Your 2026 guide to smarter crypto borrowing

Crypto credit products are a pillar of the digital asset economy. Instead of selling their holdings, users can borrow against them — unlocking liquidity while keeping exposure to potential gains. This serves long-term holders, unlocks instant capital, and expands financial access.

Here is a look at how crypto credit has evolved, and why flexible products are becoming the go-to tool.

From loans to credit lines

The crypto borrowing ecosystem centers on accessing liquidity via collateral. Users pledge crypto to borrow fiat or stablecoins, receiving their assets back once the loan is fully repaid.

Early crypto loans had rigid terms, but the landscape has grown far more sophisticated. Today, products range from simple fixed-duration loans to versatile credit lines:

- Fixed-term loans: Traditional loans with a set duration and repayment schedule.

- Crypto credit line: A revolving facility that allows repeated borrowing up to a limit, without fixed monthly payments or loan terms.

- Flash loans: Uncollateralized DeFi loans that must be repaid within one transaction.

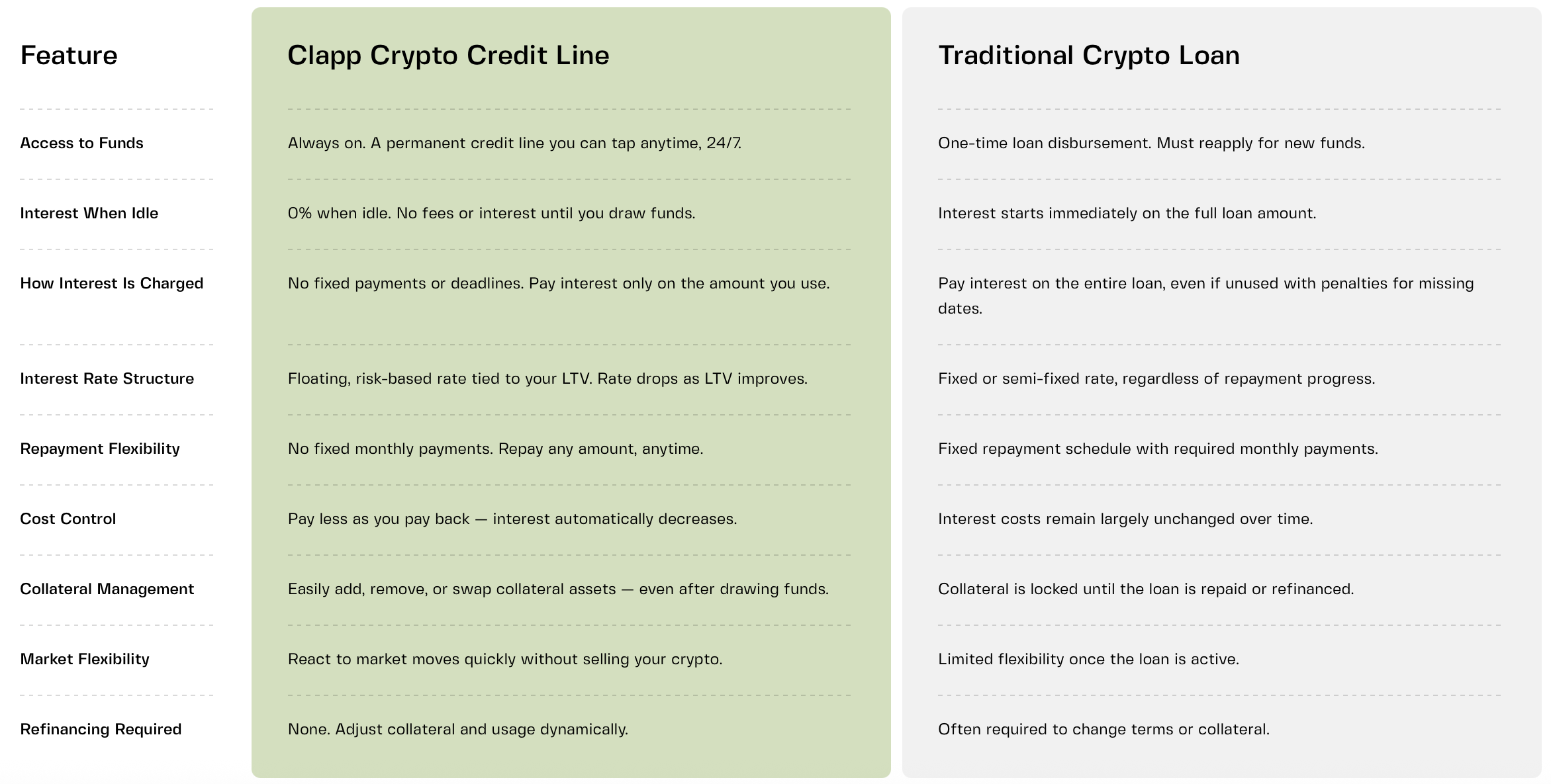

A crypto credit line works like a financial safety net: you get a pre-approved limit, draw only what you need, and pay interest exclusively on the utilized amount. There's no term expiry, and you can repay and redraw at will. Multi-collateral products allow users to combine several assets as collateral and rebalance them at any time.

Borrowing basics: Loans & credit lines

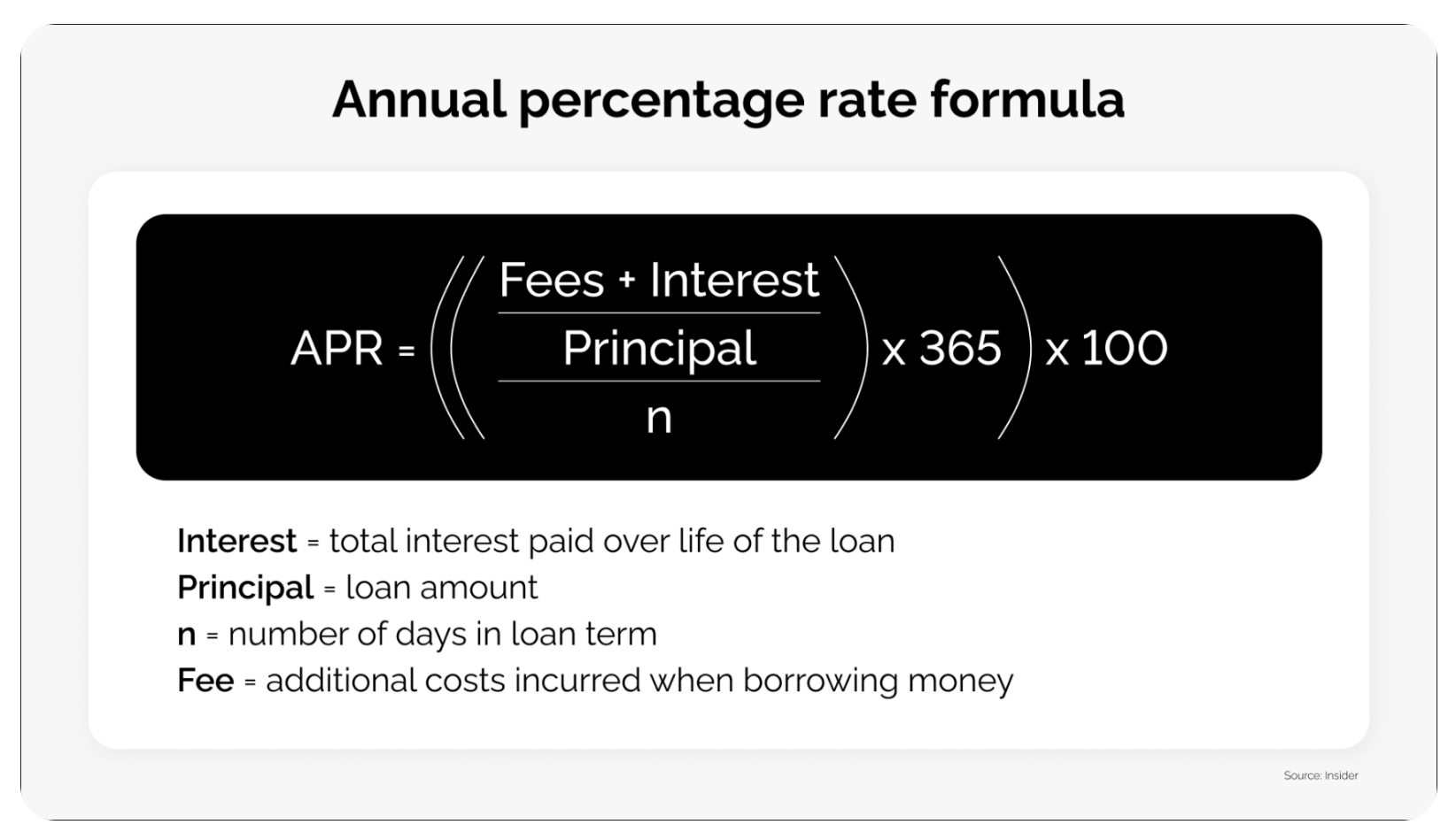

Borrowing resembles conventional loans, but with an important twist designed to protect lenders from volatility. At a high level, the mechanics are familiar: you borrow against collateral and pay interest, typically expressed as an Annual Percentage Rate (APR). For flexible credit lines, APR applies only to the amount drawn.

- Deposit your crypto to use as collateral (typically BTC or ETH) to withdraw a percentage of its dollar value in cash or stablecoins.

- Pay interest on what you borrowed, often in regular intervals (e.g., weekly or monthly).

- Receive your collateral back upon full repayment.

But wait... what about volatility?

Lenders want stable collateral — when approving a mortgage, a bank assumes the house will likely hold or increase its value. Meanwhile, BTC can still plunge 10% overnight, and altcoins often experience even greater swings.

What happens if the value of your collateral drops below the borrowed amount?

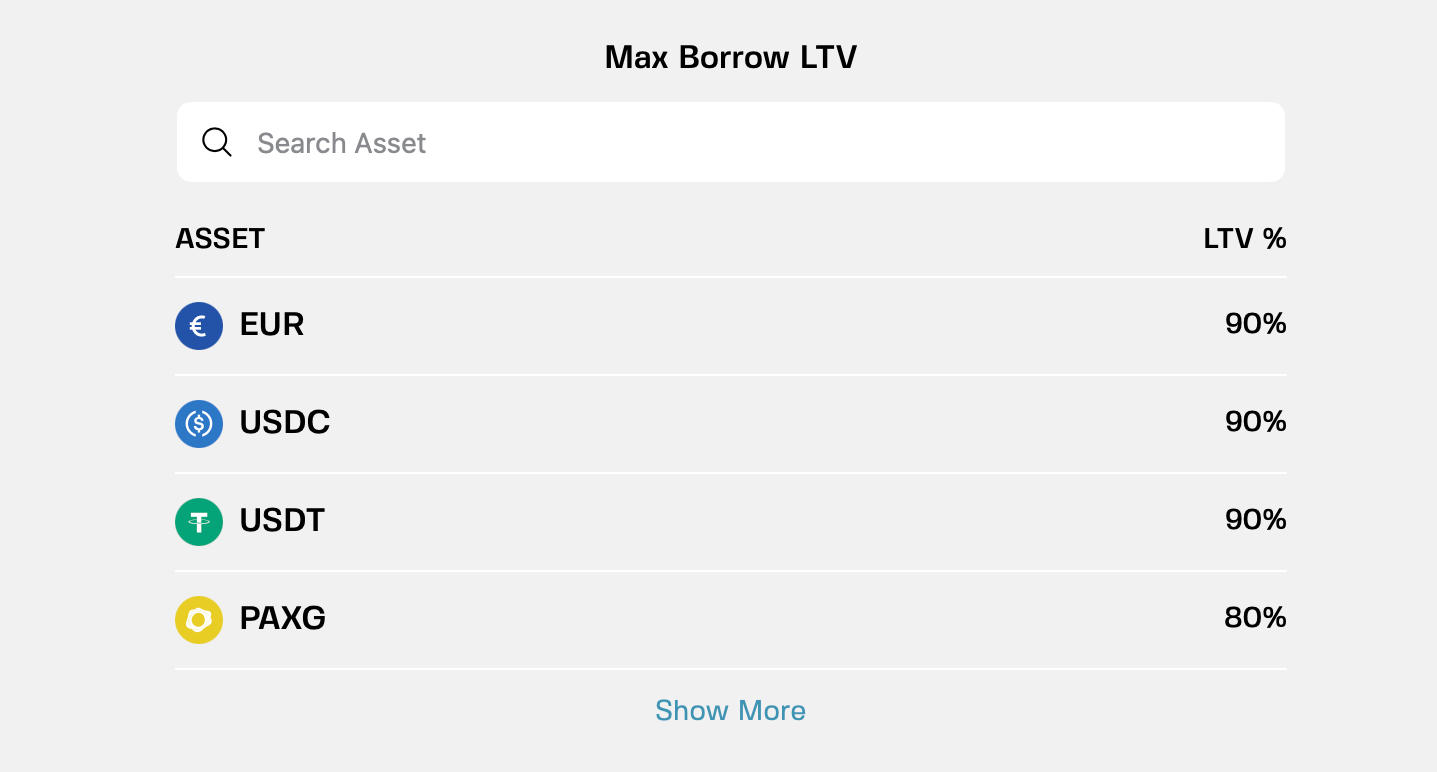

This is where loan-to-value (LTV) ratios come into play. LTV acts as a buffer against volatility, ensuring there is sufficient collateral backing the loan at all times.

Understanding loan-to-value ratio (LTV)

The loan-to-value (LTV) ratio remains key — it determines how much you can borrow. It is calculated as the amount borrowed divided by the value of the collateral, expressed as a percentage:

(Loan amount ÷ value of collateral) × 100 = LTV

Typically, an LTV of 50% is an entry-level starting point. That means if you deposit 2 ETH as collateral when ETH is worth $3,000, you can borrow up to $3,000 — half of the collateral value.

Responsible platforms reward lower LTVs with incentives such as reduced interest rates or 0% APRs, encouraging prudent borrowing.

As crypto prices fluctuate throughout the loan duration, so does the LTV. That's why crypto lenders enforce a maximum LTV threshold — if this limit is breached, collateral may be automatically liquidated to repay the loan.

Most platforms warn users when their LTV approaches this limit, allowing time to top up collateral or repay part of the loan before risking liquidation.

Key terms to know

- Collateral: Assets pledged to secure borrowing (exceeding the loan amount). In advanced systems, users can combine multiple asset types as blended collateral and adjust them at any time.

- LTV (loan-to-value): The ratio between borrowed funds and collateral value. Lower LTVs provide a larger buffer against market volatility.

- Annual Percentage Rate (APR): The annualized cost of borrowing — commonly, 8%-16% for fixed-term loans on large CeFi platforms. APRs may be fixed (set for the duration) or variable (adjusting based on market conditions).

- Margin call: An alert issued when collateral value approaches the maximum permitted LTV, typically around 70–85%.

- Liquidation: Occurs when collateral value falls too close to the loan value. Modern platforms often provide early warnings and flexible top-up options to help you avoid this outcome.

What are flash loans?

Flash loans are a powerful but highly technical tool, most commonly used by advanced traders for strategies such as arbitrage — buying an asset on one exchange where it’s undervalued and selling it on another where it’s priced higher.

- The entire process — borrowing funds, executing a transaction, and repaying the loan plus a small fee — must occur within a single blockchain transaction.

- If repayment fails, the transaction is automatically reversed, protecting the lender from loss.

While flash loans showcase the programmability of DeFi, they are generally irrelevant for everyday borrowers seeking longer-term liquidity solutions.

CeFi or DeFi lending?

Centralized (CeFi) platforms typically offer a user-friendly experience, custodial services, and customer support. Decentralized (DeFi) lending enables self-custody with rules enforced by smart contracts, but comes with smart contract risk and no human support if liquidations occur.

Benefits of crypto credit solutions

Crypto credit emerged to address limitations in traditional finance, offering faster access to capital without credit checks or lengthy paperwork.

Key benefits include:

- Liquidity without selling: Access cash without selling crypto and missing potential upside.

- Tax efficiency: In many jurisdictions, borrowing against crypto does not trigger a taxable disposal event.

Early platforms like Salt Lending popularized the concept by enabling fiat borrowing against crypto collateral. Beyond fixed-term loans, innovation has increasingly shifted toward flexible credit solutions.

Credit lines provide liquidity on demand, eliminate rigid repayment schedules, and allow borrowers to fine-tune positions as market conditions change.

Flexible credit lines in practice

Clapp’s credit lines turn static collateral into an active financial tool, emphasizing flexibility and user control:

- No fixed repayments: Borrowers repay on their own timeline.

- Multi-collateral support: Use a diversified basket of assets as collateral.

- Dynamic management: Add, remove, or rebalance collateral even after borrowing.

- Cost efficiency: Pay interest only on utilized funds; at lower LTVs, rates can be as low as 0% APR.

Such revolving credit facilities let users draw funds as needed, pay interest only on what they use, and manage collateral in real time — without the rigidity of traditional loan structures.

Things to consider

Despite its flexibility, crypto-backed borrowing also carries risks — primarily market volatility affecting collateral values.

Best practices include:

- Borrow conservatively, leaving room to add collateral if markets move against you.

- Maintain a prudent LTV and use platforms with transparent alert systems.

- Ensure your lender uses a reputable custody provider to safeguard collateral.

- Favor modern platforms that allow real-time collateral adjustments rather than locking users into static loan structures.

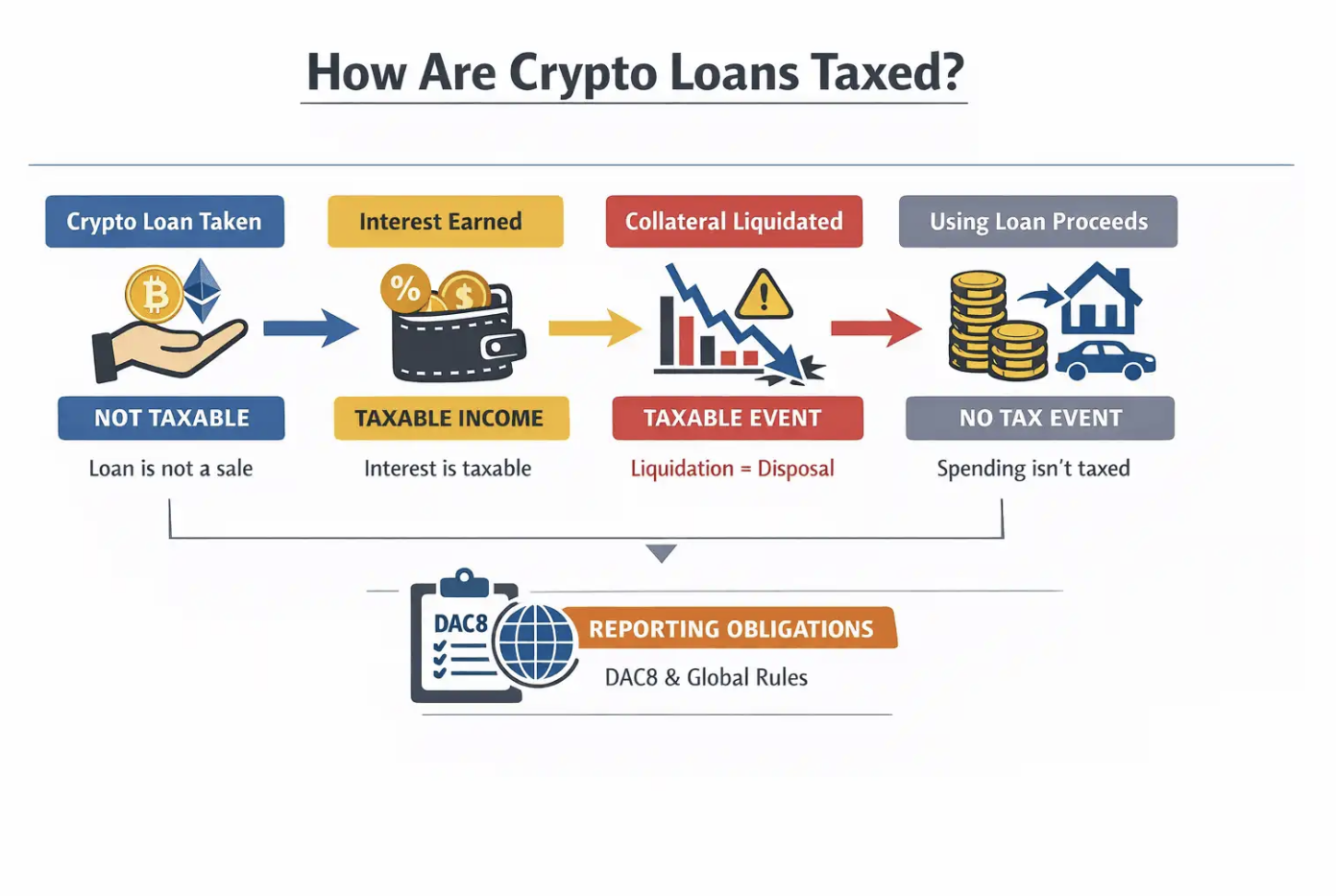

When borrowing may trigger a taxable event

Borrowing against crypto is generally not a taxable event, but taxes can arise depending on how the loan is used and how it ends.

- Forced liquidation is the primary risk: many tax authorities treat it as an involuntary disposal of the asset. In the UK, for example, the HMRC provides worked examples showing how gains are calculated when collateral — including any liquidation penalties — is sold to cover a loan.

- Using loan proceeds is typically tax-neutral, but downstream actions matter: buying another asset establishes a new cost basis, and any later liquidation of the original collateral is usually where the tax liability crystallizes.

- Rules vary by jurisdiction — the US treats digital assets as property with taxation focused on dispositions, the UK provides detailed DeFi and lending guidance, and in the EU, DAC8 will require in-scope providers to begin collecting reportable data from January 1, 2026.

Closing thoughts

Crypto credit has matured from simple fixed-term loans into sophisticated liquidity solutions. For users who prioritize flexibility and control, modern credit lines increasingly represent the future — on-demand capital without the constraints of traditional borrowing.

As the ecosystem continues to develop, choosing a transparent, secure, and user-centric platform is essential for leveraging your assets wisely. And, as with any financial tool, consulting local tax guidance is a prudent step when using crypto-backed credit.