HYPE ETF wave: What investors are really buying

It's been a rough patch for crypto so far this year, with Bitcoin dipping more than 50% from its all-time high and majors tumbling in unison. But Hyperliquid has not buckled to the sell-off — and ETF demand is a big reason for its resilience.

Here's a look at the recently launched HYPE ETFs and the regulated, brokerage-accessible exposure they provide. But what’s driving the hype, and how close are these products to the real thing under the hood?

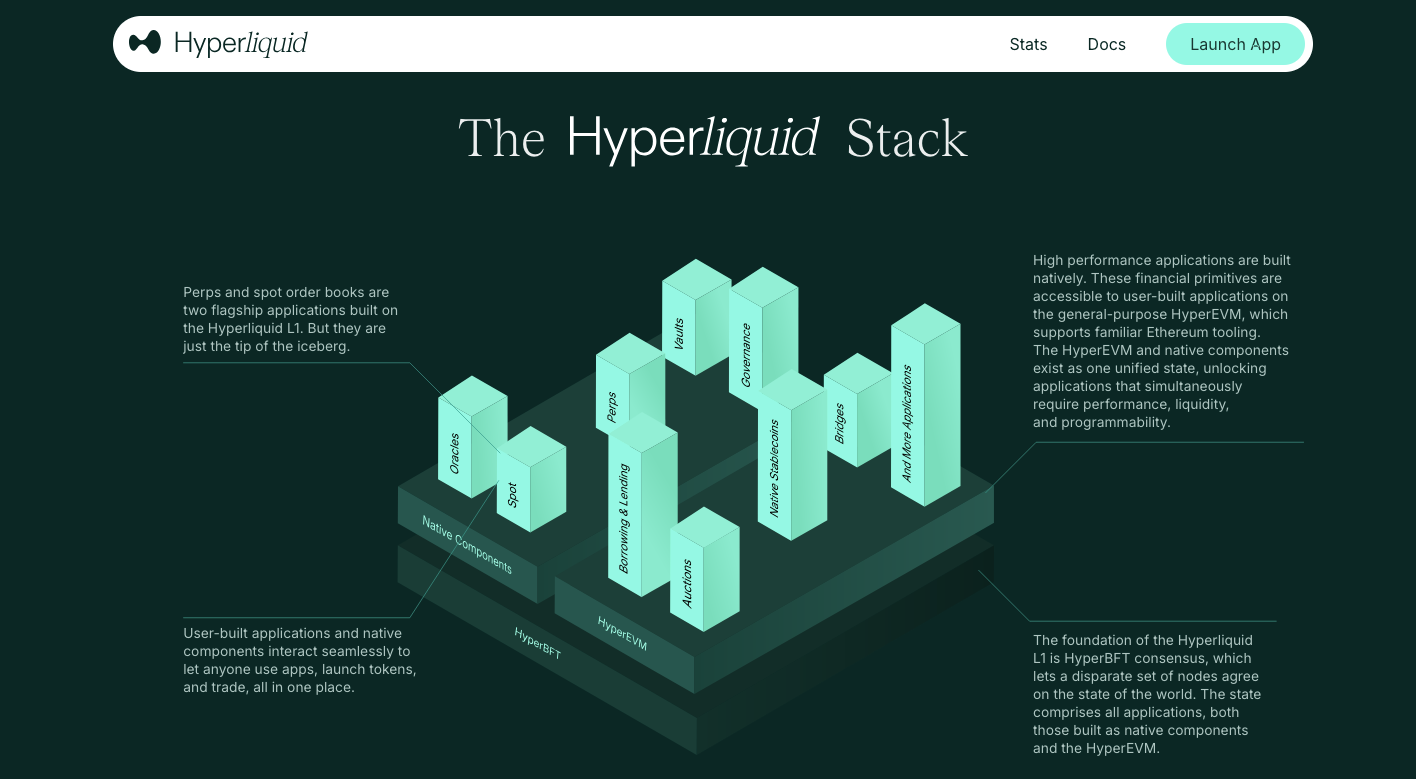

What Is Hyperliquid?

Hyperliquid is a Layer-1 proof-of-stake blockchain and decentralized exchange built for ultra-fast execution (around 200,000 orders per second) and leveraged trading. In essence, it aims to bring the strengths of centralized exchanges — deep liquidity and no KYC — to the world of DeFi, adding self-custody, transparency, and permissionless access.

It gives users the best of both worlds, complete with zero gas fees for trading. Here's how the team defines it:

"Hyperliquid is a performant blockchain built with the vision of a fully onchain open financial system. Liquidity, user applications, and trading activity synergize on a unified platform that will ultimately house all of finance."

The entire architecture helps it punch above its weight compared to other DEXs. While most rely on off-chain matching engines or external oracles, Hyperliquid operates a fully on-chain, real-time order book that minimizes latency and eliminates counterparty risks.

The exchange's flagship products are perpetual futures and spot markets, including synthetic exposure to stocks and commodities. Currently, the blockchain commands around 60% of all global on-chain derivative open interest, towering over most rivals. In 2025, Hyperliquid processed $2.95 trillion in trading volume, up over 400% year-over-year.

What Is HYPE?

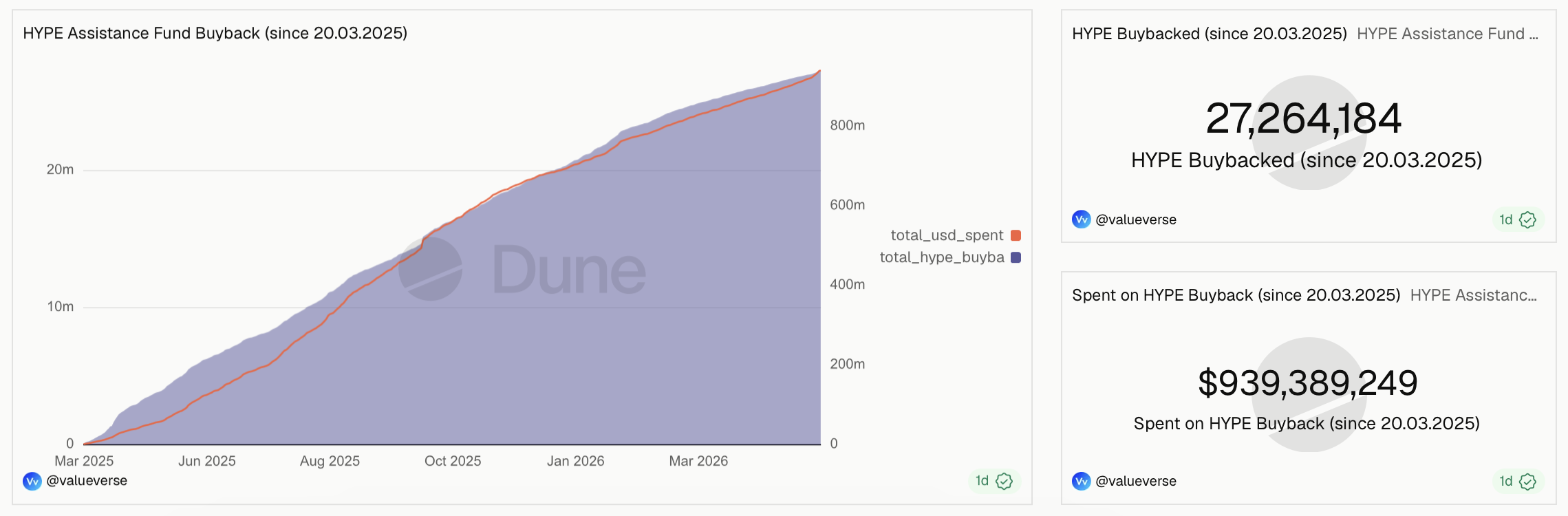

The native token, HYPE, is used for paying transaction fees across the broader ecosystem and for securing the network through staking. Roughly 97% to 99% of all fees from protocol activity flow into the Assistance Fund, which continuously buys HYPE on the open market.

Those buybacks create a direct link between protocol activity and token demand — turning trading activity into a constant source of buying pressure. So far, this stabilizing bid has approached $1 billion. Revenue feeds directly into token value rather than team profits, and the protocol also frequently burns tens of millions of HYPE to reduce the circulating supply.

This mechanism is often compared to corporate share buybacks. It creates a persistent source of demand that may help cushion periods of market weakness.

Furthermore, Hyperliquid allocated over 76% of the token supply to the community, a rarity in a sector often dominated by insiders and early investors. Since the founders turned down venture funding, there are no VC unlock schedules waiting to exert selling pressure.

Another core design choice is the absence of large-scale token emissions designed to subsidize user activity. Instead, the platform relies on execution quality, deep liquidity, zero-fee trading, and self-funded tokenomics to attract users.

In short, supporters argue that Hyperliquid's edge lies in its market position, transparent buyback structure, and community-heavy token distribution — a combination that has fueled one of crypto's strongest narratives this cycle.

How do Hyperliquid ETFs work?

Like any crypto ETF, products linked to the Hyperliquid token offer indirect exposure without holding a wallet or using a crypto exchange. Instead, investors purchase fund shares that trade on a traditional stock exchange like Nasdaq.

These shares track the HYPE price, minus fees, expenses and liabilities, using different benchmarks (for example, the FTSE Hyperliquid Index for THYP). The funds available today passively capture both price appreciation and any generated yield — committing a portion of the tokens to professional validator nodes that help secure the Hyperliquid network.

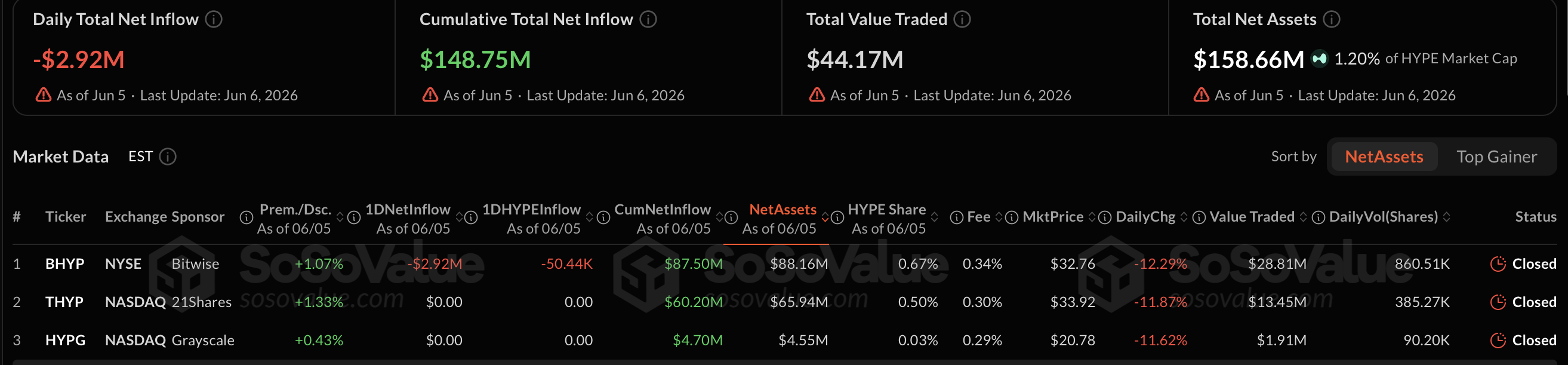

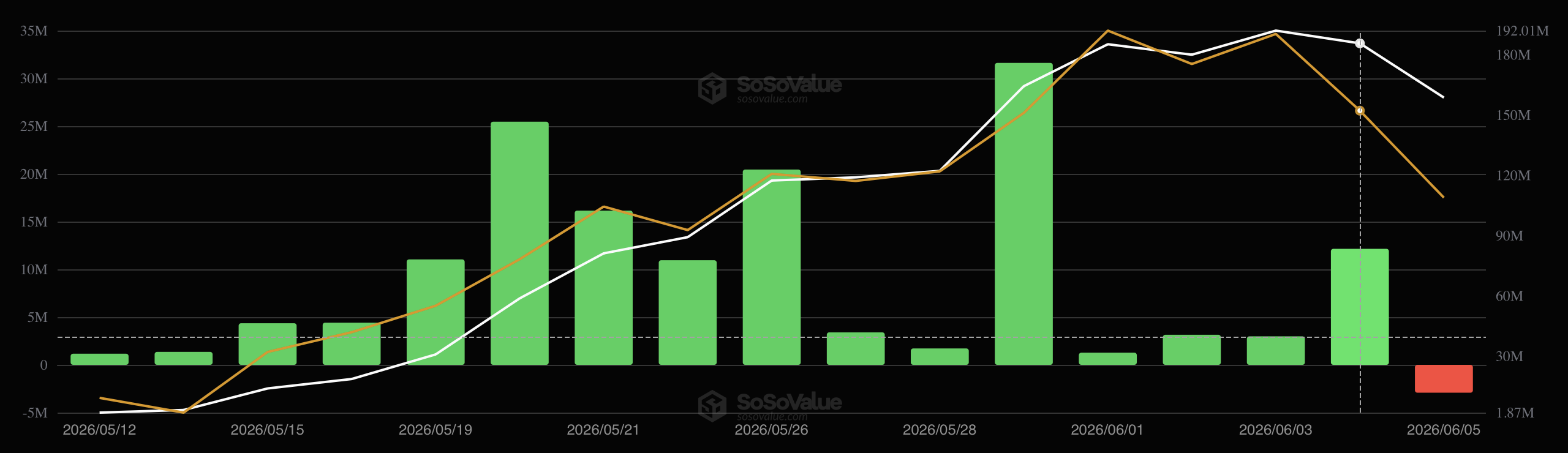

When those nodes earn rewards, the proceeds flow back to the ETF trust and are reflected in the fund’s Net Asset Value (NAV). Three products have been launched as of June 7, 2026, all in the US:

- THYP by 21Shares (Nasdaq; AUM: $87.5 million). The first to market (May 12, 2026). It has roughly 65% of its assets staked via Anchorage Digital Bank and BitGo (delegated staking with a 30% fee). Expense ratio: 0.30%

- BHYP by Bitwise (NYSE; AUM roughly $60 million). It handles staking in-house through Bitwise's proprietary on-chain infrastructure and adds realised rewards to the ETP daily. Debuted three days after THYP. Expense ratio: 0. 34% (0% for the first month).

- HYPG by Grayscale (Nasdaq; AUM $4.7 million). Released on June 3, 2026, it is seen as the opening shot in an issuer fee war. Offers a higher staking yield and the lowest expense ratio (0. 29%) compared to the other two products. At press time, roughly 54.55% of the tokens are staked.

These funds are essentially different wrappers for the same underlying asset, competing on fees, staking yields, and execution rather than exposure itself. They do not carry the same regulatory protections as conventional ETFs or mutual funds. All three are registered under the Securities Act of 1933.

One important caveat: ETF shares do not always trade exactly at the value of the underlying HYPE holdings. This happens because during periods of high demand or low liquidity, these funds can trade at a premium or discount to their net asset value (NAV).

ETFs vs. HYPE: What you actually get

Holding ETF shares does not give the same level of control as holding HYPE directly in a wallet. Access to the protocol's on-chain functionality is also unavailable through ETF ownership. Here's how fund exposure and direct ownership stack up:

- No direct ownership. ETF investors own fund shares, not actual tokens in a wallet or exchange account.

- No on-chain utility. Those holding actual HYPE can use it for trading costs on the perpetual futures DEX and gas fees on Hyperliquid's custom smart contract environment, the HyperEVM.

- Third-party custody. Tokens bought by a fund sit with the fund and its custodian. HYPE token holders either self-custody or leave them on centralized exchanges.

- ETF-related fees. ETF investors pay brokerage costs and fund fees. Token holders may pay exchange, wallet, spread, and network costs.

- Only indirect staking rewards. ETF investors do not receive staking rewards directly; any staking income (if applicable) is handled according to fund terms. Retail holders can stake directly to earn rewards, though rates vary.

Biggest risks for ETF investors

For direct token holders, the biggest concerns include price volatility, self-custody challenges, and protocol or exchange-related risks. ETFs are exposed to the same underlying token volatility, while also introducing fund-structure risks and potential deviations from net asset value (NAV).

A Hyperliquid ETF is a convenient vehicle for price exposure through a familiar brokerage account, removing much of crypto's usual friction. But convenience comes with significant risks:

- Concentration risk. You're betting on a single protocol.

- Valuation risk. ETF investors are still exposed to HYPE's price volatility. Market observers have questioned the current valuation of roughly $69 billion, which already exceeds that of Nasdaq Inc. (slightly below $50 billion).

- Centralization risk. Unlike Solana or Ethereum, the Hyperliquid blockchain uses only 27 validators. That's a relatively small validator set in comparison, increasing concerns about concentration and operational resilience.

- Staking risk. Funds that stake a portion of their holdings face lock-up or unbonding periods, validator underperformance, slashing events, and uncertain reward rates.

- Fierce competition. Hyperliquid has steamrolled past dYdX, which once held the crown as the dominant decentralized derivatives platform. A similar scenario could play out again — this time with Hyperliquid on the losing end.

- No '40 Act fund protections. These products do not offer the same investor protections associated with funds registered under the Investment Company Act of 1940. Adverse regulatory action is also possible down the road.

Wrapping up

Hyperliquid ETFs give investors a familiar on-ramp to one of crypto's standout performers this year. They track HYPE's price, capture staking income through professional validators, and remove many of the hurdles that come with owning crypto directly. No wallets, no seed phrases, no on-chain transactions — just a ticker in a brokerage account.

That simplicity comes with trade-offs. ETF holders don't receive the same benefits as direct token holders, including full staking rewards, on-chain utility, and direct control over their assets. They're also exposed to fund-specific risks such as NAV premiums and discounts.

For investors seeking straightforward exposure, the ETFs do exactly what they're designed to do. But for those who want to participate in the Hyperliquid ecosystem itself, owning HYPE directly remains a different proposition altogether.