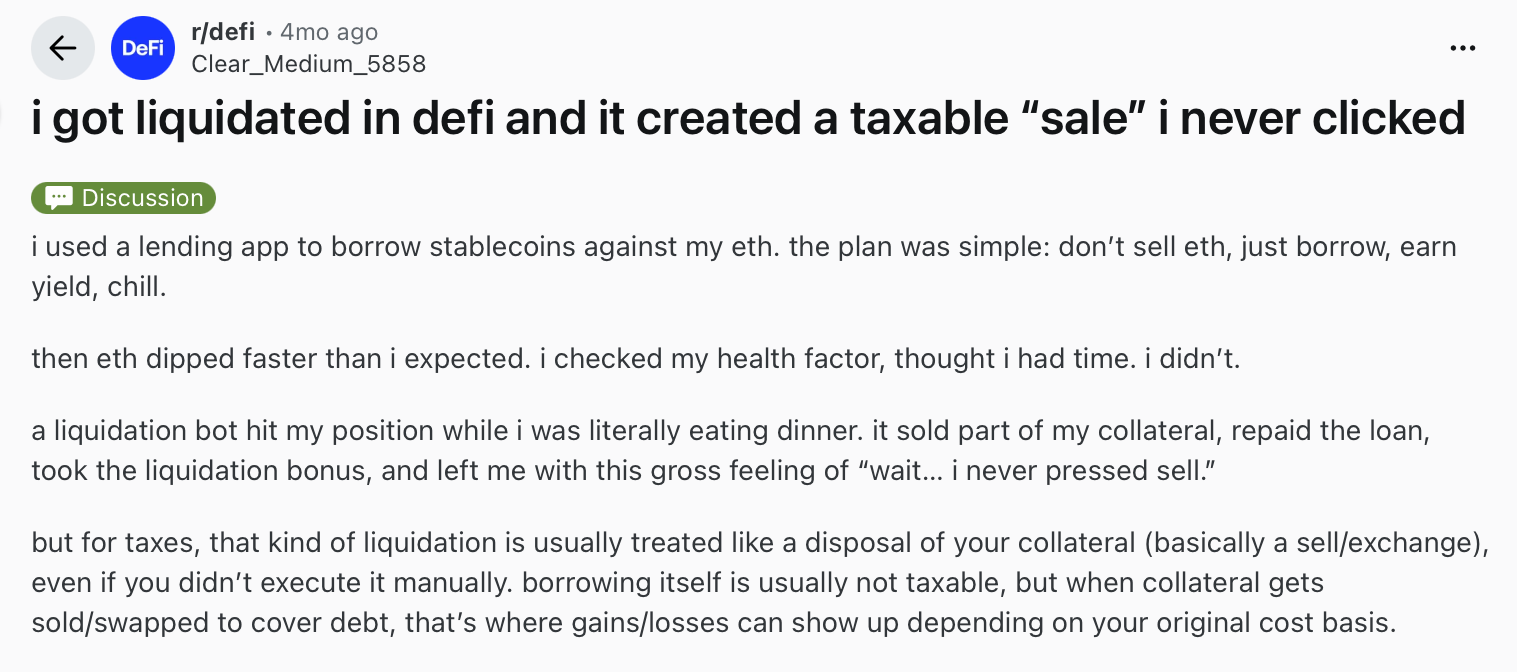

How one Reddit user lost his collateral — and how you can avoid the same mistake

"I never pressed sell."

That's what one Reddit user wrote after getting liquidated on a DeFi lending platform. They had borrowed stablecoins against their ether. The plan was simple: don't sell ETH, just borrow, earn yield, chill.

Then ETH dipped faster than expected. They checked the health factor and thought they had time — except they didn't.

A liquidation bot hit the position while they were literally eating dinner.

The bot sold part of their collateral, repaid the loan, took its liquidation bonus, and left the borrower with the sinking realization: "wait… I never pressed sell."

And for taxes, that liquidation was treated like a sale.

Let's break down what went wrong, how liquidations work, and how to avoid becoming the next cautionary Reddit post.

TL;DR

- Liquidations happen fast. A health factor that looks safe at dinner can be gone by dessert.

- In DeFi, there's no warning. No "you have 24 hours to act." Just a bot that executes instantly.

- Liquidation is a taxable event in most jurisdictions. The platform sells your collateral, and that counts as a disposal.

- Old cost basis = bigger tax hit. If you bought ETH years ago, a liquidation could trigger capital gains on paper — even if you lost money overall.

- The best liquidation is the one you avoid. Low LTV, extra collateral, and knowing your platform's rules.

What actually happened to this Reddit user

Let's reconstruct the scenario.

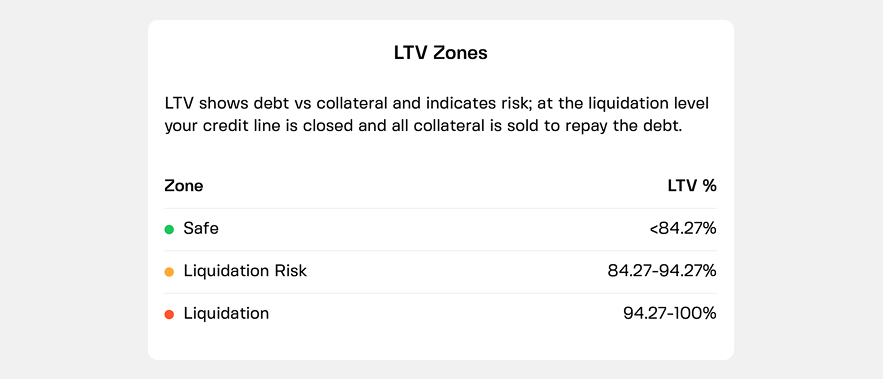

The Redditor deposited ETH as collateral and borrowed stablecoins against it. Their health factor — the DeFi equivalent of LTV (loan-to-value ratio) — looked fine, giving the false impression that there was ample time to act.

In simple terms, the lower your collateral falls relative to your loan, the worse your health factor becomes. Once it crosses a critical threshold, liquidation can happen automatically.

But ETH kept dropping. And in DeFi, there's usually no email or notification to alert you of critical drops.

Once the health factor crossed the threshold, a liquidation bot spotted the opportunity. It instantly sold a portion of the user's ETH, repaid the loan, and pocketed a liquidation bonus.

All while they were eating dinner.

There was no chance to add collateral. All the Redditor saw was a notification that their position was gone, because DeFi loans get liquidated within seconds — sometimes within a single blockchain block — by bots competing for bonuses.

Once falling collateral pushes LTV past the "liquidation threshold" (often 75-85%), the smart contract lets anyone wipe the position out.

Plus, you're hit with a penalty fee (typically 5-10%), which is deducted from your collateral to reward the bot and the protocol.

The lesson this Redditor learned was this:

"defi isn’t just swaps and yields. liquidations, auto-repayments, vault rebalances… they can create disposals whether you like it or not. i ended up running my wallet through awaken tax just to label the liquidation correctly and make sure the lots/cost basis didn’t get mangled across chains."

Why DeFi is different from CeFi

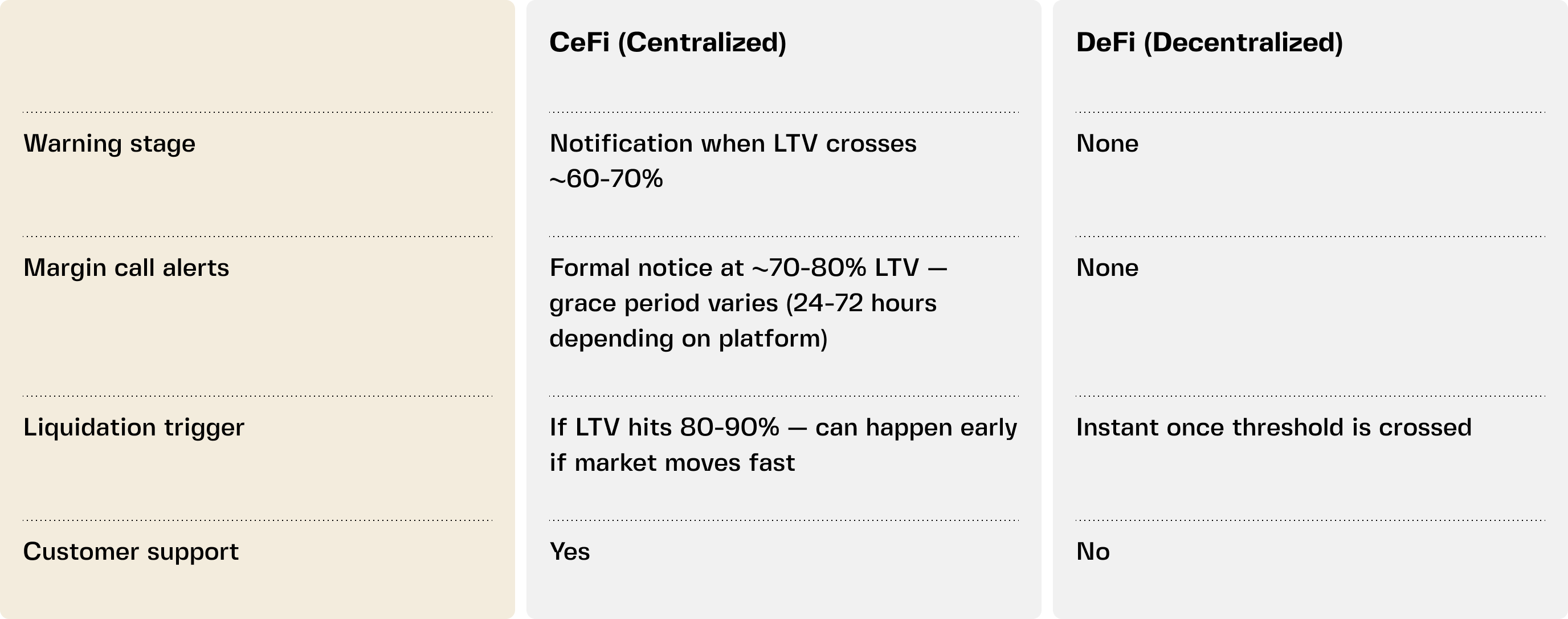

DeFi lending is run by smart contracts. CeFi platforms operate differently, though the core mechanics are similar — you borrow less than your collateral value (over-collateralization), and the loan can be liquidated if your collateral falls too far and you fail to restore a safe LTV.

However, there are also margin calls — warnings prompting you to avoid liquidation by adding more collateral or repaying part of the loan. CeFi lenders manage them off-chain, often with personalized communication and grace periods before selling assets.

This is a critical difference that catches many beginners off guard.

The CeFi process usually has two stages.

1. A warning when your LTV crosses around 60-70%. This is a heads-up — no timer, just "hey, pay attention, things are moving."

2. A margin call when LTV hits 70-80%. This comes with a formal notice and a grace period — typically 24 to 72 hours, depending on the platform. You have time to add collateral or repay.

If the market keeps falling and your LTV hits the liquidation threshold (80-90%), the platform can liquidate you early. You don't automatically get the full grace period.

DeFi skips all of it. The code doesn't warn you or care if you're at dinner — it just executes once your health factor crosses the line.

The Reddit user figured this out the hard way.

The tax nightmare

Here's where the story gets even more painful.

The Redditor didn't press sell. But for tax purposes, the liquidation was treated as a disposal of their ETH. The platform sold the collateral to cover the loan, which is a taxable event in most jurisdictions.

The cost basis was old. They had bought ETH years ago at much lower prices. So when the liquidation bot sold their ETH — even at a market low — the gain on paper looked significant.

That means losing money overall while still facing a tax bill.

Plus, the user's transaction tracker showed weird entries: "sold ETH" (even though they never clicked it), "bought stablecoin," liquidation fee legs, and sometimes duplicated entries. Sorting through the mess required running everything through crypto tax software just to label the liquidation correctly and make sure the cost basis didn't get mangled across chains.

Lesson: Liquidations aren't just about losing collateral. They can also trigger tax events you never saw coming.

How to avoid this fate

1. Know where you're borrowing

If you want warnings and time to act, stick with CeFi. If you use DeFi, understand that liquidation is instant. There's no phone call coming.

2. Keep LTV low

At 20–30% LTV, you survive most crashes. At 50%+, you're one bad night away from disaster.

3. Have extra collateral ready

Keep stablecoins in savings or more crypto on the side. When the market turns, you want options, not panic.

4. Set your own alerts

Don't rely on the platform. Set price alerts for your collateral assets. Know when you're getting close to danger before the system acts.

5. Understand your tax exposure

If you're using old cost basis assets as collateral, a liquidation could trigger capital gains. Factor that into your risk calculation.

How credit lines change the math

A traditional loan locks your collateral until you repay. A credit line gives you more flexibility.

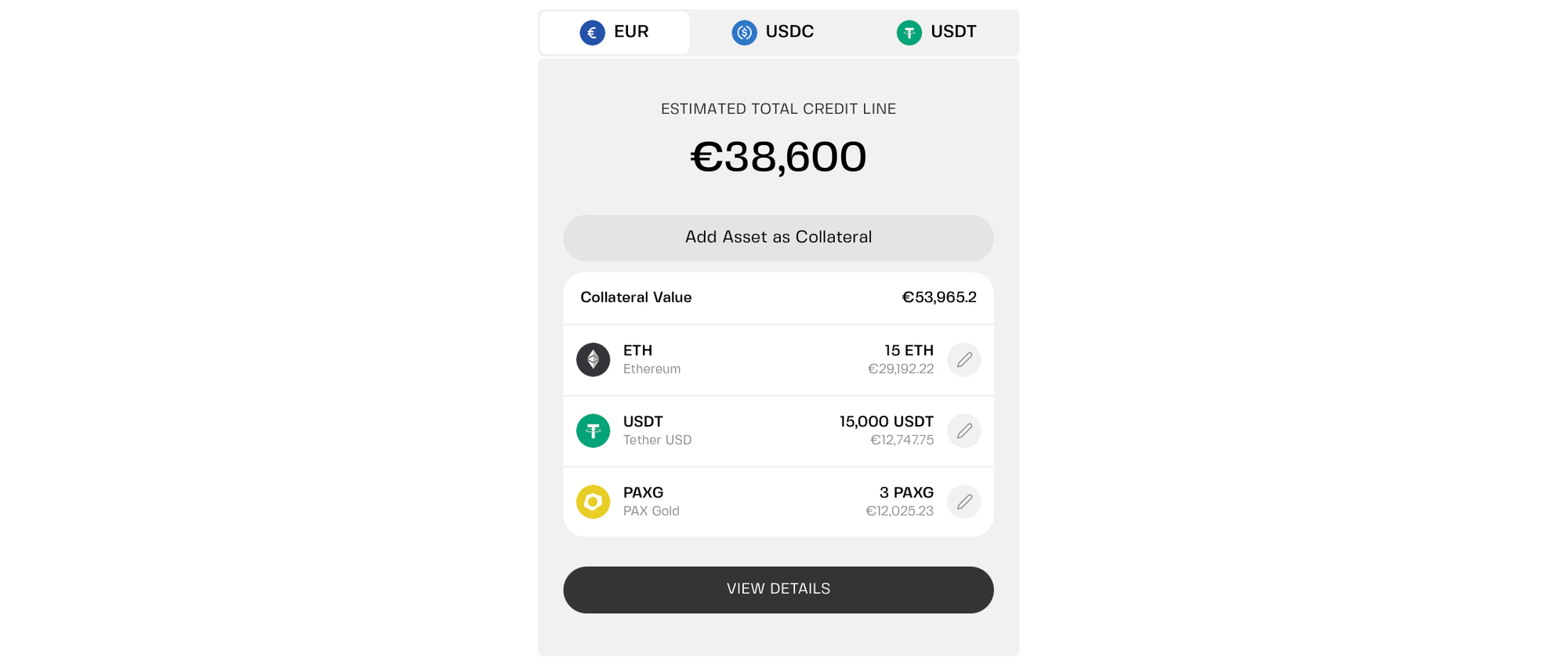

On platforms that offer multi-collateral credit lines, you can add or swap collateral without closing your position. That means when markets crash, you have tools to respond — not just a timer counting down.

Suppose your credit line is backed by a mix of volatile crypto and stablecoins — for example, ETH, USDT, and PAXG. If ETH tumbles in a downturn, adding more USDT (USD-pegged) or PAXG (gold-pegged) can restore your LTV to a healthier level — helping preserve your ETH position.

And if you keep LTV at 20% or below, platforms like Clapp even offer 0% APR. That's additional breathing room during volatile markets.

Three hard lessons

The story highlights three hard lessons for crypto borrowers.

First, DeFi doesn't wait. Liquidations happen instantly, whether you're ready or not.

Second, liquidation is a taxable event. Your collateral gets sold, and that counts as a disposal — even if you never clicked "sell."

Third, old cost basis makes the tax hit worse. What feels like a loss can look like a gain on paper.

Don't let this be your story.

Borrow conservatively. Know your platform's rules. Keep extra collateral ready. And understand that in crypto, the code doesn't care about your dinner plans.

For many first-time borrowers, platforms with built-in alerts, grace periods, and risk controls can provide more room to react when markets move fast.

Prepare for the crash before it happens, not during.

Frequently asked questions

1. Is liquidation always a taxable event?

In most jurisdictions, yes. Liquidation involves selling your collateral to repay the loan. That sale is typically treated as a disposal for tax purposes — just like if you sold voluntarily. Rules vary by country, so check local guidance.

2. Can I get liquidated in CeFi without warning?

Most CeFi platforms give 24–48 hours' notice. But if the market crashes extremely fast and your LTV hits the threshold before you act, liquidation can still happen. That's why keeping LTV low is so important.

3. What's a liquidation bot?

In DeFi, bots constantly monitor positions. When your health factor drops below the threshold, a bot can execute liquidation instantly and claim a bonus. There's no human review, no appeal, just code.

4. How do I track cost basis across liquidations?

You'll need to record the liquidation as a sale of your collateral at market price. The difference between your original cost basis and that sale price is your capital gain or loss. Crypto tax software can help label these transactions correctly.

5. Should I avoid DeFi lending altogether?

Not necessarily. DeFi lending offers benefits like self-custody and potentially higher yields. But you need to understand the risks — instant liquidation, no customer support, and tax implications. Many beginners start with CeFi for borrowing, then explore DeFi once they're comfortable.