How to turn your crypto into a passive income machine

Did you buy crypto just to wait for the price to rise? Digital assets don’t have to sit idle — they can generate steady returns even while you hold them. No selling required, no matter how the charts move.

Passive income strategies keep you in the game for potential gains while earning extra along the way. Used wisely, they can help your portfolio grow even during slower or sideways periods.

TL;DR

- Crypto passive income turns your holdings into productive assets.

- Popular methods include staking, lending, crypto savings accounts, and liquidity provision.

- Annual yields can range from around 3% to over 15%, depending on strategy and risk appetite.

- Some options require technical knowledge, while others work like turnkey savings accounts.

- Risk matters — higher yield usually comes with higher stakes.

Top 5 benefits of earning passive income with crypto

Instead of letting your crypto sit dormant, put it to work and watch it generate value daily.

- Competitive rates. Earn annual interest or rewards that may far outpace traditional bank deposits, meaningfully growing your portfolio over time.

- Compounding returns. Even modest annual yields can snowball impressively over the years — especially if you reinvest through multiple market cycles.

- Diversified income streams. Create a steady second source of returns beyond price appreciation. Stablecoins, for instance, can earn risk-adjusted yield while staying liquid.

- Keep exposure to future upside. You don’t miss out if prices climb — earn yield while holding on. Staking adds extra tokens, and lending generates interest without selling.

- Support blockchain ecosystems. Staking secures networks, and liquidity provision smooths DeFi markets. It’s a win-win: earn rewards while strengthening the system.

Control and flexibility

Platforms like Clapp give you full control: switch between fixed and flexible accounts, manage multiple assets, and withdraw whenever you need. You set the pace — how much to commit, when to reinvest, and how fast your capital grows.

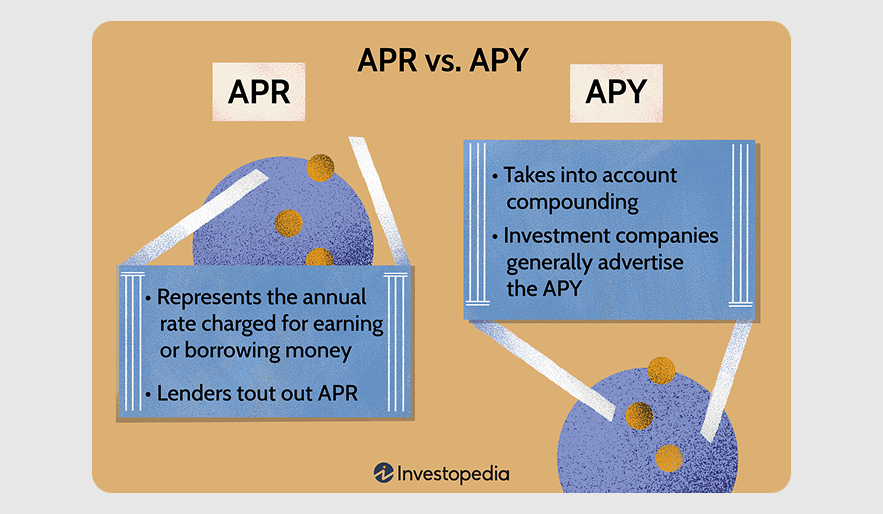

Measuring passive income: APR vs. APY

Several strategies allow investors to earn yield on their crypto holdings. Each comes with its own risk level, technical complexity, and potential returns.

Yields are usually expressed as APR or APY:

- APR (Annual Percentage Rate) shows simple yearly return without compounding.

- APY (Annual Percentage Yield) reflects compound interest: rewards are periodically added to the balance and begin generating additional returns themselves. This makes your crypto work harder over time.

Because of compounding, APY will usually appear slightly higher than APR for the same nominal rate.

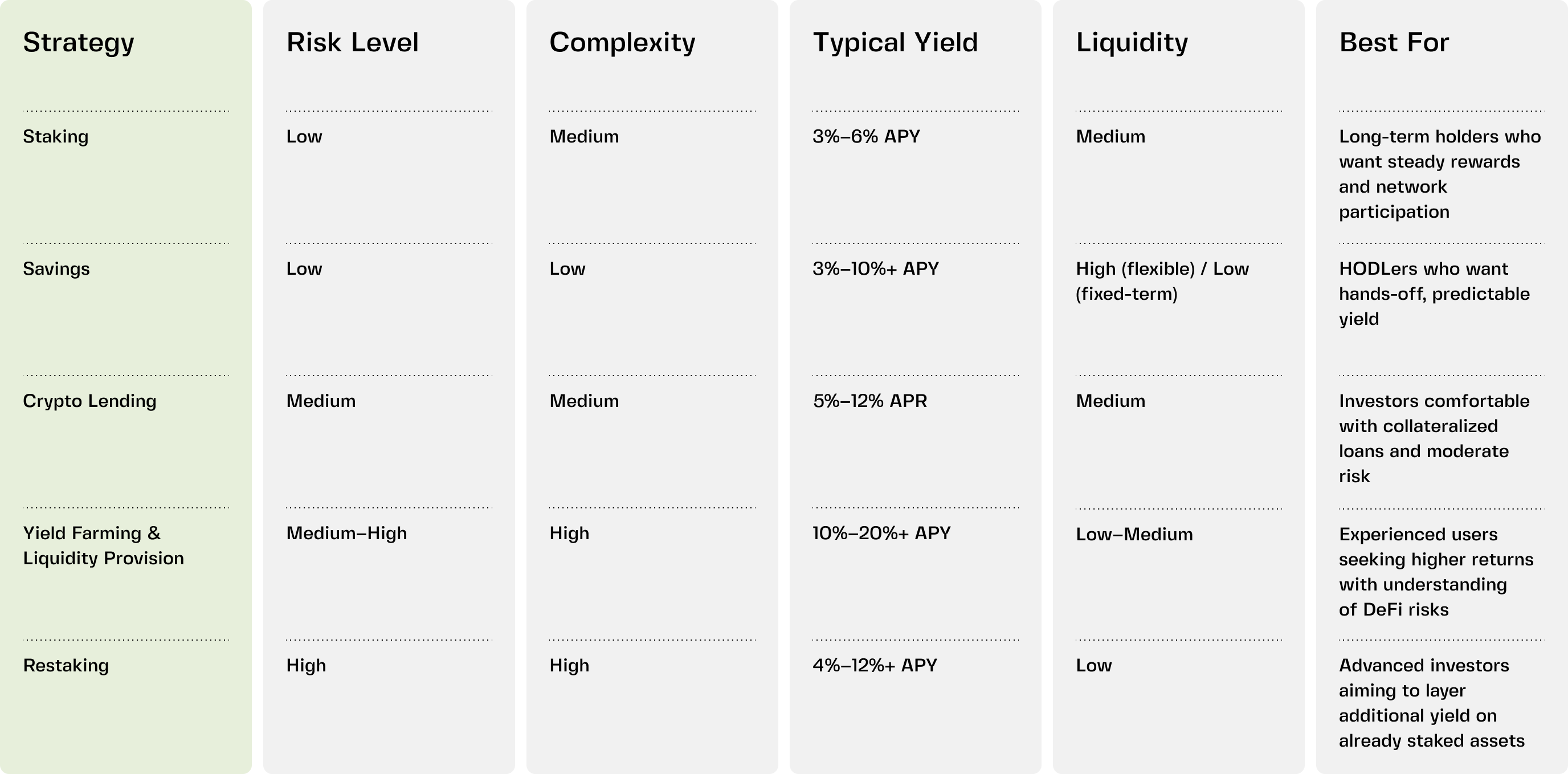

#1 Staking (relatively low risk, average complexity)

Proof-of-Stake blockchains like Ethereum, Solana, and Cardano rely on participants who lock tokens to validate transactions and keep the network secure. In return, they earn rewards.

Delegating tokens to a validator or staking pool can earn periodic rewards in the native token. Typical staking yields range from 3% to 6% annually, depending on the network and validator performance.

Staking forms:

- Running your own validator node

- Delegating tokens through staking pools

- Staking via exchanges or custodial platforms

For long-term holders of major coins, staking offers a reliable way to generate extra returns without selling.

#2 Crypto savings (relatively low risk, simple)

The easiest way in, crypto savings accounts suit holders who want hands-off yield without touching complex DeFi protocols. Deposit assets, and the platform generates returns — typically through lending or other mechanisms.

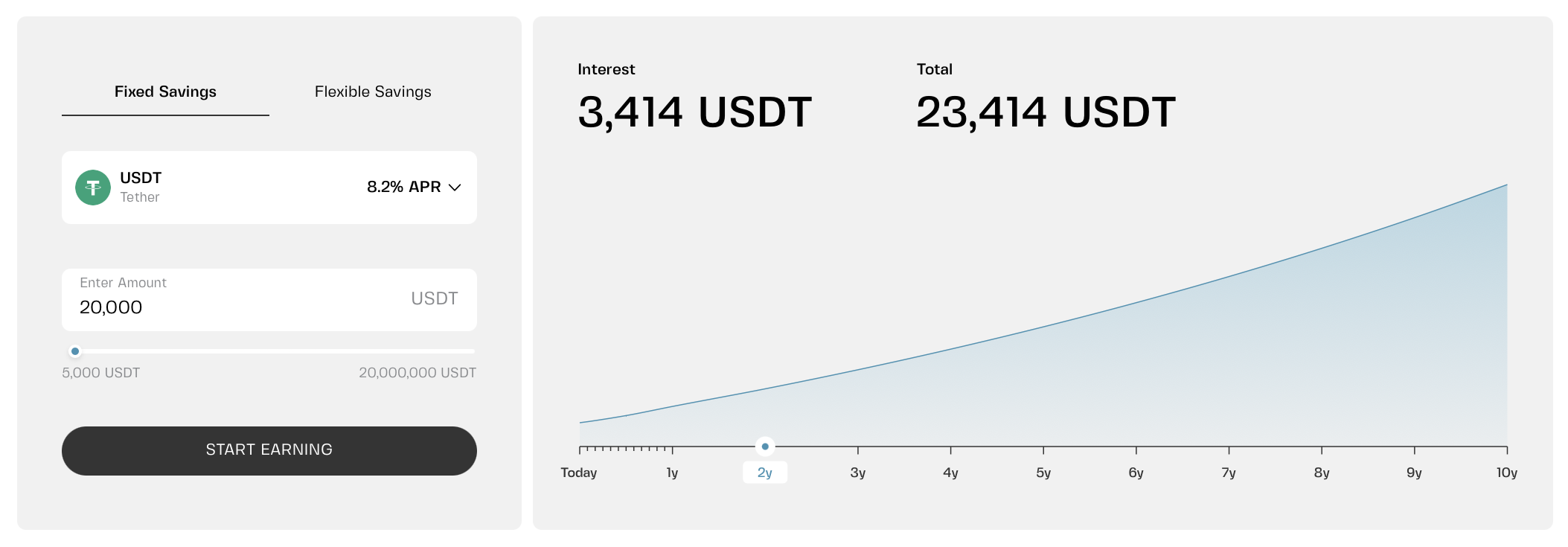

Returns usually range from 3% to 10%+, varying by asset and market conditions. Many platforms, including Clapp, offer two options: flexible products with continuous compounding and fixed-term deposits with higher potential yields.

Flexible savings — instant access, daily compounding

Flexible products keep your capital accessible: you can withdraw it anytime (partially or fully) while still earning interest that compounds daily. For example, Clapp’s 5.2% APY reflects daily compounding, where your rewards immediately start earning more rewards.

Fixed-term savings — premium yield for commitment

Alternatively, lock your assets for a defined period in exchange for higher rates, such as 8.2% APR on select fiat and stablecoins via Clapp. This is ideal for holders who plan to stay invested for months.

#3 Crypto lending (risk and complexity vary)

Earn interest by lending assets to borrowers, who may use them for trading, liquidity provision, or leveraged strategies. This works across DeFi and CeFi:

- DeFi lending: Smart contracts on platforms like Aave or Compound automate lending and borrowing.

- Centralized lending: Platforms manage lending for you, providing a simpler, more accessible experience.

Loans are typically over-collateralized to protect lenders. Crypto’s volatility means collateral value must always exceed borrowed amounts. Typical lending yields for stablecoins range from 5% to 12% annually.

#4 Yield farming and liquidity provision (moderate risk, advanced)

Yield farming means providing liquidity to DeFi platforms or decentralized exchanges in return for trading fees, reward tokens, and other incentives. Platforms include Uniswap and PancakeSwap.

Participants earn a share of trading fees, extra reward tokens, and protocol incentives. Yields can sometimes reach 10–20%+, but risks include impermanent loss, smart contract vulnerabilities, and token price swings.

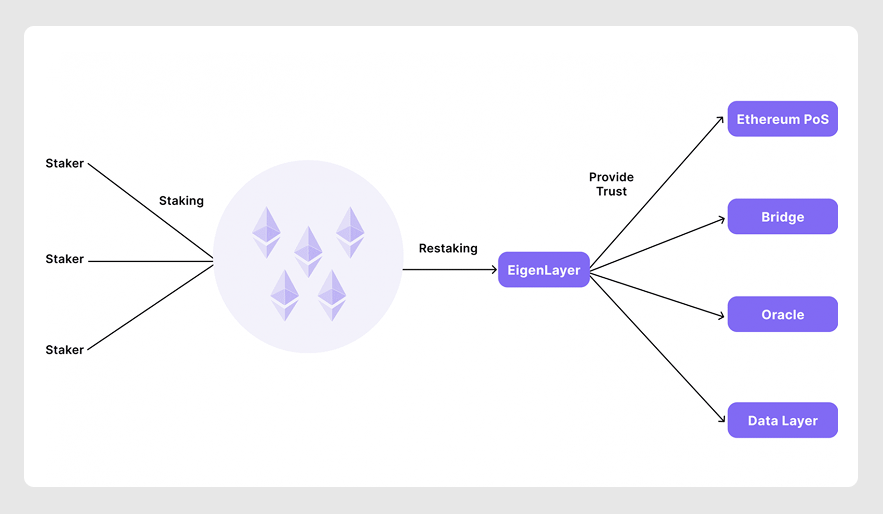

#5 Restaking (higher risk, complex)

Restaking reuses already staked assets to secure additional protocols or applications. For example, Ethereum-based systems let staked assets support multiple services simultaneously.

Rewards range from 4% to 12%+, though complexity and risk are higher. Experienced investors may find this a compelling way to layer additional yield.

Pros and cons to weigh

Passive income strategies are powerful, but come with trade-offs between return, liquidity, and security.

Risk vs. return — Higher yields usually mean higher risk. Double-digit returns often involve complex protocols or volatile tokens, while staking or savings accounts typically offer more predictable, stable returns.

Market volatility — Even with yield, the underlying asset may fluctuate. A token generating 5% yield could still lose value if prices drop sharply. Diversification is crucial.

Security and platform reliability — Where you deposit matters. Avoid platforms prone to smart contract bugs or poor management. Look for transparent, reputable providers with bank-grade security, regular audits, and multi-party computation (MPC) protection.

From sitting idle to earning daily

When used thoughtfully, passive income strategies can transform a static crypto portfolio into a steadily compounding engine of growth. From staking to lending and savings products, opportunities continue to expand.

Balance is key: pursue sustainable yields, understand risks, and choose platforms that prioritize security, transparency, and reliability.

Frequently asked questions

1. What is the safest crypto passive income strategy?

Generally, staking major PoS assets or using reputable crypto savings platforms is lower risk than advanced DeFi strategies. These provide steady yields without excessive technical or market risk.

2. How much passive income can you earn with crypto?

Returns vary widely depending on the strategy and asset. Staking major networks often generates 3–6% annually, while lending or savings products may reach 5–10%. More advanced strategies like liquidity provision can exceed these levels — with higher risks.

3. Do I need technical knowledge to earn passive income in crypto?

Not always. Staking via exchanges or depositing into savings accounts requires minimal setup. More advanced strategies like DeFi lending or yield farming demand understanding of wallets, smart contracts, and liquidity pools.

4. Can I lose money with crypto yield strategies?

Yes. While passive income can increase returns, risks still exist. Market volatility, smart contract vulnerabilities, or platform failures could result in losses. Diversifying strategies and choosing reputable platforms can help reduce risk.

5. Are crypto passive income earnings taxable?

In many jurisdictions, rewards from staking, lending, or interest accounts are considered taxable income when received. Tax rules vary by country, so consult a tax professional before large transactions.

6. Are flexible or fixed savings better?

They serve different purposes. Flexible accounts offer instant access and daily yield, suitable for liquidity management. Fixed-term accounts lock funds but pay higher rates, rewarding commitment.