What happens when you borrow against crypto and the market crashes overnight

You borrowed $15,000 against your crypto at low rates and felt comfortable with the decision.

Then you woke up to a market crash.

The charts are a sea of red candles. Your portfolio is down 30%. Your phone is buzzing with alerts you had never seen before. "Margin call." "LTV threshold exceeded." "Action required."

Suddenly, that smart move felt different.

Let's walk through what actually happens when markets turn against you, how to spot the danger before it arrives, and what to do when the "nightmare scenario" is unfolding in front of your eyes.

TL;DR

- Crashes don't just hurt your portfolio — they trigger loan risks you might not have considered.

- Your LTV rises as your collateral falls. A 40% crash can turn a safe loan into a liquidation risk.

- You'll get warnings. Most CeFi platforms send margin calls before liquidating. Don't ignore them.

- You have options. Add collateral, pay down the loan, or in some cases, swap assets.

- Panic is the real enemy. A clear plan beats raw emotion every time.

The anatomy of a margin call

Let's start with a simple example.

You deposit $50,000 in Bitcoin as collateral to borrow $15,000. Your LTV (loan-to-value ratio) is 30% — very safe territory. You're not worried.

Then the market crashes 40% overnight. That Bitcoin is now worth $30,000. Your loan is still $15,000. Your LTV just jumped to 50%.

You're not liquidated yet, but you're closer. And the market might not be done falling.

This is where collateralized borrowing starts to feel very different from simply holding crypto. That's when people panic.

They watch their LTV climb and imagine losing everything. They make rushed decisions — adding collateral they can't spare, selling other assets at a loss, or worse, doing nothing and hoping.

What actually happens when you get a margin call

First, you'll get a notification. Usually by email, push alert, or both.

It will say something like: "Your LTV has exceeded the safe threshold. Add collateral or repay part of your loan within 24 hours to avoid liquidation."

You have time. Most CeFi platforms give you a grace period — typically 24 to 72 hours, depending on the lender. Some offer less, some offer more. But you're not getting liquidated the second the market moves.

Your options:

- Add more collateral. Transfer additional crypto to your collateral pool. This lowers your LTV immediately.

- Repay part of the loan. Pay down what you owe using cash or stablecoins. This also brings LTV back down.

- Swap collateral (if your platform allows it). Replace a dropping asset with a more stable one.

- Do nothing. If you ignore the warning and the market keeps dropping, the platform will liquidate your collateral to cover the loan.

What liquidation looks like

The platform sells a portion — or all — of your collateral at market price. Often during a crash, when prices are at their worst. You keep whatever is left after the loan is repaid.

Plus, some platforms charge a liquidation fee. So you lose twice: sold low, then charged for it.

Two borrowers, same crash, different outcomes

Borrower A: Deposited $50,000 in BTC. Borrowed $10,000 at 20% LTV. Didn't panic. Had $5,000 in stablecoins set aside. Got the alert, added collateral, and rode out the storm.

Borrower B: Deposited $50,000 in BTC. Borrowed $25,000 at 50% LTV. No backup plan. Got the alert at 2 a.m., froze, did nothing. Woke up to a liquidation notice. Lost a chunk of their Bitcoin at the worst possible moment.

Same crash. Same asset. Completely different results.

The difference wasn't luck. It was preparation.

How to prepare before the crash

You can't predict the next crash. But you can prepare for it.

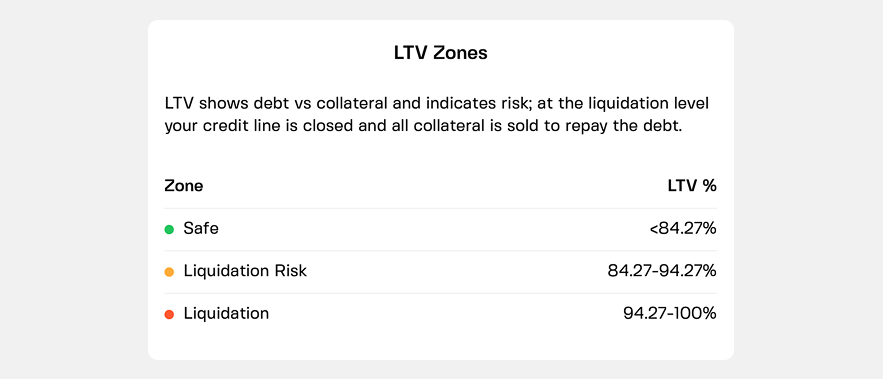

Keep LTV low from the start. 20-30% is the sweet spot. At 20% LTV, Bitcoin needs to drop about 75% to liquidate you (assuming an 80% liquidation threshold). Even in extreme events like March 2020, Bitcoin’s worst single-day moves have been on the order of ~40–50%, not catastrophic 70–80% collapses.

Have extra collateral ready. Keep stablecoins in a flexible savings account (so you can withdraw anytime) or more BTC on the side. When the margin call comes, you'll be glad you did.

Know your platform's rules. What's the LTV threshold for warnings? For liquidation? How long do you have to act? Read before you borrow. On many platforms, the liquidation threshold sits somewhere between 80% and 90%.

Set your own alerts. Don't rely on the platform alone. Set price alerts for your collateral assets. Know when you're getting close to danger before the platform tells you.

What to do if the crash is already happening

Don't panic. You have time — usually. Most centralized lenders send warnings before liquidation, though the exact timeline depends on the platform.

- Check your LTV right now. How close are you to the liquidation threshold? If you're at 70% and the threshold is 80%, you have some room. If you're at 78%, act fast.

- Add collateral if you can. Transfer stablecoins or other assets to your collateral pool. This is the quickest way to lower your LTV.

- Repay part of the loan. If you have cash or stablecoins, pay down what you owe. Every dollar repaid lowers your LTV.

- Consider swapping collateral (if your platform allows it). Some platforms let you swap depreciated assets for stablecoins within your collateral pool. This can stabilize your LTV without adding new funds.

- If you're out of options, do a partial repayment. Even paying back 10-20% of the loan can buy you breathing room.

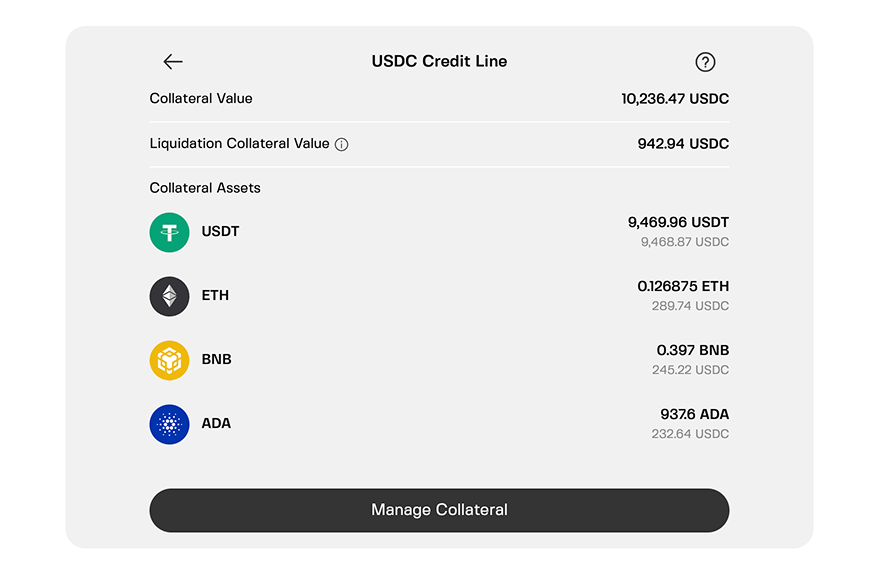

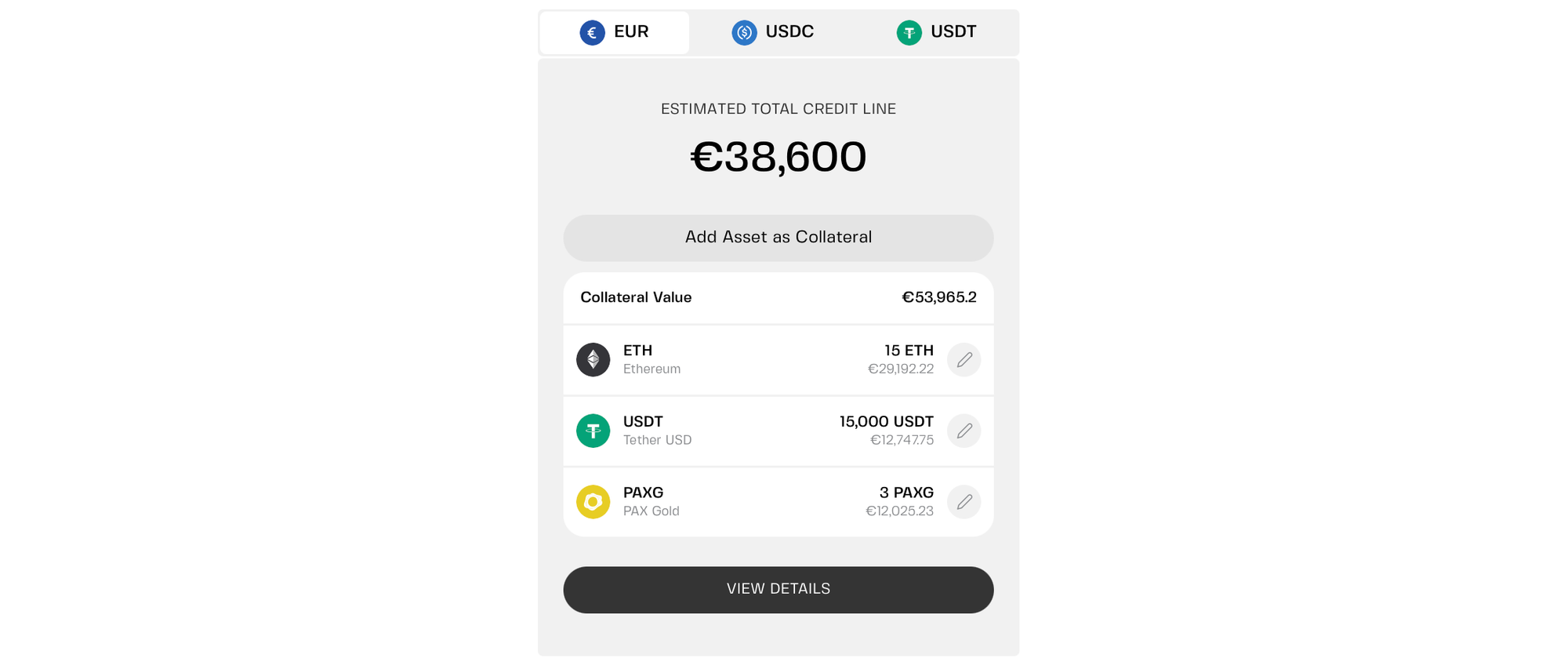

How credit lines change the equation

A traditional loan locks your collateral until you repay. A credit line is more flexible.

With a credit line, you can add or swap collateral without closing your position. That means when markets crash, you have more tools to respond.

On some platforms, you can even keep LTV at 20% or below and pay 0% APR. That's breathing room — and it doesn't cost you interest while you wait.

Platforms like Clapp also let you mix multiple assets in your collateral pool. If Bitcoin slips, you can easily add stablecoins to buffer your LTV. If you're anxious about future price swings, you can swap some volatile assets for more stable ones without closing your line.

What not to do

- Don't ignore the warning. Hoping the market rebounds before the timer runs out is not a strategy. It's gambling.

- Don't add collateral you can't afford to lose. Only use funds you have set aside for this purpose. Don't empty your emergency fund.

- Don't borrow more to cover the loan. That's called digging a deeper hole. It rarely ends well.

- Don't panic-sell other assets. Selling your Ethereum at a loss to save your Bitcoin might just shift the problem elsewhere.

Crashes don't have to destroy your loan — or your peace of mind

Know your platform's rules. Borrow conservatively, keep LTV low, and always have a backup plan. And when the red candles come, don't panic. You've already prepared for this moment.

The crypto market has weathered dramatic downturns before. Our guide to Bitcoin's 10 biggest crashes shows just how brutal some of them were. The key is making sure a dip doesn't force you out of your position at the worst possible moment.

Frequently asked questions

1. How fast can a margin call happen?

On CeFi platforms, you usually get 24 to 72 hours to act, depending on the lender. On DeFi, liquidation can be instant — no warning, no timer. That's a big reason beginners often start with CeFi.

2. Can I lose more than my collateral?

In most retail crypto-backed loans, your losses are limited to the collateral you pledged. The platform sells collateral to repay the loan, so you typically don't owe additional funds. Check your lender's terms to confirm how liquidations are handled.

3. What's the safest LTV to survive a crash?

20% LTV is very safe. Bitcoin would need to drop about 75% to liquidate you — the market has never seen a single plunge that deep. 30% is still reasonable. 50% or higher puts you at serious risk during normal bear markets.

4. Do I get anything back after liquidation?

Whatever remains of your collateral after the loan is repaid. If you had $50,000 in BTC, borrowed $25,000, and got liquidated when your collateral hit $28,000, you would get back about $3,000 minus any fees. It's not nothing, but it hurts.

5. Should I avoid borrowing altogether if I'm worried about crashes?

Not necessarily. You just need to borrow conservatively and have a plan. Many people borrow at 20-30% LTV, keep stablecoins as a buffer, and sleep fine through crashes. The problem isn't borrowing — it's over-borrowing.