How to make money with stablecoins, from simple to advanced

Stablecoins don’t rally or trend on crypto X. They are not speculative, and investors are parking billions in them precisely for that reason. Whether you’re holding stablecoins during a downturn or keeping dry powder on the sidelines, there are ways to make them work for you.

Stablecoins are about cash flow, preserving capital, and positioning strategically for the next big move. Let’s break down how retail holders can generate profit — realistically.

TL;DR

- Stablecoins don’t appreciate — you earn through yield, not price growth.

- You can generate returns via lending, savings products, or liquidity provision.

- Risk varies significantly between DeFi and centralized platforms.

- Capital preservation comes first; yield is secondary.

- Even 4%–8% on idle capital compounds meaningfully over time.

What stablecoins are (and aren’t)

Stablecoins are cryptocurrencies pegged to a stable real-world value — most commonly, 1 US dollar. Aside from fiat-backed tokens (USDT, USDC, etc.), there are also crypto-backed (such as DAI), algorithmic (such as AMPL), and hybrid models.

True to their name, stablecoins are designed to hold value, not grow it. Think of them as digital cash with programmable yield potential.

That means:

- You won’t profit from price appreciation.

- You can profit from yield mechanisms built around them.

Five ways to earn yield

Stablecoin holders can put their assets to work across CeFi and DeFi, choosing between intuitively familiar savings and more complex strategies.

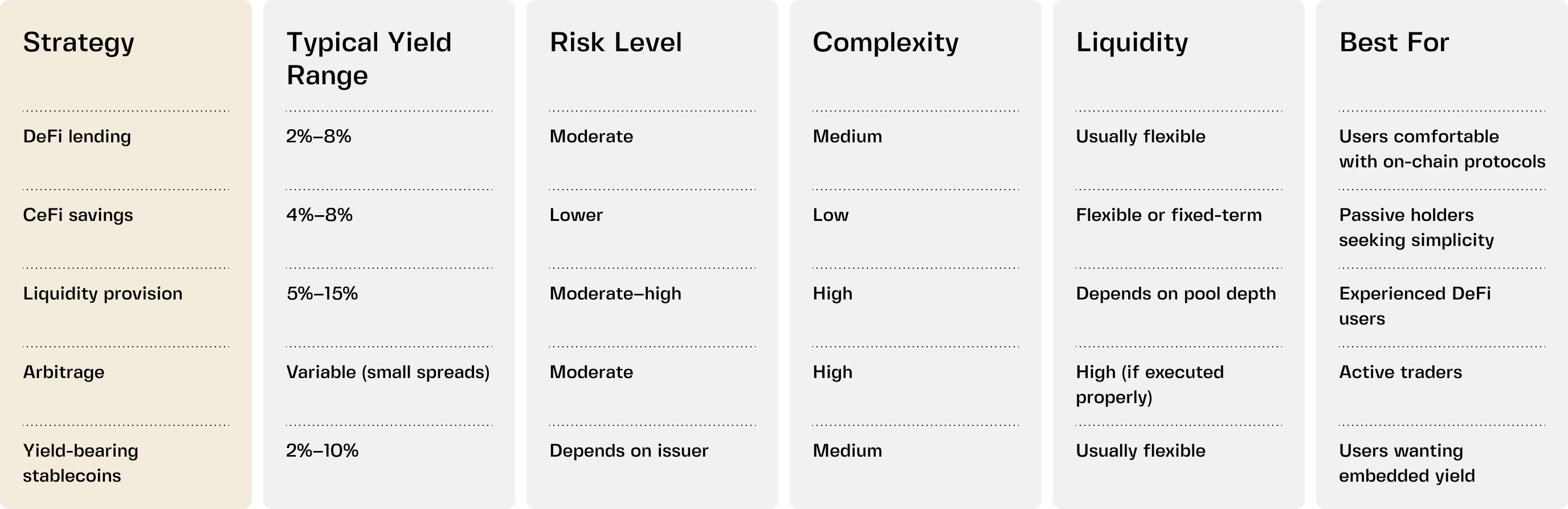

1. DeFi lending (moderate risk)

Protocols like Aave allow you to deposit stablecoins into a shared liquidity pool. Borrowers take loans and pay interest, which is then distributed to depositors.

Returns fluctuate historically between 2% and 8%, depending on demand. Higher borrowing demand = higher yields. Rates can rise significantly in bull markets and decline during bear phases.

Pros of DeFi lending:

- Transparent, on-chain

- No traditional intermediary

Risks:

- Smart contract risk

- Protocol risk

- Liquidation cascades during volatility

- No regulatory oversight

DeFi yields can look attractive, but they require understanding what you’re interacting with. The absence of consumer protections makes it hard to recover funds in case of fraud, hacks, or platform failure.

2. CeFi savings (lower risk, simple)

Structured savings products on centralized platforms (fixed or flexible) allow you to generate yield on deposited stablecoins. Behind the scenes, the provider may put your funds to work via:

- Lending strategies

- Treasury management

- Institutional liquidity provision

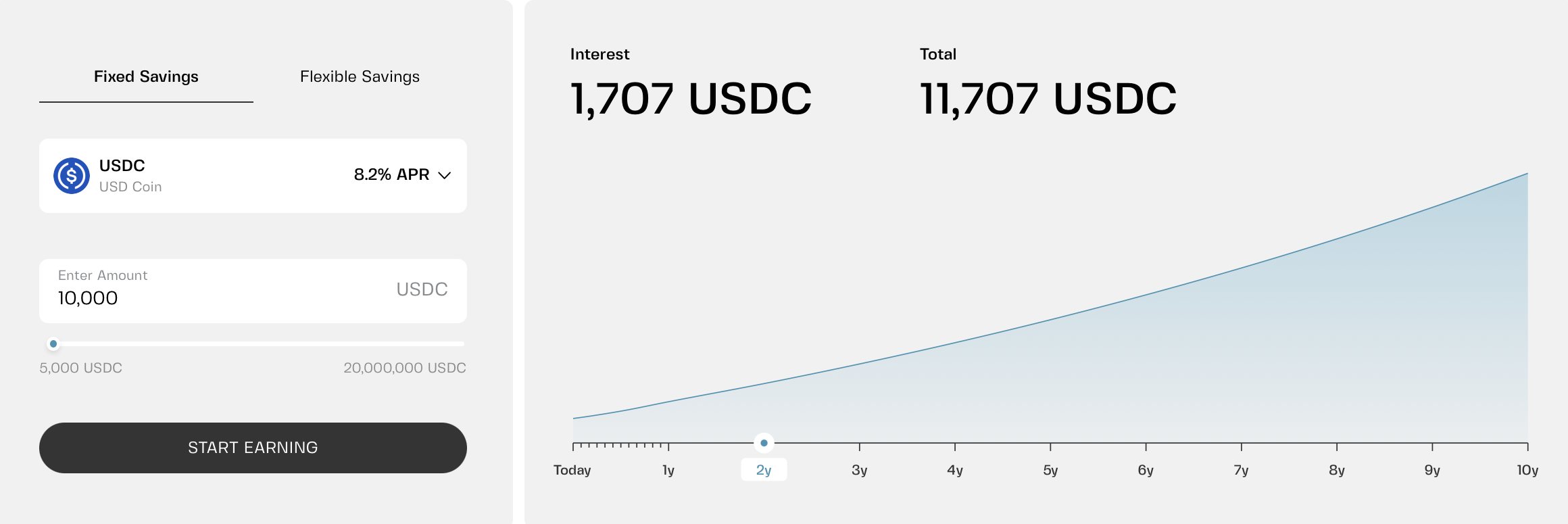

Typically, platforms may offer savings on USDT, USDC, or EUR balances. If you’re holding stablecoins anyway, earning 4%–8% annually on idle capital can meaningfully offset inflation. If the yield also includes compounding (e.g., daily), your interest earns its own interest, letting your savings grow more quickly over time.

Clapp's savings products on supported stablecoins give users a choice between premium yield for a fixed term (up to 8.2% APR) and flexible access 24/7 — as long as your assets remain on the platform, they generate returns.

Centralized platforms generally favor fiat-based stablecoins for practical reasons:

- They have performed reliably through multiple market cycles (Tether launched over a decade ago).

- Fiat-backed stables are widely accepted across CeFi and DeFi, ensuring deep liquidity to swap for other assets.

- Their reserve-backed structure is simpler and more transparent than algorithmic models.

- Issuers like Tether and Circle operate under regulatory frameworks and publish independent audits confirming their assets exceed liabilities.

In recent years, the adoption of the GENIUS Act in the US and MiCA in the EU provided much-needed clarity, establishing comprehensive legal frameworks for stablecoins.

Pros of CeFi savings:

- Simple and intuitive UX

- No need to interact with smart contracts directly

- Human customer support

This convenience comes with trade-offs: platform, counterparty, and regulatory risks. Choose licensed providers with bank-grade custody and infrastructure designed to reduce single points of failure.

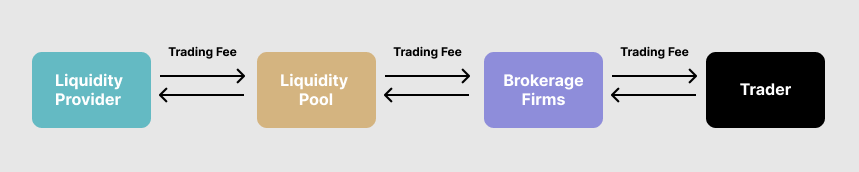

3. Providing liquidity (moderate to high risk)

You can also earn by providing stablecoins to liquidity pools used for swaps on decentralized exchanges (DEXs) such as Balancer or Uniswap.

Liquidity providers earn a share of trading fees (and sometimes governance token rewards). However, this introduces:

- Impermanent loss risk

- Market exposure (if paired with volatile assets)

- Complex mechanics

- Delayed withdrawals if the pools lack depth

While yields range historically between 5% and 15%, this strategy carries higher complexity and risk than simple lending or savings. Unless you fully understand liquidity pools, chasing yield here may not be suitable for most retail users.

4. Capturing arbitrage (moderate risk, advanced)

Occasionally, stablecoins trade slightly above or below $1 on exchanges. Traders can:

- Buy below peg

- Redeem at par

- Capture small spreads

This requires capital, speed, and low fees — not ideal for most retail users. But it shows that even assets designed to be stable can create micro-opportunities.

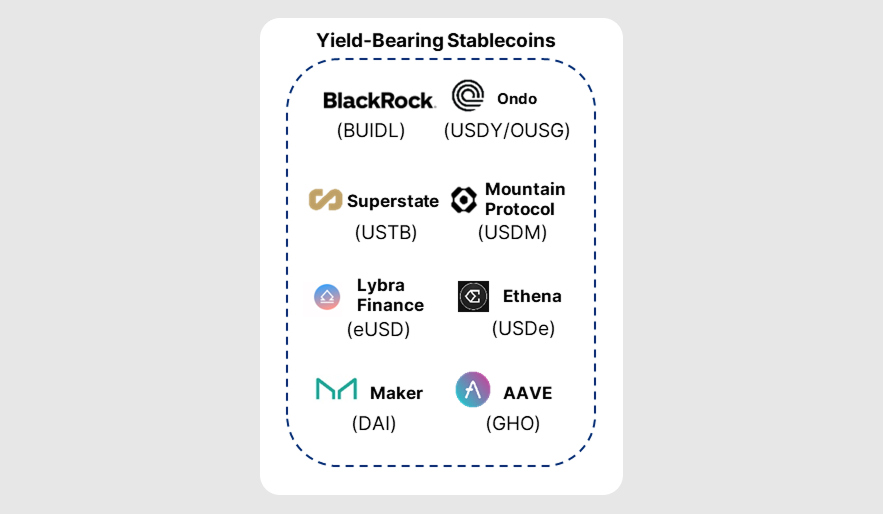

5. Yield-bearing stablecoins (risk depends on the issuer)

This specific type of digital asset has an in-built yield engine that redistributes returns from underlying assets. Common mechanisms include:

- Backing by real-world assets (RWAs) like short-term Treasury bills

- Delta-neutral strategies combining long and short positions

For example, sDAI (the yield version of DAI) represents a share in the MakerDAO yield-bearing protocol, backed by real-world assets (T-bills).

Points to monitor:

- Regulatory status — some may be classified as securities

- Issuer solvency depending on market conditions (interest rates, funding costs for short positions)

How much can you realistically earn?

If you hold $10,000 in stablecoins and earn 6% annually:

- That’s $600 per year.

- Compounded over several years, it becomes meaningful.

- During a crypto winter, that yield can offset drawdowns elsewhere.

It won’t change your life overnight, but disciplined yield on idle capital is one of the most underrated strategies in crypto.

The golden rule: stability first, yield second

The biggest mistake retail investors make is chasing yield without evaluating risk. Ask:

- How is the yield generated?

- Who is the counterparty?

- What happens if the platform fails?

- Is the yield fixed or variable?

- What is the liquidity lockup?

Stablecoins are often used as a safety buffer. Don’t turn your safety net into your biggest risk exposure.

When should you earn yield on stablecoins?

Stablecoin yield strategies are especially useful when:

- You’re waiting for entry opportunities.

- Markets are highly volatile.

- You want dry powder but not dead capital.

- You want predictable cash flow instead of speculation.

They’re less useful if:

- You need immediate liquidity (unless you deposit to flexible savings).

- You can’t tolerate platform risk.

- You don’t understand how the yield is generated.

Final thought

In a volatile market, boring can be brilliant. If you treat stablecoins as productive cash — not speculative assets — they can quietly improve your overall portfolio performance. Sometimes surviving and compounding beats chasing the next 10x.

Frequently asked questions

Can stablecoins make you rich?

Not through appreciation. Stablecoins generate steady, moderate returns — not explosive growth.

Is stablecoin yield safe?

It depends entirely on the mechanism. DeFi carries smart contract risk. Centralized platforms carry counterparty risk. There is no risk-free yield.

What’s a reasonable return to expect?

In normal market conditions, 4%–8% annually is common across various products. Anything significantly higher should raise questions.

Are stablecoins better than holding fiat?

They can be more flexible and programmable, especially if you’re active in crypto. But they are not insured bank deposits and should be treated differently.

Which strategy is the safest?

Generally, CeFi stablecoin savings on reputable, regulated platforms carry the lowest risk for retail users. They offer predictable yields, bank-grade custody, and human customer support. DeFi lending and liquidity provision can be more lucrative but involve higher complexity and smart contract risks.