Lazy investor's guide to crypto (no trading required)

You don't need to trade to win.

Spend five minutes on X and you'd think success requires staring at charts 14 hours a day, chasing pumps, and shorting dumps. Yet in reality, most active traders lose money. The ones who actually build wealth over time are often the ones doing almost nothing.

This guide is for the rest of us. The people with jobs, families, and lives who don't have time to become professional chart analysts.

Here's how to grow your crypto portfolio without breaking a sweat.

TL;DR

- Trading is hard. Most active traders underperform buy-and-hold.

- DCA works. Invest fixed amounts regularly, ignore the noise.

- Earn yield while you wait. Some platforms offer ~5%–8% APY on stablecoins, depending on market conditions and risk.

- Set it and forget it. Automate your buys, your savings, and your portfolio.

- The “lazy” approach often outperforms because it removes bad decisions, not because it requires no effort at all.

Why active trading is a trap

Here's a dirty secret the trading gurus don't advertise: most of them lose money.

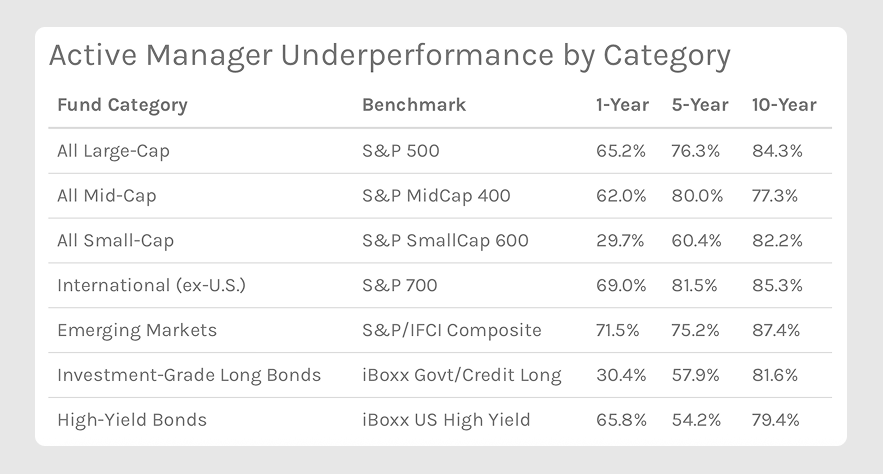

Studies across traditional finance show that active traders consistently underperform simple buy-and-hold strategies. The key reasons are these: high fees, transaction costs, and the challenge of consistent market timing.

According to S&P Dow Jones Indices (SPIVA 2024), over 80% of active fund managers underperform the S&P 500 over a 10-year period.

Crypto is even worse — more volatility, more emotion, more bad decisions at 2 a.m. Passive, low-cost investing is just more successful for most of us.

The problem isn't intelligence or effort. It's psychology.

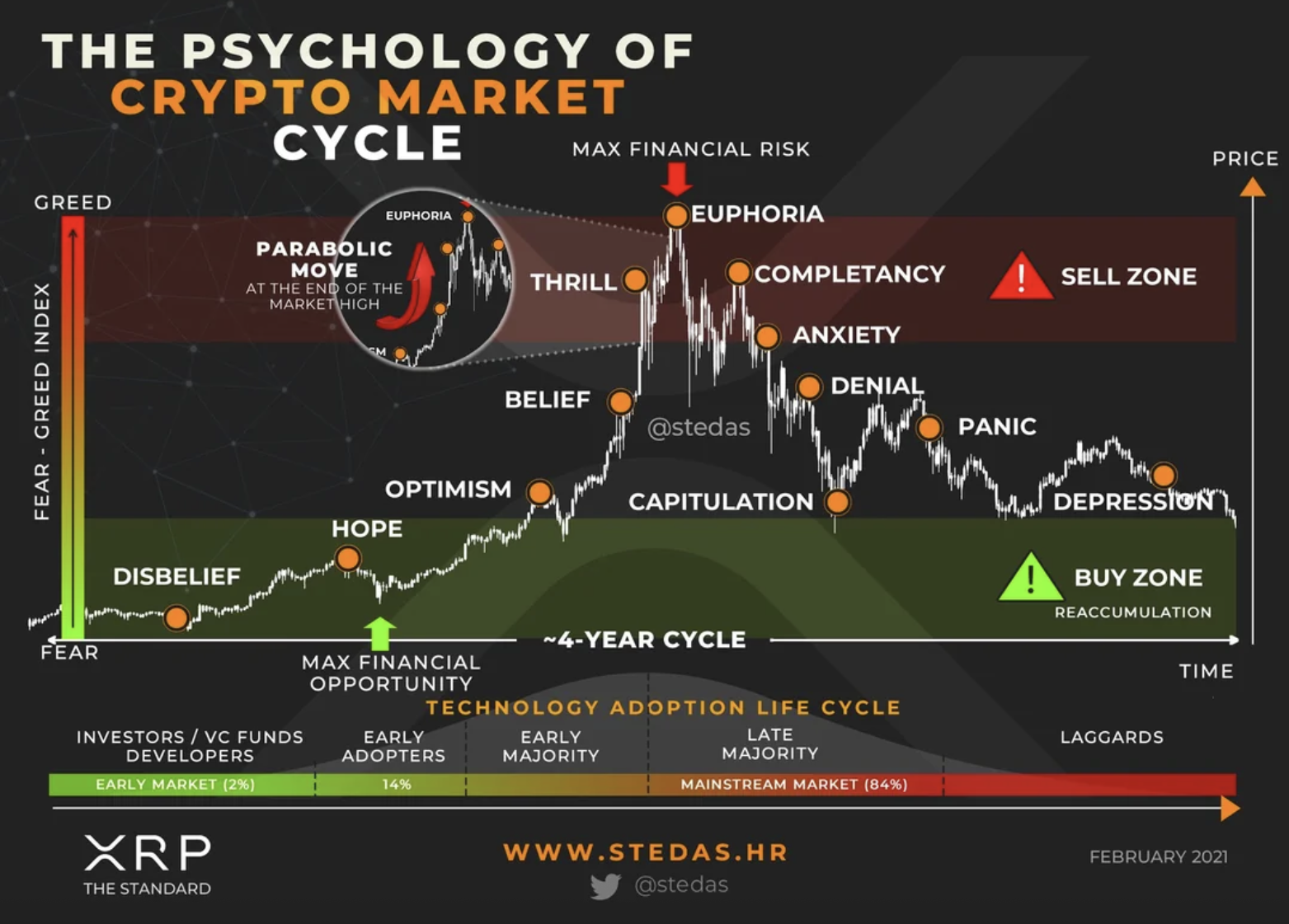

You buy, it drops. You panic-sell, it rallies. You FOMO-buy at the top and it crashes again. Repeat.

Trading feels productive as you click buttons, watch charts, and think you're smart. But feeling productive isn't the same as being productive.

The lazy investor skips all that mess and emotional see-saw. (If you’ve been in crypto long enough, you’ve probably lived this cycle firsthand.)

The lazy investor's toolkit

You don't need eight screens and a Bloomberg terminal. Here are three simple tools to consider:

1. Dollar-cost averaging (DCA)

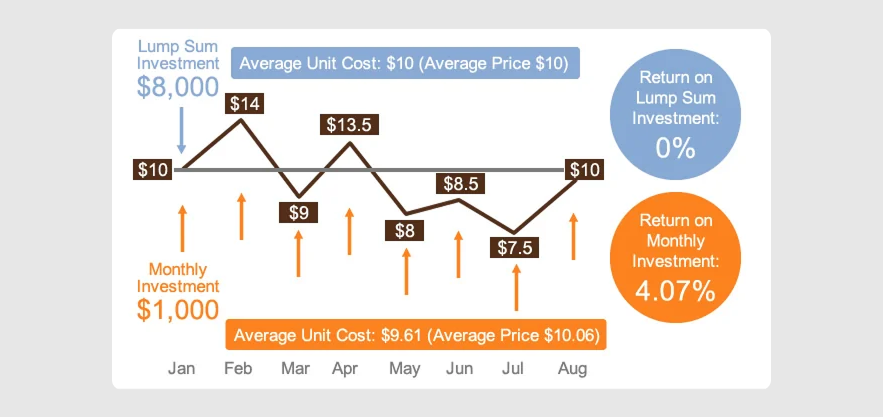

Invest a fixed amount at regular intervals. Weekly, bi-weekly, monthly — pick a rhythm and stick to it.

When prices are low, your fixed dollar buys more crypto. When prices are high, it buys less. Over time, this smooths out your entry price and removes the emotional weight of "did I buy at the worst possible moment?"

Just consistency with zero timing hassle.

A 2024 Kraken survey found that 59% of crypto investors use DCA as their primary strategy. Seasoned high earners — those making over $100,000 — prefer DCA and report higher confidence in their approach. Younger investors under 29 are more likely to try timing the market instead.

Veterans DCA; beginners chase pumps.

2. Crypto savings

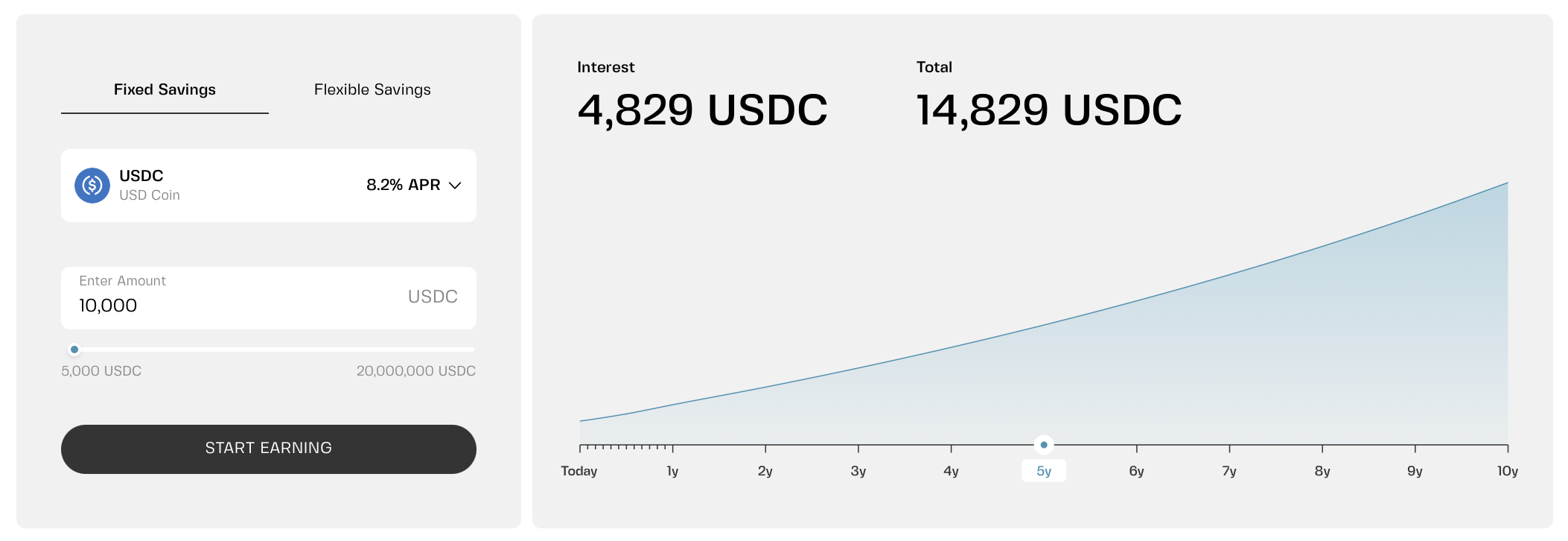

Instead of letting your stablecoins sit idle, put them in a savings account earning 5%–8% APY.

Flexible savings means you can withdraw anytime — perfect for your emergency fund or dry powder. Fixed savings lock your funds for 1–12 months in exchange for higher, guaranteed rates.

Either way, your money works while you sleep. No trading required.

Let's do the math.

You keep $10,000 in a traditional high-yield savings account at 4% annually. After one year, you earn $400.

Same $10,000 in a crypto flexible savings account at roughly 5% earns you $500 per year. At 8% for fixed savings, that’s $800 per year — roughly double what the bank pays.

Now factor in compounding. Crypto savings often add interest to your balance daily, not monthly. That $800 grows even faster because yesterday's earnings start earning today.

APR shows the base rate; APY reflects what you actually earn with compounding.

Over five years, the gap widens dramatically.

- At 4% APY (bank, monthly compounding): $10,000 becomes about $12,170

- At 5.2% APY (crypto flexible, daily compounding): about $12,840

- At 8.2% APR (crypto fixed, assuming annual reinvestment at maturity): roughly $14,830

That's an extra $2,600–$2,700 for doing nothing different except where you park your cash.

Of course, banks have FDIC insurance. That's why you diversify — keep some in both. But leaving all your cash earning 0.01% at a traditional bank while inflation eats it like slow erosion.

Crypto yield is not risk-free. Returns depend on lending activity, platform reliability, and market conditions.

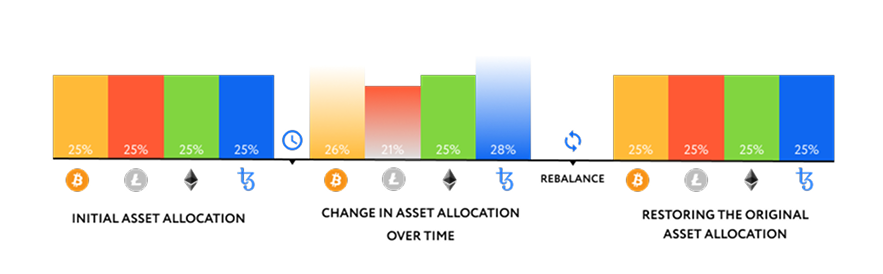

3. Automated portfolios

A simple starting point might look like 60% BTC, 30% ETH, 10% stablecoins. Pick your assets, set your target percentages, and fund it with one click.

But markets move a lot, so that neat 60/30/10 split drifts fast. Say you set it in January, but by March BTC ripped to 75% of your portfolio. You're more exposed than you wanted to be. Or ETH crashed to 15%. You missed the chance to buy low.

Rebalancing manually is possible, but some apps make this effortless with auto-rebalancing that works in the background, buying and selling small amounts to bring you back to your targets.

You're not deciding to sell ETH because you're scared of a crash. You're not wondering if now is the right time to buy more BTC. You're just letting your strategy execute — quietly, consistently, without emotion.

That's the lazy investor's edge. Not timing the market. Not picking winners. Just sticking to a plan without having to think about it.

How to set it up in 10 minutes

Here's a simple lazy portfolio you can build today.

Step 1: Pick your core holdings

Choose 3–5 assets you actually believe in long-term. Bitcoin. Ethereum. Maybe a stablecoin or two. Don't overthink it.

Step 2: Set up recurring buys

Decide how much you can invest each week or month. Start small — even $50 a week adds up over time. Automate it so you never have to think about it.

Step 3: Put your idle cash to work

Move your stablecoins into flexible savings — but look for transparent platforms with clear risk disclosures. Earn 5% while you wait (or 8% for commitment). Keep enough liquid for emergencies, but let the rest earn.

Step 4: Ignore the noise

This is the hardest step. Delete price alert apps. Mute the fear-mongers on X. Check your portfolio once a month, not once an hour.

This isn't financial advice — just a framework to think about. Crypto carries risk. What works for one person might not work for you.

What about the dips?

Here's the beautiful thing about DCA: dips don't scare you.

When prices crash, your fixed buy amount purchases more crypto. You're not panic-selling — you're accumulating at a discount. The lazy investor actually looks forward to red days.

Dry powder sitting in savings will let you manually buy extra during extreme dips. But if the system works fine on autopilot, you don't even have to.

A quick example

Let's say you commit to $500 a month into BTC and ETH through DCA.

- Over a year, that's $6,000 invested. No stress about timing or regrets about buying the top.

- Now add savings. You keep $10,000 in stablecoins earning 5% APY. That's $500 a year in interest — passive yield, not guaranteed returns. If you commit to 12-month savings, that annual yield may grow beyond 8%.

After five years, you've invested $30,000 through DCA, plus earned interest on your buffer, barely lifting a finger.

Meanwhile, the active trader spent hundreds of hours staring at charts, paid taxes on short-term gains, and probably ended up with less.

When this strategy breaks down

This approach is simple — but it still requires discipline. It tends to fall apart when:

- You override the system and start reacting to price moves.

- You constantly rotate into new coins instead of sticking to a plan.

- You chase higher yields without understanding the risks behind them.

The strategy itself isn’t complicated. Sticking to it is.

The bottom line

Trading is a job — stressful, competitive, and often unprofitable. Investing doesn't have to be. Just show up regularly and let time do its thing while you live your life.

Set up recurring buys, park cash in savings, and automate your portfolio. Done.

The lazy investor doesn't lose because they're lazy. They win by removing emotion, sticking to a system, and letting compounding do the heavy lifting over time.

Frequently Asked Questions

1. Is DCA really better than lump sum investing?

Statistically, lump sum outperforms about two-thirds of the time — in hindsight. The problem is, you don't know if today is the top or the bottom. DCA is about managing psychology and reducing regret. Most people are better off averaging in than going all in and panic-selling the first dip.

2. What if I want to buy more during a crash?

Go for it. DCA is your baseline, not a straitjacket. If you have extra dry powder and markets are down 40%, feel free to add more. Just don't abandon your regular buys trying to time the perfect entry.

3. How do I earn yield without locking up my funds?

Flexible savings. Your money stays liquid and grows while it waits, with instant withdrawals and daily compounding. Rates vary by platform, so compare transparency, risk, and consistency — not just headline APY.

4. What's the minimum I need to start?

Almost nothing. You can start DCA with $10 a week. You can even open a flexible savings account with $10. The lazy investor strategy works at any scale — the habit matters more than the amount.

5. Do I need to rebalance my portfolio?

Yes. But if you want to be extra lazy, some platforms offer auto-rebalancing portfolios. Set your target allocations once, and the system handles the rest. You don't have to think about it daily.