Your interest earns interest. Your interest's interest earns interest. Mind blown yet?

You've heard the phrase "compound interest" before. But have you ever watched it happen?

Probably not. Most banks — and even some crypto savings platforms — pay interest monthly, and the amounts are so small you barely notice. A few cents here, a few dollars there. Who's checking?

But when your money earns interest daily, and that interest starts earning its own interest the next day, something shifts. It stops feeling like math and starts feeling like a slow-motion snowball.

Let's break down how compounding actually works, why daily compounding changes the game, and how much you might be leaving on the table.

TL;DR

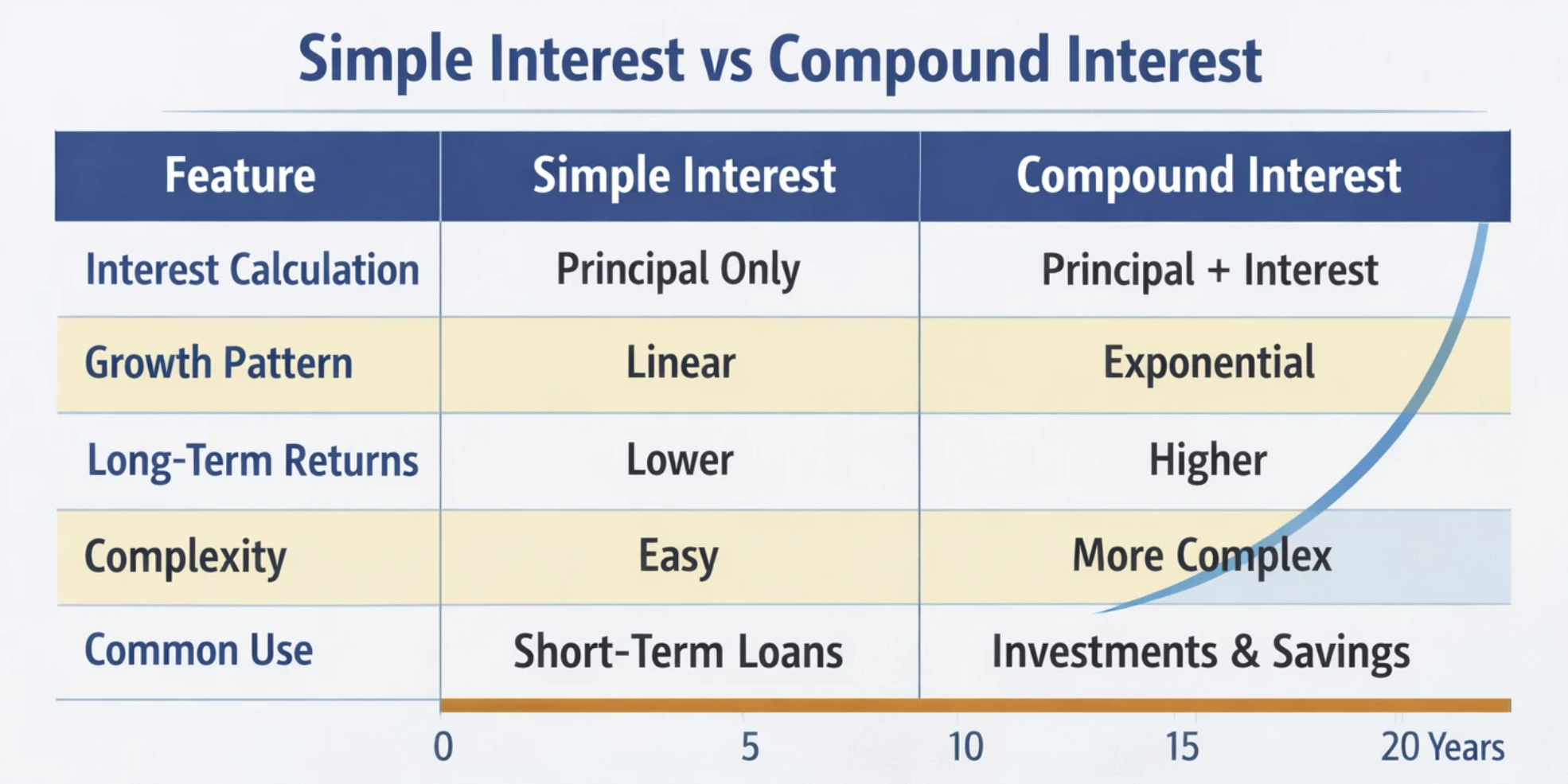

- Compound interest is interest earning interest. Your money grows faster because yesterday's earnings start earning today.

- Daily compounding beats monthly compounding. The more frequent the compounding, the faster your balance grows.

- Time is your biggest advantage. The longer you let it run, the more dramatic the effect.

- Small deposits add up. You don't need to be rich to benefit from compounding.

- Letting interest auto-compound is the lazy winner's move. Taking payouts slows the snowball.

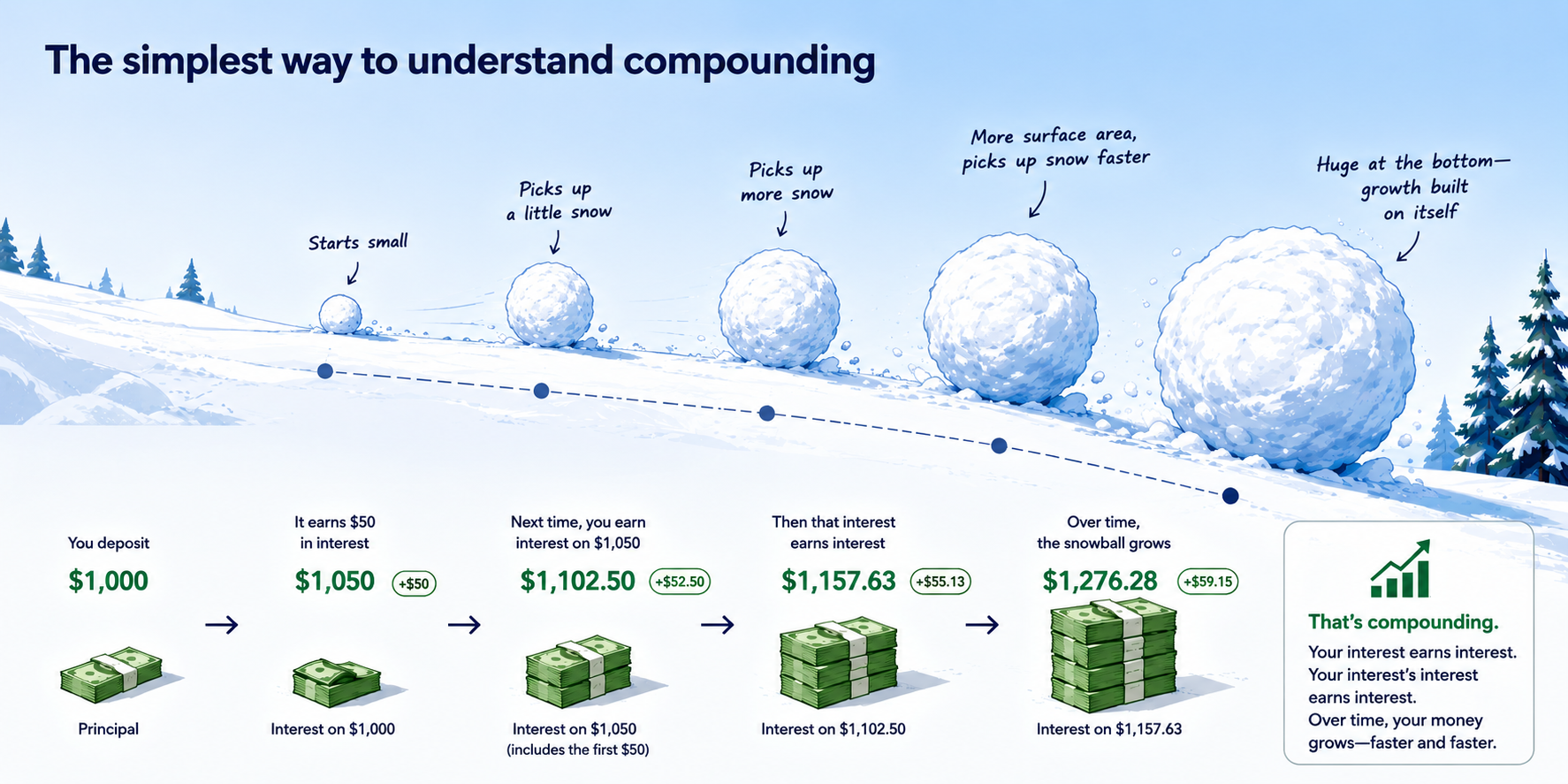

The simplest way to understand compounding

Imagine a snowball rolling down a hill.

At first, it's small. It picks up a little snow. Then a little more. As it grows, it picks up snow faster because there's more surface area. By the time it reaches the bottom, it's huge — not because it suddenly sped up, but because the growth built on itself.

Money works the same way.

You deposit $1,000 in a savings account or stablecoin yield product. It earns $50 in interest. Now you have $1,050. The next time interest is calculated, you earn interest on $1,050 — not just your original $1,000.

That extra $50 earns its own interest. Then that interest earns interest. Over time, the snowball grows.

That's it. That's compounding.

Why daily compounding is different

Most people understand compounding in theory. Fewer actually see what changes when it happens more frequently.

The difference between annual, monthly, and daily compounding isn’t dramatic over a few weeks. Even over a year, the difference can feel surprisingly small.

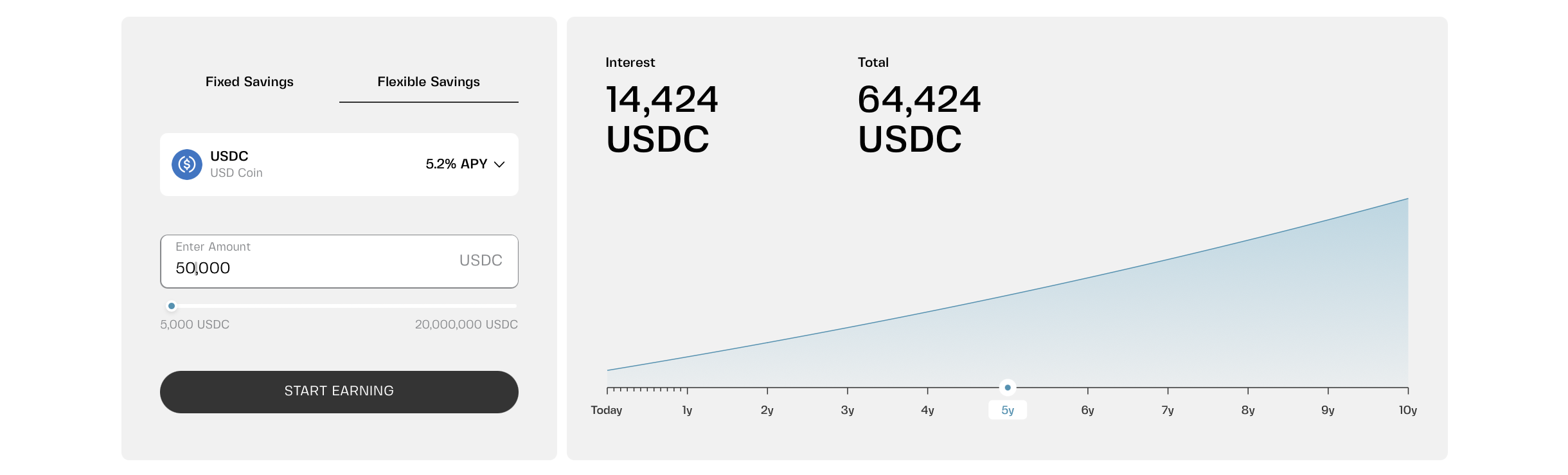

For example, on a $50,000 deposit at 5% APY, the gap after one year looks like this:

- Simple interest (no compounding): $52,500

- Daily compounding: ~$52,564

That $64difference is not a life-changing amount. It’s a few cups of coffee.

But the structure changes something more important: how growth behaves over time.

Now extend the same setup over longer periods, with regular contributions — say, adding $500 per month:

After 5 years:

- No compounding: ~$96,250

- Daily compounding: ~$99,100

The difference ($2,850) isn’t explosive, but it’s no longer negligible. The curve starts to separate.

And that separation continues quietly, every day, without any visible “moment” where it happens.

The real power shows up when you add regularly

Compounding alone is slow at first. What changes the trajectory is consistency.

Take the same example again:

- $50,000 initial deposit

- $500 added every month

- 5% APY

If you don’t rely on compounding, your growth is mostly linear. With daily compounding, interest is constantly reinvested. By year 5, you’re roughly $3,000 ahead, because each deposit starts compounding from its own point in time, creating overlapping growth curves.

That’s what creates the difference between simple growth and accelerating growth.

Compounding isn't about getting rich overnight. It's about giving your money enough time that the growth becomes self-sustaining. The snowball gets heavier, even if you're not watching it closely.

Why most people ignore compounding

Because it's boring. A 5% return on $1,000 is $50. That's dinner, not a yacht.

But $50 on $1,000 is the same percentage as $50,000 on $1,000,000. Same math, different scale.

The people who benefit most from compounding are the ones who start early and let time do the work.

Time is the multiplier you can't buy.

The rule of 72 (simple and useful)

Want to know how long it takes your money to double at a given return rate? Use the Rule of 72.

72 ÷ APY = years to double

The key detail: this works with APY, which already reflects compounding (whether it’s daily, monthly, or continuous). That means it still applies even if your interest compounds daily — as long as you're using the effective annual rate. This is commonly used for both traditional finance and crypto yield products quoted in APY.

For example:

- At 5% APY: 72 ÷ 5 ≈ 14.4 years

- At 8% APY: 72 ÷ 8 ≈ 9 years

No calculator needed. Just a quick mental shortcut for long-term growth.

The auto-compounding advantage

You have two options:

- Have your interest added to your balance automatically (auto-compound)

- Take interest payouts to your wallet (cash out)

Option 1 lets you earn interest on your interest. Option 2 stops the snowball.

The difference is small at first. But over 10 years? The snowball grows.

You don't need to be a math genius — just start

- Park your cash in a savings account that compounds daily. Even 5% is better than 0.01% at a bank.

- Add regularly. Small, consistent deposits beat large, one-off deposits over time.

- Don't cash out your interest. Let it ride. That's where the magic happens.

- Be patient. Compounding is slow until it isn't. Then it's unstoppable.

The bottom line

Compound interest isn't magic. It's just math that most people ignore because the results take time.

But time passes anyway.

You can let your money sit idle, earning nothing. Or you can put it to work, let the snowball roll, and watch it grow — slowly at first, then faster than you expect.

Your interest earns interest. Your interest's interest earns interest. Mind blown yet? Maybe not. But give it a few years? You'll see.

Frequently asked questions

1. Is daily compounding really that much better than monthly?

Over short periods, the difference is tiny. Over years with regular contributions, it adds up. Daily compounding beats less frequent compounding. Take it if you can get it.

2. Does compounding work the same for stablecoins and volatile crypto?

For savings accounts (stablecoins, EUR), yes — the interest is predictable. For staking or lending, the APY fluctuates, so compounding is based on variable returns. Same math, different input.

3. Should I take interest payouts or let them compound?

Let them compound unless you need the cash flow. Every dollar you take out stops earning. That's fine if you need the money. But if you don't, leave it in.

4. How much do I need to start?

Almost nothing. On Clapp, Flexible Savings starts at $10 equivalent. The habit matters more than the amount.

5. Is compounding worth it for small amounts?

Yes. The percentage works the same whether you have $100 or $100,000. The only difference is the dollar amount. Starting small beats not starting at all.