Stop selling crypto. Tax man is watching.

Here's something nobody tells you when you're stacking sats and dreaming of moons: selling crypto triggers taxes. Not "maybe" or "if you make enough." In most countries, every single sale is a taxable event.

You've probably seen the posts. "Just sold my ETH for a down payment. Tax? What tax?" That person is in for a surprise. And the tax man is getting better at tracking crypto every year.

So what do you do when you need cash but don't want to hand a chunk to the government? Stop selling — borrow instead.

The tax trap nobody talks about

Let's say you bought Bitcoin three years ago for $10,000. Today it's worth $50,000. You need $20,000 for a business opportunity.

If you sell, here's what happens:

- You trigger a taxable event.

- Your gain is $40,000 ($50,000 – $10,000).

- Depending where you live, you might owe $8,000–$12,000 in taxes.

- You now have $20,000 for your opportunity — but you just lost nearly half of it to taxes.

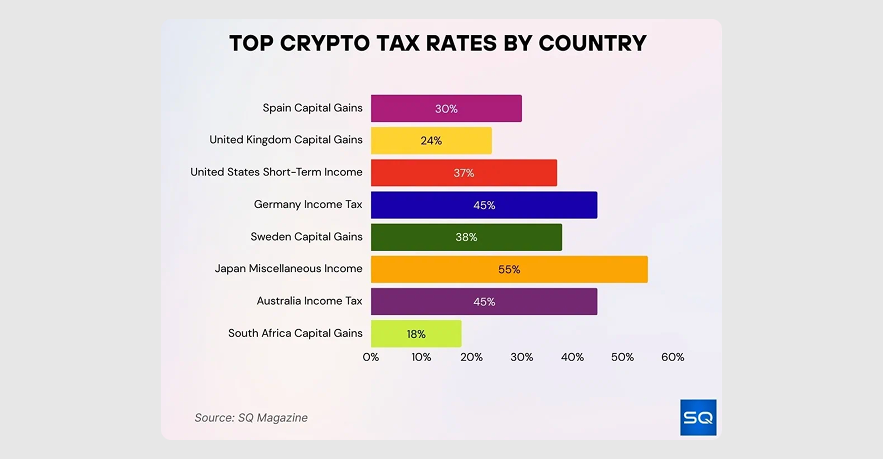

Citizens of the UAE pay no income or capital gains tax — but elsewhere, crypto holders aren't so lucky. Tax rates also vary across jurisdictions, for instance:

- In Germany, selling within a year is subject to income tax rates up to 45%.

- In the US, such sales are subject to the ordinary income tax rate that can reach 37%. Assets held for over a year constitute long-term capital gains rates (0%-20%).

- In the UK, you might pay 18% or 24% above the annual capital gains tax-free allowance (currently £3,000).

- France applies a flat 30% tax on crypto gains for occasional investors. Trading triggers progressive income tax rates (from 0% to 45%), plus social security contributions (17.2%).

Taxes are one side of the coin; selling is also expensive in terms of missed upside. If that Bitcoin you sold at $60,000 hits $100,000 next year, you'll be watching from the sidelines.

How borrowing changes the math

Now imagine you borrow against that same Bitcoin instead.

- You deposit your BTC as collateral.

- You borrow $20,000 against it.

- No sale = no tax event.

- Your coins stay yours.

- You get the cash you need.

- If Bitcoin rallies, you're still holding.

No taxes or regrets that your coins moon without you.

The wealthy have used this financial tool for generations. When they need cash, they borrow against their assets.

The rules (because nothing's free)

Borrowing against crypto isn't complicated, but it has rules you need to understand.

- It's over-collateralized. You need to pledge more than you borrow. Want $10,000? You might need $20,000–$30,000 in crypto. That's the trade-off for no credit checks and no tax event.

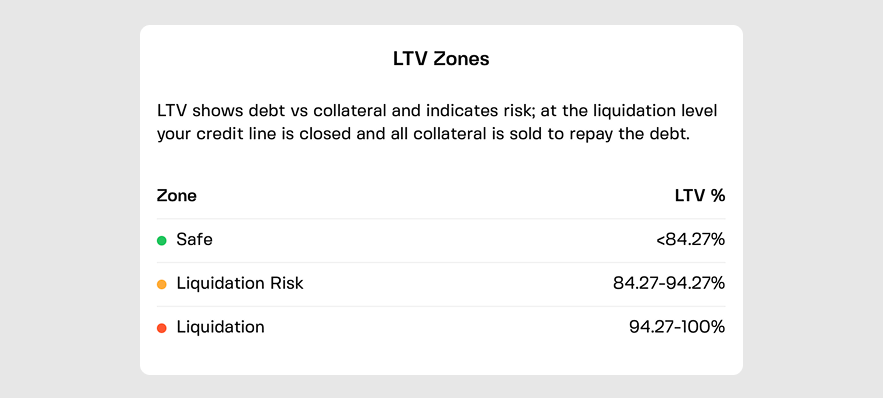

- Your Loan-to-Value (LTV) matters. This is the ratio of what you borrow to what your collateral is worth. Borrow $10,000 against $50,000 in BTC? That's 20% LTV — very safe. Some platforms even offer 0% APR at that level.

- Markets move. If your collateral drops in value, your LTV rises. You'll get a warning. Add more collateral or pay down part of the loan. Ignore it, and the platform may sell some to protect itself.

- You still have to pay it back. This isn't free money. The loan needs to be repaid. But unlike a term loan, a credit line lets you repay on your schedule — in full, in parts, whenever you're ready.

Credit lines vs. term loans

Not all borrowing is the same. Here's the difference:

- Traditional crypto loan: You borrow a lump sum. Fixed repayment schedule. Interest on the whole amount from day one. Collateral locked until it's paid off. Simple, rigid, predictable.

- Crypto credit line: You get a pre-approved limit. Draw only what you need. Pay interest only on what you use. Repay anytime, then borrow again. Flexible, adaptable, and — if you keep LTV low — sometimes 0% APR.

If you're funding a one-time purchase, a term loan might work. But if you want ongoing liquidity without selling your conviction, a credit line is a better fit.

Even more flexible: Multi-collateral credit lines

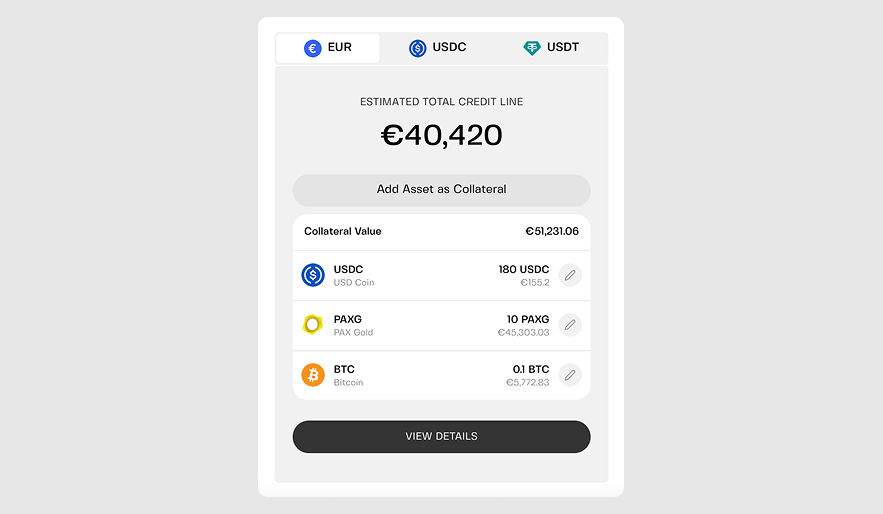

On Clapp, you can open a multi-collateral credit line using up to 25 different assets.

- Pledged BTC but want to swap to ETH? No problem — swap collateral anytime without closing your line.

- Keep your LTV at 20% or below? 0% APR. Your safety net costs you nothing until you use it.

- Need funds in a hurry? Draw EUR directly to your bank via SEPA, or take stablecoins straight into your Clapp Wallet.

The bigger picture

Crypto is maturing. It's no longer just "buy low, sell high." For long-term holders, it's becoming a real asset class — something to borrow against, earn yield on, and use without losing.

Selling crypto is permanent, the taxes are real, and those missed gains can haunt you. When borrowing, you keep your position and your upside. Get the cash you need without inviting the tax man to your next quarterly filing.

Next time you need cash, ask yourself: Do I really need to sell? Or is there another way?

There usually is.

Frequently asked questions

1. Do I really have to pay taxes every time I sell crypto?

In most countries, yes. Every sale, trade, or even swapping one crypto for another is considered a taxable event. You don't have to withdraw to your bank account — the moment you dispose of an asset, taxes can apply. The exact rate depends on where you live, how long you held it, and your income bracket. Some jurisdictions have allowances (like the UK's £3,000 tax-free), but beyond that, the tax man expects his cut.

2. How does borrowing avoid taxes?

Borrowing isn't a sale. You're not disposing of your crypto — you're using it as collateral to secure a loan. Since you still own the asset, there's no taxable event. Think of it like a home equity line of credit. You don't pay taxes when you borrow against your house. Same principle applies here.

3. What happens if my collateral value drops while I have a loan?

You'll get a warning. If the value of your pledged crypto falls, your Loan-to-Value (LTV) ratio rises. Most platforms notify you well before things get risky. You can then either add more collateral or pay down part of the loan to bring LTV back to a safe level. Ignore it, and the platform may sell your collateral to protect itself. Stay on top of it, and you're fine.

4. Is borrowing against crypto cheaper than selling?

Depends what you mean by "cheaper." Selling has immediate tax costs and the potential cost of missed upside if prices rally. Borrowing has interest costs — though some platforms offer 0% APR if you keep your LTV low. Compare that to handing 20–30% of your gains to the tax office, and borrowing often comes out ahead.

5. Can I use the borrowed funds for anything?

Absolutely. Once you draw from your credit line, the funds are yours. Pay for a business opportunity, cover an emergency expense, invest elsewhere, or just keep them liquid. There's no restriction. Just remember — you'll need to repay the loan eventually. Borrow responsibly.