Wall Street on-chain: Tokenized securities boom explained

As crypto grapples with declining market cap and falling prices, the SpaceX IPO has turned tokenized stocks into its hottest sector. With equities racing to fresh highs, the gap between the two markets has rarely been wider. Here's a deep dive into tokenized securities and the factors helping them pull in crypto liquidity.

TL;DR

- Tokenized securities are traditional assets (stocks, ETFs, bonds) issued as blockchain-based tokens, similar to stablecoins but with price appreciation and yield potential.

- Key advantages include 24/7 trading, faster settlement, lower costs, greater transparency, and broader accessibility compared to traditional markets.

- Owning the token doesn't automatically mean you legally own the security. The official record of who owns what is kept by the issuer (via a transfer agent), not on the blockchain.

- Issuer-sponsored tokens give holders the same legal rights (voting, dividends) as traditional shareholders; the only difference is record-keeping on-chain.

- Custodial third-party tokens give indirect exposure through a custodian, but holders face additional risks like bankruptcy or custody failure.

- Synthetic third-party tokens give no rights against the underlying company (no voting, no dividends) and expose holders to the credit risk of the third-party issuer.

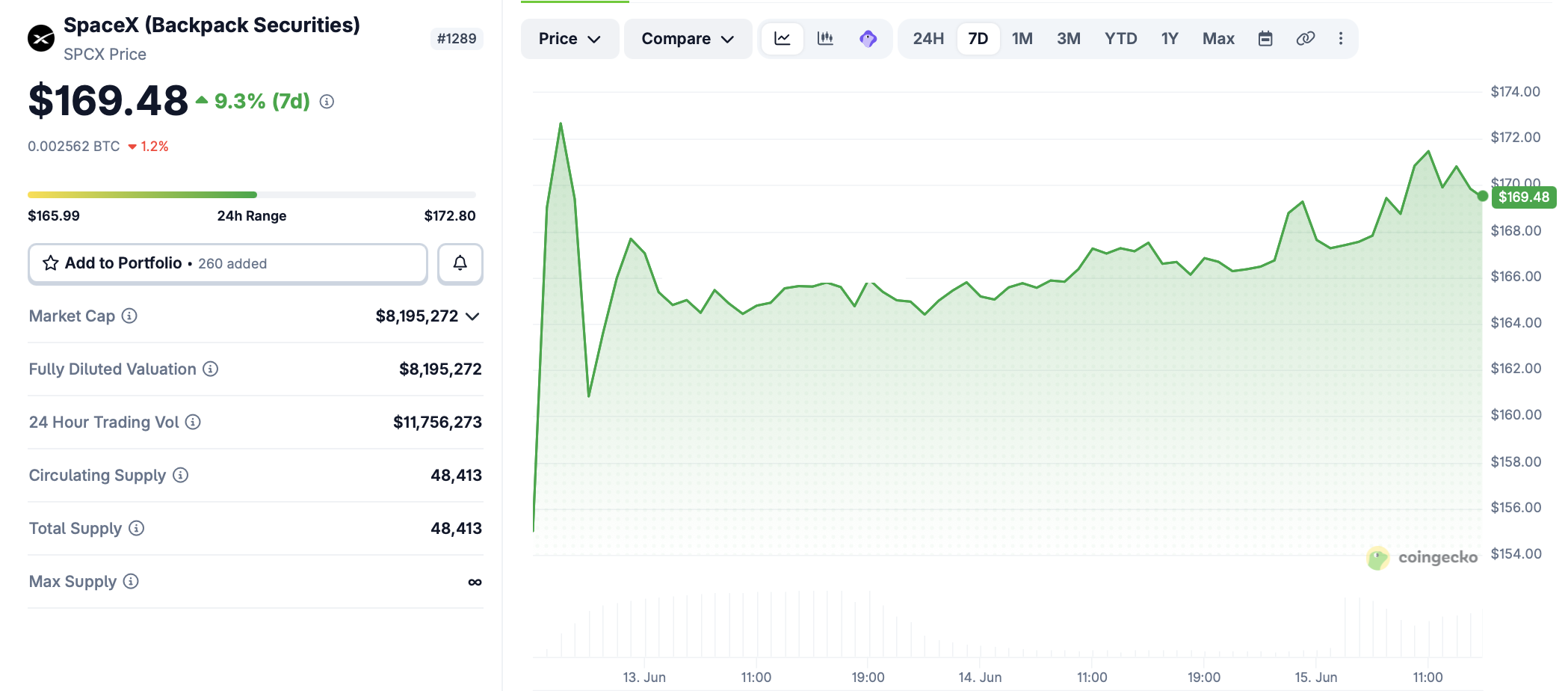

SpaceX fuels tokenization frenzy

SpaceX's debut on Nasdaq sparked demand across crypto-linked stock products. With its valuation lifted above $2 trillion, the $75 billion IPO threatens to pull capital from risk assets across the board.

Traders rushed into tokenized shares, synthetic assets, and derivatives, with providers like Hyperliquid, Binance, and Backed Finance emerging as early beneficiaries.

SPCX, collateralized 1:1 by actual SpaceX shares held in regulated custody, began trading on Solana the same day the company listed on Nasdaq. The token bridges traditional and decentralized markets, allowing holders to convert between tokenized exposure and real-world shares.

The launch brought newly listed US equities on-chain from day one. Meanwhile, XStocks and Backed Finance launched SPCXx, another fully backed tokenized version of SpaceX equity.

What are tokenized securities?

Tokenized securities — for instance, stocks, ETFs, and bonds — sit within the broader category of tokenized real-world assets. Like tokenized commodities or works of art, they represent traditional financial instruments issued on-chain as digital tokens.

In some ways, the concept is similar to stablecoins like USDT — digital tokens pegged to fiat currencies or commodities and backed by real-world cash or short-term assets. The key difference is that they can appreciate and pass through yield from the underlying assets, whereas stablecoin issuers like Circle or Tether typically retain that yield.

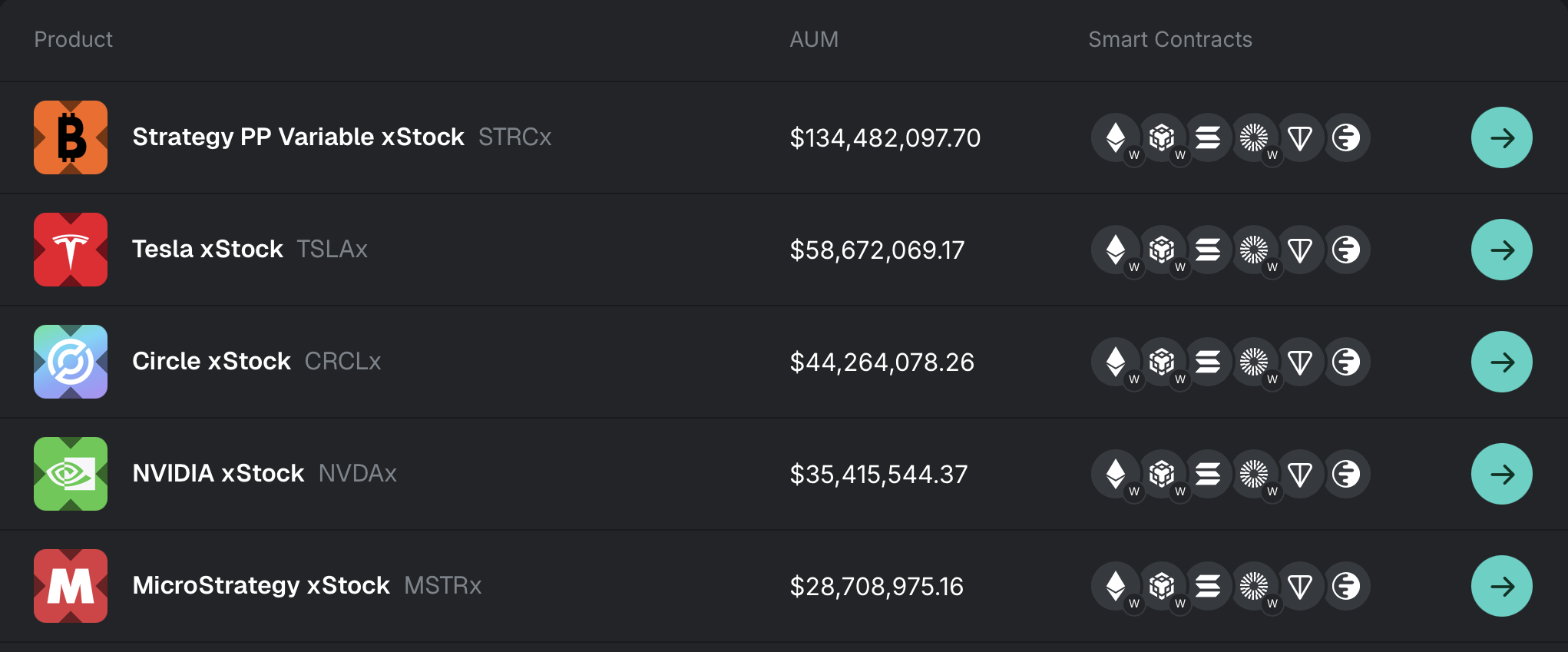

A simple example is Backed Finance, which offers tokenized exposure to stocks like Alphabet (GOOGLx), Nvidia (NVDAx), Amazon, and Tesla (TSLAx), with underlying securities held in custody by regulated entities. Its flagship tokenized asset product line is called xStocks.

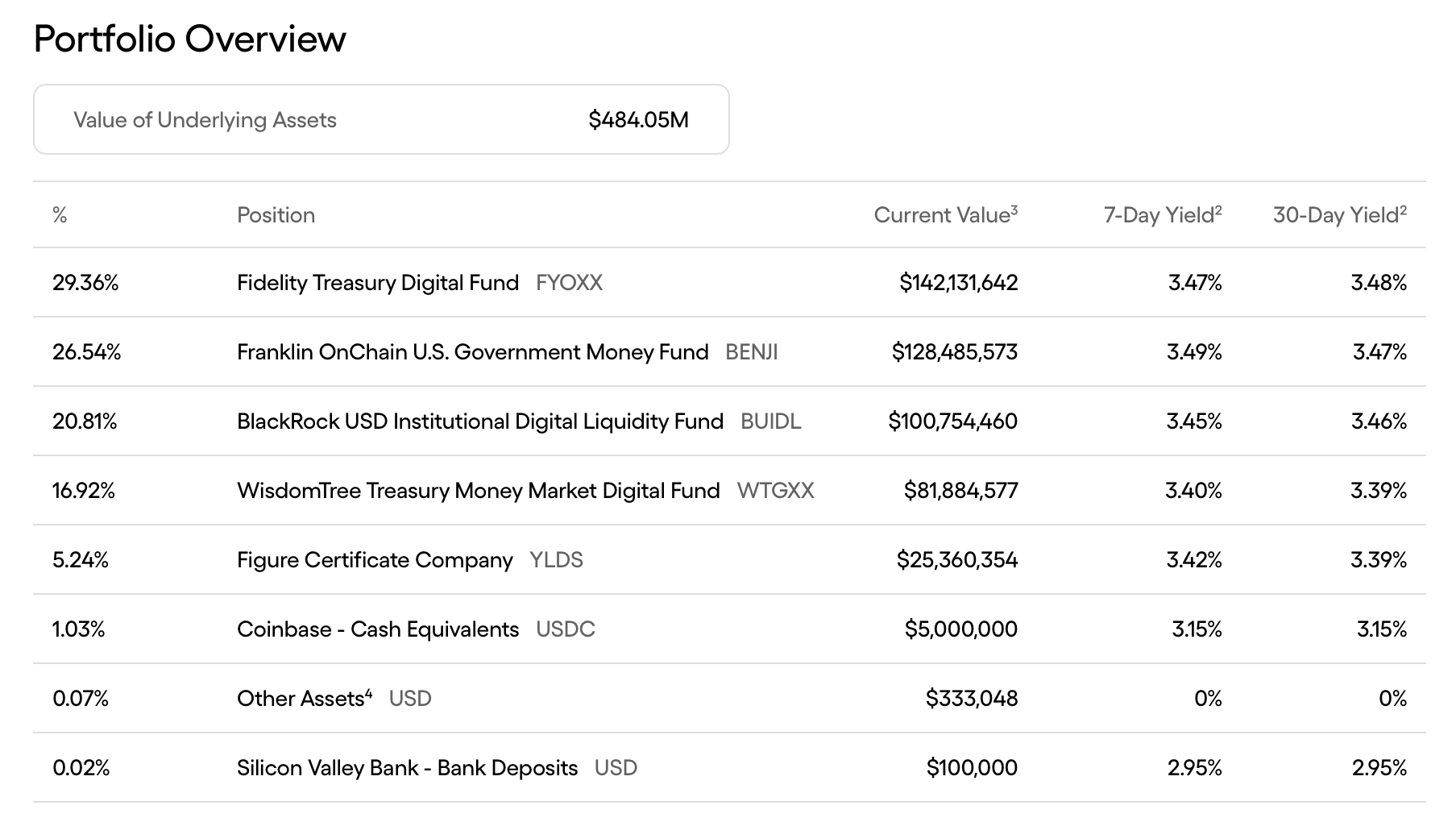

Meanwhile, the Ondo Short-term US Government Bond Fund issues the OUSG token, which represents a claim on the underlying portfolio and its yield stream. The fund holds BlackRock’s BUIDL fund (investing in US Treasury bills and cash equivalents), along with allocations to Franklin Templeton, WisdomTree, Fidelity, and other vehicles. Through OUSG, investors can earn without holding traditional fund shares.

The category extends well beyond equities and ETFs. Tokenized bond funds, credit products, and even real estate exposure are emerging on-chain. Instead of buying units in a real estate investment trust (REIT), investors can, in some cases, hold tokenized versions of similar structures directly in a crypto wallet.

Important note: Do not confuse tokenized securities with perpetual futures. Perpetuals are leveraged synthetic price bets, while tokenized securities are real-world assets represented on-chain with ownership and cash-flow rights. For a deeper dive, see our in-depth guide to crypto perpetuals.

Now zooming out to how this market actually works in practice.

Advantages of tokenized securities

In practice, tokenized securities aim to bring traditional financial assets into crypto-native infrastructure. In markets where valuations are often speculative, they introduce a cash-flow-linked layer of value, while also reducing settlement friction and improving liquidity.

Because they trade on blockchain rails, they can operate 24/7 and settle faster than traditional brokerage systems. In effect, they behave like crypto-native instruments with traditional asset backing — tracking ownership on-chain, but still governed by conventional securities rules.

This market is growing rapidly, driven by new use cases and a set of practical advantages for both issuers and investors. The former benefit from management fees and broader distribution, often with lower issuance and operational costs. Holders, in turn, gain access to several structural advantages:

- Superior liquidity compared to traditional markets, with trading available 24/7, without weekends or bank holidays.

- Broader accessibility, allowing smaller investors to gain exposure to assets that were previously out of reach, although some platforms still set high minimums for token issuance — in some cases up to $100,000.

- Lower transaction costs, as blockchain rails can reduce friction compared to traditional financial infrastructure, even accounting for Ethereum gas fees, which have declined following recent network upgrades.

- Greater transparency, with issuers able to publish frequent asset disclosures that can be verified across both on-chain and off-chain records.

- More reliable collateral for borrowing, since tokenized securities tend to be less volatile than assets like Bitcoin, making them more attractive in lending markets.

- Yield opportunities, where certain tokenized securities allow holders to earn returns linked to the underlying asset — often with more stable, cash-flow-based returns than crypto staking rewards. For instance, OUSG provides net return of the underlying portfolio, minus management fees charged by Ondo and any underlying fund expenses.

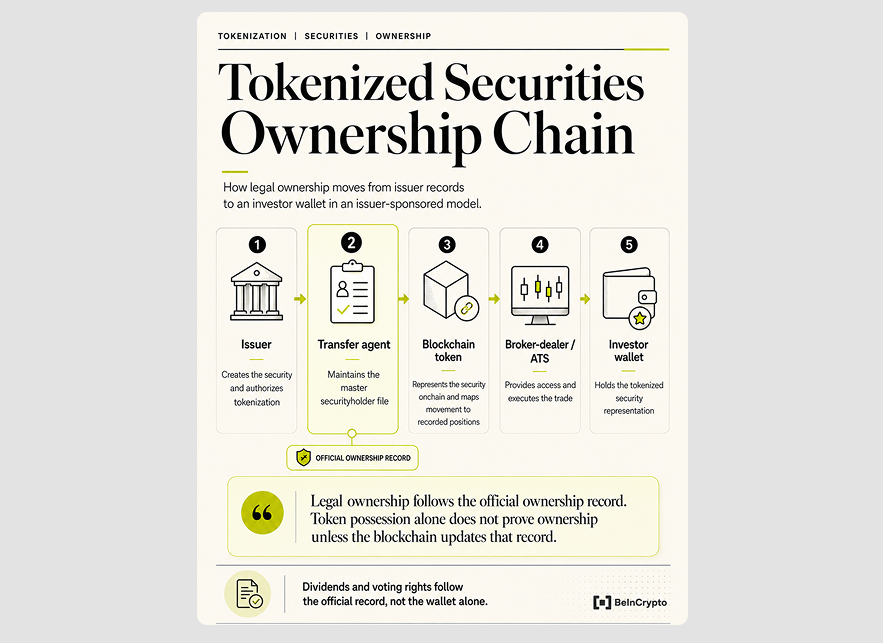

How does tokenized securities ownership work?

The ownership process revolves around a crucial intermediary: the transfer agent. This is the entity that manages the administrative layer, maintaining the issuer's securityholder file — the official record of who legally owns a security. The agent is also empowered to cancel or issue certificates and distribute dividends.

To understand the system, it helps to first separate the roles involved from the actual transaction flow.

The ecosystem includes six core actors:

- Issuer creates the security and authorizes tokenization

- Transfer agent maintains and updates the master securityholder file

- Blockchain records asset movement and may update ownership records if integrated as the official system of record

- Broker-dealer or alternative trading system (ATS) provides trading access and executes transactions

- Custodian holds tokenized securities or entitlements in certain models

- Investor wallet stores the token or tokenized representation; it does not itself establish legal ownership unless the blockchain is recognized as the official record

The official ownership record is ultimately controlled by the issuer, the transfer agent, and — in some setups — the blockchain if it is integrated into the system of record.

Once those roles are clear, the actual flow becomes easier to follow:

- The issuer creates a tokenized security and appoints a transfer agent.

- The transfer agent establishes or connects the master securityholder file to a blockchain network.

- The issuer mints tokens that correspond to the ownership positions recorded in that file.

- An investor purchases the tokens through a broker-dealer or ATS.

- Once the transaction settles, the transfer updates the master securityholder file and links the ownership record to the investor's name, address, and wallet.

- Voting rights, dividends, and other corporate actions are then administered based on the official ownership record and the associated wallet.

One important nuance: if the blockchain is not integrated into the official record system, the final ownership updates may still be handled manually.

Regulation of tokenized securities

Most regulators follow a "substance over form" approach. This means that a token that functions as a security is generally subject to the same securities laws as its traditional counterpart.

In the EU, tokenized securities are generally regulated under existing financial services rules, including MiFID II, rather than MiCA. The Markets in Crypto-Assets Regulation primarily applies to crypto-assets that do not qualify as financial instruments.

In practice, regulators tend to focus less on the technology itself and more on the rights attached to the asset.

How SEC treats tokenized securities

In the US, the SEC requires all securities to be registered, tokenized or not. It defines a tokenized security as follows:

"A financial instrument enumerated in the definition of “security” under the federal securities laws that is formatted as or represented by a crypto asset, where the record of ownership is maintained in whole or in part on or through one or more crypto networks."

It distinguishes between two categories of assets:

Issuer-Sponsored Tokenized Securities

These are tokenized by or on behalf of the issuers of such securities. All registration, disclosure, and reporting requirements apply as if the security were in traditional paper form. Holders have the same legal rights and obligations as traditional security holders (e.g., voting, dividends, etc.). The primary difference lies in how ownership records are maintained.

Third Party-Sponsored Tokenized Securities

These are tokenized by third parties unaffiliated with an issuer. Two primary models exist:

- Custodial. The issuer holds the actual underlying security in custody and mints a token representing an indirect interest (like a security entitlement). This format does not change the underlying regulatory treatment, but holders face additional risks related to the third party (e.g., bankruptcy, custody failure).

- Synthetic. A third party issues its own security (a linked note or a swap) that provides synthetic exposure to another issuer’s security. These instruments are regulated as separate securities (linked securities or security-based swaps). Holders have no rights against the other issuer (no voting, no dividends, no information rights), and they are also exposed to the credit risk of the third-party issuer.

Wrapping up

Tokenized securities bridge traditional finance with blockchain rails in one of crypto’s most practical sectors. Unlike speculative assets, they offer stable yield and lower volatility, all while remaining firmly under existing securities regulations.

The SpaceX IPO has intensified interest, with products like SPCX and Backed Finance’s xStocks bringing equities on-chain almost instantly.

That said, ownership and legal rights depend critically on the structure. As regulators like the SEC apply a “substance over form” approach, investors must look past the token format to understand who the issuer is, what rights they actually hold, and where the risks truly lie.