Why your savings account is stealing from you — and what to do about it

Remember when savings accounts actually paid you to save?

Probably not. For most of us, the best we've ever seen is maybe 1% or 2% — or even 0.01%. You know what that means? On $10,000, you're earning one dollar. Per year.

Meanwhile, inflation is chipping away at your purchasing power. Your money is literally shrinking while it sits "safely" in the bank.

Your savings account isn't just failing you. It's quietly stealing from you.

TL;DR

- Your bank account is losing to inflation. At 0.01%–4% APY, you're barely keeping up. At 8% on stablecoins, you're actually growing your wealth.

- Crypto savings aren't magic — just more efficient. Fewer middlemen means more yield goes to you. Same basic concept as a bank account, just better rates.

- Flexible vs. Fixed savings. Flexible keeps you liquid. Fixed pays you more. Combine if needed.

- Risks exist, but you can manage them. No FDIC insurance means platform choice matters. Stick with regulated providers, institutional custody, and transparent terms.

- Start small, watch it compound. You don't need to move everything overnight. Drop a few hundred, see how daily compounding feels, then decide.

Let's run the numbers.

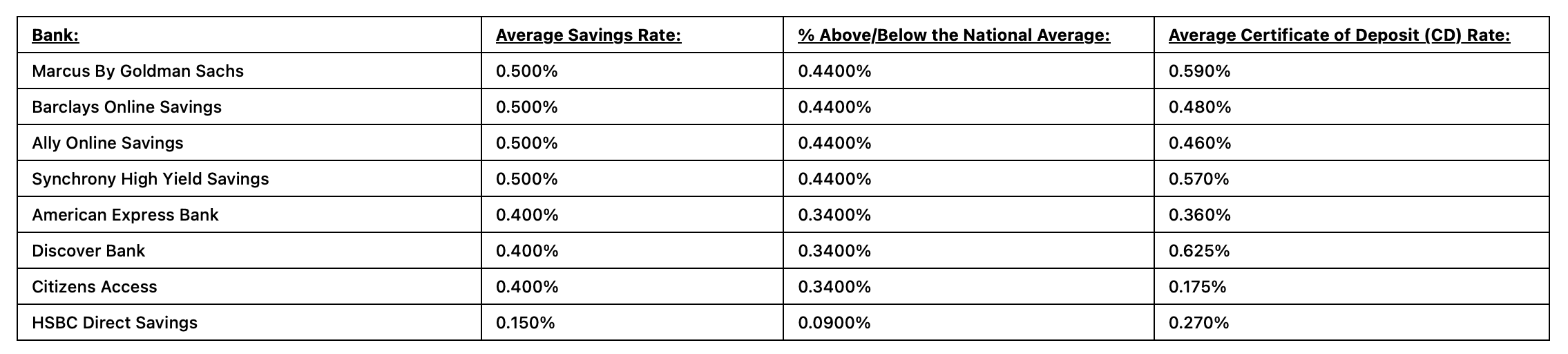

In the US, the national average for savings account is roughly 0.39% to 0.60%, while high-yield (HYSA) offers reach 4%. In the EU, top-tier easy-access accounts currently offer roughly 2.0% to 2.5% annually.

You have $10,000 sitting in a high-yield TradFi savings account. Let's be generous and say the interest rate is 4%:

- After one year, you've earned $400. Not great, but fine.

- Now factor in inflation at 3%. Your purchasing power is up about 1% — $100 in real terms.

If inflation is 3% and your savings account pays 1%, your real return is -2%.

Now compare that to a crypto savings account offering 5%–8% on stablecoins. Same $10,000.

- At 8%, you earn $800.

- After the same 3% inflation, you're up $500 in real terms. Five times better.

And there's more. In many countries, the bank pays you in dollars that then lose value. Crypto savings pay you in assets that often appreciate over time. You're not just earning yield — you're earning yield on something that might also go up in value.

The erosion happens slowly

Every year your money stays in a bank account, it buys less as the cost of everything from groceries to rent and clothing increases. You won't notice it month to month, and that's the trap.

A coffee that cost $3.50 last year might cost $3.70 this year. Your $10,000 from five years ago? It buys what $8,500 bought then. You've lost $1,500 in purchasing power — just by doing nothing.

The bank won't send you a letter saying "We've devalued your savings." They'll just keep paying you peanuts while inflation eats your lunch.

What makes crypto savings different

Crypto savings accounts work like a bank account — except the rates are higher.

How it works: You deposit stablecoins (or sometimes crypto like BTC, ETH) into a savings account. The platform lends them out, stakes them, or deploys them across DeFi protocols. A slice of the revenue comes back to you as interest. You do nothing.

Why rates are higher: In traditional banking, your money gets lent out, but the bank takes most of the profit. Crypto cuts out layers of middlemen. More of the revenue goes to you.

What you get:

- 5%–8% annually on stablecoins and fiat (vs. 0.01%–4% at a bank)

- Daily compounding — your interest earns interest, every 24 hours

- 24/7 access — no bank hours, no "3–5 business days"

- Flexibility — withdraw anytime or lock for higher rates

Two simple ways to earn

Not all crypto savings are the same. Here are the most user-friendly options that let you escape DeFi jargon or chasing yields across protocols:

Flexible savings: Perfect for emergency funds or cash you might need soon. Withdraw anytime without penalties. Lower rates, but your money stays liquid. On Clapp, that's up to 5.2% APY on stablecoins and EUR — with daily compounding and instant withdrawals.

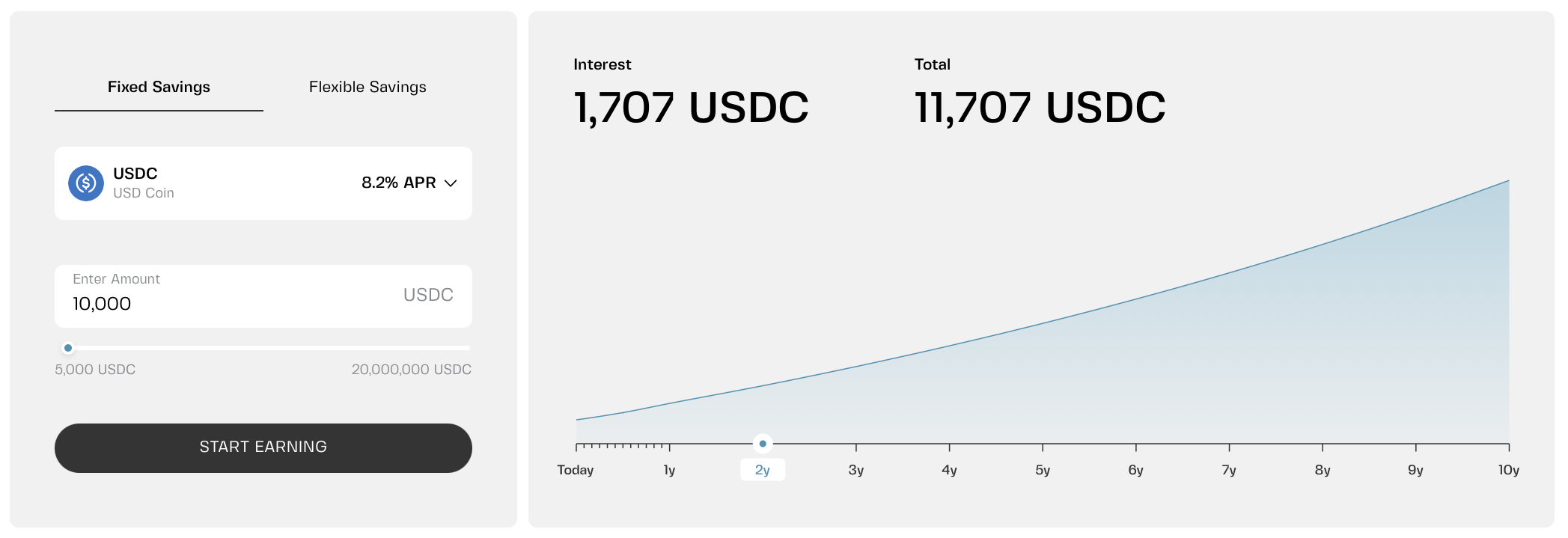

Fixed savings: Ideal for money you're confident you won't need. Just deposit, pick your term (1, 3, 6, or 12 months), and let the yield build. Higher, guaranteed rates in exchange for commitment — for instance, up to 8.2% APR on stablecoins and fiat.

APY includes compounding over time, while APR is a simple annual rate without compounding.

Many people do both: keep emergency cash in Flexible, lock long-term savings in Fixed.

What to watch for

- No FDIC insurance. A bank account is insured up to $250,000. Crypto savings aren't. That's why choosing a transparent, regulated platform matters. Look for licensed providers with institutional custody.

- Volatility still applies. If you're earning 6% on ETH but ETH drops 40%, you're still down. Stablecoins avoid this risk — they're pegged to the dollar.

- Platform risk. Not all providers are built the same. Do your homework.

- Taxes. Interest is usually taxable income in most countries. Keep records.

Your savings account is a storage fee

In TradFi, your savings account isn't really a savings account anymore. Your bank is playing by old rules that no longer serve you. You're paying it to hold your money while inflation quietly steals its value.

Crypto savings flip that model, allowing you to earn as your money grows and keep full control. It's just a smarter place to park your savings: earn real yield without complicated trading or lock-ups (unless you choose them).

No need to move everything overnight. Start with a portion of your emergency fund and see how it feels. Watch the daily compounding do its thing.

The money you save today should be worth more tomorrow, not less.

Frequently asked questions

1. Is crypto savings safe? How do I protect my funds?

It's safer than DeFi yield farming but riskier than a bank account. The key is choosing a regulated platform with transparent terms. Look for licensed providers, institutional-grade custody (like Fireblocks), and segregated accounts for user funds. A regulated platform is a lot safer than chasing 15% yields on unknown protocols.

2. What's the difference between Flexible and Fixed savings?

Flexible lets you withdraw anytime — no penalties or lock-ups. Perfect for emergency funds or cash you might need next week. Rates are lower because you're paying for that flexibility. Fixed locks your funds for a set term (1, 3, 6, or 12 months) in exchange for higher, guaranteed rates. Many people use both.

3. Can I lose my principal in crypto savings?

With stablecoins, your principal stays in the same asset — you're not trading, so no market risk on the principal itself. The main risk is platform failure. That's why choosing a transparent, regulated provider matters. Some platforms also offer fixed-term products where your rate is guaranteed. You won't lose your deposit to market swings, but you could lose access if the platform fails. Do your homework.

4. How does daily compounding work?

Most banks pay interest monthly. Crypto savings often calculate and credit interest daily. That means your earnings from today are added to your balance overnight, and tomorrow you earn interest on that larger amount. Over a year, daily compounding adds up to more than monthly or annual compounding — without you lifting a finger.

5. Do I have to pay taxes on crypto savings interest?

In most countries, interest earned on crypto is treated as taxable income — just like interest from a traditional bank savings account. The difference is that banks usually report your interest to tax authorities automatically. With crypto, you're responsible for tracking and reporting it yourself. The rules vary by jurisdiction, so check with a local tax professional.