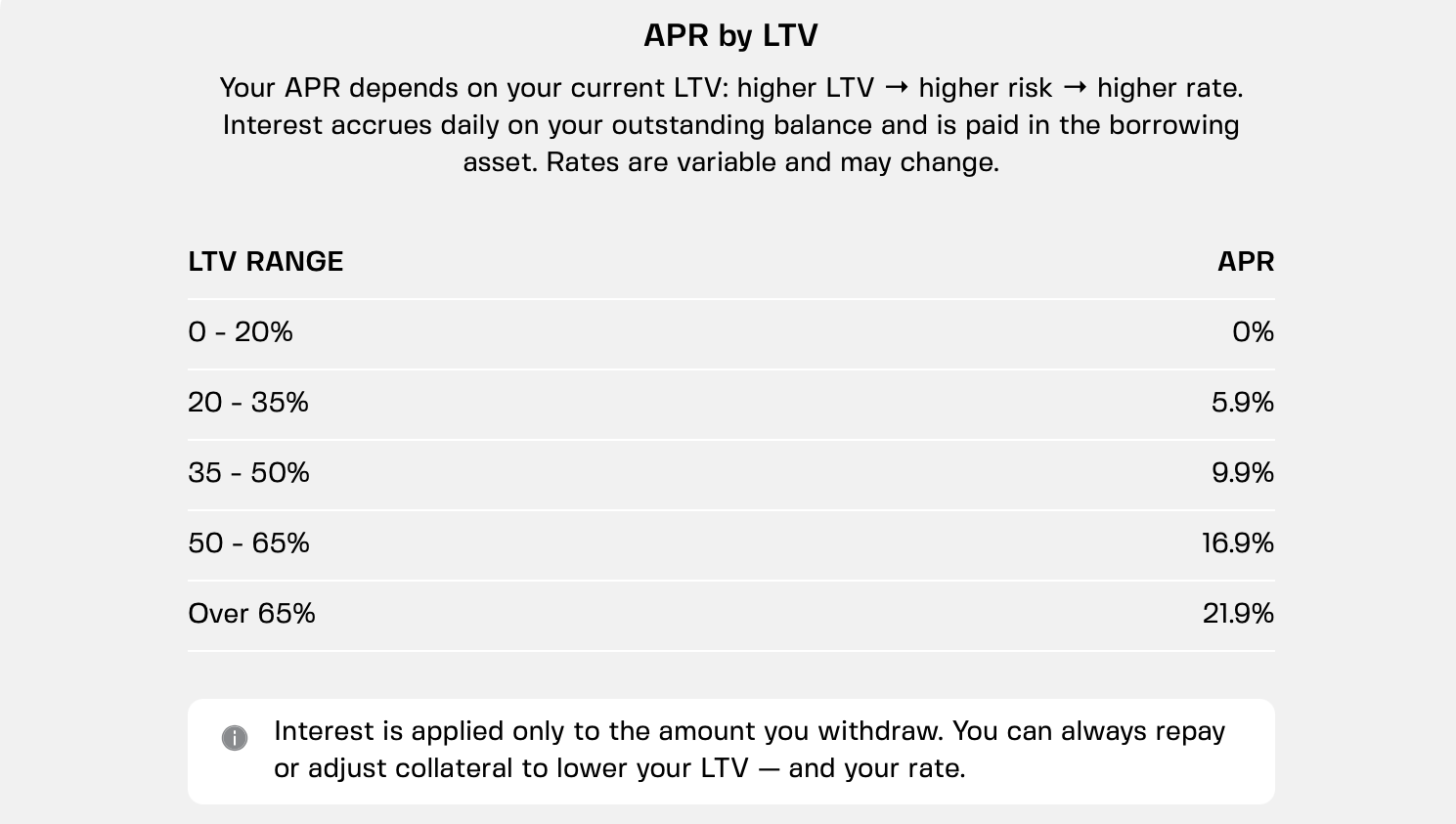

Because BTC is a volatile asset, platforms assign it a lower LTV (loan-to-value) ratio limit than stablecoins — often, 70%. You could potentially max out to $54,150, but you borrow less to keep your interest rate to zero.

Some crypto lenders offer 0% APR as long as your LTV stays below a specific threshold (e.g., 20%, depending on the platform). In our example, 15,400 USDC is just under 20% LTV.

So you borrow 15,400 USDC at 0% APR and deposit it into Fixed Savings.

- Borrowing costs: zero.

- Extra yield: 8.2% on $15,400 or about $1,262 per year.

That's the double-dip.

Where it gets messy

The math works perfectly when nothing moves. But crypto moves.

First problem: LTV creep

You borrowed $15,400 against roughly $77,300 in BTC. That's 20% LTV. Then you deposited that $15,400 back into savings.

If you borrow against a volatile asset like BTC or ETH, your LTV moves with the market.

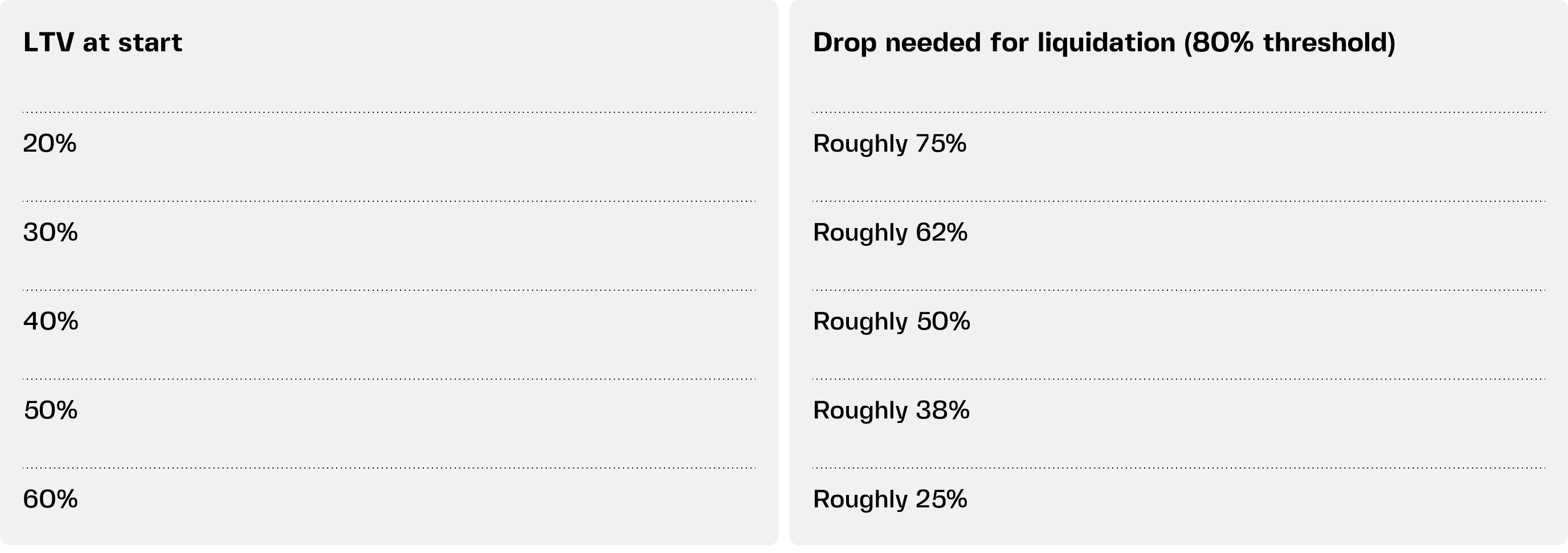

- BTC drops 50%. Your $77,300 collateral becomes $38,650. Your $15,400 loan is now nearly 40% LTV. Still safe, but closer to the edge — and you start paying interest because it crept past the zero-interest threshold.

Second problem: margin calls

If the LTV climbs high enough, you face a margin call. The platform will ask you to add more collateral or repay part of the loan.

The interest you start paying eats into your savings yield. But the bigger risk is liquidation. If you ignore the margin call and BTC keeps falling, the platform may sell your BTC to cover the loan.

Now your 1 BTC is gone. The borrowed funds themselves didn’t disappear — your 15,400 USDC is still sitting in savings, earning yield.

The real damage comes from losing the BTC collateral.

So what's the actual loss?

- You lost your BTC collateral. That 1 BTC was worth around $77,300.

- You still have $15,400 in savings plus whatever yield it earned.

- You're down roughly $61,900 — plus you missed out on any future BTC price recovery.

The double-dip becomes a double-loss because you lose your original collateral, while the yield earned on the borrowed funds is nowhere near enough to offset that loss.

Your net position is crushed. The yield on $15,400 doesn't come close to making up for losing 1 BTC.

Third problem: locked collateral

Typically, the assets you pledged as collateral stop earning yield. In the example above, your 1 BTC is locked as collateral. It′s not earning. Just the 15,400 USDC you borrowed and deposited is earning.

So your net gain isn't 8.2% on 15,400 ($1,262). It′s $1,262 minus the yield you lost on the 1 BTC that's no longer earning.

That changes the economics quite a bit.

When it actually works

The double-dip makes the most sense in specific scenarios.

Borrowing against stablecoins to earn on stablecoins. No volatility means no surprise LTV spikes. Your collateral stays stable. Your borrowed funds stay stable. Your potential profit becomes more predictable.

Using otherwise idle assets as collateral. If you have tokens that don't earn yield on their own — like certain altcoins that aren't accepted in savings — you can pledge them as collateral, borrow stablecoins, and earn yield on those. You weren't earning anything on the altcoins anyway. Now you are.

Keeping LTV very low. Borrow $5,000 against $50,000 in collateral. That's 10% LTV. Even a sharp market drop won't push you into interest-paying territory. The safety buffer is huge.

Here’s a cleaner double-dip

You hold $10,000 worth of SOL. SOL isn′t supported in savings, but it is accepted as collateral. You open a $2,000 credit line in USDC at 0% APR.

You deposit that 2,000 USDC into Fixed Savings earning 8.2% APR.

- Your SOL stays locked as collateral, but it wasn't earning yield anyway.

- Your borrowed USDC is now earning about $164 per year.

- Your borrowing costs: zero.

If SOL drops 50%, your collateral is worth $5,000. Your $2,000 loan is now 40% LTV. You're still safe, and your savings are still earning. But at this point, you start paying interest once your LTV crosses that 20% threshold.

To restore it to the zero-interest state, you need to add more collateral or swap collateral assets. Multi-collateral credit lines allow you to do this at any point — even after drawing your entire limit.

That's a cleaner double-dip. You turned idle collateral into active yield.

What Clapp makes possible

On Clapp, you can mix up to 25 different assets in your collateral pool. That means you can pledge a basket of tokens — some volatile, some stable — to smooth out your LTV.

You can also swap collateral without closing your credit line. If your SOL starts dropping, you can add USDC to your collateral pool to stabilize your LTV. Or swap some SOL for a more stable asset.

And because the credit line has no fixed repayment schedule, you can keep the strategy running as long as it makes sense. No fixed monthly payments eating into your yield.

Borrowing to earn yield is math with risks attached

The spread between borrowing costs and savings yields is real. But volatility, LTV creep, and lost yield on locked collateral can eat into your gains.

The strategy works best when you borrow against stablecoins or otherwise idle assets, keep LTV very low, and have a plan for market drops.

Double-dip carefully. Or you might double-dip into trouble.

Frequently asked questions

1. Is this strategy risk-free?

No. The main risks are LTV creep (if you borrow against volatile assets), platform risk (the lending or savings platform fails), and opportunity cost (your collateral stops earning yield). Stablecoin-to-stablecoin borrowing minimizes volatility risk but doesn't eliminate platform risk.

2. What's the ideal LTV for this strategy?

20% or below. At that level, even a sharp market drop won't push you into paying interest. Some platforms offer 0% APR at 20% LTV, which is perfect for this strategy.

3. Can I do this with a fixed-term loan instead of a credit line?

Not really. Fixed-term loans charge interest on the full amount from day one. That interest would eat into your savings yield. Credit lines with 0% APR at low LTV are the right tool for this.

4. What happens if the savings rate drops below my borrowing cost?

You close the loop. Repay the borrowed funds from your savings. The strategy stops making sense, so you stop running it. That's why you want no early repayment penalties.

5. Is this worth doing for small amounts?

The math works at any scale. On $1,000 at 5%, that’s only about $50 per year. Not life-changing, but not nothing. The habit of putting idle assets to work matters more than the dollar amount.