Why earning 5% isn't really earning 5% (APR vs. APY explained)

What does earning 5% on crypto actually mean? You might think: “That’s $50 on every $1,000 I deposit.”

But it’s not that simple.

The difference between APR and APY changes what you actually earn. And depending on how interest is calculated, the same 5% can produce very different outcomes over time.

Let’s break down the difference so you can spot it before you lock up your funds.

TL;DR

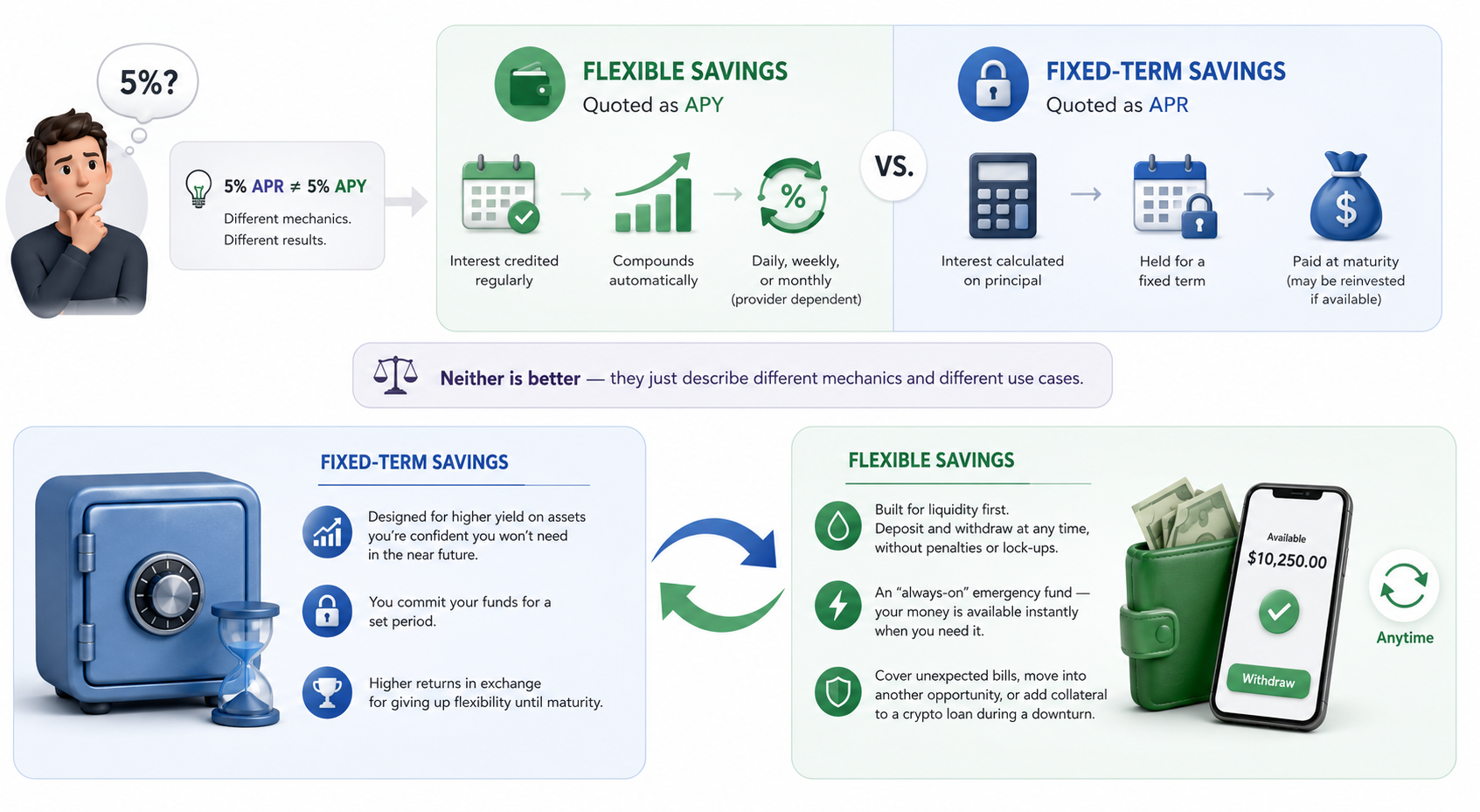

- APR is simple interest. It doesn’t include compounding. The rate is applied to your original deposit only.

- APY includes compounding. Interest earns interest over time, reflecting your actual annual return.

- APR is lower than APY when compounding is factored in. The more frequent the compounding, the bigger the gap.

- APR is often used for fixed-term products, while APY is often used for flexible products where interest compounds.

- Always check which one you’re looking at. A 5% APR does not equal a 5% APY.

APR: The simple version

APR stands for Annual Percentage Rate. It's the simple interest rate on your deposit, just like in traditional finance.

If you deposit $1,000 at 5% APR, you earn $50 over one year. Linear, predictable, no compounding effect.

Where you’ll see APR: fixed-term savings, some loans, and products where interest is only paid at maturity.

APY: The compounding version

APY stands for Annual Percentage Yield. It includes compounding — interest earning interest — and it's another term crypto borrowed from TradFi.

If you deposit $1,000 at 5% APY with daily compounding, you earn slightly more than $50 — about $51.27.

Why? Because interest starts earning interest as soon as it’s credited.

The more frequently compounding happens, the closer APY gets to its true annual return — and the further it pulls away from APR.

Where you’ll see APY: flexible savings products where interest is credited regularly and remains in the account.

Important nuance

APR is exactly what you earn during the term because interest does not compound while the product is active. However, if you reinvest your principal and interest at maturity, your overall returns can still compound over time.

The gap between APR and APY

The difference might look small at first, but it compounds over time and scale.

Suppose you deposit $10,000 worth of crypto. Here's how your balance changes after five years:

5% APR (no compounding) — ≈ $12,500

5% APY (daily compounding) — ≈ $12,840

The gap after five years is about $340. Over ten years, it widens to nearly $1,500.

The bigger the deposit, the bigger the gap. On a $100,000 deposit over 10 years, daily compounding can produce roughly $15,000 more compared to simple interest.

Why this matters for your savings

Most people see “5%” and assume it means the same thing everywhere.

But a product advertised at 5% APR doesn't earn the same as one advertised at 5% APY. This difference often only becomes clear when you actually calculate returns.

- Flexible savings often quote APY. This means interest is credited regularly and compounds automatically (daily, weekly, or monthly, depending on the provider).

- Fixed-term savings often quote APR. Interest is calculated on principal and paid at maturity. It can also be reinvested if this option is available.

Neither is better — they just describe different mechanics and different use cases.

Different terms for different goals

Clapp uses both terms, depending on the savings product.

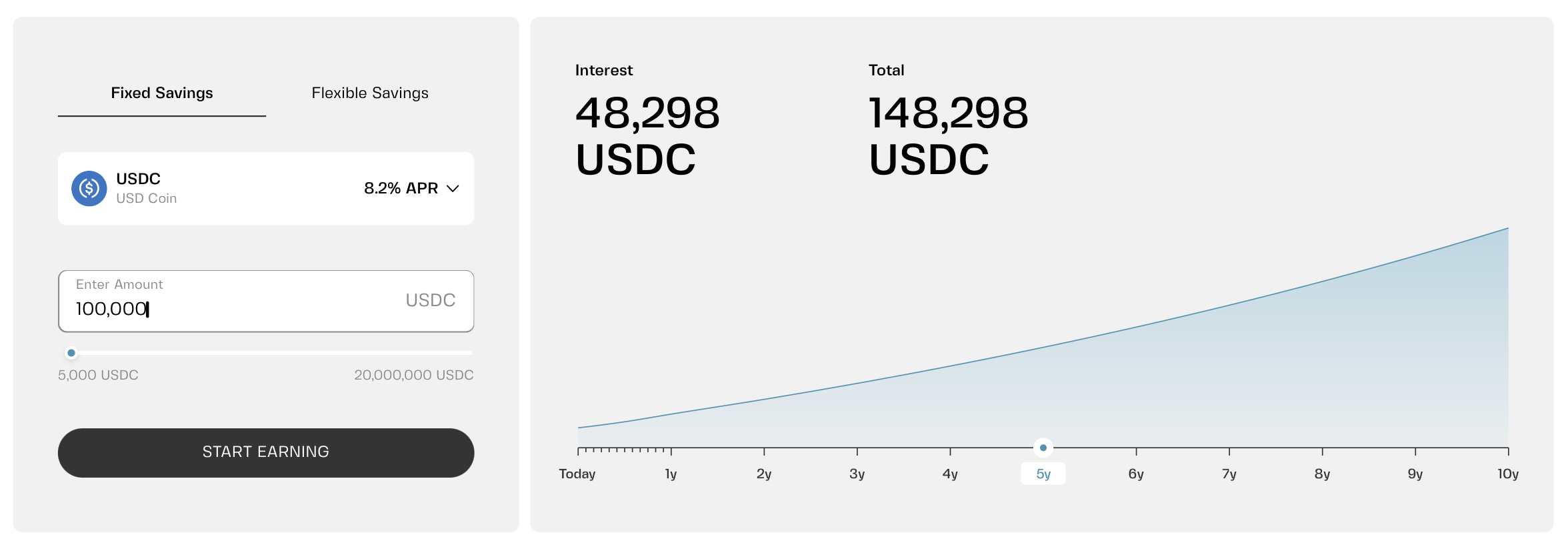

- Fixed Savings is advertised with APR. The rate is locked for your chosen term — 1, 3, 6, or 12 months — and interest is calculated on the principal only. No intra-term compounding. The higher rate (up to 8.2% APR) compensates for the lock-up.

- Flexible Savings is advertised with APY. Interest is calculated daily, credited to your balance, and starts earning its own interest the next day. That 5.2% APY includes daily compounding.

Fixed-term savings are designed for higher yield on assets you’re confident you won’t need in the near future. You commit your funds for a set period, and in return you typically receive a higher rate. The trade-off is simple: better returns in exchange for giving up flexibility until maturity.

Flexible savings are built for liquidity first. You can deposit and withdraw at any time, without penalties or lock-ups, while still earning yield on your balance.

Think of it as an “always-on” emergency fund — your money is available instantly if you need it, whether that’s to cover an unexpected bill, move into another opportunity, or add collateral to a crypto loan during a market downturn.

Comparing advertised rates

At first glance, you might wonder whether 5.2% APY is close to 8.2% APR.

It isn't. Even with daily compounding, 5.2% APY does not close that 3-percentage-point gap.

On $100,000 in USDC over a five-year horizon:

- 8.2% APR (paid annually, with interest reinvested each year) — $48,298 in interest

- 5.2% APY (daily compounding) — $28,848 in interest

Difference: ≈ $19,450

That doesn't make flexible savings products inferior. For many savers, that flexibility has real value. An emergency expense, a market opportunity, or a sudden need to add collateral to a crypto loan can all require immediate access to funds.

In those situations, earning a slightly lower yield may be a worthwhile trade-off for knowing your assets are always within reach.

In a nutshell

If you're comparing two products, always use the same metric.

- Compare APY to APY for products that compound.

- Compare APR to APR for products that don't.

- Don't compare APR to APY directly — they're not the same.

Rule of thumb. If you see APY, it already includes compounding. If you see APR, it doesn't. Compounding only matters if you leave your interest in the account.

Bottom line: 5% isn't always 5%

It depends on whether you're looking at APR or APY.

APR is simple. APY includes compounding. The difference grows with time and the amount you deposit.

Before you commit money anywhere, check which rate you're being offered and how interest is calculated. Then decide whether the product fits your goals.

A 5% APY with daily compounding will earn more than a 5% APR with no compounding. But a higher APR can still outperform a lower APY.

The key is to compare actual returns — not just the headline rate — and understand what the advertised number actually represents.

Frequently asked questions

1. Is APY always better than APR?

Not necessarily. APY includes compounding, so the number is higher. But the product itself might have different features — lock-ups, flexibility, or risk profile. Compare products, not just numbers.

2. Why do fixed-term products use APR?

Because the interest isn't compounding during the term. It's calculated on the principal and paid at maturity. APR accurately reflects what you earn when there's no compounding.

3. Does daily compounding really make a difference?

Over short periods with small deposits, the difference is tiny. Over years with larger deposits, it adds up. The more time and money you have, the more compounding matters.

4. How do I know if I'm being offered APR or APY?

It should be stated clearly. If it's not, ask. Always check the product description or terms before you deposit.

5. Which one should I choose for my savings?

It depends on your goals. Flexible savings (APY) gives you daily compounding and access to your funds. Fixed savings (APR) gives you a guaranteed rate for a set period. Many people use both: flexible for liquidity, fixed for higher returns on money they won't need soon.