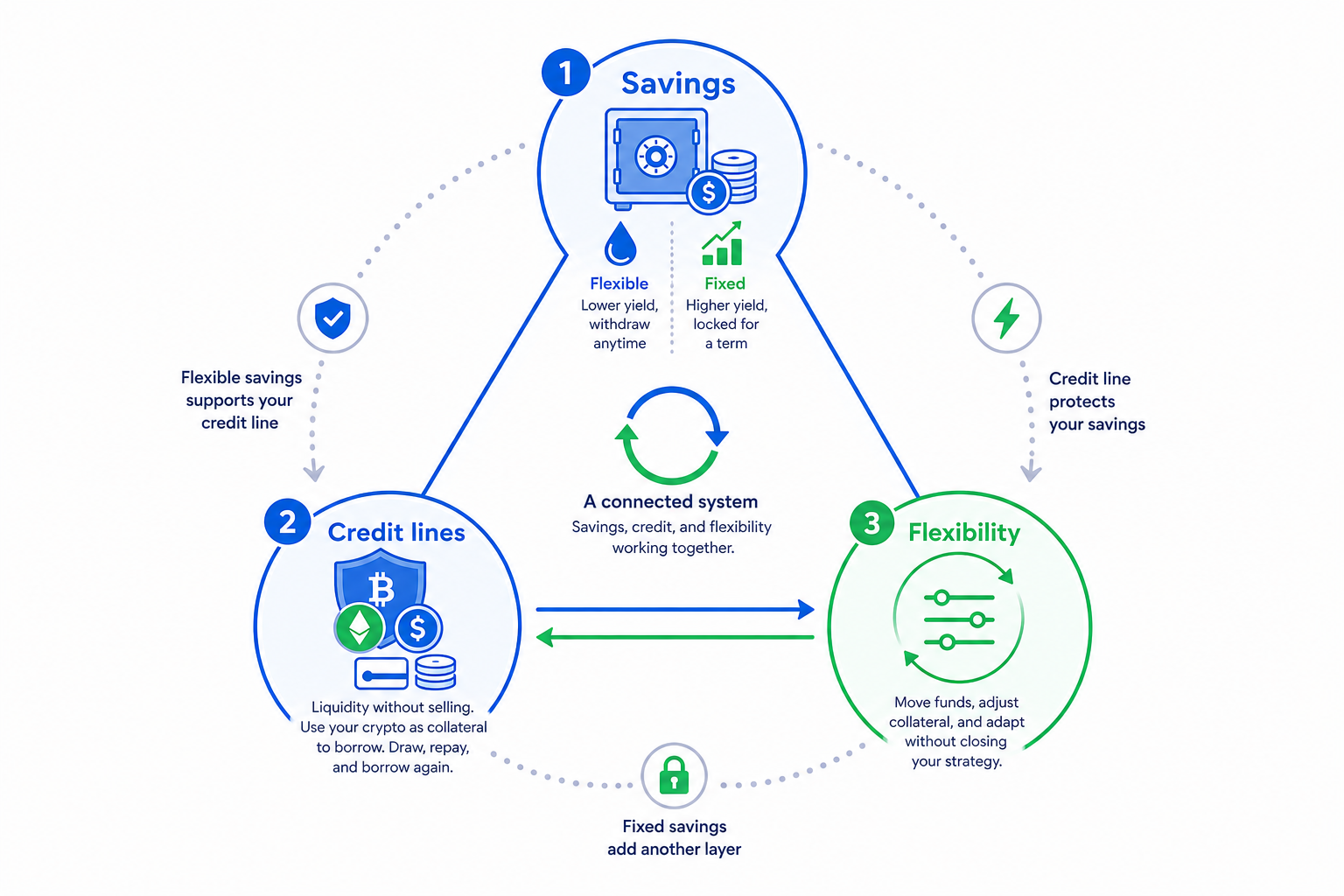

Liquidity triangle: Savings, credit lines, and why flexibility matters

In crypto, there are several ways to access liquidity — and every option comes with trade-offs.

You can sell your assets, but that may trigger taxes and reduce your exposure to future upside. You can borrow against them, but that requires collateral. You can keep funds in savings, but some products lock your assets away for higher yields.

The challenge isn't choosing one option over another. It's having the flexibility to use the right tool at the right time.

That's where the liquidity triangle comes in: a simple framework built around savings, credit lines, and liquidity buffers. Together, they help you stay invested, access cash when needed, and react to opportunities or market volatility without disrupting your long-term strategy.

Let's look at how the three pieces work together.

TL;DR

- Savings give you yield. Flexible savings keep your funds accessible. Fixed savings give you higher rates but lock your money.

- Credit lines give you liquidity without selling. Keep LTV low and some platforms offer 0% APR.

- Flexibility is the bridge. Being able to move funds between savings, collateral, and credit lines is what makes the system work.

- A lack of flexibility costs you money. Locked funds you can't access. Collateral you can't swap. Savings you can't use.

- The best strategy combines all three. Savings for yield, credit line for emergencies, and flexibility to move between them.

The three corners of the triangle

Corner 1: Savings

Savings are your liquidity reserve.

This is where idle assets earn yield while waiting for their next job.

Flexible savings keeps your money accessible. The yield is lower, but you can withdraw at any time without penalties. That makes it ideal for emergency funds, collateral top-ups, or opportunities that require quick action.

Fixed savings sits at the other end of the spectrum. In exchange for committing funds for a set period, you typically earn a higher rate. The catch is that your money isn't readily available until the term ends.

The trade-off is straightforward: the more yield you want, the less flexibility you usually get.

Corner 2: Credit lines

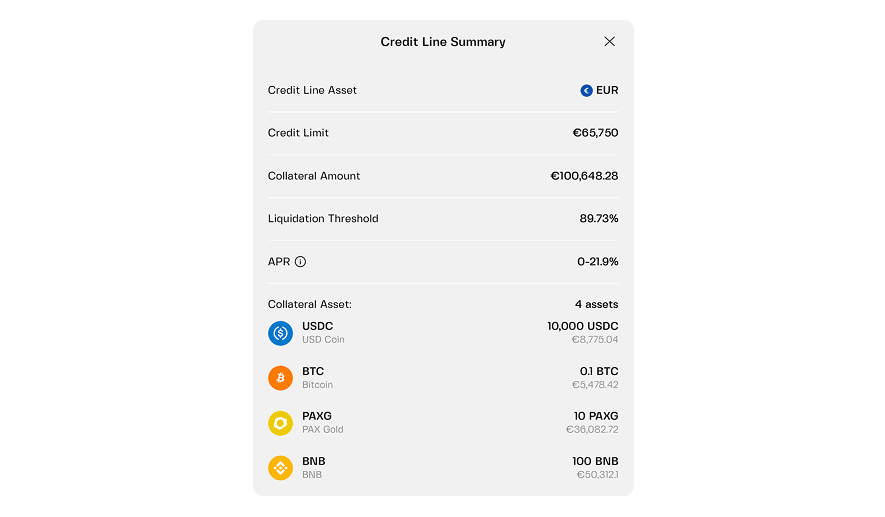

Credit lines are your source of liquidity without selling.

Instead of cashing out your crypto, you pledge it as collateral and borrow against it. You keep your exposure to the market while gaining access to funds when you need them.

Unlike traditional loans, you don't need to draw the full amount at once. Your credit line is there when you need it. Borrow, repay, and borrow again as circumstances change.

On platforms like Clapp, maintaining a conservative LTV can even reduce borrowing costs to 0% APR.

The trade-off is that your collateral remains tied to the loan — although multi-collateral credit lines can make managing that collateral much more flexible.

Market volatility can still affect your position. But you access liquidity without selling assets and potentially triggering a taxable event.

Corner 3: Flexibility

Yield is useful. So is liquidity. But flexibility is what allows them to work together.

It's the ability to:

• Move funds from savings into collateral when markets fall

• Withdraw cash without unwinding your entire strategy

• Adjust your collateral mix without closing your credit line

With flexibility, savings and borrowing become a system. Without it, they're just separate products.

How the pieces connect

Flexible savings can support your credit line.

Your savings are earning yield — but when they're flexible, they're also dry powder. If your LTV rises during a market downturn, you can move stablecoins from savings into your collateral pool in minutes. It's one of the simplest ways to avoid a forced sale or liquidation.

Without flexible savings, you'd need to find additional collateral elsewhere — or accept the risk of your position being liquidated.

Your credit line can protect your savings.

When you need liquidity, you don't necessarily have to withdraw from savings. Instead, you can draw from your credit line while your assets continue earning yield.

That means you can access cash without disrupting your portfolio. In many jurisdictions, it can also help you avoid triggering a taxable event that might arise from selling appreciated assets.

Fixed savings add another layer.

You don't have to choose between liquidity and yield. Funds you're confident you won't need in the near future can be allocated to fixed savings, where they typically earn a higher rate — for instance, up to 8.2% per year on Clapp.

Those assets are less liquid, but they're working harder for you. When the term ends, you can reinvest the funds, move them into flexible savings, or use them to repay part of your credit line if needed.

What happens when you lack flexibility

The value of flexibility only becomes obvious when you need it.

Consider two investors with the same portfolio and the same market conditions.

Scenario A: No flexibility

You have $10,000 in fixed savings earning 8%. You also have a credit line backed by BTC.

Then the market drops 30%.

Your LTV rises sharply. To keep your position safe, you need to either add collateral or repay part of the borrowed amount.

The problem is your savings are locked for another six months. You have no flexible reserves available.

Now you're forced into difficult choices: sell assets at an unfavorable time, find liquidity elsewhere, or risk liquidation if the market continues moving against you. In many jurisdictions, selling crypto can also trigger a taxable event, adding another layer of cost to an already stressful situation.

A short-term liquidity problem has suddenly become a portfolio problem — all because your liquidity was locked when you needed it most.

Scenario B: Flexibility

You have $5,000 in fixed savings for the long term and $5,000 in flexible savings as a liquidity buffer. You also have the same credit line backed by BTC.

The market drops 30%.

Your LTV rises — but this time you have options.

You move stablecoins from flexible savings into your collateral pool. A few taps later, your collateral buffer is restored and your position is back within a comfortable range.

No forced selling or scrambling for liquidity. Your long-term strategy remains intact.

Same market crash. Same assets. Different outcome.

That's the value of flexibility. It's about having liquidity available when it matters most. Maximizing yield is secondary.

How credit lines add optionality

A fixed-term loan typically locks you into a repayment schedule. Depending on the provider, it may also come with origination fees, late-payment penalties, and limited flexibility once the loan is active.

Credit lines work differently. Instead of taking out a one-time loan, you have liquidity available when you need it. Draw funds, repay them, and borrow again without having to reapply each time.

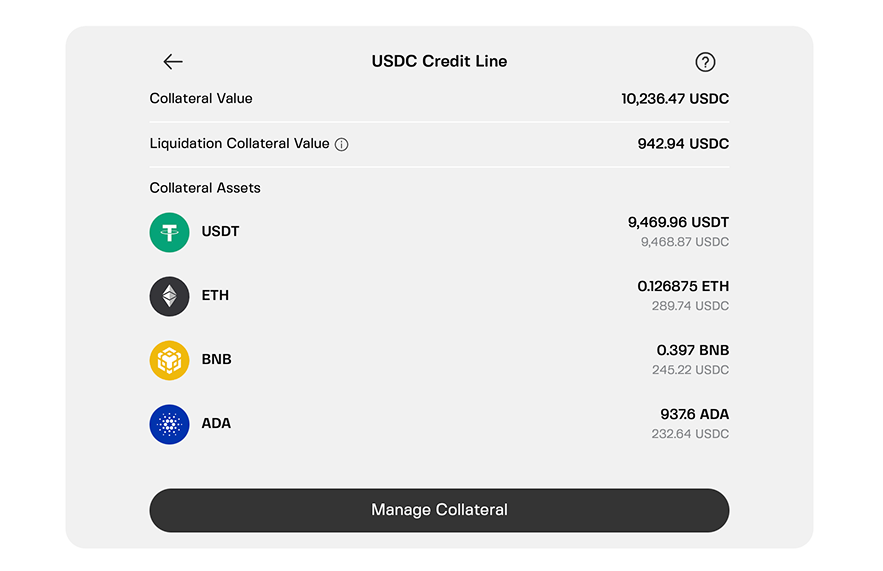

Multi-collateral credit lines add another layer of flexibility. You can add, remove, or swap collateral assets without closing your position. That means your liquidity strategy can evolve alongside your portfolio.

Clapp lets you combine up to 25 assets in a single collateral pool. Rather than relying on one coin, you can adjust your collateral mix as market conditions change.

That's optionality. You're not forced into a single decision on day one. You have the flexibility to adapt as opportunities and risks emerge.

Putting the triangle to work

A balanced liquidity strategy can look something like this:

- Flexible savings for funds you may need at short notice. Your assets remain accessible while continuing to earn yield.

- Fixed savings for capital you're confident you won't need for months. Locking funds for a set term can provide higher returns while keeping those assets productive.

- Credit lines for liquidity without selling. Instead of liquidating holdings, you can borrow against them when needed while maintaining exposure to potential upside.

- Flexibility to move between all three as your circumstances change.

Together, these components create a system that balances yield, liquidity, and resilience. Instead of relying on a single product, you have multiple sources of liquidity available when you need them.

Connecting the three dots

Savings generate yield. Credit lines provide liquidity. Flexibility is what ties them together.

The goal isn't to maximize any one piece of the triangle. It's to make sure each part supports the others.

Flexible savings can help you respond to unexpected expenses. Credit lines can provide liquidity without forcing you to sell. Fixed savings can put long-term holdings to work at higher rates.

Used together, they create a more resilient portfolio — one that can generate returns, access liquidity, and adapt to changing market conditions without sacrificing long-term goals.

Frequently asked questions

1. Should I put all my cash in fixed savings for the higher rate?

No. Keep at least 3-6 months of expenses in flexible savings. That's your emergency fund. Lock only the portion you're confident you won't need.

2. How much should I keep in my credit line?

You don't need to draw anything. On platforms that offer 0% APR at low LTV levels (such as Clapp), you can keep a credit line available as a safety net without paying borrowing costs until you actually use it.

3. Can I use my flexible savings as collateral for my credit line?

On platforms like Clapp, yes. You can move funds from savings to your collateral pool instantly. That's what makes the triangle work.

4. What if my fixed savings term ends during a crash?

You have options. You can roll it into a new fixed term, move it to flexible savings, or use it to repay your credit line. Flexibility is about having choices — and you'll have them.

5. Is this strategy only for large portfolios?

No. The math works at any scale. $1,000 in flexible savings, a credit line with low LTV, and a small fixed savings deposit give you the same structural advantages. Start where you are. The system scales with you.