The #1 mistake young crypto investors make

"Went all in on crypto at 22. Retired at 28." It's the dream, right? Skip the 9-to-5 grind, skip the decades of slow compounding. Just pick the right coins, hold tight, and let the magic happen.

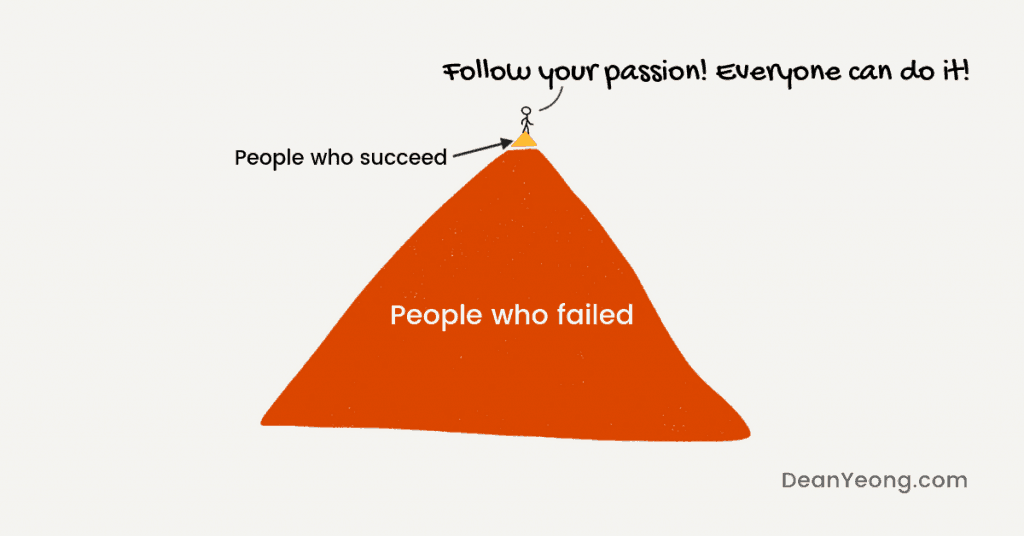

Yet behind these shiny facades, there is a graveyard of crypto portfolios that never took off. The people who went all in on projects that evaporated. The ones who bought the top and sold the bottom. You don't hear from them because they don't have a yacht to pose on.

The truth isn't nice to hear, but it must be known.

TL;DR

- Don't go all in on crypto. Even Bitcoin has dropped 80%+ before.

- 35% of Gen Z crypto investors have over half their portfolio in crypto. That's risky.

- Survivorship bias is real. You hear about winners, not the thousands who lost.

- 1%–5% in crypto is a conservative allocation; 5%–15% is aggressive.

Numbers that should make you pause

According to the World Economic Forum's 2024 Global Retail Investor Outlook, 35% of Gen Z crypto investors have allocated over half of their portfolios to cryptocurrency. For millennials, it's 26%.

Think about what these investors are actually doing. More than a third of them have most of their money in one of the most volatile asset classes on the planet.

Bitcoin has dropped over 70% multiple times before. Ether too. Smaller coins can go to zero and never come back. Here are the most recent bear market examples:

- 2013-2015: BTC slid 87% in a prolonged downturn worsened by China's ban and the collapse of Mt. Gox.

- 2017-2018: A year-long 84% decline following the launch of Bitcoin futures and China's regulatory crackdown.

- 2021-2022: BTC lost 77% overall following China's mining ban, Tesla suspending BTC payments, and domino-effect collapses of crypto firms after Terra Luna's depegging.

If you're in your 20s with 60% of your net worth in crypto, a bad bear market doesn't just hurt — it wipes out years of savings.

Survivorship bias trap

Here's a mental trick that gets almost everyone.

You hear about someone who put $5,000 into Dogecoin in 2020 and cashed out a million. You hear about the early Bitcoin adopter who bought at $10 and held to $60,000.

You don't hear about the person who put $5,000 into Terra Luna — the trigger of the 2022 market bloodbath. Or Celsius that followed in a domino effect. Or any of the hundreds of projects that have collapsed spectacularly.

Survivorship bias is about taking a cognitive shortcut — you only see the winners and assume their path was likely. It wasn't. For every crypto millionaire, there are thousands who lost money. You just never read their interviews.

Even Bitcoin — the king, the most established, the "safe" one — has seen 80% drawdowns. If you bought the top in 2017, you waited three years just to break even. That's a long time to hold when your rent depends on it.

Most cautious approach (boring but effective)

Here's what most financial advisors would tell you, and it's actually good advice:

Keep crypto to 1%–5% of your portfolio.

That's it — just a small slice. Not 50% or 100%. Crypto can still give you outsize returns even at 5%.

If your portfolio is $100,000 and you put $5,000 into BTC, and BTC does a 10x? That's $50,000 — half your original portfolio value. Life-changing money for many people.

But if crypto crashes 80% (which it has done, multiple times), you lose $4,000. That hurts, but it doesn't ruin you. You're still in the game.

How to get there without timing the market

"Okay, I want 5% in crypto, but prices are high right now. Should I wait for a dip?"

No. You should dollar-cost average.

Dollar-cost averaging (DCA) is simple: you invest a fixed amount at regular intervals, regardless of price. Weekly, bi-weekly, monthly — pick a rhythm and stick to it.

When prices are low, your fixed dollar buys more crypto. When prices are high, it buys less. Over time, this smooths out your entry price and removes the emotional weight of "did I buy at the worst possible moment?"

Say you want to build a $10,000 crypto position over a year. Instead of dumping all $10,000 in one go and praying, you split it into $833 monthly purchases. You'll catch some highs, some lows, and probably end up with a better average price than anyone who tried to time the perfect entry.

On some apps, you can set up recurring buys to automate this.

What a balanced portfolio looks like

There's no single "right" portfolio for everyone — it varies greatly depending on who you ask.

- BlackRock suggests a modest allocation of 1% to 2% in BTC for most multi-asset investor portfolios — "if investors believe it will become more widely adopted and can bear the risk of potentially rapid price plunges."

- According to Bitwise, "optimal allocation ranges consistently fall between 4-6% for Bitcoin and 4-5% for diversified crypto baskets."

- Ric Edelman, head of the Digital Assets Council of Financial Advisors, has called for 10%-40% crypto allocations, citing “the evolution of crypto in the past four years,” making it a "mainstream asset."

For most people, a 1%–5% allocation is a conservative baseline. If you have higher risk tolerance and understand the volatility, 5%–15% can be reasonable. It's still meaningful — you'll feel the upside if it rallies, but you won't be destroyed if it crashes.

Combining products to build smarter

HODLing is not the only way to benefit from upswings. Many platforms now offer ways to earn yield, diversify, or borrow against your crypto. Treat these tools as extensions of your crypto allocation — not substitutes for diversification.

For instance, here is how this works on Clapp:

- Flexible Savings earns yield on crypto, stablecoins, or fiat while you wait, without lockups.

- Fixed Savings reward you with premium yield (up to 8.2% annually) for committing to a specific period (usually between 1 month and 1 year).

- Portfolios let you diversify across multiple assets with one click.

- Credit lines give you liquidity without selling your position.

You don't have to go all in. You just have to be smart about what you hold and how you use it.

What to do with the rest of your money

Young investors have a massive advantage: time.

Say you're 25 and put $10,000 into a boring stock index (S&P 500) that averages 10.86% annually. Here's what historical averages suggest by age 65:

- No additional contributions: $10,000 becomes about $584,000

- Add $500 a month: you're looking at roughly $3.78 million.

Based on the S&P 500's 10.86% compound annual growth rate over the past 34 years (1990–2024). Past performance doesn't guarantee future results — this is just an illustration, not a promise.

That's not sexy. It doesn't make for good tweets. But it works, and it doesn't require you to stare at charts at 2 a.m.

You don't have to choose between crypto and stocks — do both, just don't bet the farm on one horse.

Going all in is the number one mistake

Not because crypto is bad, but because putting half your net worth into anything that volatile is risky.

Keep most of your money boring. Keep a small slice exciting. And let the boring part quietly compound while you sleep.

The people who win over the long term aren't the ones who got lucky once. They're the ones who stayed in the game, diversified, and let time do its work.

You can be one of them. Just don't bet everything on a moonshot.

Frequently asked questions

1. Isn't crypto different from stocks? Won't it 100x while stocks only do 10% a year?

Maybe. But "maybe" isn't a plan. Crypto could 100x. It could also drop 90% and stay down for years. Stocks have a century of historical data showing steady compounding. Crypto has hype cycles and crashes. The smart move isn't choosing one — it's owning both, but keeping the risky part small enough that you can sleep at night.

2. I'm young. Shouldn't I take more risk?

Yes — but there's a difference between smart risk and gambling. Being young means you can afford volatility, not that you should bet your entire net worth on a single asset class. A 25-year-old with 10% in crypto and 60% in stocks is still taking plenty of risk. They're just not risking everything.

3. What if I missed the boat on stocks and need crypto to catch up?

That's fear talking, not math. Missing out on past gains doesn't mean you need to overcompensate with extreme risk now. The stock market will be there for decades. Start investing what you can, consistently, and let time do its thing. Crypto can be part of that — just not all of it.

4. How do I actually build a balanced portfolio?

Start simple. For instance, one might open a retirement account (IRA, 401k, or your country's equivalent) and consider putting money into a low-cost S&P 500 index fund. Set up automatic monthly contributions. Then, separately, put a small amount into crypto — 5%–15% depending on your comfort. Rebalance once a year. Don't overcomplicate it.

5. What about stablecoin yield? Doesn't that change the risk calculation?

Stablecoin savings (5%–8% APY) are less volatile than holding BTC or ETH directly. That's good. But they still carry platform risk — no FDIC insurance, and not all platforms are licensed or trustworthy. You can use them as part of your crypto allocation, but don't confuse "less volatile" with "safe." Diversify there too.