Saylor’s spiral: How long can Strategy defy Bitcoin's gravity?

Bitcoin’s latest plunge has reignited fears that Michael Saylor's Strategy could be forced to offload a portion of its massive BTC holdings. While metrics from Myriad show a 16% chance of that happening in 2026, financial experts are increasingly on edge.

At its core, Strategy’s model only works as long as its stock trades at a meaningful premium to the value of its Bitcoin. That premium allowed the company to issue shares at attractive prices, buy more BTC, and increase Bitcoin per share (BPS). As that premium compresses, the flywheel slows and may even reverse.

The software firm's Bitcoin shopping spree continues — but how long will it hold?

Multi-year Bitcoin shopping spree

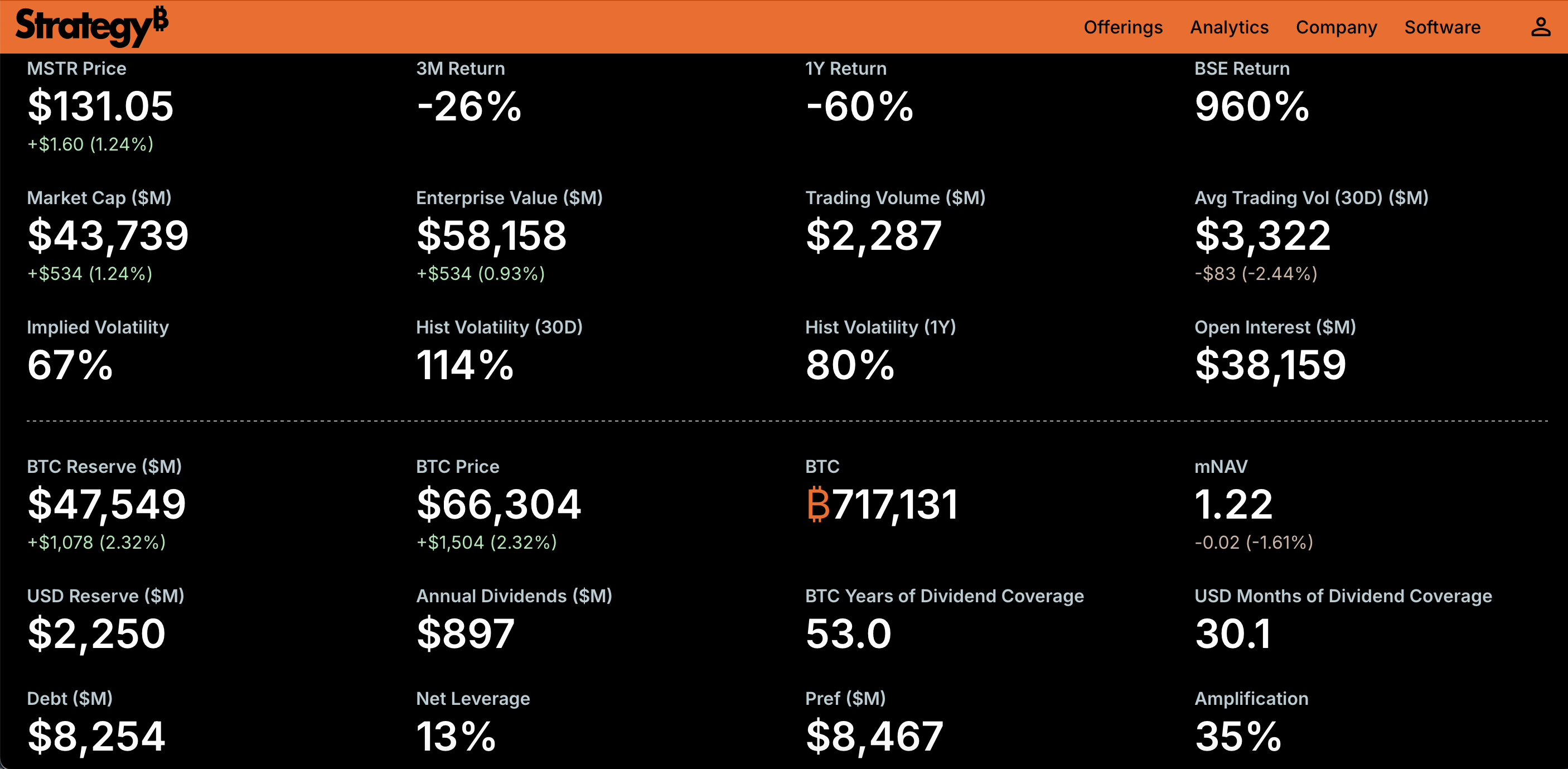

Strategy, formerly MicroStrategy, started amassing BTC in the summer of 2020. As of February 23, 2026, the company hoards 717,131 BTC in its coffers, and it keeps snapping up more at least once weekly. That total stash amounts to 3.41% of the total Bitcoin supply, capped at 21 million.

Initially, Strategy funded the purchases with its existing corporate cash war chest. Later, the firm pivoted to issuing debt via equity and convertible notes.

How the 'accretion machine' worked

At the end of Q2 2020, MicroStrategy had 76 million shares of Class A common stock outstanding. That number has since rocketed by 313% to over 314 million as of February 23, 2026. Class A accounts for all the new shares issued over the past 6 years.

Strategy's model is based on constantly gobbling up more Bitcoin and boosting the amount of BTC investors own per share (the Bitcoin per share, or BPS metric). Until 2026, the company mostly relied on raising funds from stock sales to fuel its crypto purchases.

It worked because its stock price growth kept outshining the pace of Bitcoin rallies. For instance, from the end of 2023 to mid-July 2025, Strategy shares soared more than 7x, far beyond BTC’s 2.8x climb. Post-Independence Day 2025, Strategy could buy 3.8 BTC by selling 1,000 shares — 150% more than at the end of 2023.

Fortune's Shawn Tully characterized this strategy as an “accretion-via-dilution” machine. Saylor continuously increased the BTC every shareholder effectively “owned” (BPS).

- Sell more shares at lofty prices

- Buy more BTC

- Ramp up earnings per share

The share price hit a year-to-date high of $457 in the summer. For the rest of 2025, Strategy continued relentlessly issuing — its Q4 presentation labels it “largest US equity issuer” for that year.

As long as MSTR appreciated faster than Bitcoin, issuing new shares was accretive. Yet once that relationship flipped, dilution stopped increasing Bitcoin per share. Instead, it began eroding it.

When the premium cracked

Then came the inflection point.

At press time, Strategy shares are changing hands at $130, a 72% collapse from the apex. In comparison, Bitcoin is only 47% down from the ATH ($126,080) to its current level. This means:

- The accretion scheme is no longer self-reinforcing.

- Every time Saylor sells new stock at depressed prices to buy BTC, he's diluting the mix, not “sweetening” it.

- If MSTR underperforms BTC for a sustained period, each equity raise reduces the BPS rather than enhancing it.

In other words, the model depends not just on Bitcoin going up — but on Strategy stock outperforming Bitcoin itself.

Strategy can no longer count on meteoric MSTR stock prices to keep the train rolling — unless they rocket again. Its formula may be sabotaging its business objective, officially formulated as “increasing Bitcoin per share.”

mNAV compression

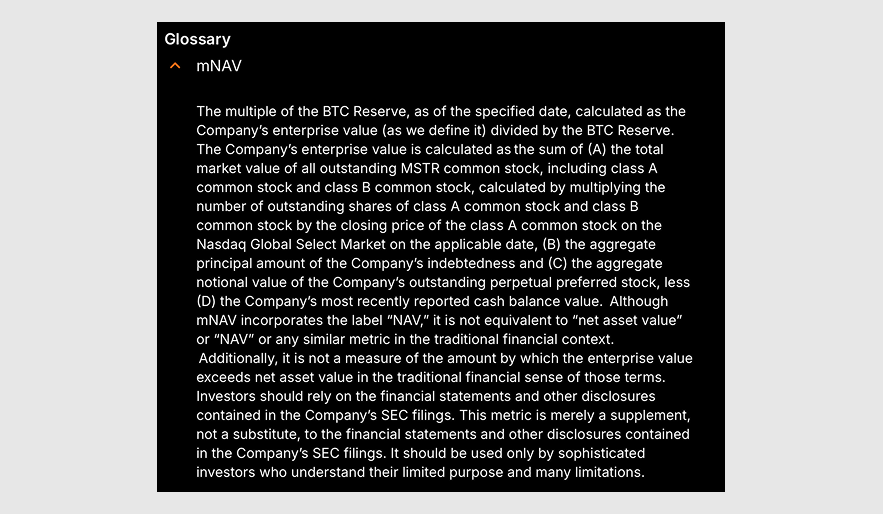

The critical pressure point is mNAV (market-to-net-asset value). This measures how much investors are willing to pay above the value of Strategy’s Bitcoin holdings. mNAV is calculated as the company's enterprise value divided by the market value of the BTC reserve.

If the stock trades at a premium, the company can issue shares at favorable terms and buy more BTC per share. If it trades at a discount, that mechanism breaks.

Historically, the premium reflected three things: leveraged Bitcoin exposure, strong retail/institutional demand during bull cycles, and capital markets optionality — a company’s ability to access different sources of funding in the financial markets. But in a risk-off environment, that premium can compress rapidly.

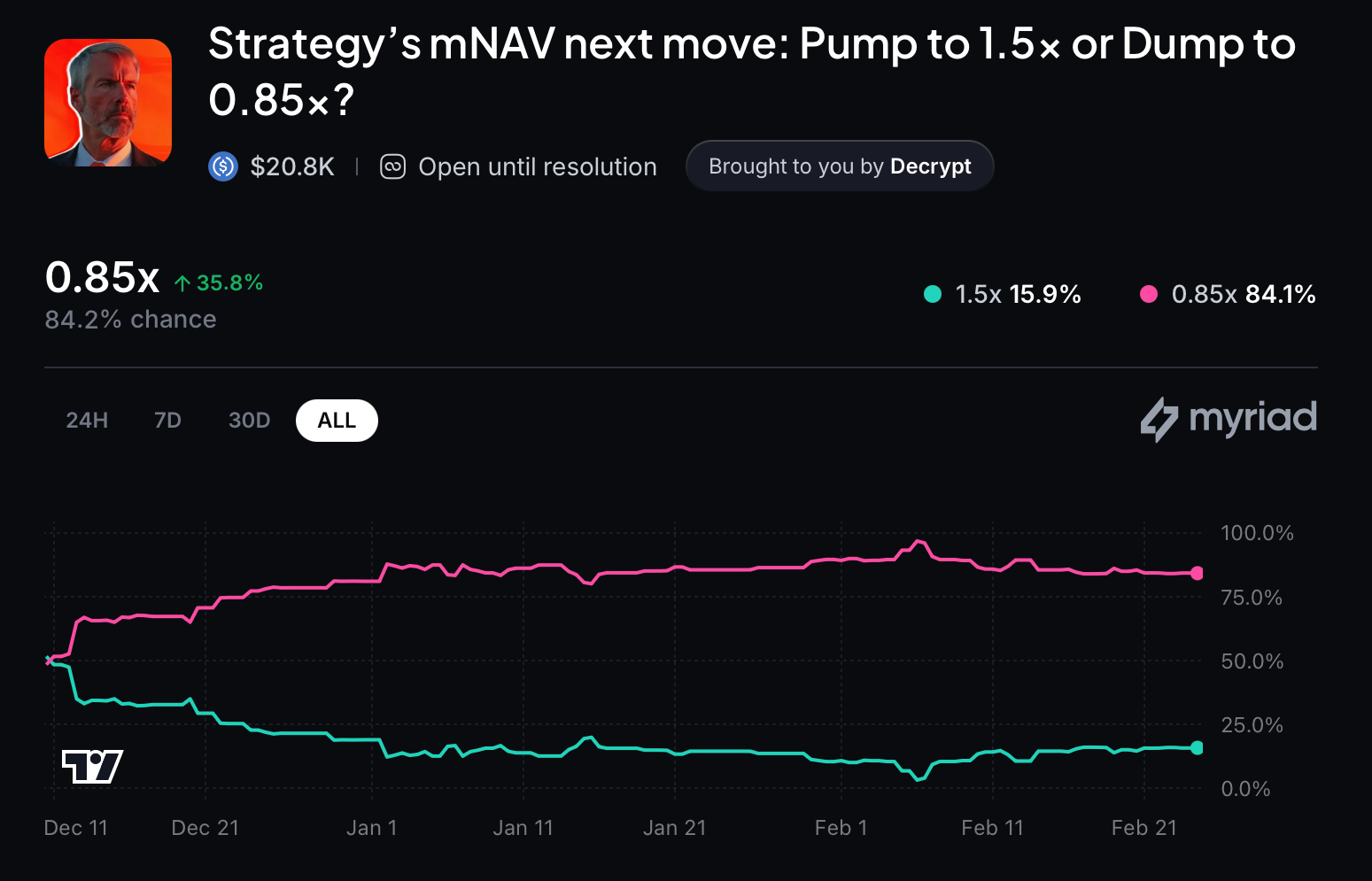

If mNAV remains below 1.0x for an extended period, Strategy effectively loses access to its most powerful funding tool: accretive equity issuance. At press time, it stands at 1.22x.

Yet on Myriad, over 84% of bettors consider a dip to 0.85x more likely than a rise to 1.5x.

Plan B: Switching to costlier fuel

Issuing more common stock during the downturn would only cause more bleeding. So Strategy made a pivot to preferred stocks — shielding its existing common stockholders.

Still, this scheme also harbors risks.

Its Class A stocks are effectively a high-beta play on Bitcoin. They attract growth-focused investors, but may appear too jittery for others.

- Preferred stocks pay a regular, guaranteed and higher dividend (an 8% series, a 10% series, and an 11.25% “Stretch” series). Their holders also enjoy priority over common shareholders (hence the term “preferred”). This appeals to more conservative investors.

- Importantly, preferred stocks have no maturity date, which eliminates the risk of Strategy being forced to sell BTC at a loss to repay holders in a downturn.

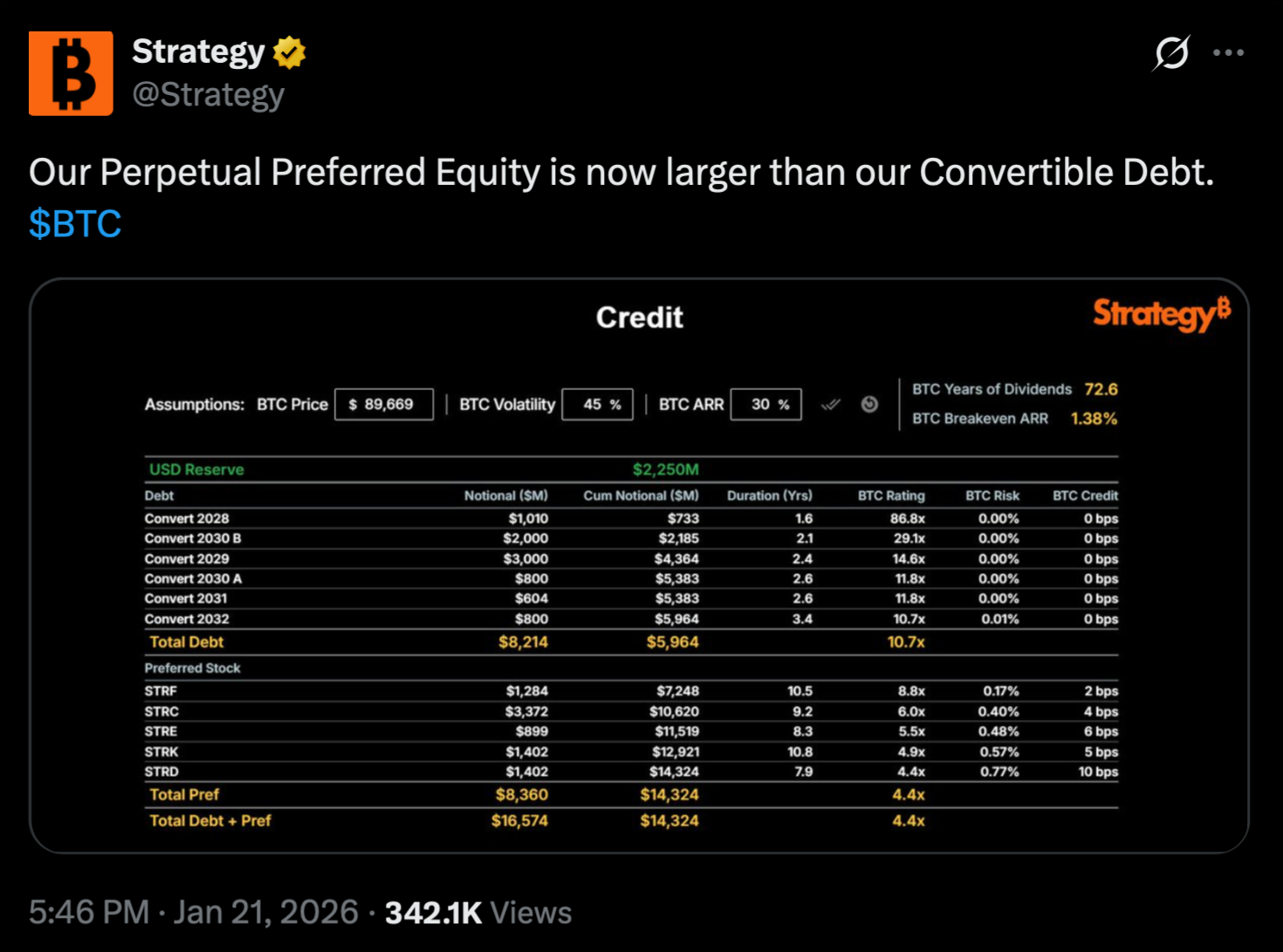

According to the company's own Q4 presentation, it became America's largest issuer of preferred stocks in 2025, raking in $7 billion from those offerings — or a third of every dollar raised on Wall Street. That figure has now climbed to $8.36 billion, according to the company's January X post.

For context, this is slightly above the $8.21 billion raised using convertible debt with maturity between 2027 and 2032. So far, refinancing has only involved new equity or conversion to stock, not BTC selling.

Thanks to the influx of cash, Strategy was able to relatively steady the BPS.

But the trade-off is significant: the company currently faces almost $900 million a year in fixed dividend payments. That's a major cash drain independent of Bitcoin’s price. Meanwhile, the core software business generates approximately $123 million in quarterly revenue.

In simple words, this financial pivot is similar to switching to a new, more expensive type of fuel to keep your car moving without adding extra weight to its chassis. If the car fails to reach the next pit stop — BTC price recovery — before that fuel also runs dry, the engine could still seize up.

This maneuver allows Strategy to continue buying Bitcoin, but it also introduces a high-wire risk — a massive, ongoing cash obligation that the company must meet regardless of the BTC price. However, it also stockpiles around $2.25 billion in USD reserves.

Four structural stressors

Despite this cushion, Decrypt’s Akash Girimath has pointed out the four biggest issues with this approach.

#1 Bear market

If BTC sheds over 50% of its value and lingers low for over two years (echoing the previous crypto winters), it will erode the stock premium. The firm might not be able to raise new capital.

#2 Persistently low MSTR price

In this case, debt holders will not convert — they will demand cash repayments. Preferred dividends will also require ongoing cash payments, while fading investor appetite could make refinancing through new equity impossible. Strategy may be cornered into repaying its obligations in cash or through Bitcoin sales.

#3 High MSTR-BTC correlation

Strategy’s perceived status as a Bitcoin proxy magnifies the coin's price swings. That was a blessing between 2020 and 2024 — during a bull run — but now MSTR is exaggerating the downside. From early October to late November 2025, BTC shed 32%, while MSTR plummeted 52%.

#4 Falling mNAV (Market-to-Net-Asset-Value)

A falling premium limits equity issuance and strains dividend funding flexibility.

Each factor compounds the others. Reduced premium limits capital access. Limited capital access increases refinancing risk. Refinancing risk further pressures the stock.

Strategy's liquidity clock

- The $2.25 billion in cash reserves can cover the $900 million annual dividend payments for preferred shares for around 30 months.

- In September 2027, investors can activate a $1.01 billion “put” option on the 2028 notes. If the stock price is too low, this might trigger a cash repayment.

- Most convertible notes mature between 2027 and 2032, as shown in this chart below.

Doom loop: Slow grind could end it all

Each of the four stressors worsens the others in a chain reaction that could theoretically push Strategy into a death spiral. That said, analysts expect a slow bleed, not a spectacular blow-up.

In this negative hypothetical scenario, the MSTR stock will continue lagging behind BTC for years because of the dilution drag. Eventually, it will become “a cautionary tale about corporate treasury strategies,” as Caladan’s head of research Derek Lim put it. Possibly, this process is already underway.

Strategy's defence

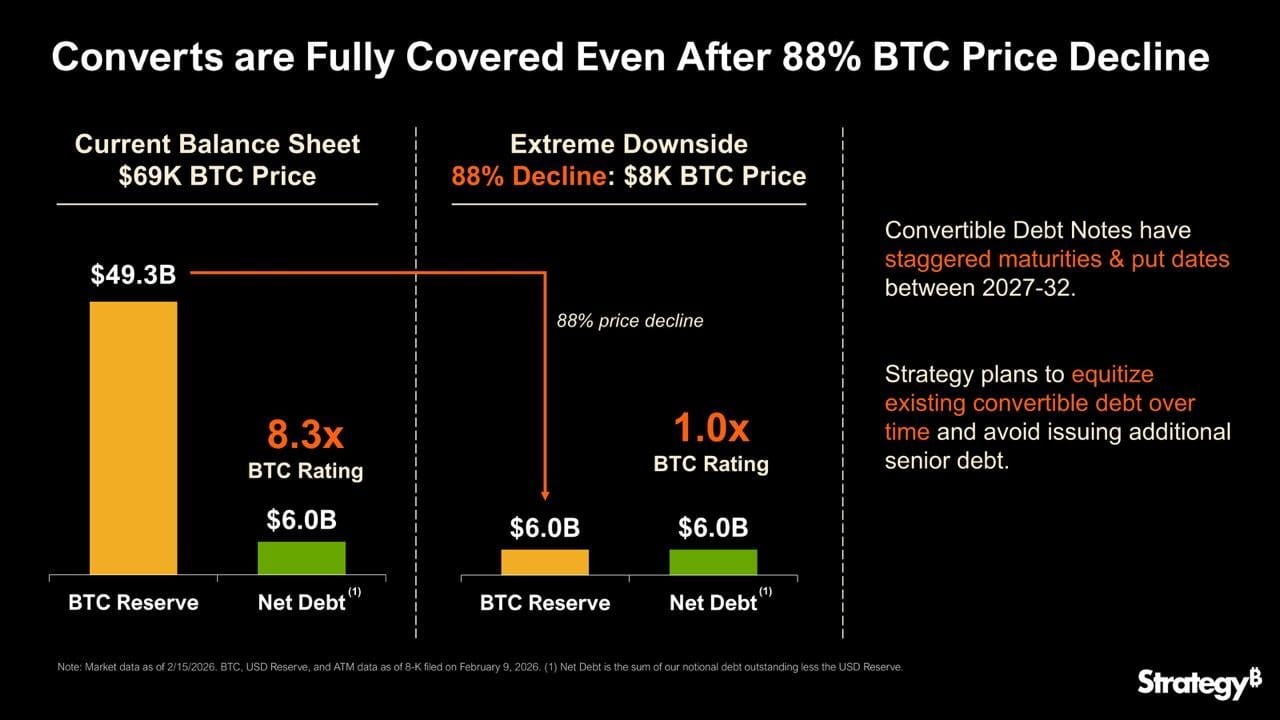

Currently, with BTC hovering around the $66,000 mark, the company's Bitcoin reserves are worth roughly $47.4 billion, as opposed to a net debt of $6.0 billion.

On February 5th, Strategy defended its balance sheet strategy in an X post:

"Strategy can withstand a drawdown in $BTC price to $8K and still have sufficient assets to fully cover our debt.”

The accompanying graph showed all convertible notes would be fully covered even if BTC lost 88% of its value, tanking to $8,000. In this case, the total Bitcoin reserves would be worth around $6.0 billion, effectively matching the net debt.

According to CEO Phong Lee, the coin would have to stagnate at that mark for 5-6 years before the firm would face any real trouble covering its convertible debt.

Even so, debt coverage is not the same as shareholder value preservation. Even if convertibles remain covered, prolonged equity dilution and fixed dividend burdens could materially impair common shareholders well before a theoretical insolvency threshold is reached.

Furthermore, remaining solvent would mean liquidating the entire Bitcoin treasury, contradicting the company's proclaimed ethos.

As noted above, the first major debt maturity comes in September 2027. However, critics also flag the $900 million in annual dividend obligations that may drain the company's Bitcoin reserves. The existing cash stash of $2.25 billion is enough to ride out over 30 months of the payments without touching a single Bitcoin.

MSCI concerns

This year, Strategy almost got booted from major US indices. The MSCI considered excluding entities with over 50% of their balance sheet in digital assets — but later decided to table the matter temporarily.

Those doubts echoed investors' long-time worries.

Battle-tested, but margin for error is slimmer

Strategy weathered the 2022 crypto winter, when BTC traded more than 50% below its average purchase price for 16 months.

However, the company now carries a larger, more layered capital stack and depends more heavily on maintaining a premium valuation to fund operations and growth. Its shrinking mNAV means the margin for error is now thinner.

If Bitcoin stays subdued for an extended period of time and the premium does not recover, the company will likely face refinancing issues as dilution risk explodes.

Conclusion: Defying gravity — or orbit decay?

Strategy’s model has been battle-tested, but it now faces a different challenge. This is no longer just a directional Bitcoin bet. It is a capital markets strategy built on maintaining a valuation premium.

If that premium returns, the flywheel can restart. If it does not, the company may not implode overnight — but it could gradually transform into a case study in the limits of corporate treasury leverage.

The real question is not whether Strategy can survive an 88% Bitcoin drawdown. It is whether it can sustain investor confidence long enough to keep its capital machine running.