Scared of a crypto crash? Here's your buffer.

You've been here before.

Wake up. Check phone. Portfolio down 15%. Scroll X. "Bloodbath." "Liquidations everywhere."

Your stomach drops as you do the math. How much you've lost, how long it took to earn it, and how long it might take to get it back.

Here's the thing about crypto crashes: they're not surprises anymore. They're part of the deal. But being prepared for them is a choice.

Let's talk about building a buffer — so you stop panicking and start planning.

TL;DR

- Crypto crashes happen regularly. Bitcoin has dropped 70–80% multiple times.

- A buffer protects you from forced selling. Stablecoins, cash, or low-LTV credit lines.

- Don't be the person who sells at the bottom. Have dry powder ready instead.

- Earn yield on your buffer. Flexible Savings keeps it liquid and growing.

- Borrow against crypto, don't sell it. Keep your upside, access cash.

Why crashes feel worse than they should

The real pain of a bear market is forced selling.

You lose your job. You have an unexpected expense. Your portfolio is down 50%, but you need cash for rent. So you sell — at the worst possible moment.

That's survival, not investing.

The people who sleep through crashes aren't psychic or genius traders who shorted the top. They just have one thing you might be missing: a buffer.

What a buffer actually is

A buffer is money you can access when everything else is on fire. It's not your crypto portfolio or leveraged positions. It's the boring, stable, and intentionally unexciting pile of assets that sits there waiting for emergencies.

How big should your buffer be?

According to NerdWallet, "three to six months' worth of your current living expenses is a good rule of thumb." However, there's no magic number — it all depends on your lifestyle and expenses.

- Stable job, low expenses: 3–6 months of living expenses

- Freelancer, irregular income: 6-12 months

- Heavy crypto exposure (50%+ of net worth): 12+ months

If you're living off your crypto full-time (never recommended!), you would probably want a year's worth of expenses sitting in something that won't drop 50% overnight.

If even the minimum seems too steep, start small. If you add $10 to savings weekly and don’t have to dip into those funds, it’ll add up to more than $500 after a year. Having access to that $500 could help pay for a surprise car repair or medical bill without debt.

This emergency fund calculator could help you estimate how much buffer you need.

Where to keep your buffer funds?

The buffer isn't about getting rich. It's about never being forced to sell crypto at a loss. Balanced diversification is key — consider a mix of:

- Stablecoins and/or fiat earning 5%–8% in crypto savings

- Cash in a high-yield bank account (lower rates, but insured)

- An unused credit line with 0% APR at low LTV

As of April 2026, high-yield savings accounts in traditional US banks provide up to 4.21% annually. Some crypto savings products do offer higher rates for fiat, but without FDIC-style insurance. Diversify wisely — never keep all eggs in one basket.

Crypto savings and lending platforms also carry counterparty risk. Spread it across reputable and well-established providers.

Why flexible savings?

This is where most people get stuck. "Cash is trash, right? Inflation will eat it."

Fair point. But crypto crashes eat more.

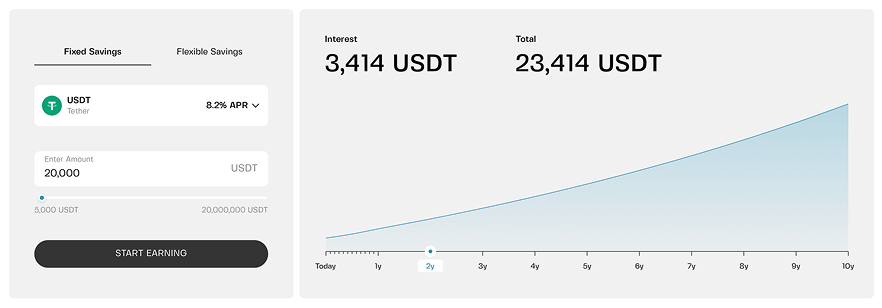

Flexible savings — Stablecoins and fiat earning 5.2% APY, daily compounding, instant withdrawals. Your buffer grows while it waits, and you can access it 24/7.

Compare that to a bank savings account at 0.01%. One works for you; the other barely keeps up.

The highest savings yield requires locking your funds in fixed-term savings for a set duration (typically, between 1 and 12 months). Yet for an emergency buffer, the ability to withdraw 24/7 trumps APY.

You're not trying to maximize returns on your buffer — just try to preserve capital while keeping it liquid. 5% is plenty for that job.

The credit line as a backup buffer

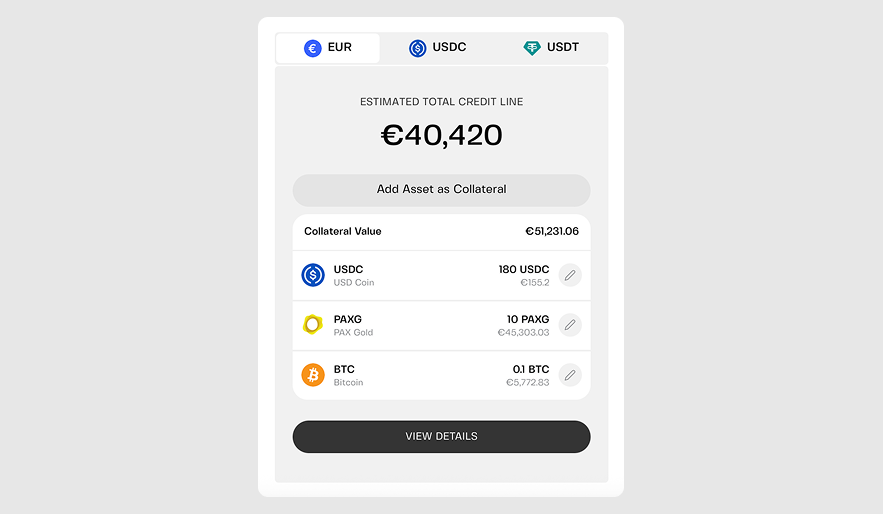

Instead of keeping all your buffer in stablecoins, you can keep a smaller amount there — and use a credit line for the rest.

How it works:

- Keep $5,000 in crypto savings for immediate needs

- Set up a credit line with $20,000 available at 0% APR (keep LTV low)

- If disaster strikes, use the credit line first, then repay from your stablecoins

It's about stacking buffers on top of buffers. You're not paying interest or selling crypto.

Some products let you bundle assets for collateral (even mixing crypto, fiat, and stablecoins) — or even swap them at any time, even after borrowing. So, instead of letting your BNB or XRP sit idle, use them to secure a credit line that will always be on hand.

In some cases, borrowing costs can be very low or even 0% APR — but typically only if you keep your loan-to-value (LTV) ratio conservative (e.g., 20% on Clapp).

LTV is the percentage of your collateral you’re borrowing against — lower is safer. If collateral value drops and your LTV rises too high (e.g., over 90%), your assets can be liquidated. Risk management is critical.

What to do when the crash actually comes

Crashes are stressful, and that's normal. But with a buffer, you have options.

Instead of panic-selling, you can:

- Use your stablecoin buffer to cover expenses while you wait

- Draw from your credit line if you need more than your buffer holds

- Buy the dip if you believe in long-term recovery (because you have dry powder)

- Do nothing — because you don't need to sell

That last one is underrated. Sometimes the best move is to close the app, go outside, and let the market do its thing.

A quick example

Let's say you have $30,000 in Bitcoin and $10,000 in a flexible savings account earning 5.2% APY.

A crash hits. Bitcoin drops 40%. Your portfolio is now worth $18,000. Then you lose your job the same week, with $5,000 worth of unpaid rent and bills.

Without a buffer: you sell some Bitcoin at the worst moment — locking in losses and missing the recovery.

With a buffer: you withdraw $5,000 from your flexible savings. Your BTC stays untouched. And when the market recovers six months later, you're still holding.

That's the difference.

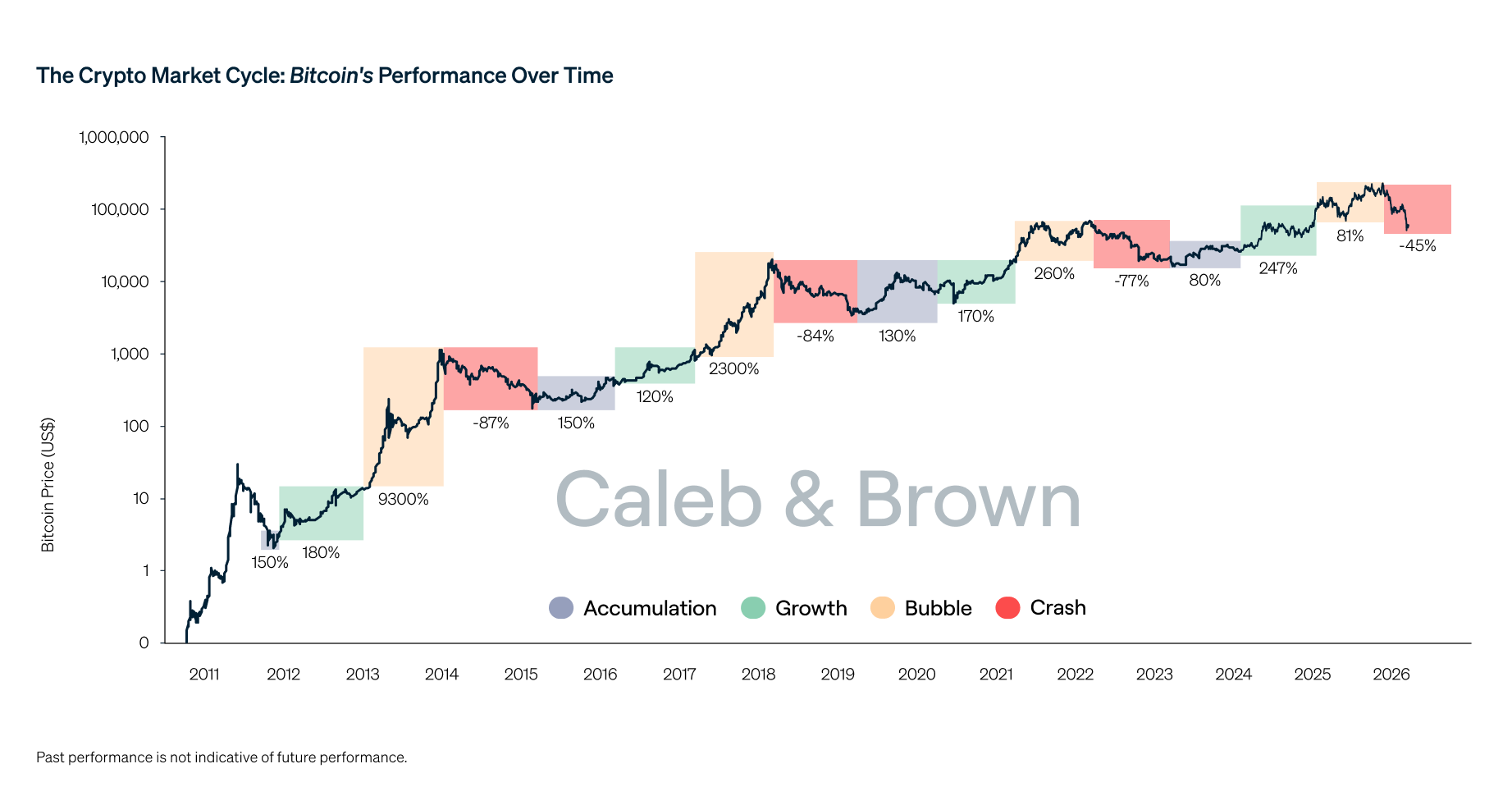

Crypto's four-year cycle

Crypto has historically moved in boom-and-bust cycles, often tied to Bitcoin’s halving events. Three good years, then one bad year, then repeat — but the timing and severity vary each cycle.

Bitcoin — the big dog that still makes up 59% of the entire crypto market — leads the dance. When BTC crashes, everything crashes with it. When BTC rallies, it lifts the whole boat.

Right now, we're in the bad phase. Bitcoin is down 43% from its all-time high of $126,000. That's painful, but it could go even lower. In previous cycles (e.g., 2014, 2018, 2022), Bitcoin shed 75%–94% of its value before recovering.

The bottom line

This is not financial advice — just a framework to manage risk in a volatile market. Crypto crashes are inevitable, but panic is optional.

Build a buffer and keep it boring. Earn yield on it while it waits. And if you want extra protection, add a credit line with 0% APR.

You don't need to predict the next crash — just survive it.

Because the people who survive crashes are the ones who get to enjoy the next bull run.

Frequently asked questions

1. Isn't keeping stablecoins risky too? What if USDT depegs?

It's a valid concern. That's why you diversify your buffer — some USDC, some EUR, maybe some cash in a bank account. While major stablecoins are designed to maintain their peg, they carry different risks than volatile assets like Bitcoin — so spreading exposure is key.

2. How do I earn yield on my buffer without locking it up?

Flexible savings. No lock-ups, instant withdrawals, daily compounding. On Clapp, that's 5.2% APY on stablecoins and EUR. Your buffer stays liquid and grows while it waits.

3. What's the catch with 0% APR credit lines?

You need to keep your LTV low — usually 20% or below (depending on the platform). Borrow conservatively and it's free. Borrow aggressively and interest kicks in. It's a reward for responsible borrowing, not free money for everyone.

4. How much buffer is too much?

If you have two years of expenses sitting in stablecoins earning 5%, you're probably missing out on upside. The goal isn't to hoard cash — it's to have enough that you never need to sell crypto at a loss. For most people, 6–12 months is plenty.

5. Can I use my buffer to buy the dip?

Absolutely. That's the best part. Having dry powder means you're not just surviving crashes — you're positioned to take advantage of them. When everyone else is panic-selling, you're buying at a discount. That's how wealth is built over time.