The truth about earning interest on crypto (worth it or not?)

You've seen the headlines: "Earn 5%, even 15% APY on your crypto!" It sounds like free money compared with a bank account paying 0.01%.

People are earning yield on crypto, but there’s always a catch. Some platforms deliver, others don’t. Some strategies are simple, others require a PhD in DeFi to understand.

Let’s cut through the noise.

TL;DR

- You can earn interest on crypto by staking, lending, or supplying liquidity.

- APYs often beat traditional savings, but they come with higher risk.

- The yield usually comes from borrowers, staking rewards, or trading fees.

- Lock-ups, smart contract risk, and taxes are important to understand first.

- It’s a way to accumulate more crypto over time — not a shield against price drops.

How does interest on crypto work?

It's simpler than it sounds. Think of it like a savings account — but for digital assets.

Instead of leaving crypto idle, you deposit it on a platform to grow. Your coins stay yours; interest is added regularly.

You'll usually see this advertised as APY (Annual Percentage Yield) rather than APR (Annual Percentage Rate).

APY includes compounding — meaning your interest earns interest. That 5.2% APY on stablecoins will actually grow faster than a simple 5.2% APR would suggest.

Strategies range from complex DeFi lending to simple savings products on centralized platforms:

- Staking — Lock assets to help secure blockchain networks in exchange for rewards

- Centralized savings — Simple deposit accounts where the platform handles the rest

- DeFi lending — Deposit into smart contracts that lend your assets to borrowers

- Liquidity pools — Provide funds to decentralized exchanges and earn a cut of trading fees (e.g., yield farming strategies).

Why people are doing it

For many, these products have worked well. For disciplined investors who understand the risks, it's been a legitimate way to beat traditional finance at its own game.

No trading or market timing. Just steady accumulation while still benefiting from price rallies.

Where the yield actually comes from

Crypto interest isn’t created out of thin air. The yield usually comes from one of three sources.

- Borrowing demand. Many platforms lend deposited crypto to traders who want to use leverage. Because crypto markets move quickly, traders are often willing to pay high borrowing rates.

- Blockchain rewards. Some assets generate yield through staking. By locking tokens to help secure a network like Ethereum, participants receive newly issued coins and transaction fees.

- Trading activity. In DeFi exchanges, liquidity providers earn a portion of trading fees when users swap assets in liquidity pools.

The platform simply distributes a share of these revenues back to depositors.

Getting started is easy

With the simplest option — savings products — the process is refreshingly boring, which is exactly the point.

1. Pick a platform that offers crypto earning

Not every exchange does this. You'll want one that supports earning on assets you actually hold — typically, BTC, ETH, stablecoins, or fiat.

2. Add your crypto

Buy directly on the platform or transfer assets from elsewhere. It’s as quick as sending an email.

3. Decide: flexible or fixed?

Some accounts let you pull your money out anytime. Others lock it for a set period in exchange for higher rates. Your call.

4. Start earning

Once your crypto lands, it usually begins earning within 24 hours. Interest might hit your account daily, weekly, or at the end of a fixed term — depends on the product you choose.

Now read the fine print

Here is where the "truth" gets complicated.

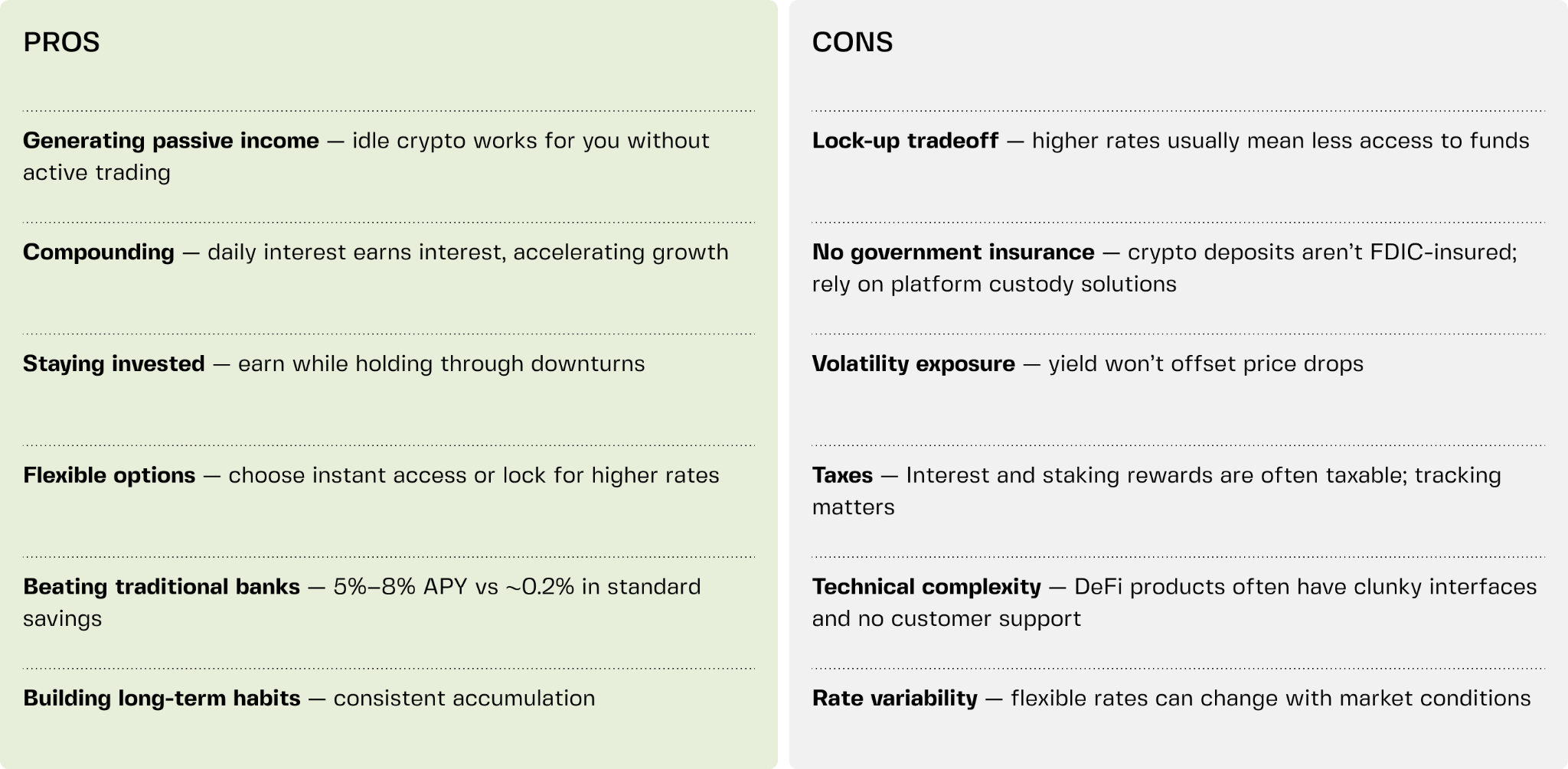

First, volatility doesn't pause while you earn. A 5% yield won’t offset a 40% drop; you’re still exposed. Interest is a strategy, not a shield.

To get the highest yields, you're often dealing with complex DeFi protocols. Not only are the interfaces clunky — the entire industry remains largely unregulated. There's no legal recourse if a smart contract bug or hack affects your holdings.

The next truth bomb is about lock-ups. Many platforms offer attractive rates if you agree not to touch your money for 90 days. In crypto markets, 90 days can feel like an eternity. If the market crashes, you cannot sell. You're trapped.

Taxes get complicated. In many places, interest earned on crypto counts as taxable income. Staking rewards too. It's not a reason to avoid earning — just something to factor in, ideally with help from someone who knows what they're doing.

Finally, insurance. Unlike traditional banking, there's no FDIC protection for crypto deposits. Make sure the platform you choose is licensed, regulated, transparent, and uses multi-layer security protections — not just 2FA. Ideally, you want one that's boring in all the right ways.

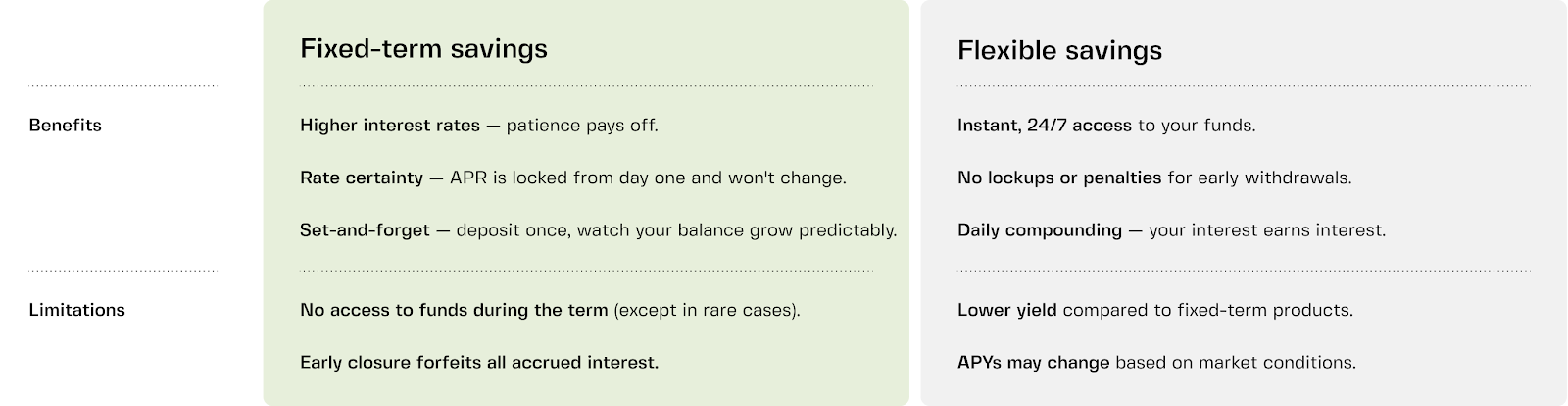

Flexible vs. fixed crypto savings

Not all earning products are the same. The big fork in the road comes down to one question: Do you need access to your crypto, or can you lock it away?

Flexible savings — earn while staying liquid

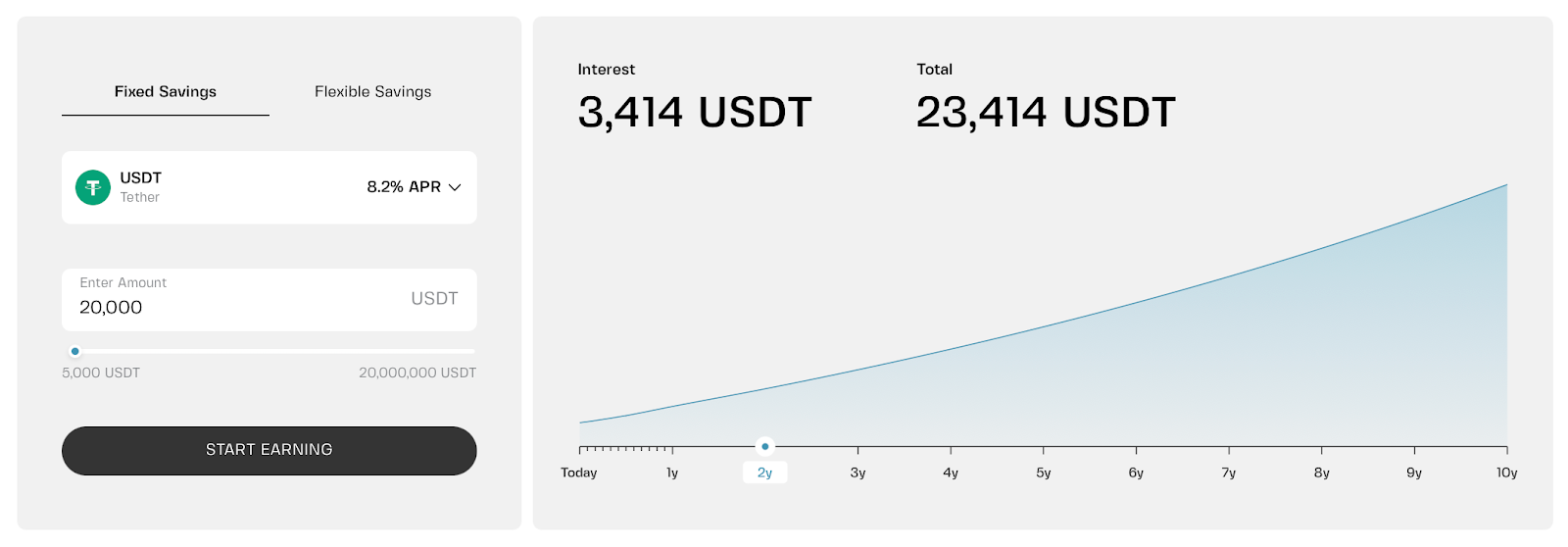

This is the "keep your options open" approach. Your crypto or fiat stays accessible — withdraw, swap, or move it anytime. Interest lands in your account daily and compounds, so yesterday's earnings start earning today. On Clapp, stablecoins and EUR earn up to 5.2% APY.

Fixed savings — higher rates for longer commitments

This one's for the true long-term believers. You lock your crypto for a set period — 1, 3, 6, or 12 months — and in exchange, you get a premium rate locked from day one. Interest may pay out at maturity or monthly, depending on the provider.

No matter what the market does, your return is locked. On fiat and stablecoins, returns can reach 8.2% APR.

Why not use both?

Flexible Savings is for money you might need. It's your emergency fund, "just in case" stack, or dry powder.

Fixed Savings is for the part of your portfolio you're confident won't be touched for a while. The trade-off is simple: less access, more yield.

Many holders do both. Keep some in Flexible for agility, lock the rest in Fixed to capture those higher rates. There’s no rule saying you have to pick just one.

Why bother during a down market?

Fair question. If prices are sliding, what's the point of earning a few percent?

- Holding feels better when it's productive. Even slow growth makes the waiting easier while the market does whatever it’s going to do.

- Interest can soften the sting of volatility. It won't cancel out a 30% drop. But over time, those steady additions add up, helping when the cycle turns.

- No timing required. Nobody knows when the bottom hits. Earning interest keeps you invested without second-guessing, no “should I sell?” or “buy back in?” — just steady accumulation.

- It builds a habit. For some, the real win isn't the yield — it's the discipline. Setting up a system where your crypto works for you, month after month, regardless of what the news says.

Turn waiting into a strategy

When markets are shaky, holding can feel like doing nothing. Earning interest flips that script.

Flexible Savings keeps you nimble. Fixed Savings rewards conviction. Both let you stay in the game — accumulating, building, letting time do its thing — while everyone else tries to time the perfect entry.

The market will recover eventually. It always has.

The question is whether you'll have more crypto when it does.

Frequently asked questions

1. Is earning interest on crypto safe?

It depends on the platform and how you do it. Centralized platforms with proper licenses, regulation, and institutional-grade custody (like Fireblocks) are generally safer than chasing 15% yields from unknown DeFi protocols. Your crypto is never 100% risk-free, but choosing a transparent, boring platform reduces the gamble significantly.

2. Can I withdraw my crypto anytime?

With Flexible Savings, yes — usually instantly, 24/7, with no penalties. With Fixed Savings, your crypto is locked until the term ends (1, 3, 6, or 12 months). Early withdrawal may not be possible, or could forfeit all earned interest. Always check the terms before you commit.

3. How are platform products different from staking?

Staking is one specific way to earn yield — you lock assets to help secure a blockchain network (like Ethereum or Solana) and receive rewards. Earning interest on platforms is broader: it can include staking, but also lending your crypto to borrowers or providing liquidity. Savings products often bundle these strategies behind the scenes so you don't have to manage them yourself.

4. Do I have to pay taxes on crypto interest?

In most countries, yes. Interest earned, staking rewards, and other yield are often treated as taxable income — even if you haven't sold anything. Rules vary by jurisdiction, so it's worth checking with a tax professional who understands crypto. Don't let the tax tail wag the investment dog, but don't ignore it either.